Good morning, it's Paul here with the SCVR for Thursday. Apologies for the placeholder being a little late (07:24), this is because my phone was accidentally turned off, and so my alarm didn't go off as usual at 06:50.

Timings - TBC.

Agenda -

Portmeirion (LON:PMP) (I hold) - Interim results

Bigdish (LON:DISH) (I hold) - funding update

Character (LON:CCT) - trading update

.

Bigdish (LON:DISH)

Share price: 2.0p

No. shares: 275.7m

Market cap: £5.5m

(I hold)

This is a tiny, pre-revenue share, so I'll keep it brief. It's one of my larger personal holdings, because I see interesting highly speculative upside. The concept was originally a discount dining app, that used yield management principles to allow restaurants to offer discounts for specific half hour slots, in order to get bums on seats at times they would otherwise be empty. It worked superbly, and I used it at least twice per week, pre lockdown.

The business model was recently broadened, to expand into takeaways, link into EPoS systems, and become a package (initially free, to rapidly gain market share) intended to disrupt existing booking apps, and in particular to start eating JustEat's lunch (who price gouge takeaways by charging 14%).

The market potential for an ordering & discounting app is clearly much larger now, as restaurants need to manage the flow of customers more closely, in order to maximise revenues, given that capacity constraints and 10pm closure are being imposed to help battle covid.

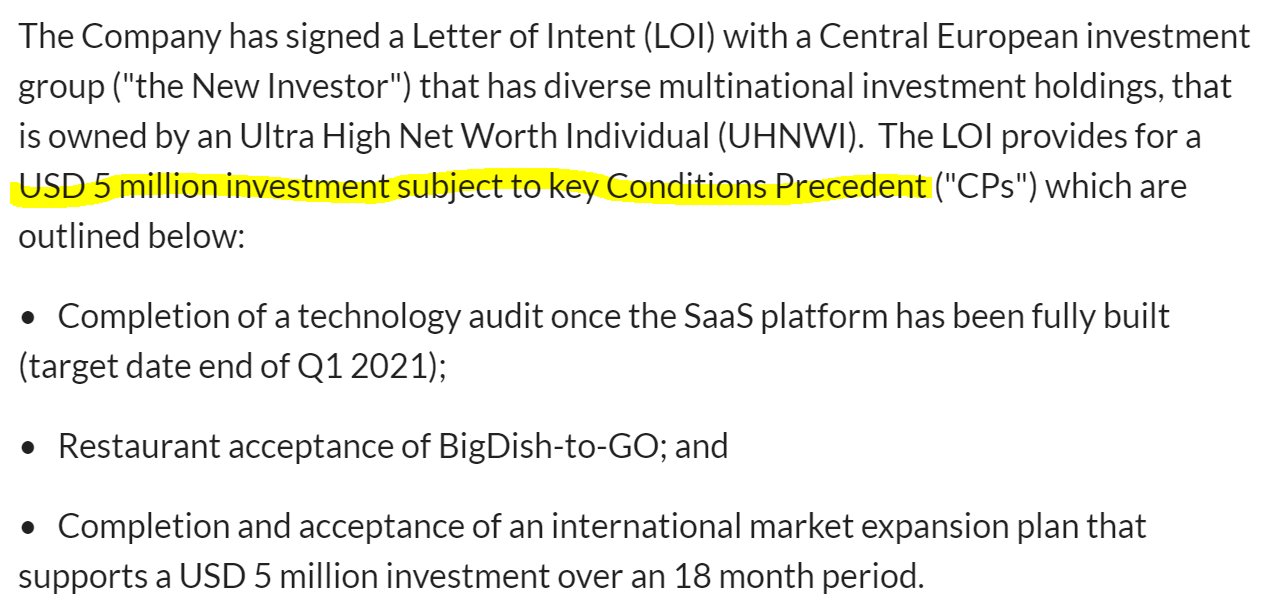

Quite an ambitious plan, and it needed funding of $5m, with the remaining cash close to running out. The Chairman told me he didn't want to dilute existing equity, so was looking at alternatives. Since DISH has a full listing, not AIM, a conventional equity fundraising would be too expensive, needing a prospectus to be produced. He's proven adept at raising money before, getting c.£2m from a US investor last year, at 7p per share (price now c.2p per share). Technology investors will pay mind-boggling money for startups these days, especially in America.

Today we're told of a deal that's been done, but it's subject to quite stringent conditions.

Short term funding of £540k has been secured as a loan, which extends the cash runway until June 2021 - good news. Although I don't suppose the loan would be cheap, but we're not told the terms. It avoids dilution at a low share price, so as a shareholder, I'm very pleased about that.

Potential $5m funding - heavily conditional, so obviously there's no guarantee this will complete next year;

.

.

My opinion - I'm happy with this. My main worry was that cash is close to running out, so I wanted to avoid being diluted in a further fundraising. As I've emphasised numerous times before, this is highly speculative share, which will either go bust, or be taken private for peanuts, or multi-bag. If it works, it could be a major multibagger - that's obviously why I'm having a punt on this, in the hope the shares could go bananas next year. But I'm fully aware of the risks, and have sized the position so that it won't kill me if things fail.

Given that the existing app is excellent (I used it a lot pre-lockdown) then I understood the potential for this, if everything goes well in the future. Plus the company already has an excellent telesales operation, which pre-covid had a proven track record of recruiting restaurants rapidly.

The stock market is obviously sceptical at this stage, which is why the market cap is so small. That's fine, it will take 6-9 months for this project to develop, so we'll see what happens in due course. Definitely not for widows & orphans!

.

My mouse just clipped the "BROWSE" button on the left, by accident, and I lost the entire section I'd almost finished writing on Portmeirion. An hour's work destroyed, arrgghhh! So I'll have to start all over again. It's so maddening when that happens. I think I've managed to successfully suppress my rage & urge to destroy something!! And breathe. Right, here goes...

Portmeirion (LON:PMP)

Share price: 375p (up 2%, at 09:43)

No. shares: 13.97m

Market cap: £52.4m

(I hold)

Portmeirion Group PLC, the designer, manufacturer and worldwide distributor of high quality homewares under the Portmeirion, Spode, Royal Worcester, Pimpernel, Wax Lyrical and Nambé brands, is pleased to announce its results for the six months ended 30 June 2020.

It's worth having a recap of my report on 15 July 2020 here, which summarised the H1 trading update. Today's figures are consistent with that, so no surprises.

H1 revenue down 8.3% to £32.0m (helped by acquisition of Nambe, organic growth was minus 20.4%) - obviously caused by covid resulting in customers shutting down their retail sites

Headline loss of £(2.7)m - not bad in my view. H1 is seasonally slow anyway, with only a £0.5m profit LY

Continuing improvement in sales within H2, and UK factories now close to pre-covid capacity

Online growth very strong at +90% in UK & USA. This is a very important element of the new growth strategy, with digital marketing & eCommerce specialists having been recruited to drive sales through this (higher margin) channel. The company is expecting continued strong growth in H2

Net cash of £1.1m, plus plenty of headroom on bank facilities - helped greatly by £11.2m (net) placing at 380p

Dividends expected to resume in 2021. Historically PMP paid generous divis, so I think buying now could lock in a decent long-term income stream - although remember to adjust for the increased number of shares in issue since the placing.

Balance sheet - is strong. NAV: £56.5m, less intangibles of £16.5m, gives £40.0m NTAV - which is plenty for a group this size, and not much less than the market cap.

Inventories look high at £30.6m - possible over-stocking, I wonder? Or it could just be due to the last acquisition coming into the numbers for the first time?

Note the pension deficit, of £2.0m. Not much, but it consumed cash of £1.2m last year, and that fell to £0.4m in H1 TY. With interest rates now permanently zero (probably), then pension deficits are an ongoing problem.

Cashflow statement - looks fine.

Outlook - very vague comments, sticking to the previous formula of saying that H2 should be profitable - which sets the bar very low, because H2 is usually strongly profitable, making almost all the year's profit.

Webinar & interview - there's a InvestorMeetCompany results presentation, with Q&A at 2pm on 28 Sept.

Plus, I will be interviewing the CEO (audio) late on 2 Oct. So if you have a brief and coherent question (not some rambling essay, as people often post!) that you'd like me to ask the CEO, then please leave a comment below. It's great to have some crowd-sourced questions.

My opinion - the growth strategy appeals to me, especially online growth. I've ordered twice, and am delighted with the Botanic Garden range of items received - terrific product quality, and not expensive for what it is. There's a clear opportunity to engage directly with customers, which bags both the wholesale and retail margins for PMP, and talking directly to the end customer means they're more likely to repeat buy, as the products are nice things to collect, and replace when they get broken. Email marketing to an existing customer is free. Although I am finding the frequency of emails rather annoying. How many plates do they think I'm destroying? Well after today's episode of losing my work, to be fair, it could have been several! Maybe I have some Greek blood?!

I was watching coverage of Nike results on CNBC last night, and they're now selling about a third direct to end customers. I think this is the way forward for brands. It's a huge threat to Jd Sports Fashion (LON:JD.) and Frasers (LON:FRAS) I reckon, as more brands are likely to go down this route, of cutting out the middleman and instead building a relationship direct with end customers. It could also ultimately prove a threat even to £AMZN as brands take back their customers from the original disruptor, possibly?

Some of my best investments in recent years, have been companies which crack the online market. A great example is Best Of The Best (LON:BOTB) (I still hold, but have reduced my position size more recently). I doubt whether PMP is likely to shoot the lights out like BOTB has done, but it could do well if it successfully migrates more sales online. In the meantime we should start receiving divis again next year, and sleep soundly knowing that the business is strongly financed, and has demonstrated the ability to cope well with covid problems.

Not the most exciting investment idea, but it looks solid, and good value to me, taking a long term view.

I almost forgot to mention, the historic problem of grey imports into South Korea (PMP's 3rd largest market) seems to have been fixed. This is where retailers would order product at lower cost via another country, thus reducing PMP's margins.

I think the challenge for the new CEO is to get trading back on track post-covid, but then to establish a renewed upward trend in profitability. In the last few years, profits seemed to stall, despite acquisitions - meaning that the original business was going backwards. That's why the share price has fallen a lot. Maybe a buying opportunity, maybe a stagnant struggling business? Time will tell.

.

.

Character (LON:CCT)

Share price: 316p (down 2% today, at 11:08)

No. shares: 21.38m

Market cap: £67.6m

Designers, developers, and international distributor of toys, games, and giftware

The Board of The Character Group plc (AIM: CCT) (the "Board") provides the following update to shareholders on the Group's trading ahead of the publication of the Company's results for the year ended 31 August 2020.

This is a rather quaintly-worded update, but it seems to read well. Key points;

UK lockdown had considerable impact

Trading has been satisfactory

H2 should be at least as profitable as H1. I've looked up H1 figures, and it was PBT of £2.5m, and diluted EPS of nearly 10p. Therefore it sounds as if the full year FY 08/2020 should be 20p+ EPS - rather poor since the prior year was c.43p EPS - but not a disaster, considering all the problems this year re covid

Demand resilient

Expecting "steady progress" for Xmas 2020 & into 2021

Early feedback on 2021 Xmas products "extremely gratifying"

Strong balance sheet, and "sizeable" cash, plus unutilised facilities

Prospects good

My opinion - I've checked back to the last published balance sheet, and it's excellent, with over £32m in NTAV, and pots of cash, nearly £20m, less a little debt. This is therefore an unusually strongly asset-backed small cap. That greatly reduces risk for shareholders, and means you're getting a load of surplus assets in for free, the way I look at things. Plus you're not likely to be diluted, as it won't need to do any fundraisings. And/or the cash could be used to make earnings-enhancing acquisitions, or a special dividend? Lots of opportunity when a company is sitting on a lot of surplus cash.

I also like what is said in today's update about strengthening relationships with customers during this troubled period. That's important, because business is essentially all about relationships, and trust. Therefore, companies which understand this, will have used the covid period to strengthen those relationships (e.g. giving customers more time to pay, or reduce order sizes, etc). It sounds as if CCT has done that.

Broker forecasts look too high, given what is implied today about H2 being similar to H1 earnings.

This share always looks cheap, and it's been an excellent dividend payer for years, so the total shareholder return is a lot better than the share price suggests. Looks quite good to me, as a value share.

.

I'm taking a break for lunch now. Will look at a couple more things later.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.