Hi, it's Paul here.

Good morning! I'm settling into a pattern of writing from late morning, through to tea time, which works best for me. Therefore today's report estimated time of completion is 5pm.

Update at 16:57 - today's report is now finished. I decided to have a bit of a ramble about macro stuff in the last section about PEB, so will check it for spelling & grammar mistakes next (I type fast & inaccurately when something interesting crops up!), and then invite your comments!

I see we have 1 or 2 subscribers who insist on giving each report a thumbs down, every day, late morning, presumably because they are displeased that the report isn't complete by then. We agreed some time ago (overwhelmingly supported by readers at the time) that I would take my time writing these reports, and not rush for any deadline.

Therefore if you want to see a completed report, please come back at the indicated (above in bold) completion time. Thanks.

BOTB

Share price: 288p (up 6% today, at 11:12)

No. shares: 9.38m

Market cap: £27.0m

(at the time of writing, I hold a long position in this share)

Trading update (AGM statement)

Best of the Best PLC, (LSE: BOTB) the online organiser of weekly competitions to win cars and other luxury items...

Trading seems to be going well;

The Group is pleased to report that the positive momentum to the start of the year, reported at the time of the full year results in June, has been maintained and the Company has continued to make good progress and is trading comfortably in line with market expectations for the current financial year.

I'm not a fan of the phrase "comfortably in line". Surely that must mean: slightly ahead? In which case why not just say so?

The last physical airport site has now gone. Therefore BOTB is now an online only business, which makes it simpler to manage. The physical sites had a different business model - high ticket prices, as one-off purchases. So that wasn't really compatible with the online model of much cheaper tickets, to encourage frequent purchases by customers.

Note that the gradual closure of the physical sites in recent years actually masked the stronger growth coming from online operations. With those sites now all gone, this means that the top line growth rate could now accelerate - a trigger for a possible re-rating, perhaps?

Valuation - the latest house broker note (available on Research Tree) shows 17.0p for FY 04/2020. Although it notes today that there's possibly upside on that, given today's favourable RNS. That's a PER of less than 16.9 - which strikes me as excellent value, for a small, but decently growing, profitable & cash generative online business, with recurring revenues, that operates in a niche of its own. Its market is global, now it's online only, so there's almost limitless growth possible.

My opinion - I remain a happy, long-term shareholder here. The company has paid out loads of dividends in recent years, including specials. In drawing sensible salaries too, management has proven thoroughly decent, by treating minority shareholders fairly. Therefore I trust management to look after my & other small shareholders' interests. That matters a lot, as there are plenty of rogues around on AIM, as we know.

An adverse tax ruling has dented forecasts a little, but the company seems to have taken that in its stride (meaning that underlying growth is stronger than reported growth). Marketing spend can be dialled up & down as required, so the business is nicely set up, in the event of a recession. I get the impression that management is learning & improving what online advertising works best.

It's a pity the shares are so illiquid, so it takes time to build up, or unwind a shareholding here.

The valuation currently looks very appealing to me - it's a GARP share (growth at reasonable price) in my view.

S4 Capital (LON:SFOR)

Share price: 139.25p (up c.1% today, at 12:15)

No. shares: 365.1m

Market cap: £508.4m

About S4Capital

S4Capital plc (SFOR.L) is a new age/new era digital advertising and marketing services company, established by Sir Martin Sorrell in May 2018.

Its strategy is to build a purely digital advertising and marketing services business for global, multinational, regional, local clients and millennial-driven influencer brands. This will be achieved initially by integrating leading businesses in three practice areas: first-party data, digital content, digital media planning and buying, along with an emphasis on "faster, better, cheaper" executions in an always-on consumer-led environment, with a unitary structure.

This one is a bit bigger than the usual companies I look at, but the Martin Sorrell factor makes it particularly interesting;

Sir Martin was CEO of WPP for 33 years, building it from a £1 million "shell" company in 1985 into the world's largest advertising and marketing services company with a market capitalisation of over £16 billion on the day he left.

Therefore, his latest venture, S4 Capital is being closely watched. Sorrell is very scathing about conventional marketing, saying that it's had its day, and digital is the only area of interest to him now.

I looked at its last few trading updates, and thought they sounded a bit rampy, trumpeting top line growth, but saying little about profitability. Hence I decided to reserve judgement until the next figures are issued, which has happened today.

Interim results -

Revenue growth is strong;

Revenue was £87.97 million, up 41.6.% from £62.13 million on a pro-forma basis in the comparable period in 2018 pro-forma.

Operating profit - this is where it gets tricky to analyse. The statutory figures show a big deterioration from a profit of £12.2m last time (pro forma, to strip out the effect of timing of acquisitions), to a loss of -£6.2m this time.

Adjusted profit - there are nearly £15m of adjusting items, which improves this year's H1 to an H1 adjusted operating profit of £8.7m (although even the adjusted figure is down on last time's £12.3m). The company explains that it is in a dash for growth, hence is loading up on headcount to achieve further growth.

Adjusting items - are highly material, so needs scrutiny, see note 1 to today's accounts. These are the adjusted items;

Amortisation charge relating to acquisitions of £6.3m. That's fine to adjust out, in my opinion, and this is standard practice with most acquisitive groups. The book entries for goodwill & amortisation are irrelevant when it comes to valuing a company & assessing its underlying profitability.

Non-recurring expenses of £8.7m is the balance of the adjustment to profits. So what's in this total? Sub-note 1 tells us;

Non-recurring expenses relate to the total expenses for acquisitions of £ 7.4 million and share based compensation of £ 1.3 million. In addition, there is a (deferred) income tax credit of £ 1.3 million.

Since the group has been making large acquisitions, then expenses of £7.4m sounds reasonable to me.

The only item I normally quibble over, is share based compensation, which is really remuneration, and should therefore be expensed, in my view. But £1.3m is not terribly significant relative to the total figures.

Overall then, it seems to me that the adjusted profit is probably acceptable as a means to measure performance & valuation, in this case.

Sector thoughts - It's worth pointing out that PR/marketing companies are in the business of polishing things to appear better than they are. This often extends to their own accounts too, in my experience! They just can't help themselves. Therefore more than usual scepticism is required when investing in this sector.

Another sector risk is that marketing spend is often the first thing that companies cut back on, when recession bites. So if you have a negative macro view, then this sector is probably best avoided.

Balance sheet -

NAV: £334.3m

NTAV: is negative, at -67.6m - this is due to the humongous £401.9m intangible asset line, created when it made some large acquisitions. I don't normally like investing in companies with negative NTAV, but it can sometimes be acceptable if they are highly cash generative.

Overall, I'd say the balance sheet is weakish, but not alarmingly so.

Valuation - I think it's best to rely on broker forecasts, as we don't have a lot to go on re historic results, as this is a newly created, rapidly growing group.

The lastest figures I have are 5.4p EPS for FY 12/2019, and 8.5p EPS for FY 12/2020.

At 139p per share, that gives PERs of 25.7 (expensive), and 16.4 (more reasonable).

Therefore, if forecasts are likely to be achieved, then this share could be worth a punt.

There again, rapidly growing groups are not necessarily best valued on short term profitability. It can be all about creating the groundwork for a much bigger business in future. That's something to consider.

The Sorrell factor is another quandary for investors to consider. No doubt there are plenty of investors who are essentially backing his experience & judgement, rather than the short term results. He's getting on a bit in years, and his style may not be to everyone's taste, but it's difficult to argue with his track record.

My opinion - I like the whole digital marketing space, and Sorrell is an industry heavyweight. Therefore it's really tempting to just buy some S4 Capital shares, and tuck them away for the long term.

I can't see anything awful in the figures today. The adjusted profit looks OK. The balance sheet is weakish, but not a deal-breaker.

Overall then, this gets a cautious thumbs up from me.

The spike in price in Sep/Oct 2018 seems to have been a speculative frenzy when the new group was set up:

Epwin (LON:EPWN)

Share price: 80p (up 6% today, at 14:16)

No. shares: 142.9m

Market cap: £114.3m

Epwin Group Plc (AIM: EPWN) ("Epwin" or the "Group"), a leading manufacturer of low maintenance building products, supplying the Repair, Maintenance and Improvement ("RMI"), new build and social housing sectors, announces its half year results for the six months to 30 June 2019.

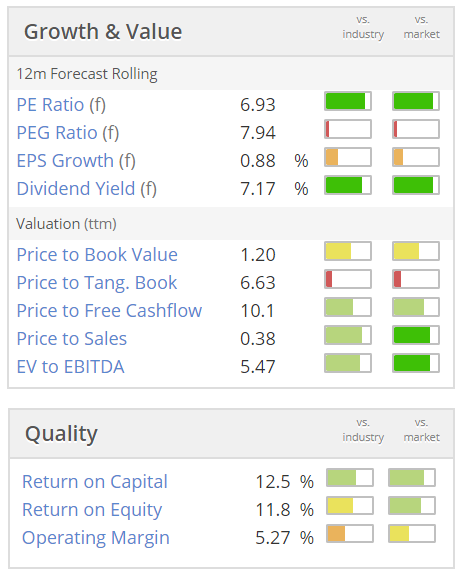

A quick look at the StockReport here suggests that this could be an interesting value share: low PER & high yield;

It's very unusual these days to find a dividend yield (7.17%) higher than the PER (6.93), and when you do - it's usually a sign of trouble!

Maybe Epwin could be an exception to that?

Outlook - sounds good - this excerpt below is the key part, with more detail available in the RNS for anyone interested in digging deeper (remember, my comments here are just a review);

The Group made an encouraging start to 2019 and trading since the half year has continued in line with expectations.

Price increases have begun to mitigate the significant material cost inflation experienced during 2017 and 2018, we have seen stable volume in our core products and the initial benefits of our footprint reshaping are coming through.

The Board anticipates adjusted profit before tax for the full year to be in line with market expectations.

However, despite the external environment, the Board remains confident that the actions it is taking to strengthen the Group's position by consolidating the footprint of its manufacturing operations and focusing it towards the higher margin extrusion and moulding operations, which have technological and investment barriers to entry, will deliver an improving financial performance.

The Group remains well placed in its markets, with sound prospects for the future, supported by our confidence in the medium and long-term drivers of the RMI market.

I particularly like the comments above about recouping previously absorbed (by Epwin) cost price inflation. I've come across this many times, both as an investor, and running a business myself (as part of a team). It is often the case that, in the short term, input cost increases have to be borne by a company, thus reducing its profit margins. However, over time, customer contracts are re-negotiated, and providing you present a good case to the customer as to why prices have to go up, normally they're pretty reasonable about it. Especially as competitors are also quoting higher prices, since they are also subject to higher input costs.

Therefore, there is typically a time lag when input prices rise sharply, which companies then gradually recover, in future, through price rises. It looks like Epwin is in that situation now - which makes the shares potentially attractive.

Purchase, sale & leaseback - this sounds interesting;

The Group's financial position remains strong, with good cash generation in the half year and net debt of £29.2m, representing 1x adjusted EBITDA.

Furthermore, the arm's length transactions to acquire, sell, develop and lease the new Telford warehouse and finishing plant, which are expected to deliver circa £8.0 million of surplus cash to the Group in the current year, will significantly reduce the Group's debt. This gives the Group significant funding headroom to continue to invest in the business and progress with its strategy.

I think investors need to look at this closely. Interest rates are incredibly low at the moment. Therefore, signing a lease at potentially a high implied rate of interest, may not be the right thing to do at all. It could lock in a high funding cost.

It might be a lot better to buy the freehold, and then put that into a SPV with a long-term, fixed rate (ultra low) interest rate, with no recourse to the group.

Investors might want to look into this & question the logic of it. Generally, I'm not keen on sale & leaseback type arrangements, to reduce gearing, as it can often mean committing to excessive future rents.

Again, I'm not judging this - merely flagging it to readers as something you might want to look into in more detail, if considering a purchase. More recent subscribers might not know that Graham & I just offer a review, and personal comments, on company results. We're never recommending, or tipping things. We leave that to the spivs elsewhere!

Balance sheet - usual key figures;

NAV: £86.9m, which includes £76.1m intangibles (ignoring the daft new right of use leasehold asset)

NTAV: £10.8m - I'd like this to be stronger, but it's not a deal-breaker.

My opinion - as with several companies I've reviewed this week, my preconception was negative (typically caused by previous disappointing results), but on scrutinising the latest numbers & commentary, I'm left with a more favourable view.

In terms of macro - it seems to be focused on products for housebuilding & maintenance, which are not likely to decline in volume any time soon. Also, the weaker sterling should help make it more competitive versus imports. As always though, macro comments & assumptions are little more than educated guesswork.

In conclusion then, I give Epwin a cautious thumbs up, and think it looks worthy of a closer inspection.

Pebble Beach Systems (LON:PEB)

Share price: 7.15p

No. shares: 124.6m

Market cap: £8.9m (NB. note the net debt of £9.0m)

Interim results yesterday show a good turnaround at the P&L level. However, the balance sheet is laden with way too much debt, so that will need to be refinanced at some point. Extremely high risk.

That said, with interest rates so low, banks are often happy to let struggling companies tread water, and trade their way out of problems, which makes sense for everyone concerned. They used to be called "zombie companies", but we hear that phrase very little today. The world has never seen sustained, ultra-low interest rates before. So we're in uncharted territory. It probably won't end well, as sooner or later, credit is likely to be withdrawn. Unless the banks are nationalised, and it becomes policy to continue extending un-repayable debt? e.g. China. That actually makes debt repayable (as it becomes re-financable), bizarrely. So who knows?

As an aside, I make a conscious effort now to stop using the artificial certainty of the word "will". e.g. this will lead to that happening. The reality is that all commentators are guessing. Very few people accurately predict the future, in fact hardly anyone does. Therefore, when I read commentary, I like to hear a bit of modesty. Since my decision to extinguish my strident, and rather angry Twitter personality, being aggravated and perturbed about almost every aspect of modern life, I'm trying to re-phrase comments more in terms of: this might happen, or that might happen.

Commentators who are certain that this or that WILL happen, are almost certainly going to be wrong. For reasons unknown, or not imaginable. When people predict things, they rarely have insights. They normally just extend current trends ad infinitum. e.g. we all know that the economy is cyclical. Yet, when the first signs of a downturn start, how many brokers start predicting an operationally geared downturn in earnings? Hardly anyone! They just keep the existing spreadsheets with a 10-20% growth in earnings, which don't make sense any more.

All I would say, is that history shows clearly that when people start to think conventional financial rules don't apply any more, then you're at or near the top of a bubble, with a huge crash impending. Why? Because cheap credit means that credit is mis-allocated, and creates over-supply through over-investment. Think too many glitzy but uneconomic restaurants (Jamie?), too many new hotels, too much of everything. As they become loss-making, and go bust, then banks withdraw credit from vulnerable sectors, which triggers a wider recession, as staff and suppliers begin to lose out.

Back to Pebble Beach: there are some smallish Director buys announced today.

My opinion - neutral. I'm just flagging this as a potentially interesting share, for turnaround specialist investors to possibly have a look at. I like the revenue growth, and upbeat commentary - so I see signs of life in the figures.

It's a bit too high risk for me personally, given the heavy debt burden on the balance sheet. Although it's tempting to have a small punt on PEB shares, in case the turnaround does take hold. At this stage, I would not invest anything more than fun money, as the risk of a 100% loss still looks quite high, albeit reducing following improved figures.

Closing comment - I realise that things are changing rapidly, but we must be one of the first (and possibly last) societies which ignores the wisdom of people who have lived the longest, and seen & done the most, and instead elevates the naive idealism & simplistic views of children.

Best wishes, Paul.

(P.S. if you don't put out the recycling bin, I'm telling Greta Thunberg!)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.