Good morning, it's Paul here with Thursday's SCVR.

Estimated timings - I'm working early today, so should be finished by 1pm official finish time.

Edit at 12:20 - I need a break now, as my eyes are struggling after looking at screens since 6am. Will finish off the last 2 company sections after lunch, so revised finish time of 3pm.

Edit at 14:21 - today's report is now finished. I've dropped LOOK from the list, because it doesn't interest me, and I've got something more important to do some work on.

Preamble

Judging from the positive comments and much higher thumbs ups here, you seem to like it when I do more general market commentary, that seems to be what you want! Therefore I'm refocusing on doing more of that, when there's something interesting to say, and spending less time on those company results that I find uninteresting. I'll still be doing the deeper looks into companies of interest. That suits you, and suits me too!

CNBC - Given that we're living in unique times, Graham and I should be covering the more general economic situation & outlook. As one commentator on CNBC (which I have running in audio in the background, all afternoon/evening) said, this is the first ever "engineered collapse of the economy" - a very apt phrase I think. Jim Cramer drives me up the wall, trivialising the subject matter, and I can't even understand what he's saying a lot of the time, but many of the other CNBC commentators are excellent. Above all, it guides me as to the big picture in the USA, and I've made good money from soaking up news & views on CNBC.

Yesterday was a good example - I woke up to another thumping great loss on my Dow short, with it up about 200 points pre-market. It soon became clear to me that, even though this was supposed to be a hedge, I couldn't take any more pain on it, and the market seemed likely to keep going up. So I banked the loss, closing my short, flipped it round and went long instead, By the close of play, the Dow was up 500 points, and I'd recouped all my previous loss. When it ran out of steam, I closed the long just before the closing bell at 9pm UK time, and went short again - as I really do want a hedge against my UK longs.

Why am I mentioning this? To reinforce a point from yesterday's report, namely that I'm learning to take losses sooner. With this kind of trading, it's better to just drop our preconceptions on what we think the market should be doing, and instead just observe & follow what it is actually doing.

The same thing happened with Zoom $ZM (as also mentioned yesterday). The market wants to take it higher, and there's no doubt it is a phenomenon. I used it again last night for a business meeting, and again it works brilliantly. I'd be happy to pay say £10 per month for it, although my account is free at the moment. Therefore it was crazy being short of it, which I realised, and took the loss, flipped it round & went long, at 3 times the original position size. Thankfully, that action recouped all my shorting loss yesterday, as it continued rising. The most recent accounts look very promising too. Note that the apparently amazing cashflow is actually largely driven by increased customer cash paid up-front. I think the valuation probably can be justified, looking at the stellar growth, and the future guidance. Hence I'm planning on remaining long, even though the valuation does look nuts at first sight.

Dow Jones Index (DJIA) - Why on earth is the Dow now up at over 26,000, having bottomed out at c.18,500 only just over 2 months ago? As one CNBC commentator aptly put it;

The cyclical trade is overwhelming the covid trade.

In other words, economic data is starting to improve, as the economy re-opens. The market doesn't seem to care that the figures are still horrendous. Vast Govt stimulus is (so far) preventing economic meltdown, but at a huge price.

The re-opening information I'm hearing is generally better than expected. Recent examples are;

Cheesecake Factory $CAKE - rose 16% yesterday on reports that;

* CHEESECAKE FACTORY INC - REOPENED CHEESECAKE FACTORY RESTAURANTS HAVE RECAPTURED, ON AVERAGE, APPROXIMATELY 75% OF PRIOR YEAR SALES LEVELS

I think that's a remarkably good statistic, given that the restaurants it has re-opened, are doing so on limited capacity - i.e. tables spread out for social distancing, etc. This shows that enough people are happy to go back to restaurants, to make them appear to be viable again. That's assuming the 75% level can be further improved upon. The fear was that it would be much lower than that, forcing restaurants to close again as being economically unviable. Maybe we could go from a surplus of restaurant capacity, to a shortage, requiring that people have to book in advance, and dine out on days/times that may not be ideal. Prices could go up, if capacity constraints meet strong consumer demand to eat out again. I'm itching to visit my favourite restaurants again, and will be tipping generously to help them get back on their feet.

Reports are that in Germany, restaurant bookings have started again, and are amazingly high - almost at pre-covid levels.

Therefore, perhaps we should look again at the hospitality sector, and price in a decent recovery?

Retail re-opening happens here in the UK on 15 June, and share prices seem to be anticipating a successful resumption of retailers' trading. Which is great news for my portfolio, as I'm heavily slanted towards that outcome. As mentioned yesterday, I've been selectively buying retailers, and my retail property REITs have been stunningly good performers, esp. Hammerson (LON:HMSO) . I've decided to run with that one, rather than banking the profits. I looked at its website, and it owns many decent shopping centres. With re-financed tenants (some of them anyway), and a (hopefully) strong resumption of retailing from 15 June, then this share could have further to recover.

Overall then, whilst I still don't expect a V-shaped economic recovery, it is looking increasingly likely that the economic recovery could be faster & stronger than I previously thought. That's what the stock markets are telling us, very strongly, as is other data. Better to run with the trend, than to constantly complain about how bonkers it is - after all we're in this game to make money, not to be proven right about our hunches. I'm disciplining myself more these days to search for, and act on facts & figures, rather than my hunches. Put the two together, with an open mind that you're readily able to change quickly when the facts change, and it's surprising how much better the results are.

Investor Meet Company

Just to flag up a new website that looks useful for investors. It does online webinars for listed companies. I watched the recorded video it did for Cloudcall (LON:CALL) (in which I hold a long position), and it was fine - a useful update from the company, and investors can submit questions.

I like what Investor Meet Company, in that when you register, you can set up a watchlist (yes, another one! Wouldn't it be nice if we only had to maintain one watchlist, instead of about 6 of them on various websites), to request which companies you would like to provide webinars on this platform. What a good idea! IMC can then approach companies, where there's a lot of investor interest, and persuade them to engage with investors using their platform.

As usual, I have no connection with this website, am just flagging it up as it looks useful, and is free.

In a similar vein, Primary Bid seems to be gaining traction. The concept here is to allow private investors to participate in placings. The problem in the past was that it only seemed to be used by very low quality companies, who were desperate for money. That's completely changed now, with some better & much larger companies using it. Amazingly, large cap Compass (LON:CPG) recently included Primary Bid in its fundraising.

The only drawback I've seen is that there's no price given for the fundraising. Why would anyone put in an order, without knowing what the price is going to be?! When I've taken part in placings in the past, my broker finds out the price, as obviously that is the key determinant in whether I would want to buy in the placing or not. I'm not sure how PB gets round that? Using a conventional broker, one can submit bids in a placing at various price levels. E.g. 50k shares if the price is 100p, 75k shares if it's 90p, and 100k shares if the price is 80p, etc. That's quite a good way of doing it. I'm not sure if PB has that facility. Has anyone used Primary Bid? If so, I would be very interested to hear your experiences of it. Looks a great concept though.

.

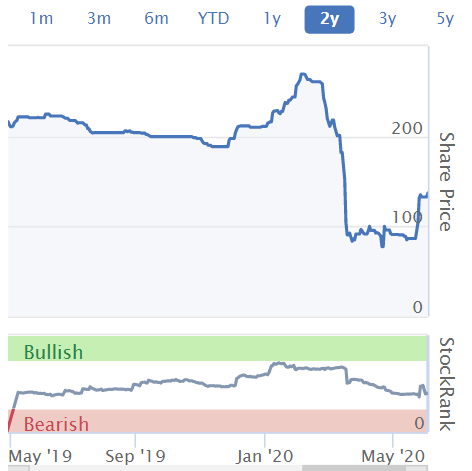

Intercede (LON:IGP)

Share price: 76p

No. shares: 50.5m

Market cap: £38.4m

(I hold a long position in this company at the time of writing)

Zoom call with management

My usual 6-monthly results meeting with IGP management had to happen online, instead of in person. Zoom to the rescue, which worked great. I tend to prepare beforehand, and just do Q&A, rather than ploughing through a presentation pack. This saves time for everyone.

Q1. Why were receivables on balance sheet so high at year end (about half of full year revenues).

A1. Per RNS of 31 March 2020, a $4.6m order was received at the year end, as expected. That was billed, and hence in receivables at year end. Funds received now, so receivables have normalised.

Q2. Is the year end cash balance an unusually favourable level?

A2. The CFO ran me through how the company's cashflow worked, and I was satisfied that the year end figure is not an unusual spike. In fact, as noted in the recent results announcement, year end cash of £4.7m was augmented by £3.7m received on 1 May 2020 - this is the big debtor referred to above - i.e. invoice raised on contract renewal date of 31 March 2020 (year end date), cash received a month later.

Q3. Will the company be applying for Govt-backed loans re covid?

A3. Have looked into it. Applications have to demonstrate that covid has caused financial problems. Since Intercede has only experienced a small impact, just some small delayed orders, and the sales pipeline is strong (up 40% on last year), then the company doesn't qualify, and doesn't need the money anyway.

Q4. We discussed the convertible loans.

A4. These should be gone in about 18 months, mixture of repaying some, others converting into equity - fairly small dilution. Balance sheet will look much better once these are gone, and it might arguably remove a brake on the share price. Depends how the market sees it. The company is in control of the situation, now that it has enough cash to repay them in full - much better situation than 2 years ago.

My opinion - I'm really pleased with how this investment is progressing. The original 3-year turnaround plan was summarised as: crawl, walk, run. I.e. there was a lot to sort out across the business, which has been done. The focus now, at the start of year 3, is driving revenue growth, having fixed everything else. The sales pipeline being up 40% Y-on-Y is a good leading indicator in my view. It's now all about execution. The only fly in the ointment is that customers may be reluctant to sign contracts, given the macro situation. Intercede can't control that, so if delays happen (as they did in the last week of March), because customers were not available being in lockdown, then we just have to live with temporary problems like that. Overall though, Intercede seems to have been largely unaffected by covid, which is very pleasing indeed. It shows the strength of the business model, which is largely recurring/repeating revenues, for mission-critical software, very long-term, in large organisations.

As I concluded at the meeting, everything sounds good, now you've got to deliver revenue/profit growth. Management agreed. Let's see what happens over the next year.

Here's the 10-year chart, which gives a nice idea of price upside, once growth kicks in (as it did briefly a few years ago). Since then, revenues have ticked along at about £10m pa.. In the last 2 years, the CEO has stripped out a lot of cost, so the business is now profitable (run rate of about £1-2m, once the big finance charge relating to the loan notes disappears in 18 months time) at this level. The excitement is what happens when revenue growth kicks in. Operational gearing is extremely high, hence the opportunity is for profits to soar, if strong revenue growth can be achieved in the next few years. Which may, or may not, happen. Having delved deeply into the business model & strategy, I think there's a better than 50:50 chance of the company achieving good growth in future. Time will tell if I'm right or wrong.

.

.

Loungers (LON:LGRS)

Share price: 133.5p (up c.1% today, at 10:05)

No. shares: 102.4m

Market cap: £136.7m

This is a chain of all-day cafe/bar/restaurants.

It secured a refinancing recently, so we know the business is financially secure well into 2021.

Today I'm mainly interested in its re-opening plans, and adapting the business model to the new covid world. Remember that a lot of this covid stuff might only be temporary, if treatments and ultimately a vaccine, might make all this stuff redundant. Or it could come back with a vengeance in a second wave, it's all unknown at this stage, making our ability to assess shares much more uncertain than in the past.

Historically, human ingenuity has resulted in practically all problems being overcome, or at least reduced to a manageable level. The economy always recovers. Therefore the logical stance is to be optimistic about the long-term.

To summarise;

Details given of ongoing staff engagement & consultation during furlough

Consultation with customers shows 98% say they would be comfortable to come back when Govt allows re-opening. Although bear in mind the survey was done from the most engaged customers, so that might not be representative of the population as a whole. Although it is a very positive indicator I think, and confirms what I was saying above about the sector generally bouncing back potentially better than people currently imagine.

Takeaway food & drink - 17 sites already opened for takeaways, further 10 opening on this basis this week. Has been a big success, and could provide an additional revenue stream in future. For me, this is a very important point. I've observed with local businesses, the restaurants that have embraced takeaway, are doing a roaring trade here in Bou'mth (e.g. El Murrino). Whereas the ones that have closed, with now dirty windows, and not even a notice in the door informing customers of what's going on (e.g. Piccolo Italia) are a stark contrast. The ones I mention are the 2 best Italian restaurants here in Bou'mth. The one that embraced takeaway is surviving & prospering. The one that didn't looks finished - surely if they were intending to re-open, they would have cleaned the windows, maybe painted the facade to freshen it up, and put big notices in the windows saying "re-opening soon!"? As always, the business owners that fight for survival, and adapt/innovate are going to come through this crisis with a lot less competition. Crises/recessions usually sow the seeds of future success for the best businesses.

Ordering app - will be trialled when they re-open, so people can order from their table.

Cashless - will also be trialled.

Smaller menu & more physical distancing in kitchens.

Re-opening in July, subject to Govt approval, but this date is seen as likely (I've heard that from other sector management).

Revised layouts, removing some furniture to space out tables.

...Due to the size and layout of the majority of our sites and the spread of our trade across the day parts, we anticipate being able to trade profitably with distancing rules in place. [Paul: very important point]

There is, however, a marked difference between 1 metre and 2 metre distancing, and if 2 metres is implemented, it may not make sense to open a small number of our more compact sites immediately.

The size of cafe/bar/restaurant sites is a vital point. There's a considerable advantage for operators of larger bars. They should be better placed to trade profitably with social distancing. Whereas small sites would have to remove most of the tables, and hence be uneconomic. If the Govt (likely, I reckon) reduces the distancing from 2 metres to perhaps 1.5 metres, then after a face-saving delay, down to 1m, then that would be very good for this sector.

Remember also that many smaller operators probably won't re-open at all. Hence there's likely to be loads more market share for the bigger operators like this one.

Repairs & maintenance being done during closure period - very sensible. Customers like refurbs, and are likely to return more readily to newly freshened up bars.

Adapting design of sites

My opinion - this is a useful update, and I think demonstrates how a strong operator uses a crisis to make its business better.

I suspect this share could continue its recovery. The unknown factors are;

1) How strong trading is going to be once re-opening is allowed (I'm fairly positive about this), and

2) How much damage a second wave of covid in the autumn might wreak.

The question for investors, is to weigh up the risks, with the potential upside, and decide whether it stacks up to buy now, or not.

.

.

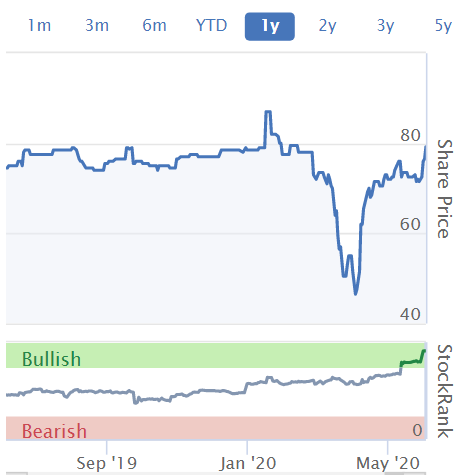

Luceco (LON:LUCE)

Share price: 122p (up 16% today, at 11:20)

No. shares: 160.8m

Market cap: £196.2m

Luceco plc ("the Group"), the manufacturer and distributor of high quality and innovative wiring accessories, LED lighting and portable power products...

Trading has improved since last update on 23 April.

Revenue was down 10% in Q1, due to covid-related supply chain issues, now resolved.

Revenue in Q2 (Apr-Jun) expected to be 25% down on 2019 - seems relatively good to me, given that many customers must have been in lockdown.

Profitability - this is amazing, and seems almost too good to be true in the circumstances. Stringent overheads reduction is cited;

Expecting H1 2020 Adjusted Operating Profit to be at least in line with H1 2019 (£7.2m), with double-digit Adjusted Operating Margin.

Cash generative in H1.

No new bad debts.

Net debt should be similar relative to EBITDA as last year.

Outlook - some uncertainty still.

Although the performance to date has been encouraging, macro uncertainty continues to prevent us from offering full year guidance. New guidance will be given as soon as it can be reasonably assessed.

My opinion - I'm flummoxed by this update. Even with cost-cutting, I don't see how it's possible to side-step the economic crisis that we're currently in. Maybe the impact could have been deferred into H2 in some way?

I'd like to see the H1 accounts, and have a good rummage, before being convinced that everything is as positive as the company says it is today.

.

Elecosoft (LON:ELCO)

Share price: 79.2p (up 3.5% today, at 13:51)

No. shares: 82.2m

Market cap: £65.1m

This company sells project management software, and is something I have a positive impression of, that we've commented here favourably about for some time. See my notes here on 11 May 2020 to get up to speed, where I reviewed the 2019 numbers, and the last trading update. I felt the price was up to speed with events at 77p, similar to today's price.

Today, we have;

Trading update for the four-month period ended 30 April 2020

Key points;

Revenues down only 3% vs 4m in 2019 - very impressive

Profit before tax up 25% - even more impressive!

Net cash of £3.1m at 30 April 2020 (up £2.0m in last 4 months)

Outlook - nothing said.

My opinion - this is a really impressive update in the circumstances.

It's worth remembering how resilient some software companies are in a crisis, because much of their revenues is contracted & recurring (especially if they've pivoted to a SaaS model in recent years).

All good then, but we're not given any guidance for the full year. Therefore there's still a chance that covid could have a delayed impact later this year, if customers go bust or don't renew annual contracts.

Given the continuing uncertainty, I think the valuation looks about right. Nice company, but I'm not prepared to chase the price any higher right now.

.

.

All done for today. See you tomorrow!

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.