Good morning from Paul & Roland! We've been rather overwhelmed with the huge volume of updates today, so I'm going to sign off today's report, and come back to do some more work later today, and have it ready for tomorrow's report first thing.

As expected, albeit with a lower voting margin than expected, Liz Truss becomes the new PM. Let's reserve judgement until we hear what the energy crisis action is, and how that will affect companies & households, which is all that matters for our purposes here.

Agenda -

Paul's Section:

Vertu Motors (LON:VTU) (I hold) a generally reassuring H1 update, still trading in line with expectations (which factor in a halving of earnings from last year's one-off peak. An H1 weighting is expected this year. My only concern is the cost of electricity, as a fixed rate deal expires at the end of this month. I think we could have done with some better guidance on the likely impact, and whether existing forecasts can absorb this? Superb asset backing, and sector consolidation only a matter of time, so I remain happy with this share.

PCI- PAL (LON:PCIP) - very strong growth from this niche software company. It's heading in the right direction, with losses falling, but there is the nuisance of a patent infringement case, causing exceptional costs. Cash looks adequate. I had a good Q&A session with management over the phone earlier today, and this remains one of my favourite growth shares (am not currently holding, but am considering buying back in at some stage).

Roland's Section:

Alumasc (LON:ALU) - this building products business has reported a strong set of results. The shares could be cheap at current levels if the current level of trading is sustainable. However, broker forecasts suggest a 14% drop in earnings this year, so I think investors need to take their own view on the cyclical risks here.

Inland Homes (LON:INL) - a dire update from this land and housebuilding group. Inland’s founder is to depart, leaving behind expected losses and a range of operational problems and project delays. The company is also at risk of a liquidity crunch. A strategic review has been initiated to decide what to do next. One to avoid, I fear.

Luceco (LON:LUCE) (+19%) - [no section below] - after a bumper set of results during the pandemic, this wiring and electrical parts business appears to be on track to resume its pre-pandemic growth trajectory. Today’s half-year results show revenue up by 29% to £106m and pre-tax profit up 72% to £10.5m, both versus 2019 figures.

Although DIY activity has slowed, the company says that market demand for its products is stronger than current results suggest, due to destocking. Product cost inflation has been passed through and is now reversing, improving margins. New ranges of EV charging products are said to have “exciting” potential.

Trading since the end of June has been in line with expectations, and full-year results are expected to be in line with current forecasts. After this morning’s gains, that prices Luceco on eight times forecast earnings, with a 6% dividend yield.

My view: The market wasn’t pricing in such a positive outcome, and Luceco’s share price has fallen by over 70% since the start of 2022. As things stand, I think it’s starting to look like the shares may be too cheap at current levels.

I don’t think we can afford to discount the risk of a further slowdown in demand for Luceco’s products. But the company appears to be executing and trading very well at the moment. Definitely worth a closer look, in my view.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section

Vertu Motors (LON:VTU) (I hold)

45.5p (down 3% at 09:04)

Market cap £159m

The current financial year ends 28 Feb 2023, so we get an H1 (to end Aug 2022) update today -

Ahead of the announcement of its results for the six-month period ended 31 August 2022, Vertu Motors, the automotive retailer with a network of 160 sales and aftersales outlets across the UK, is pleased to announce an update on current trading.

Company’s summary -

Strong trading performance in the first half - in line with market expectations for the full year

Quite a detailed update, here are my notes -

Performed strongly in H1.

Continuing uncertainty in both supply (semiconductor shortage still limiting new vehicle production), and demand.

Expecting an H1 weighting to this year’s results.

Still trading in line with full year expectations (note that existing forecasts already bake in a substantial fall in earnings compared with last year’s one-off bumper profits).

New car volumes down on last year (which was boosted by pent-up demand).

High order book.

Stronger margins on new cars, so gross profit up despite volumes being down.

Used cars - volumes also down vs LY.

Used car prices (which shot up last year) now stabilising.

Gross profit per unit in used car sales is still high, but reduced from LY’s highs.

Aftersales - high margin, and LFL revenues are up.

Continued growth expected from new franchises.

Energy costs - this is probably the only significant negative in this update - its fixed price electricity deal ends imminently, Sept 2022. I think we need more detail on this, so a question mark is hanging over this significant issue. It’s not enough for companies to just say costs will rise, we need to be given proper guidance on the likely financial impact. Although I suppose it’s uncertain at the moment, but might become clearer in the next week, with the expected Govt support measures.

My opinion - it’s the freehold property asset backing at VTU which stands out the most.

Checking back to my notes from June 2022 here, I estimated that NTAV would be c.67-71p, taking into account H1 profits after tax. So being able to buy the shares at about 47p now, is an exciting discount to NTAV - free money, effectively.

Sector consolidation is only a matter of time, the CEO of Vertu has previously said.

It’s very obvious that consumer demand is likely to soften, although there is a counter-argument that people might order new cars now, to side-step substantial price increases in the pipeline. I’ve just ordered a new car, an Audi A4 (boring, but competent!), on a lease that is only £267 per month (inc VAT). There’s a wait of several months, but once it arrives, I’ll have a nice new car, on a modest monthly payment, fixed for 4 years, with no worries about inflation or residual values. Hence demand may not fall off a cliff, as the market seems to currently imagine, but time will tell. Most cars are sold on finance, or leases, and you could argue that they're not really big ticket items any more.

The only thing that bothers me, is the bit about utility costs. 160 large showrooms are going to cost a lot to heat & light. So there is an element of short-term risk due to that factor.

PCI- PAL (LON:PCIP)

52p - mkt cap £34m

PCI-PAL PLC (AIM: PCIP), the global provider of secure payment solutions for business communications, is pleased to announce full year results for the year ended 30 June 2022 (the "period").

What follows below is a mixture of my notes from the RNS, and a quick Q&A call with management today.

Very impressive growth here, with revenues up 62% to £11.9m.

High gross margin of 84% (up from 75% last year) - due to customers migrating to the cloud, rather than more expensive on-site software.

Adj operating loss of £(2.0)m, improved from £(3.85)m last year.

Note the exceptional costs, mainly £0.8m costs of defending an “unfounded” patent infringement claim from a competitor. This could drag on for another 2 years, and cost £2.9m, if the parties are not able to settle out of court. It’s certainly a fly in the ointment, and likely to weigh on investor sentiment unfortunately, although PCIP is robustly defending it, and management clearly think they are in the right.

The loss before tax is £(3.1)m, which includes exceptional costs, and share options charge of £246k.

Most revenues are recurring, and customer churn is low.

Balance sheet is adequate I would say - software companies don’t tend to need much tangible net assets.

Customers pay up-front, hence the business is funded on deferred income.

There’s £4.9m cash, and no interest bearing debt, which looks OK.

Cash looks adequate, and when I queried this with the company, the CFO sounded confident it’s adequately funded, and expects deferred income to keep rising (new customers typically paying 12 months up-front means the strong growth helps cashflow). Patent costs anticipated of £2.9m are spread over 24 months, so that should be affordable within existing resources.

Upward pressure on salaries for IT staff as said to have calmed considerably recently.

Energy costs are not an issue, because c.80% of staff work from home, although winter fuel bills might encourage more to return to the office.

Management are excited about new product developments.

Current trading is in line with expectations. Note that PCIP has tended to upgrade expectations as years progress, so I think the budgeting is quite prudent, and it obviously has an in demand product.

I asked whether reseller commissions are charged further down the P&L (say in admin costs)? Pleasingly, this is not the case - the revenue booked is the wholesale price charged to the reseller, so the 85% gross margin is real!

My opinion - breakeven is now within sight, and with the market cap only £34m, I can see good upside here in the next bull market. Obviously the patent case is a nuisance, and is a drag on the share price. So there is some risk from that.

I’m adding this to my watchlist for potential future buys, once the markets have settled down a bit. Probably just a small to medium sized position for me though, due to the uncertainty re the patent dispute.

The share price doesn't reflect the strong progress that has been made over the last 3 years, in my view. Although note the low StockRank.

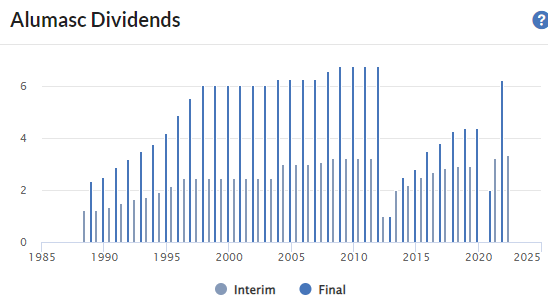

Alumasc (LON:ALU)

Share price: 165p (+9% at 0845)

Shares in issue: 36.1m

Market cap: £59m

“I am delighted to report this excellent set of results across our core businesses”

Building products group Alumasc has issued a solid set of full-year results today and the shares have responded well, up 11% as I write.

Revenue from continuing operations are up by 15%, while underlying pre-tax profit is 27% higher for the year ended 30 June.

Management also appears to be relieved to have ditched the loss-making Levolux business, and reports a confident outlook for the year ahead.

I can’t help feeling a degree of concern about the cyclical risks here. I’m also disappointed by the level of shareholder value destruction resulting from the sale of Levolux. As Paul explained recently, Alumasc is effectively paying the buyer to take the company away. while also swallowing a £15m impairment charge.

However, the Levolux acquisition dates back to a previous property boom – 2007 – so perhaps it’s right that Alumasc’s current management is determined to move on and focus on its core businesses. These are geared towards product supply, rather than design and fit.

Today’s results certainly seem to justify some confidence, in my view, if market conditions remain stable.

Operational highlights: Alumasc reports encouraging growth across all three of its operation divisions, all of which appear to enjoy decent pricing power.

- Water Management: record revenues of £47.6m, up by 24% from 2021. Operating profit rose by 43% to £8.8m, another record. This implies an 18.4% operating margin.

- Building Envelope: revenue up 4% to £29.4m, underlying operating profit unchanged at £3.6m (12.2% margin)

- Housebuilding products: revenue +12% to £12.4m, operating profit £2.4m. That’s a 19.7% operating margin, which is a solid result. But this business generated a margin of 23% last year, so perhaps there are some cost pressures at work?

Financial highlights: Today’s results highlight growth across the group’s continuing operations, together with a welcome reduction in pension deficit payments.

- Revenue +14.9% to £89.4m

- Pre-tax profit from continuing operations +27% to £12.0m

- Net loss including discontinued operations: (£7.1m)

- Net debt up £3.8m to £4.7m

- Adjusted earnings up 27% to 28.6p per share

- Full-year dividend up 5.3% to 10p per share

- Pension contributions reduced from £2.3m to £1.2m pa from October

Balance sheet/cash flow: The balance sheet looks healthy enough to me, but my sums suggest that the dividend of £3.6m is only just covered by free cash flow from continuing operations. On a statutory basis (including discontinued operations), the payout isn’t covered at all.

Free cash flow has been depressed by inventory builds and working capital movements. This may not be a concern if trading remains stable and supply chain conditions return to normal. However, if we do see a cyclical downturn in this sector, I wonder whether Alumasc might (once again) be forced to cut its payout.

At this uncertain stage in the cycle, I’d prefer to see a more robust level of free cash flow dividend cover.

Outlook: Despite the “uncertain macroeconomic outlook”, the Board reports a “robust start to FY23” and has confidence in the future.

However, updated forecasts from house broker FinnCap suggest adjusted earnings could fall by 14% to 24.2p per share this year, before stabilising in FY24. This outlook appears to be driven by cost inflation and slowing revenue growth.

Notably, FinnCap is forecasting a significant improvement in cash generation, so perhaps my concerns about the dividend are unwarranted. This updated note is available on Research Tree; thanks as always to FinnCap for making these available to the investor community.

My view: After this morning’s share price gains, Alumasc is trading on about seven times forecast earnings, with a 5.9% dividend yield. That could certainly be an attractive valuation for a business with stable finances and double-digit operating margins.

The main risks I can see are cyclical; are we about to see a slowdown in the construction sector?

I’m naturally bearish, but have often been wrong on this front. So I’m withholding judgement, at least until we learn more about the new government’s plans for financial support.

Ultimately, I think this is a DYOR situation. An investor who calls the macro outlook right could do well. But if we do get a cyclical downturn, Alumasc’s results could be much worse than anticipated.

Inland Homes (LON:INL)

Share price: 20p (-27% at 0900)

Shares in issue: 224m

Market cap: £44m

Retirement of CEO, strategic review and trading update

Commiserations to anyone holding Inland Homes this morning. The shares have collapsed after a profit warning which has created more questions than answers, in my view.

Here’s a summary of the current position, as far as I can tell.

CEO resignation: Founder and chief executive Stephen Wicks is to retire, and will step down on 30 September, although he’ll be available for another 12 months.

Strategic review: the company makes much play on its credentials as a brownfield land regeneration specialist. In today’s update, the company says that the gross development value of its land bank is “in excess of £2.7bn” (September 2021: £3bn).

However, Inland says that “the continual deterioration of the planning system has presented Inland Homes with challenges in predicting the timing of planning permissions and thus the realisation of asset values”.

As a result, the board has decided that “this is an appropriate time to conduct a strategic review of the business”. As a result, the current share buyback programme has been suspended.

Trading update: Some big land sales appear to have run into delays. The company said that it had expected to book £75m of land sales by the end of the financial year (30 September).

According to management, “there is now a question on the legal completion date”. It seems likely that some or all of these sales will now slip into the next financial year, resulting in a big hit to expected profits.

Confusingly, the company says that the sale of these assets will now be reviewed as part of the strategic review to maximise shareholder value. This seems to suggest that the sales might not go ahead at all.

In addition, the company says that the performance of its contract income and housebuilding divisions have “not been satisfactory for some time”. Cost inflation appears to have run out of control and has not been successfully managed.

As a result, an investigation commissioned by the board has concluded that the group is expected to make an operating loss of £29.3m for the year ending 30 September. Previous forecasts I can see were for an operating profit of £23m.

However, the company says that they’ve also reached an agreement in principle for a land sale that would generate a profit of £25m. If this completes by the end of September, this year’s operating loss could be reduced to c.£4m. Sounds a little desperate, to me.

Debt risk: Net debt is said to have been reduced from £148m in September 2020 to under £100m today. However, that still represents a 69% LTV against the company’s revised NAV estimate of £146m.

I’ve often wondered at Inland’s high level of debt. Most housebuilders have completely deleveraged after a 10-year boom, keen to avoid the problems they had in 2008.

Inland’s high leverage now appears to be causing problems. The company warns that there’s a risk that it could breach its interest cover covenant with one lender, to whom it owes £19.3m.

The lender is expected to agree to a waiver, but with such uncertainty on future revenue, I see this as a significant risk.

My view: I wonder if this is a situation where an overbearing founder has evaded effective board oversight until it’s too late.

Today’s update suggests to me that some of these problems have been known about for some time within the business. Shareholders have been kept in the dark – the company’s half-year report in June left full-year guidance unchanged.

Personally, I see the shares as uninvestable at the moment, given the level of uncertainty about the outlook.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.