Good morning, it's just Paul here today, as Jack is sick - get well soon Jack! Today's report is now finished. Wishing you a delightful very long weekend!

Agenda - it's quiet today, but I'll look at a couple of catch up items, so there should be a full report up by 1pm.

Missguided - has been bought out of administration by Frasers (LON:FRAS) not Boohoo (LON:BOO) (I hold).

Parsley Box (LON:MEAL) - revenue guidance for this year is reduced, but little change to guidance for heavy losses. This looks a basket case to me, but probably has enough cash to keep going for maybe another 2 years?

On Beach group (LON:OTB) - I check out its interims to 3/2022. Still impacted by omicron, it only reached breakeven in H1. The future's looking more bright though. Could be quite good, but lots of travel shares look cheap now, so I'd be inclined to look at a few, and maybe buy small positions in several? Balance sheet is adequate, but it's good to see customer deposits ring-fenced in a trust account.

Victorian Plumbing (LON:VIC) - I have a quick look at recent interims for this bathroom supplies eCommerce business. Can't make up my mind whether it's any good or not.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Missguided update - according to the Retail Gazette here, Frasers (LON:FRAS) has emerged as the buyer (out of administration) of fast fashion failure Missguided, for just £20m. I’m a bit disappointed that Boohoo (LON:BOO) (I hold) didn’t take out a competitor, but they obviously decided it wasn’t worth it.

Frasers has issued an RNS this morning as follows -

Frasers Group plc ("FG" or "The Group") announces that it has acquired certain intellectual property of the online women's fashion retailer, Missguided Limited (in administration), Mennace Limited (in administration) and Missguided (IP) Limited for a cash consideration of £20 million. Following completion, the business will be operated by the administrator under a transitional agreement for a period of approximately 8 weeks. It is then the intention that Missguided will operate as a standalone business within the Group.

Michael Murray, Chief Executive of Frasers Group, commented: "We are delighted to secure a long-term future for Missguided, which will benefit from the strength and scale of FG's platform and our operational excellence. Missguided's digital-first approach to the latest trends in women's fashion will bring additional expertise to the wider Frasers Group."

Parsley Box (LON:MEAL)

18.5p (yesterday’s close)

Market cap £13m

Parsley Box Group plc (AIM: MEAL), the direct to consumer provider of ready meals and other products focused on the 65+ demographic, today issues an update on trading for the first 5 months of 2022.

This update tries to sound upbeat, with progress having been made on product availability, and gross margins.

Marketing spending is now more focused.

Losses are reducing, but still considerable.

Average order values rising over 10%.

On the downside, volumes have been below expectations.

Lowering revenue guidance to £22.5m for FY 12/2022 (the StockReport is currently showing £25.5m)

EBITDA guidance is little changed, at a loss of £(4.0)m for the current year, which is £(4.6)m at the PBT level.

Cash - we’re just told it is well funded, but no figure given. It raised £6.1m in March 2022, at 20p per share.

My opinion - MEAL has bought itself more time, to try to make this concept work. I don’t mind loss-making companies, if they’re demonstrating strong growth, and a clear trajectory towards profitability. That’s not the case with MEAL, since revenues are falling, and losses remain considerable, at about 20% of revenues. So that would need a big rise in revenues to get to breakeven. That’s just not realistic.

So all the signs now are that MEAL probably staggers on for another 2 years maybe, then runs out of money again, with little to no commercial progress made.

The reality seems to be that MEAL addresses a very niche market. Its main point of difference being small ready meals that can be kept at room temperature. For everyone else, then supermarkets and other online companies (such as the excellent “COOK”) provide far better value meals, which can be stored in a fridge or freezer.

Hence I think there’s a possibility MEAL might be able to scrape its way to breakeven (but needs heavy cost-cutting to get there), but there’s clearly not an opportunity here for it to scale up into a bigger business - the product is far too niche. They've tried, with massive marketing spend, and it's not worked.

Every time I’ve mystery shopped MEAL, the product has been very erratic - some items were quite tasty, others were (to be blunt) appalling - with so little meat content in the beef dishes, that they were more like a soup than a meal. For that reason, I suspect MEAL will have surprised most customers on the downside, which is why revenues are falling.

This has been one of the worst recent floats, and it's joined the 90% down club. I recall in the 2000-2002 tech crash, many shares that joined the 90% club went on to become members of the 99% club. MEAL looks a prime candidate for that, over the next couple of years. However, things can change, so I'll keep an eye on it. Trouble is, the current £13m market cap is all I would be prepared to pay if MEAL does manage to reach a modest level of profitability. So the upside is already baked in, but the downside scenario looks by far the most likely outcome. Hence risk:reward looks terrible, and it's best avoided.

.

.

On Beach group (LON:OTB)

204p

Market cap £336m

Sector & macro thoughts - I’m interested in the holiday sector right now, because share prices seem to be low again, despite the pandemic receding and people prioritising holidays again.

Also, the data suggests to me that the cost of living crisis is hitting the poor hardest (e.g. benefits/state pension upped by a miserly 3.1%, versus inflation rate c.11% for the poor [due to food & energy being a high % of outgoings]).

Whereas those in work, and especially middle class, are seeing a lower rate of inflation c.7%, and the latest ONS data (published 17 May 2022) shows that average weekly earnings have shot up to +7.0% year-on-year, in March 2022 [source].

Therefore, that data demonstrates that there isn’t any real income squeeze at all on many people in work, particularly in the middle and upper income segments.

Unemployment is extremely low, at only 3.7% [source: ONS], which enables people to shop around for higher wages with a new employer. I remember reading somewhere that on average when people change jobs, they get 12% higher pay.

Therefore, my assertion is that the cost of living crisis is not actually a crisis for most people, and they want holidays, having been denied them during the pandemic.

Having to pay staff a lot more, is likely to hit profitability at many companies. So I am worried about profit warnings. However, I’m less worried about a fall in demand. Companies offering value for money product/services, or having some other form of pricing power, should be OK. Hopefully! Nobody really knows for sure. The words of Premier Miton (LON:PMI) in its recent results stuck in my mind - that a whole generation of investors are now navigating uncharted waters, since we’ve not had to worry about inflation for about 30 years. I can remember the impact of inflation in the 1970-80s, but wasn’t investing at the time, so have no idea which companies it impacted the most. Plus there were lots of other problems at the time which muddied the waters.

Anyway, those are my half-baked ideas which are pushing me towards potential bargains in holidays, retail & hospitality sectors. Have the falls in share prices been overdone, I wonder? Last year’s dogs can become oversold, and provide the next year’s buying opportunities, sometimes. Stock market sentiment can change in the blink of an eye, so who knows?

Covering the 6-months ended 31 March 2022 - which would have seen prior year comparatives suffering from the last lockdown.

Also, it’s the winter season, which would be seasonally weaker, due to OTB as its name suggests, focused on summer holidays mainly. Although checking the handy Stockopedia H1/H2 results table here, shows that there was an H2 bias to profits (taking into account the “unusual expenses” line, which seems to hit H2 mainly. Although not as big an H2 bias to profits (pre pandemic) as I would have expected. Then of course it’s a sea of red ink in the periods hit by the pandemic.

H1 revenue is £52.9m, up hugely against LY of course, but down 17% on the previous (pre pandemic) H1 2019

Profits? Nothing, just breakeven for H1 this year, which is poor against £15.7m H1 profit pre-pandemic. That’s using favourable adjusted figures. The statutory loss is £(7.0)m before tax in H1.

No divis - fair enough, it’s too early for that, whilst the business is still bouncing back from covid.

Travel restrictions - were only relaxed in Jan 2022, so that would have restricted results in H1 to Mar 2022. Omicron hit sales in Nov-Dec 2021 & early 2022. Fair enough, so these numbers are not representative of the hopefully better future run rate without restrictions, so let’s not get too bogged down in them.

What matters is the outlook, and how the balance sheet is looking.

Outlook -

Summer 2022 sales well ahead of pre-covid (up 22%, and accelerating to +33% in last 8 weeks to 22 May).

Visibility is limited (some customers booking late), cautious & don’t know how cost of living crisis will impact bookings.

Attracting more premium customers.

Recent relaxing of Spain restrictions should help late bookings.

Expecting profitability in H2.

Balance Sheet -

NAV is £147.6m. I’ll deduct £73.3m intangible assets, making NTAV £74.3m. That means there’s little asset backing for a market cap of £336m. Not necessarily a problem, but the valuation of this share rests largely on earnings & cashflow, not on asset backing.

Customer deposits are ring-fenced, in a trust account, and shown separately on the balance sheet as £99.1m “Trust account” within current assets. That’s good, prudent accounting, and should mean customer deposits are safe.

The company’s own cash is modest, at £16.8m, but £75m bank facilities (undrawn it seems) look ample.

Dilution - I’d say this is a not particularly strong balance sheet, but it looks adequate, and the risk of dilution doesn’t seem great, although you can’t rule out management deciding to do another raise if they want to spend big on marketing at some point. As long as that was less than 10% dilution, then I wouldn’t worry too much about it.

Note that dilution did happen in the pandemic, to prop up the company - the share count was 131m before covid, and is 165.9m now - enlargement of 27%. Therefore, when you look at the share price, don’t imagine the share price would necessarily recover fully to pre-covid levels, as that would represent a 27% higher market cap. People often overlook this point, when drawing lines on charts, but it’s very important for valuation purposes to check the share count carefully.

My target share price - By my calculations, as the share count is 27% larger now, then EPS (if profit rises to the same in £ terms as pre-covid) would be 21% lower. Therefore, logically the share price should be 21% lower than pre-covid, if profit fully recovers.

The 200-day moving average share price was flat around 430p in 2019, so take 21% off that for dilution, suggests to me that if OTB returns to pre-covid profits, and the same PER, then our target price would be c.340p. That’s about 67% upside on the current share price, which looks quite attractive to me.

However, investors might not be prepared to pay the same PER as pre-covid, as we now know how vulnerable travel shares are to any future lockdowns. So investors may want a significant discount in future. Hence that 67% upside figure looks rather optimistic in that light.

Broker forecasts - are low at 7.1p EPS for FY 9/2022, which is fine because we know H1 was only breakeven, due to covid restrictions.

FY 9/2023 is forecast at 17.6p - which looks achievable to me, assuming no more restrictions. That would be a PER of 11.6 - reasonably OK, but given the risks, I’m not sure that’s a compellingly cheap price.

My opinion - this looks quite good for a recovery, but there might be more compelling value in other travel stocks. Hence I’d be inclined to review a selection, and maybe buy a few small positions in several travel shares.

As the problems at airports are showing, it’s likely to take the travel sector a while to properly recover from the damage done by the pandemic.

Chart looks like it might be limbering up for a bounce, possibly?

.

Victorian Plumbing (LON:VIC)

72p

Market cap £234m

I’m having a quick look through interims for this online specialist bathroom retailer, to see if it’s a potential bargain, having crashed about 75% from an opportunistically over-priced IPO

Looking through our previous notes here (links below are to SCVR articles, not the RNS) -

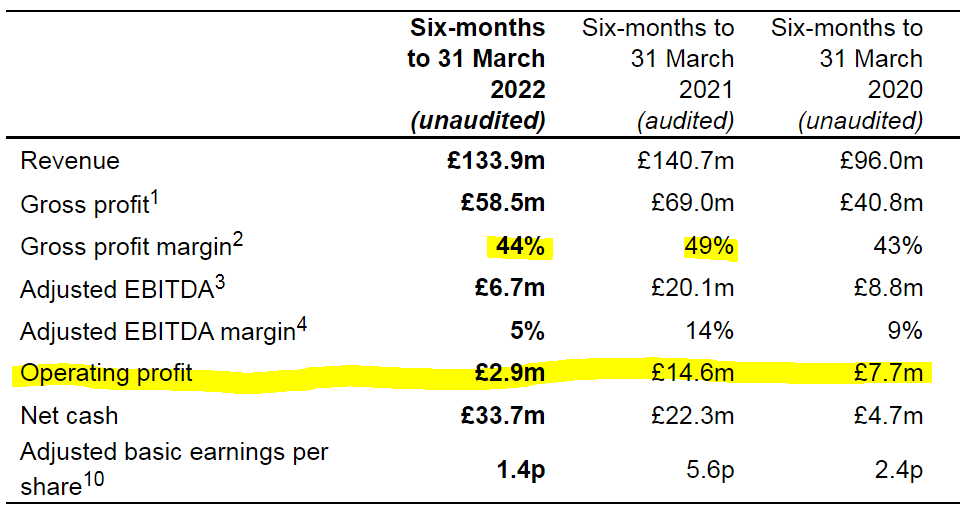

9 Dec 2021 - I first looked at VIC (this is quite a good intro to the numbers), and liked the strong FY 9/2021 results, but it came with a profit warning, with the company flagging that exceptional gross margins of 49% in the pandemic would drop back to more normal 44%. I was tempted to have a dabble at 99p, but thankfully didn’t.

24 Feb 2022 - a mild profit warning that Jack covered, caused by higher costs.

This table below sums things up nicely - a big boost from the pandemic caused a DIY boom in lockdowns - revenue & profit margin both up considerably. These numbers were used to fuel an over-priced IPO.

This year H1 shows the company has held on to most of the revenue growth, but gross margin has returned to normal. Costs have increased, resulting in profitability (at both EBITDA and operating profit) now well below pandemic levels. This is not good. The commentary says that it had to absorb more costs in order to hang on to market share. I don’t like that. We’re looking for companies with pricing power right now, which VIC doesn’t seem to have. Also it spends massive amounts on marketing, suggesting quite a lot of one-off purchases, rather than loyal, repeating customers -

.

Outlook - doesn’t fill me with confidence -

Revenues in H1 2022 were in line with recent guidance and reflect the lower demand compared to the same period last year when the UK was in a lockdown environment. The Group focused on increasing market share and invested more heavily in marketing in the early part of H1 2022 to successfully drive market share gains. That marketing spend has now normalised as planned.

The Group expects to deliver modest year-on-year revenue growth through the second half, as previously guided in the AGM statement on 24 February 2022. There are well reported ongoing inflationary cost pressures and we remain acutely aware that our customers are also managing these pressures. The Group will therefore continue its careful approach to price rises through the second half of the financial year.

That sounds like the customers have the whip hand.

Marketing costs - are a staggering £40.2m in H1, which is spending most of the gross profit (£58.5m). If VIC can find a way of achieving better returns from a smaller marketing budget, then profits could soar. Is that feasible though? Or does it have to keep recycling most of the gross profit into marketing, just to stand still?

Surely it would make more sense to slash selling prices, and also slash the marketing budget, and become known as the lowest cost seller where customers will go automatically? Maybe it’s not that simple. Although with a marketing budget that is 30% of revenues, it does suggest there might be some mileage in my idea - slash the selling prices by 30%, and rely on just emailing the existing database (free) with compelling everyday low prices.

Balance sheet - looks sound, but NAV is only £35.0m. NTAV is £31.9m. So not much asset backing.

My opinion - the market cap of £234m still looks quite high, now there’s quite low visibility of earnings in future, now we know the prior year profits were a one-off boost from covid.

The Stockopedia numbers look unappealing below, so I think there would need to be a significant out-performance against current forecasts to propel shares sustainably higher.

It’s a very competitive sector, you can get bathroom fittings from so many places. With such a huge marketing budget, maybe VIC could be a long-term winner?

I can’t decide, so will just be neutral on this one.

.

.

.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.