Good morning!

Quite a few things to look at today.

- Distribution Finance Capital Holdings (LON:DFCH)

- Watches of Switzerland (ticker unknown)

- Argo Blockchain (LON:ARB)

- Watchstone (LON:WTG)

- Water Intelligence (LON:WATR)

- Character (LON:CCT)

- Superdry (LON:SDRY)

- Charles Stanley (LON:CAY)

- Versarien (LON:VRS)

Financial Reporting Council

The FRC has imposed sanctions against Laura Ashley Holdings (LON:ALY) 's accountant in relation to its work on that company's accounts for FY June 2016. Fines were reduced to reflect "an exceptional level of co-operation" by the accountancy practice and its audit partner.

I've been criticising the authorities for taking up to a decade to resolve cases such as this. Bravo to the FRC for the quick turnaround on this investigation.

Distribution Finance Capital Holdings (LON:DFCH)

- Placing price: 90p

- No. of shares: 106.6 million

- Market cap on admission: £96 million

Admission to trading and first day of dealings

The share price has popped higher on the first day of dealings for this brand new financial stock.

Distribution Finance provides working capital for businesses, in partnership with major manufacturers. Its primary customers are the dealerships who sell equipment into business. The types of things it finances include mopeds, motorbikes, RVs, marine craft, industrial and agricultural equipment.

I was interested to check whether pricing might be attractive but the admission document tells me that the company's book value at December 2018 was just £54.6 million. I don't think that any of the IPO proceeds are going to the company.

The IPO is a demerger from TruFin (LON:TRU) that is designed to help DFCH in its application for a banking license, enabling it to offer retail and SME desposit facilities.

Long-term, it is hoping to achieve ROE of 25% with a £1.2 billion receivables book. It wants to develop a wide range of working capital solutions for business - invoice discounting, finished goods financing, etc. And it will accept leverage of up to 7x.

The plans are quite aggressive but I would still be open to investing in it. 25% ROE would be a terrific result, if it can be achieved.

Unfortunately the pricing isn't cheap, with a Price/Book Value ratio of 1.6x based on the placing price of 90p. And the share price has already rallied to 118p.

So I'll be keeping an eye on this while in no particular rush to buy into it at current levels. On the watchlist.

Watches of Switzerland

Intention to float on the London Stock Exchange

This is "the UK's leading luxury watch retailer".

It has also entered the "significant, but underdeveloped US market".

You can find its showrooms in prestigious shopping locations such as Regent Street, Oxford Street, the Royal Exchange and Heathrow Airport. Several of its stores trade simply as Rolex.

Rolex, Patek Philipe and Cartier are the headliners but it supplies over 40 brands in total.

Details of placing: it might raise £155 million (gross) in new money and give an exit to certain existing holders.

Raising these funds will reduce net debt to £120 million, or 1.56x adj. EBITDA.

My view: will need to see further details. I'm very selective when it comes to retailers but I do admire the luxury sector and would be happy to learn more about this one.

Argo Blockchain (LON:ARB)

- Share price: 3.36p (-4%)

- No. of shares: 294 million

- Market cap: £10 million

The major shareholder in Argo is on the warpath (see yesterday's report). It notes with palpable anger that Argo's executives have spent £3 million since the end of March on new crypto mining equipment.

The shareholder had requisitioned a general meeting on March 28th, with the hope of forcing the company to change strategy and save its cash from being wasted. So you can understand why it's not happy about this additional spending.

I can't agree more with this paragraph. EBITDA is irrelevant:

FIH also notes that management have set out that they expect Argo “operating cash breakeven during May” and “EBITDA break-even in the second half of this year”, which First Investments strongly believes are irrelevant metrics, given that the depreciation of the crypto hardware is not included, which is currently one of the major costs to the business and, as evidenced by the Argo Announcement yesterday, is draining Shareholders’ funds at what, in FIH’s view, is unsustainable on any level.

If I held any shares in Argo Blockchain, I would vote YES to the proposals at the General Meeting.

Watchstone (LON:WTG)

- Share price: 85.1p (-5%)

- No. of shares: 46 million

- Market cap: £39 million

This holding company is preparing for trial with Slater & Gordon over the botched deal it made in 2014/2015.

The "underlying" loss it reports for 2018 is £6 million, and the total loss is £20 million.

I don't think the businesses it owns are worth much. It says that it wants to generate as much value is it can from them. Why doesn't it sell them immediately? I'm not sure why it hasn't sold them already.

The S&G trial will take considerable time to resolve - and if Watchstone loses, then it can say goodbye to the £50 million that is held in an escrow account and will also have to pay significant legal fees. The legal expenses in 2018 alone were almost £6 million.

NAV has reduced from 144p in last year's accounts to just 101p in these accounts, and more operating losses and legal expenses are almost certain to drag it lower again this year.

There is a chance that £50 million from the escrow account could be recovered, if it wins the legal battle. Against that, you have to bear in mind that the rest of the group could turn out to be worthless, depending on expenses and on how quickly they shut down/sell off the remaining businesses. Not for me.

Water Intelligence (LON:WATR)

- Share price: 368.5p (-10%)

- No. of shares: 15.2 million

- Market cap: £59 million

This US-based, international group provides leak detection and remediation services. It has been sitting on a very high earnings multiple for a while, which it has been growing into.

Growth numbers are excellent for FY 2018, as expected:

- revenues +45% to $25.5 million

This is not the same thing as "system sales" (including sales made by its franchisees to customers). System sales are over $100 mllion.

- PBT +53% to $1.8 million

Evidence of operational leverage, with profits growing faster than sales.

- The UK unit crosses into profitability for the first time

- 2019 is on track to meet market expectations

Latest broker forecasts I can see are for Adj. EPS in 2019 of 15.3 cents, rising to 17.8 cents in 2020.

Given that we are heading for half-way through 2019 already, I think it's reasonable to focus on the 2020 numbers. The current share price is equivalent to 479 cents, putting this on a prospective 2020 P/E ratio of 27x.

The December 2018 cash balance ($5.2 million) equates to 33 cents per share, so the ex-cash P/E ratio is more like 25x.

I admire Water Intelligence's ambitions. As noted before, it wants to be a "world-class multinational growth company". While such ambition is often worthy of scorn from a small company, it is rarely backed up by strong, profitable growth.

Any negatives?

- it conducts close to zero R&D. So while it considers itself a technology company rather than a support services company, it is not currently developing any new technologies. And I don't know if it actually owns any proprietary technology. It's hard to imagine that someone has a monopoly on thermal imaging.

- Many franchises have been reacquired in 2019. This is bad news for me: I prefer the capital-light franchise model to the capital-intensive corporate-owned model.

Indeed, the company understands that royalty revenue is "especially valuable" in terms of having an "optimal capital formation", but seems to have a preference for having more corporate-owned stores, anyway:

Our operating plan for 2019 will be to keep pushing sales growth of corporate locations but continue to increase margins to levels closer to that of franchisees which are typically above 20%. Hence selective reacquisitions can be a driver of the share price reflecting an organic expansion of profits and equity multiple.

The paragraph above also worries me in that management seems to have a strong interest in the share price and P/E multiple.

I prefer when management is concerned primarily with metrics like ROCE and free cash flow per share, rather than share price and P/E multiple. If ROCE is consistently strong while a company reinvests its earnings, then strong profit growth is guaranteed.

But it sounds like Water Intelligence is choosing to boost earnings in the short-run, with half an eye on its share price, even at the possible expense of lower returns and lower growth in the long-run.

Or it might just be the case that it can't think of anything better to do with the cash flow it's generating, and that's why it is buying back so many franchises. It spent $1.8 million in 2018 doing this, and $2.3 million so far in 2019.

I was tempted to open a starter position in this share today but the historical quality metrics back up what I'm saying about low returns, and I'm a bit concerned that they might not rise very far from these levels.

Don't get me wrong: I still like the company and expect it to continue generating profitable growth. Time will tell whether my concerns are valid.

Character (LON:CCT)

- Share price: 582p (+1%)

- No. of shares: 21 million

- Market cap: £124 million

Designers, developers and international distributor of toys, games and giftware

We have covered this one plenty of times before - see the archives.

This update shows good progress. Trading is in line with expectations. An acquisition made last year has suffered a setback (a bankrupt distributor), but is expected to recover.

I like the fact that Character buys back its own shares sometimes - a good thing to do when you have excess cash, a cheap P/E multiple and are confident in your trading prospects. It hasn't bought many in recent times, but has the authority to buy up to 3 million this year. That could support the share price if sentiment weakened.

I haven't got anything else to add, as little has changed.

Superdry (LON:SDRY)

- Share price: 498p (+4%)

- No. of shares: 82 million

- Market cap: £408 million

Trading performance continues to be weak; initiatives to stabilise and improve performance underway

This is very interesting. Superdry says that full-year underlying PBT is likely to be below market expectations - and yet the share price is up!

- "Global brand revenue" (the amounts paid by customers for Superdry gear including taxes and from wholesale channels) is up 3.6% year-on-year.

- Superdry Plc revenue is flat year-on-year. Wholesale is up while store sales are down.

The range of market expectations for PBT is given as £54.1 million to £59.4 million. So the actual result will be lower than this.

Julian Dunkerton is back in the (Interim) CEO position, and has taken the following actions:

- More options for sale online

- Greater density of stock in flagship stores

- Less promotional activity, enhancing margins and strengthening the brand (this used to be a hallmark of Superdry's strategy)

- 500 new products planned for first six months

Mr. Dunkerton adds a positive comment: he is "more confident than ever that we can restore Superdry to being the design led business with strong brand identity that I know it can be".

My view: I think this has an excellent chance of succeeding under Dunkerton's leadership. He still owns 18% of the company and is highly incentivised and capable. This share is now primarily a bet on his vision. Tempted to open a long position here.

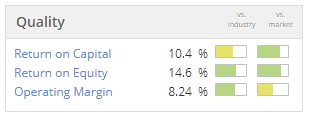

StockRanks rate it very highly in Quality and Value, though it currently lacks Momentum.

A few quick comments to finish off.

Charles Stanley (LON:CAY) - still working on its 15% net margin goal, launching a transformation project to achieve this. The jury is out.

Works co uk (LON:WRKS) - shares down 18% after guiding for adjusted PBT at the lower end of market expectations. Share price performance is minus 40% since IPO'ing less than a year ago. Might be getting into value territory but extreme caution needed.

Cambria Automobiles (LON:CAMB) - guiding ahead of expectations for the full-year. I still think that some of these dealership shares will turn out to be bargains. CAMB on a single-digit P/E.

Versarien (LON:VRS) - opens an office and a lab in North America. Announces four exciting agreements with partners to "explore" the use of graphene, "investigate" the use of graphene, "explore" combining graphene and carbon, and "establish graphene supply chain components".

And it's also taking part in a big graphene summit. And it says it's receiving a high number of enquiries.

It's little wonder that VRS is leading the way in the supply of RNS announcements.

Ok, I have to call it a day there. Paul will be back tomorrow.

See you in Mello, those of you attending!

Graham

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.