Good morning from Graham and Roland!

This will be the final SCVR until Tuesday, as the UK market is closed for Easter bank holidays on Friday and Monday.

Today's report is now complete (10.15). Enjoy the long weekend!

Quick comments -

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Graham's section

Gear4music (HOLDINGS) (LON:G4M)

- Share price: 74p (-16%)

- Market cap: £15m

This is a stock that Paul usually covers, but here we are! Gear4Music is an eCommerce business that sells musical instruments. It has an amazingly volatile share price history:

Today we have a year-end update for FY March 2023.

These numbers are below expectations, as revenues and profits were “impacted by weaker consumer demand during February and March”.

Total sales £152m (expectations: £155.1m). The UK underperforms Europe and Rest of World.

Gross margin at 25.7% is weaker than last year, but perhaps this is the “normal” level for margins?

EBITDA £7.3 - £7.7m (expectations: £8.9m)

Net debt reduced by £10m during the year to £14.5m - that’s one bit of good news, as it was only expected to reduce to £17.5m.

Even if the numbers are disappointing on the whole, I greatly appreciate the transparency of this update. Most other companies require you to look up the broker notes to figure out prior expectations - thank you to Gear4Music for including this information in the update!

Looking ahead, there is “further reduction of net debt and a return to more profitable growth expected during FY24”.

I agree with Paul’s prior comments that the level of HSBC debt here was inappropriate. Fortunately, it appears to be heading in the right direction as inventory is reduced to the usual levels.

CEO comment: he reiterates the belief that FY 2024 will be better than FY 2023.

The further investment into our European distribution infrastructure during FY22 underpinned our progress in Europe during FY23, although high rates of inflation continue to squeeze consumer spending on discretionary items across all of our markets. In the UK, as previously announced, courier disruption impacted trading during our busiest period.

We are confident, however, of profitability recovering in FY24 as growth initiatives such as AV.com gain traction and the benefits of our continued focus on overhead cost efficiencies filter through.

The company is now offering second-hand products and trade-ins - an interesting idea! They will be competing with established operators in this space including eBay, Facebook Marketplace, Gumtree and Reverb.

My view

I’m sympathetic to the view that this stock offers investors a value opportunity.

Some reasons:

Great progress in debt reduction.

Exceptionally low price to sales multiple in the region of 0.1x

Shareholders have not been diluted yet, despite various acquisitions and extremely volatile trading. Management appear suitably reluctant to raise equity except as a last resort.

But we also need to be realistic about the stock:

Not very profitable in these conditions; needs a rejuvenated consumer to get it performing again.

Gross margin under some pressure. Pricing power remains questionable. Competitive market.

Unlikely to have the quality or resilience to justify holding any bank debt long-term; therefore should probably not pay any dividends until this is resolved.

I’m content to stay neutral at this level.

Solid State (LON:SOLI)

- Share price: 1130p (unch. today)

- Market cap: £128m

I checked out this company’s interim results in December, when it raised its expectations for the full-year. Yesterday, it produced a trading update for FY March 2023.

It describes itself as “the specialist value added component supplier and design-in manufacturer of computing, power, and communications products”.

Performance in H2 was strong and therefore FY March 2023 is again at least in line with consensus expectations

Revenues up 47% to £125m (expectations: £120.3m)

Organic revenue growth at constant FX is an impressive 20%

Adjusted PBT up 46% to at least £10.5m (expectations: £10.45m)

In August 2022, Solid State agreed to pay $45m for a California-based battery/energy company: Custom Power. It is performing in line with expectations, but is not going to achieve a full earn-out for the vendors, based on its revenue targets. So that will reduce the amount payable by up to $5m.

Contract wins: previously announced contract wins with NATO will “dilute the margin mix” but “contribute positively to the attainment of expectations for FY23/24”. I’ve remarked previously that Solid State puts a lot of focus on margins - but clearly they’re not going to say no to NATO contracts, even if these contracts hurt margins!

Order book: £120m extending over 18 months, up from £85.5m a year ago. There are still some supply chain challenges in the electronics industry, and this may be contributing to the bloated order book.

Solid State says it is navigating the situation:

…inconsistencies remain such that pro-active inventory management continues to provide competitive advantages to the Group and supply chain confidence for clients.

My view

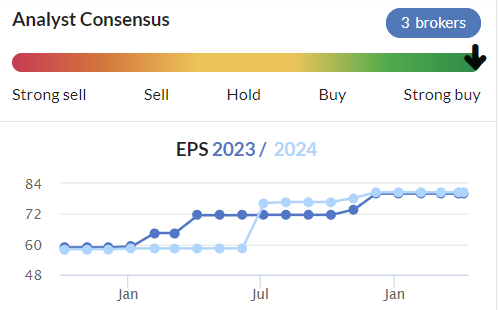

This one continues to strike me as a better-than-average manufacturer and distributor. I like management’s focus on margins, I’m impressed by the trend in earnings expectations over the past year, and returns are adequate.

EPS trend:

Returns:

The share price has retreated to where it was during late 2021/early 2022, so this could be worth digging into in more detail.

Roland's section

Motorpoint (LON:MOTR)

Share price: 131p (pre-market)

Market cap: £118m

The used car supermarket group has issued a year-end update today confirming it expects to breakeven this year at a pre-tax profit level on record sales of £1,437m.

It’s a dramatic comedown for a company that generated over £21m of pre-tax profit during its previous financial year (Motorpoint has a 31 March year end).

The share price has reflected this brutal decline, falling 65% from the record highs seen during the pandemic:

I’ll look at Motorpoint’s business model and the reasons for this slump in a moment, but let’s start with the main highlights from the year just ended:

Record revenue of c.£1,437m, up 9%

Pre-tax profit expected “to be broadly breakeven”

3.5% market share for vehicles under four years old (Dec ‘21: 2.7%)

£5m cash at year end and “significant borrowing headroom”

New Chief Technology Officer to drive digital growth

Net Promoter Score at “industry leading 84”

What’s gone wrong? In an update in January, management said that higher financing costs and falling prices on some electric cars had led to a reduction in gross profit per vehicle sold. Unfortunately, the company’s costs – staffing, energy, rent and stock financing – will not have fallen.

The wafer-thin margins on used cars leave no room for error, so Motorpoint’s historic profitability has evaporated.

In my coverage of Lookers (LON:LOOK) yesterday I commented on the importance of aftersales income to car dealers. This is why.

Conventional car dealers also earn low margins on their car sales. But by owning freehold property and securing high-margin aftersales work, dealers can more easily absorb some variation in margins on car sales.

For Motorpoint, it’s much harder. This trend could reverse at some point, though, and profits could rebound very quickly. Chief executive and 10% shareholder Mark Carpenter believes we could be approaching such a turning point:

"Whilst the impact of higher interest rates and inflation will continue into FY24, new car registrations rose 18% in March, with the fleet market driving this eighth consecutive month of growth, which will in turn benefit used vehicle supply. This, coupled with continued market share gains and progress on our key initiatives, will enable Motorpoint to emerge from the current environment a highly profitable market leader."

My view

I’ve previously had a favourable impression of this business and have owned the share in the past. Motorpoint’s policy of specialising in high-quality, nearly-new cars in bulk at competitive prices has given it a significant share of the market and strong customer loyalty metrics.

I can’t deny the risks here, though. This business depends on earning a wafer-thin margin on high volumes of used cars. If volumes slow, financing costs rise, or used car prices fall, this model is disrupted.

If macro trends continue to go against Motorpoint, the group’s financial model could break down altogether. Unlike conventional dealers, it can’t backstop losses with aftersales revenue or property sales.

On the other hand, if market conditions stabilise and the company’s core strengths return, profits could bounce back quickly.

On balance, I am cautiously optimistic that Motorpoint will survive and return to profitability. I’m also encouraged by the presence of owner-management – CEO Mark Carpenter has also seen his net worth plummet with the share price.

However, the situation is too risky for me to take a positive stance at this point. There’s no way to be sure the group will outlast difficult conditions in used car markets.

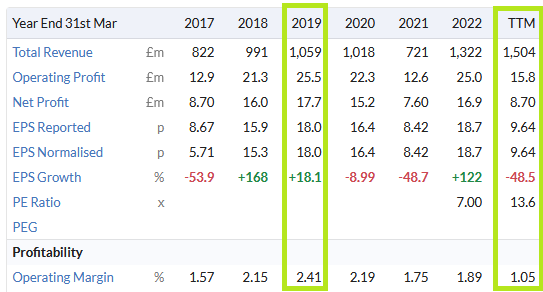

Robert Walters (LON:RWA)

- Share price: 424p (-3% at 08.40)

- Market cap: £327m

Today’s update from recruiter Robert Walters covers the three months to 31 March. It highlights challenging macroeconomic conditions in global recruiting markets, but does not seem to flag up any new problems.

CEO Robert Walters seems to be confident that underlying recruitment demand will remain positive, when conditions stabilise:

"It is worth noting that recruitment market fundamentals such as vacancy levels and salary inflation remain relatively robust, which coupled with a systemic global shortage of qualified professionals gives cause for optimism that activity levels will bounce back when global market conditions become more benign.”

The group’s Q1 revenue figures highlight the geographic diversity of this business (all at constant currency):

Q1 revenue: £102.4m (unchanged)

Asia Pacific: £43.4m (-3%)

Europe: £34.3m (+10%)

UK: £16.3m (-9%)

Other international regions: £8.4m (+8%)

Other operational metrics suggest a stable position:

Headcount up 1% quarter-on-quarter to 4,403

Net cash: £70.5m (December 2022: £97.1m)

One potential positive factor is the re-opening of the Chinese economy. The company says that net fee income in Mainland China fell by 44% during the quarter. I’d imagine that a return to normal here could provide a useful boost.

The company’s commentary on the UK market suggests that financial services hiring is holding up well, but other sectors are more muted.

My view

This recruitment group is one of my top choices in this sector. It provides global exposure and has a solid history of shareholder returns.

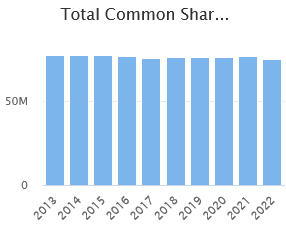

There’s also been no dilution for at least 10 years:

The shares look decent value to me on nine times 2023 forecast earnings. The dividend yield of 5.6% should be covered twice by earnings and backed by net cash, reducing the risk of a cut.

I’ve no idea what the short-term outlook will be for this business or the wider market. But taking a long-term view, the chart above and the company’s recent results suggest to me that now might be a good point in the cycle to begin building a long-term position.

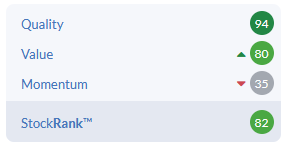

Stockopedia’s algorithms reinforce this view, with a high StockRank and Contrarian rating:

One possible risk is that founder-CEO Robert Walters will be retiring later this year after 37 years.

A successor has already been appointed who has been with the group since 1999, so I don’t expect massive change. But the departure of a long-serving leader is often an inflexion point, I’ve found. Founders often have good timing, too.

However, on balance I have no qualms about taking a positive view on Robert Walters. I think the shares look reasonably valued, with a solid balance sheet and excellent track record.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.