Good morning, it’s Paul here with the SCVR for Thursday.

Timing - Today's report is now finished.

Agenda -

Firstly, here are some brief comments on a few company news items from yesterday.

Greggs (LON:GRG) - trading update

Wandisco (LON:WAND) - more jam tomorrow!

Gresham Technologies (LON:GHT) - 2020 trading update

Auto Trader (LON:AUTO) - trading update - possible read across for small cap car dealer shares?

Mitchells & Butlers (LON:MAB) - exploring a fundraising & trading update

Joules (LON:JOUL) (I hold) - Xmas trading update

Mpac (LON:MPAC) (I hold) - 2020 year end trading update

Judges Scientific (LON:JDG) - 2020 year end trading update

.

Greggs (LON:GRG)

1920p (up 8% yesterday) - mkt cap £1.95bn

This is an update for FY 12/2020.

Greggs is a leading UK food-on-the-go retailer, with more than 2,000 retail outlets throughout the country

- FY 12/2020 revenues down 31% to £811m

- Year-end net cash of £37m

- £100m 3-year bank facility available, so liquidity sounds OK

- Repaid Govt CCFF loan - reinforcing that liquidity is OK

- Modest full year loss of £15m - not bad considering the covid/lockdown chaos in 2020

- Successfully developed takeaway & delivery alternatives (5.5% of store sales)

- New sites accessed by cars “performing particularly well”

- Q4 shop LFL sales were down 19% - to be expected given changing restrictions, and reduced number of people in city/town centres

- 820 staff redundancies

- Plan to open 100 new stores in 2021, net of closures

- Diary date - preliminary results due on 16 March 2021

Outlook - not great -

Looking ahead, the significant uncertainty over the duration of social restrictions, along with the impact of higher unemployment levels, makes it difficult to predict performance.

However, we do not expect that profits will return to pre-COVID levels until 2022 at the earliest.

Valuation - these figures look a lot better than the consensus broker forecasts shown on the StockReport, which is good.

Greggs made c.100p EPS in 2019, by the sounds of it we’re looking at possibly getting back to that level in 2022, so 2 years’ time. The share price is 19.2 times that target. That doesn’t strike me as very good value - recovery looks fully priced-in, so why would I want to buy now?

It’s a terrific business, no doubts about that, but I’m worried footfall may not return to pre-covid levels, ever, because many people have probably got used to shopping online, and working from home. What happens when business rates kick back in too?

It would have made a super purchase over the summer/autumn lows, but it’s since rallied too much in my view, hence doesn’t interest me on valuation grounds now - good business, but too expensive for me.

.

.

Wandisco (LON:WAND)

520p (up 8% yesterday) - mkt cap £283m

This company is always promising jam tomorrow, and claiming to have unique, ground-breaking software.

Paltry revenues for FY 12/2020 at least $10.5m - some (not given figure) sales deferred into 2021

This time last year, FY 12/2020 revenues were forecast at $32.3m - so the outturn is just under a third of the original forecast - pathetic I would say. Yet the share price now of 520p, is actually up on the 438p a year earlier. How does that make sense?

Year end cash of $21m

Outlook - reckons it has a “building pipeline of opportunities” for 2021, and guides for revenue of $35m in 2021 - more than tripling 2020 revenues - a very punchy forecast, and not credible based on past performance, in my view. I’m happy to be proven wrong though.

It says higher forecast sales are due to moving to the cloud, AWS and Azure, allowing fast implementations of new clients. 11 customers signed, but no indication of deal sizes given in this update.

My opinion - I’ve got no way of judging whether it is likely to achieve the huge forecast increase in sales or not. Historic performance has been very poor, so not something I want to gamble on. Good luck to holders.

The company has been listed since 2012, with revenues going nowhere ($10-20m and back down again to $10.5m a.) and racking up huge cumulative losses. Therefore it takes a big leap of faith to think it will suddenly achieve commercial viability. Maybe it will, I don’t know, but would need a lot of convincing evidence before wanting to take the plunge here myself.

That said, the technology has always sounded very impressive, so who knows, maybe it might eventually take off, or one of the big tech companies might buy the company?

I do recall that a few years ago, we managed to catch a big move up in this shares, and made a few bob, but that was just a lucky trade really, not an investment.

One for tech experts only, I reckon.

.

Gresham Technologies (LON:GHT)

148p - mkt cap £104m

Trading Update

This software company reports on performance in FY 12/2020.

Not very impressive is my conclusion. It says EBITDA of “at least” £4.4m achieved, but that reduces to zero once development spend is taken into account.

Cash of £8.8m

Overall trading for the year in line with recently upgraded market expectations

The Group's sales pipeline strengthened steadily during H2 2020 and the Company continues to see positive demand for its intelligent automation and connectivity solutions in financial markets despite challenging macro-economic factors.

In the second half of the year, we increased investment in sales and marketing, as well as completing our strategic investment into the regulatory and STP markets with our acquisition of Inforalgo. These excellent foundations have set us up well for another exciting year ahead."

My opinion - the market cap is just over £100m, and I’m finding it difficult to see why that makes any sense, given that it’s not making any cash profits.

This is another company that has been listed for a very long time, and doesn’t seem to live up to ambitious expectations.

.

Auto Trader (LON:AUTO)

610p - mkt cap £5.9bn

Current trading

Interesting for read-across to the general health of the market for secondhand cars.

Oct-Dec 2020 visits to its website were up 20% vs LY (NB not the same as revenues)

Expecting sales volumes to be impacted in Jan & Feb 2021.

Offering free advertising packages in Dec 2020 & Feb 2021, causing anticipated losses of £5-7m in each month

Drawings of £45m on £400m facility

Substantially within bank covenants

Latest lockdown has forced car dealers to close their showrooms again

My opinion - I don’t think there is enough clarity to know how car dealers might trade in these turbulent times.

AUTO is staggeringly profitable, with amazingly high profit margins. Whilst that’s good, I’d be worried about one of the internet giants destroying its lucrative near-monopoly. A bit like Rightmove.

.

Mitchells & Butlers (LON:MAB)

212p (down 10.5% at 08:11) - mkt cap £913m

I'm trying to cover as many trading updates as possible, even from mid to larger caps, at the moment. This is because reaction to lockdown 3 is very important, and has read-across to small caps. Plus, being locked down in Bournemouth in foul weather, I don't have a lot else to do right now!

As Phuntt helpfully points out in the comments section, this update is indeed stark.

MAB is a sprawling pubs group, with no less than 15 brands;

.

Trading statement covering the 14 weeks ended 2 January 2021.

My summary & comments -

- Enforced site closures meant reduced sales activity over the important festive season.

- All sites now closed (since 30 Dec 2020)

- Q1 (Oct, Nov, Dec 2020) sales down 67.1% on LY - ouch

- LFL sales (i.e. only when sites open) down 30.1% on LY

- Minimising costs & capex

- Cash currently £125m, all borrowing facilities maxed out

- Cash burn in lockdown is now £35-40m per month (before debt servicing costs)

- Debt repayments are £50m per quarter, as the group has a lot of borrowings, but backed up by large freehold property assets

- Put those last 3 items together, and we can see that the group is likely to run out of cash by end March

- Exploring an equity capital raise - no decisions yet made on timing, size, or terms

My opinion - it looks as if MAB management have misjudged the cash requirement. A new lockdown with little to no sales until Easter is nothing new - other hospitality companies have been planning on that basis as the most likely, or at least possible, scenario.

Checking back to MAB's results for FY 09/2020, the balance sheet looks out of balance, in that there's clearly inadequate working capital: current assets of £239m, and current liabilities of £(701)m.

Overall the balance sheet looks OK, because there are £4.3bn of fixed assets, which includes £3.79bn of freehold property (source: 2020 Annual Report)

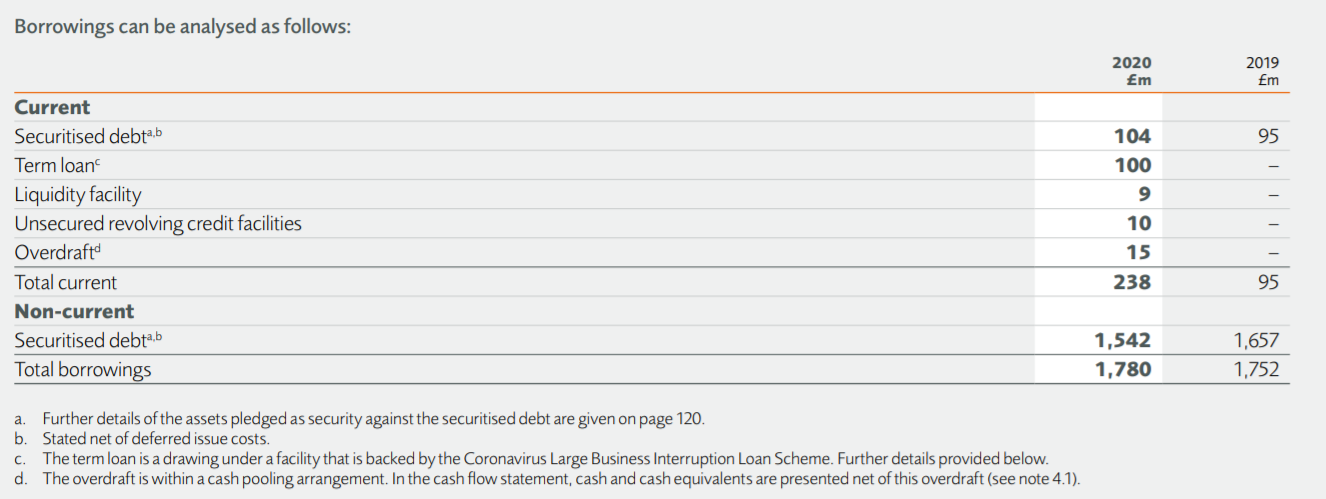

Material uncertainty re going concern was flagged by the auditors in the last Annual Report. The business seems to potentially rely on the leniency of holders of bonds which provides most of the funding. Long term borrowings were £1.54bn at at 26 Sept 2020. See note 4.2 of Annual Report, including this breakdown of net debt -

.

Even if we halve the value of the freehold property, it's still enough to cover the debt. Therefore I don't see this as a distressed situation.

Therefore it should be possible to refinance the group again, with fresh equity, perhaps as part of a package to include resetting terms of debt, and covenants.

It could get messy if bondholders decide to play hardball.

Personally I'm not tempted to get involved, at least until the equity fundraising has been done. I'm sure institutional shareholders will support an equity raise, but we don't know the price - it could be at a significant discount, who knows. Therefore why take the risk of getting involved in this share now, with that uncertainty hanging over it?

The sector read-across is that investors need to do the sums to ensure other hospitality companies have adequate funding. I've crunched the numbers for Revolution Bars (LON:RBG) (I hold) and am happy that it can survive until Easter with zero revenues. Although RBG did confirm in its last update that the covenants are tight at end March 2021. That said, with re-openings likely to have happened, or be imminent by then, it shouldn't be a problem if a small amount of bridging finance is needed.

With vulnerable people hopefully vaccinated by Easter, then restrictions on trading are only likely to last c.3 months, based on current facts. Therefore shareholders are likely to support any fundamentally sound hospitality companies. That's not necessarily true of privately owned companies, so I think we're likely to see carnage in this sector, with potentially thousands of privately owned bars going bust between now and Easter. More market share for the bigger operators of course, once they're allowed to re-open.

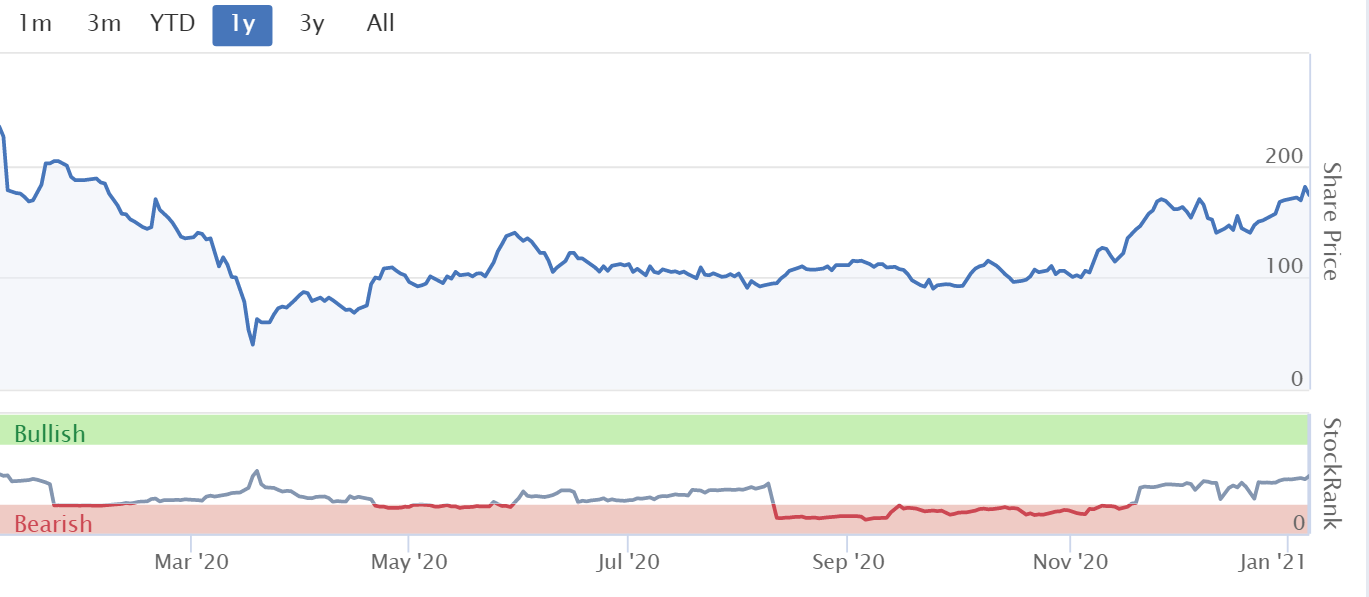

Looking at this chart, I'm surprised MAB shares have held up so well. I came to a similar conclusion when looking at J D Wetherspoon (LON:JDW) shares recently - too much recovery is already priced-in for my liking. Hence risk:reward doesn't look attractive at this point in time.

.

.

Joules (LON:JOUL)

171p (down 5% at 10:18) - mkt cap £186m

(I hold)

This is a distinctive UK fashion brand. It sells wholesale, retails from its own shops, and has a strikingly high percentage of total sales online - which makes it interesting to me. As regulars here might know, I’m usually only interested in retailers that are nailing it online, and reducing their exposure to physical stores.

By this stage, fashion brands really should have got half their sales online, and be rapidly reducing lease liabilities. Otherwise they’re in danger of following Arcadia down the pan. I’m not convinced by Superdry (LON:SDRY) or Ted Baker (LON:TED) as examples which are trying to sort themselves out, but have not yet convincingly demonstrated a turnaround. Although I’m keeping an eye on both, because if they do pull off a turnaround, then there could be decent upside. Both possibly a bit old hat, in terms of brands?

Back to JOUL, an up & coming brand. A little while ago I decided to bank my profits on Marks And Spencer (LON:MKS) (not often you can say those words! It was a lucky purchase at the lows), and put the money into a starter size position in JOUL, at about 150p per share. I was worried that I might have overpaid, but am taking a long-term view with JOUL now, hence the exact purchase price doesn’t really matter to me. The strength of online sales, and my review of the 8 Dec 2020 trading update, convinced me to dip my toe in with a modest initial purchase just before Xmas.

Today’s update - it’s a Xmas trading update, usually peak trading, but obviously disrupted this time by covid;

Joules, the premium British lifestyle brand, is pleased to provide a trading update for the Group's retail channels during the seven-week period to 3 January 2021 (the "Period").

The most important bit is buried in the middle of the announcement, which sounds very encouraging to me;

Total retail revenue through Joules' own-branded retail channels(2) during the Period was up by 0.3% against the prior year, with the growth in Joules e-commerce sales more than offsetting the decline from stores.

(2 )Excludes third-party retail platforms that Joules sells through

eCommerce sales have been very strong. This is important because (although we’re not given the figures unfortunately), Joules is making the majority of its sales online these days;

Total retail sales through Joules' websites, including sales through the Friends of Joules digital marketplace, increased 66% year on year1

1 Gross sales, including Joules own e-commerce and Friends of Joules, prior to returns, calculated consistently in each period

Store closures due to lockdown restrictions has obviously hit store sales hard -

Total store sales declined by 58% during the Period, reflecting the enforced closures of non-essential stores and reduced footfall as and when stores were able to remain open.

(5 )Stores were closed (on average) for approximately half of the seven-week period

LFL sales when stores could open, was better, at 23% lower - not bad in the circumstances, in my view.

Good brand metrics, including an impressive 1.5m active customers.

(4 )An active customer is a customer registered on the Joules database who has transacted in the last 12 months

Net cash of £13m at 3 Jan 2021, and £63m total liquidity headroom - sounds ample, so no solvency worries here.

Outlook -

All stores now closed in lockdown 3

Estimated loss of sales will be £14-18m, assuming re-opening on 1 April 2021, and includes lost wholesale & country shows revenues. Useful information.

Mitigation from;

- Better than expected trading in first 7 months of FY 05/2021

- Strong online performance

- Cost reductions, including HO costs & lease renegotiations.

Diary date - interim results (6m to 11/2020) due out on 28 Jan 2021.

Broker update - many thanks to Liberum, for making their update note available today on Research Tree. This is tremendously helpful to PIs, and helps generate buying interest in the shares & improve liquidity. I wish more brokers would follow suit with many more companies.

Forecast for FY 05/2021 PBT has been cut today by £1.4m, to £3.7m, reflecting impact of lockdown 3. I'm relaxed about that, as it's a factor outside the company's control, and pent-up demand often returns afterwards, or shifts online.

Valuation - forecast EPS for FY 05/2021 is now 2.6p, which at a 171p share price gives a current year PER of almost 66 ! Eeek that’s expensive. However, it’s a highly disrupted year, so shouldn’t be typical of future performance once we’re past covid.

Earnings clearly need to grow strongly in future years, to justify the current valuation. 6.8p is forecast for FY 05/2022, a forward PER of 25 times, which I think can be justified given the unique brand, and very strong online performance.

My opinion - the current valuation does look a bit aggressive, but I’m prepared to look beyond the current financial year. If future profits don't bounce back strongly, then there could be downside risk. Things have gone wrong in the past, so it's not risk-free by any means.

However, it seems to me that there is something special with this brand, and having demonstrated that it can shift to successfully selling online when shops are forced to close, that greatly de-risks the business model. The "friends of joules" marketplace is an interesting development. Could this be an early-stage fashion portal for yummy mummies?! It's possible. Fashion doesn't really work on Amazon.

I don’t want to chase the share price any higher, as it looks fully valued for now. However, I’ll be looking to buy any market dips in 2021, to slowly build up a bigger position size in Joules. After several years following, and appraising it, I’m now satisfied that this should be a good long-term investment (5+ years timescale for me). Hence I want to build up my holding on the dips, in 2021. As usual, I have no idea (or view) on what the short term share price is likely to do.

Note that the founder still holds a large stake, often a good thing, in my view. Although there's a risk that private equity could tempt him to take it private, if things start doing really well. Although I'm told the small print can be horrible with PE deals, so probably best to stay listed on AIM. We need more decent companies like Joules coming to join AIM. Too much junk gets floated.

.

.

Quite a lot of recovery has already been priced-in

.

Mpac (LON:MPAC)

455p (up 8% at 12:32) - mkt cap £90m

(I hold)

This is a very interesting group of companies, making packaging & automation machinery.

Here is my review of the recent interim results, published on 3 Sept 2020, to quickly get up to speed on the background. Profit was down 45% on H1 LY, due to project deferrals caused by covid.

Jack reviewed MPAC here - flagging the enormous pension scheme liabilities, which does worry me, because small changes in assumptions can trigger big moves in surplus/deficits. Especially as interest rates could even turn negative at some point.

Trading update today -

Mpac Group plc, a global leader in high-speed packaging and automation solutions, provides a pre-close trading update (unaudited) for the year ended 31 December 2020.

The summary says -

Resilient FY20 trading performance, ahead of market expectations and encouraging outlook for FY21

The Board is pleased to announce that the Group expects to report underlying profit before tax for the full year 2020 above market expectations, primarily as a result of better than expected margins in Q4 driven by sector mix.

Trading continues to be resilient, as Mpac serves essential healthcare, food, and beverage markets, deploying digital technology to mitigate travel restrictions despite the continued headwinds from the pandemic.

That sounds good.

Acquisition of Switchback Group Inc - announced in Sept 2020. Going well, it is trading ahead of expectations, with synergies secured.

Order book was £45.4m as at 3 Sept 2020, is now up to £55.5m. No orders cancelled due to covid.

Diary date - FY 12/2020 results are due out w/c 1 Mar 2021

Outlook - is upbeat;

Our pipeline of qualified opportunities and our closing order book give confidence for 2021. The acquisition of Switchback has further enhanced our presence in the Americas and the integration into the wider Group has been successful.

I am confident that we will be able to report a robust financial performance for 2020 and a positive outlook for 2021 which is testament to the fundamental strengths of the Group."

Research update - Paul Hill of Equity Development is an excellent analyst, very thorough. He’s published an update today here. There’s also a 10-minute results video out today, here:

.

H1 produced adj PBT of £2.5m. Paul Hill forecasts £3.5m in H2, giving £6.0m for FY 12/2020, which equates to 25.7p EPS.

That’s a PER of 17.7 (based on 455p share price), which sounds about right to me.

My opinion - I’m sitting tight on my small position in MPAC. Looking back, am wishing I’d bought more, but it was terribly illiquid when I was trying to buy at about 280p. Clearly I should have just paid up, not faffed around worrying about a few pence!

The pension schemes are the key issue that need carefully checking out, so people should check the last Annual Report for more detail on that. I’m wary of pension schemes, given how ultra-low interest rates seem to be causing considerable risk of cash outflows needed to prop them up.

Other than that, MPAC seems to be a decent quality business, operating in a nice growth area. Acquisitions are sprinkling a bit of fizz on top too.

Note below that the StockRank system is super-positive on MPAC, a reassuring indicator.

.

.

Judges Scientific (LON:JDG)

6350p (up <1% at 14:02) - mkt cap £400m

Trading Statement

The Board of Judges Scientific plc, a group focused on acquiring and developing companies in the scientific instrument sector, provides the following update on the Group's trading performance for the financial year ended 31 December 2020.

This seems a pleasing update, the key part saying;

… the Group's performance has remained resilient with the second half of the financial year showing a gradual improvement in our trading environment. As a result, the Board anticipates that Adjusted(3) Earnings Per Share for the full year ended 31 December 2020 will be ahead of market expectations(4)....

3. Adjusted earnings figures are stated before adjusting items relating to hedging of risks materialising after the end of the period, amortisation of acquired intangible assets, share based payments and acquisition-related costs.

4. Market consensus Adjusted Earnings Per Share of 151.8p.

Hooray for footnote 4, thank you to the company & its advisers, that saves investors so much time & avoided confusion! Why can't all companies help us in this way?

Unfortunately we’re not given any idea on how much ahead of expectations, so all I can really say is that at 6350p per share, the PER is lower than 42 times, but we don’t know how much lower! These high PERs can’t keep rising forever, and the risk is that they might revert to the mean, or at least reduce somewhat, in future.

My opinion - it wasn’t long ago that we could buy this on about 13 times earnings, so there has been a massive expansion of the PER by the looks of it. That applies to lots of shares.

The price is too rich for me, but good luck to holders.

.

That's it for today! See you tomorrow.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.