Good morning from Paul & Roland!

Liz Truss - Energy Statement (House of Commons today)

Here are my notes of the main points -

New energy price guarantee, will curb inflation.

Temporary suspension of green levies on energy bills.

Households - rate will be capped so that average household spends £2.5k (as expected).

Additional £400 support will continue, as previously announced, plus additional support for poorer households already announced.

This supersedes OFGEM price cap.

This deal has been agreed with energy suppliers.

Long-term measures being taken to secure more affordable supplies.

Fund will be set up to give equivalent help to households that are off-grid, e.g. using oil, and park homes.

Business - will get equivalent support for 6 months. Longer support for hospitality sector.

Emergency legislation will be introduced to push this through.

Chancellor of Exchequer will set out costs later this month.

Not doing another windfall tax, because we need to encourage home-grown supply, not stifle investment.

Our approach is pro-growth, pro-business, pro-investment.

Can’t tax our way to growth (intervention from John Redwood)

This is the moment to be bold (she obviously listens to my podcasts LOL!)

We’ll defray the cost of this intervention by ramping up supply.

Maddie McT?????? Is already negotiating new supply contracts.

Accelerating all domestic production - new licensing round (for oil/gas?) expected to agree over 100 new licences.

Accelerating renewables & nuclear - prices will move to CFDs, not based on gas price.

UK is already a global leader in offshore wind.

Generators will receive a fair price, bringing down the cost, under new contracts.

Question re Rolls-Royce small, modular nuclear reactors. Yes, these are important.

Substantial boost to the economy.

These measures expected to curb inflation by up to 5% bps - this will reduce cost of servicing Govt debt.

£40bn fund will be set up (by BoE I think she said?) to provide liquidity to the energy suppliers, to stop more going bust, and hence reduce costs.

Net zero - remain completely committed to this by 2050.

Why are we in this situation? Policy has not previously focused on energy supply.

We didn’t build any new nuclear in the last 25 years.

Regulatory framework has failed. Left us vulnerable to global factors & bad actors (Putin).

Putin has weaponised energy supply.

Question - we have 150 years supply of shale gas, why are we not using it?

Answer - we’re going to end the moratorium on shale gas (fracking). Production could start as soon as 6 months. Only where there is local support.

We must never get into this situation again.

2 reviews will be launched;

- Review of energy regulation, to fix underlying problems, address supply & affordability long-term.

- Review how to achieve net zero by 2050, that’s pro-business, pro-growth, led by member for Kingswood (Chris Skidmore)

Launching “Great British Nuclear”, with aim to achieve 25% of total electricity supply by 2050.

Question - Rough Gas storage facility closure was short-sighted wasn’t it?

Answer - she dodged the question.

UK will be a net energy exporter by 2040 - plan will be set out in next 2 months.

Secure energy supply has been ignored for too long. I will end short-term approach on energy security, once and for all.

Keir Starmer - put on mute, so I could type up the above!

Energy Crisis - latest thoughts

Probably like many of you, I was glued to the TV news yesterday, trying to pick up facts & views on the ongoing energy crisis. Just a few snippets worth repeating -

Big announcements are scheduled for today, on both the energy relief packages for households and businesses. Plus they're tackling the problem of inadequate supply, and the structure of the energy market too, apparently. The Speaker insisted these have to be announced to the House of Commons first, but a lot seems to have already been leaked to the press.

Looking at the TV schedule for today, "Live House of Commons" starts at 11:30 (EDIT: a friend says it might be slightly earlier at 11:15) on the BBC Parliament channel, so I'll have that on in the background, and will take notes to put up here. It's so important for corporate earnings, and market sentiment, hence this is the no.1 macro issue right now.

There was also some useful analysis from journalists. One reported that high prices have already dented demand i the UK, which is down 7% apparently (gas and electricity, presumably?) and that currently the UK is exporting energy to Europe, but that is expected to reverse later this year (if they have the capacity to supply us?).

Forecasters have already begun lowering their expectations for peak inflation, which is obviously very encouraging. Clearly it is obvious that inflation should peak much lower, if bills are capped at £2.5k, versus the previous expectation that they would soar to £6k in early 2023. Although we don't know what, if any, side effects there would be from a big rise in Govt borrowing. Anyway let's reserve judgement until we know the full facts, hopefully c. lunchtime today.

Markets tend to start moving up when there's a solution in sight to major problems, but before the actual solution has had a positive effect. We saw that from Oct 2008 when it became clear Govts would backstop the major banks. As mentioned yesterday, during the pandemic, the initial Govt measures (e.g. furlough, extensive loan schemes) stopped markets falling in Mar/Apr 2020, and began a decent rally. Then a huge bull run started when the news came through of the vaccines in autumn 2020. So it's key, game-changing news that tends to spark the big recoveries in share prices, I've observed. As mentioned yesterday, I think we're at that point again. I'm not saying everything is fine, and we're back to a bull market, but just that I think the blind panic we've been seeing of late, with people anticipating armageddon, now looks overdone, given that a huge package of support is being brought in, and fast. So a decent rally in bombed out small caps, is my current thinking. But nobody knows, it's just a hunch based on what I've seen happen in the past.

Also worth mentioning is that the reversal of the planned corporation tax rise from c.19% to c.25% (rough figures), is a big boost to future corporate earnings, and should mean that forecast EPS can be revised up, or at least mean fewer profit warnings, if companies leave forecasts unchanged with the now defunct higher corp tax rate. A significant tailwind, to help offset the many headwinds.

Agenda -

Paul's Section:

Warpaint London (LON:W7L) - another positive update, with profit guidance raised c.8% - not entirely unexpected, as we commented here in June that it looked set up to beat soft forecasts. This share ticks all the right boxes for me - trading well, modest PER of about 11, terrific balance sheet, and a dividend yield of 6.0%. Also it has entrepreneurial management, that I'd like to speak to at some stage. So an enthusiastic thumbs up from me. You see, it's not all doom & gloom is it?!

Roland's Section:

Severfield (LON:SFR) - a solid update from this steel group, with stable order books and an unchanged outlook for the full year. Severfield claims to be managing inflationary pressures and have good visibility for the remainder of the year. Exposure to industrial and infrastructure markets may provide some protection against cyclical pressures. With the shares close to their pandemic lows, there could be value on offer here.

MPAC (LON:MPAC) - today’s half-year results from this packaging and automation specialist give us a chance to learn more about the impact of July’s profit warning. The picture isn’t very appealing, in my view. Profitability has collapsed and underlying order intake is flat, at best. I’m not yet convinced that management has created much value for shareholders, post-Molins. However, I accept the group’s redevelopment is still ongoing. DYOR.

Speedy Hire (LON:SDY) - [no section below] - Today’s AGM update from this equipment hire firm continues the theme of robust trading in the infrastructure and industrial construction markets. Management says that “some recent weakening in market conditions” has been offset by new contract wins with “major customers” effective from October 2022.

Speedy is also continuing to invest in its retail and trade offering, through a partnership with B&Q. A new marketing campaign is underway to promote the business to consumers.

Net debt was £95m at the end of August. This looks reasonable to me, at under 30% of fixed assets.

Outlook: overall trading is said to be in line with expectations. Consensus forecasts put the stock on seven times earnings, with a yield of 6.6%. As with Severfield, I think there could be some value here, if the UK economy can be stabilised without a major recession.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s section

Warpaint London (LON:W7L)

111p (pre market open) - mkt cap £85m

I last reviewed this makeup company here at end June, coming away with a positive impression. My inkling at the time was that full year forecasts looked beatable - that’s what we like, forecasts set lowish, which should then mean less risk of a profit warning clobbering the share price by 30-50%.

Today we get another positive update, as anticipated -

Strong trading performance continues and results for the year ending 31 December 2022 now expected to be ahead of market expectations

New guidance is at least £61m revenues for FY 12/2022.

Gross margin robust, and above 2021.

Adj PBT for FY 12/2022 now expected to be at least £9m.

Potential further benefit from forex hedging arrangements.

I’ve not seen any new broker notes yet today, but it’s easy enough to compare new guidance with the last note from Shore, which was £8.3m adj PBT (now raised to £9.0m, possibly more), and EPS of 8.8p, which I can raise by the same 8.4%, becoming 9.5p. What’s the betting they beat that in turn, and come out c.10p?

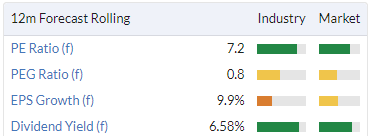

Valuation - The shares are 111p at close of play yesterday, so the PER looks to be only about 11. That’s too cheap I think, given that the company is performing well.

My opinion - thumbs up from me, I think this looks a good entry point at a modest PER, for a business that’s performing well despite all the macro headwinds.

The divis are really good too, with a forecast yield of 6.0%.

It has a cracking balance sheet too. Entrepreneurial management have big personal stakes.

So overall, this share is right up my street, and gets an enthusiastic thumbs up. If I had any spare cash, I would have bought on the opening bell today.

.

Roland’s section

Severfield (LON:SFR)

59p (+5% at 08.10)

Market cap £182m

When I last covered structural steel group Severfield in April, I commented on the obvious cyclical risks but suggested the shares could be good value.

Events have moved on since then and the market has priced in a further downturn, but once again today’s update reports solid trading and confirms full-year expectations.

“Performance in the first five months of the 2023 financial year has been strong and trading is in line with management’s expectations”

Operational highlights - The company says it’s managing inflationary pressures – it’s a big energy user – and expects several ongoing projects to deliver “significant profits in H2”.

Severfield’s operations are divided into two geographic segments:

UK and Europe: The order book stood at £483m on 1 September. This compares to £486m in June 2022, and £393m in November 2021. So the trend does appear to be positive, or at least stable.

I think that one reason for this may be the diversity of Severfield’s client base. The company supplies commercial and industrial construction projects, plus infrastructure and nuclear projects.

Management says they’re seeing “a good mix of projects” across the company’s key market sectors.

One other point worth mentioning is that 97% of the order book is for UK projects, so this is really a play on the UK economy. Europe is largely irrelevant at the moment. Although the company says it has a strong pipeline of bidding opportunities in Europe, its market share on the continent must be minimal.

India: Severfield is continuing to invest in this market as part of the JSSL joint venture. The order book is stable at £152m (June 2022: £158m) with “an improving pipeline of potential orders”.

Management says that the “ongoing conversion of the market from concrete to steel” should drive long-term growth and value in India.

However, as I’ve reported previously, profitability from JSSL has been minimal in the past, so I’m not sure how to value this part of the company.

Outlook: Management expects full year results to be in line with previous expectations. That prices Severfield shares on seven times forecast earnings with an attractive 5.7% yield.

Forecasts for the current year reflect expectations for a strong H2. Broker numbers suggest operating margins could hit 7%, with double-digit return on capital employed. That would be an improvement on last year’s performance:

My view: Severfield appears to have resolved its historic problems and is operating with respectable profitability and a healthy balance sheet. Demand appears to be stable and broker forecasts remain positive:

Severfield could be a winner if the government’s planned energy bailout helps to create a soft landing for the UK economy.

Personally, I’m not completely convinced. But for investors who are more bullish and expect a stable outlook, I think Severfield could be worth a closer look at current levels, especially given the high dividend yield on offer.

MPAC (LON:MPAC)

231 (-8% at 08.30)

Market cap £47m

This consumer goods-focused “high speed packaging and automation solutions” group has been a successful turnaround investment in recent years. However, MPAC blotted its copybook in July with a big profit warning that caused the shares to collapse:

Graham covered the July profit warning here. Today’s half-year results give us a chance to see how the business is operating in more detail and gain an updated view on the outlook for the full year.

Financial highlights: The headline numbers do not look especially positive to me. New order intake has fallen and profitability has collapsed.

- Order intake of £32.8m (H1 2021: £51.7m)

- H1 closing order book of £62.6m (H1 2021: £62m, FY21: £78.4m)

- Revenue +14% to £50.6m

- Underlying pre-tax profit £1.1m (H1 2021: £4.7m)

- Statutory pre-tax loss of £0.4m (H1 2021: £2.8m profit)

- Net cash £9.5m (H1 2021: £11.2m, FY21: £14.5m)

Order book: MPAC says that the shortfall in orders during the first half was due to “a significant value of orders” that were brought forward from 2022 into Q4 2021 in order to secure lead times.

We can test this. The order book rose by £16m during the second half of last year. If I add this to the H1 2022 order intake, I get a figure of c.£49m, which is only slightly below the H1 2021 order intake of £51.7m.

However, there’s no escaping the lack of growth here. At best, I think we might say that MPAC’s underlying order intake has flatlined over the last year.

Revenue: sales growth appears to have been driven by the order backlog accumulated at the end of last year. Sales of original equipment were 17% higher, but service revenue only rose by 6%. The company says customer site activity was impacted by Covid restrictions.

Profitability: MPAC’s profit margins have collapsed. The company says this is due to higher costs, changing product mix and supply chain disruption, plus investment in new products.

MPAC’s gross profit margin fell to 21.1% (2021: 33.4%) due to “product and sector mix” as well as supply chain disruption.

The group’s underlying operating profit margin for the period fell to 2.4%, compared to more than 10% during H1 2021.

These figures suggest to me that MPAC has not been able to pass on higher costs to its customers. That’s a little disappointing. It calls into question the company’s competitive advantages, in my view.

Cash: Fortunately, MPAC is still well-endowed with cash from the £30m sale of its Molins tobacco machinery business in 2017. Unfortunately, MPAC is continuing to consume this cash:

Investing for long-term growth makes sense. But how much value is being created?

If we strip out the pension-related items from the balance sheet, MPAC’s net asset value today is just £23.2m.

The comparable NAV figure at the end of 2016, before the Molins disposal, was £37.6m.

Cash generation during the first half of the year was poor in my view, as it was last year:

I haven’t looked into this in detail, but I wonder if MPAC benefited from Covid-19 related contracts in 2020 which buoyed the firm’s results?

Outlook: MPAC’s management remains positive about the prospects for an agreement with FREYR Battery regarding battery cell automation lines. However, these discussions haven’t yet reached a contractual stage.

In terms of current business lines, the company says it’s seen “good acquisition” of new customers in healthcare and plant-based food.

A new Group Procurement Director has been appointed to manage the supply chain. Perhaps he or she will be able to improve cost control. The company continues to expect supply chain issues to ease in 2023.

The financial outlook is unchanged from the revised market expectations set out in July. According to broker consensus forecasts, these are for revenue of £95.2m and adjusted earnings of 14.6p per share.

Incidentally, this implies that H2 revenue will be c.£45m, which is below the H1 figure of £50.6m. This seems to support my conclusion that H1 revenue growth was due to the backlog of orders being cleared.

My view: I haven’t followed MPAC in any detail in recent years. I’d need to do more research to understand the company’s business lines and its prospects.

However, based on my reading of today’s results, I have reservations about how much shareholder value this business is creating. Profitability and cash generation seem poor and the company’s pricing power appears to be weak.

Another lingering concern for me is that the size of MPAC’s pension liabilities dwarf the value of its business. Today’s accounts show defined benefit obligations of £316.5m and assets of £376.5m. This compare to a market cap of c.£50m.

The scheme is in surplus and rising interest rates may mean that the company is able to reduce future payments into the scheme. However, as things stand the company has to make £1.9m deficit reduction payments each year until 2024. Administration charges are also material, at around £1m annually.

I’d need to do a lot more research to see if I could get comfortable with MPAC shares. But on balance, my feeling is that there are probably better opportunities elsewhere.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.