Good morning , Graham and Megan here this morning as Paul is off.

Summaries

Allied Minds (LON:ALM) (£26m) (-42%) [no section below] - let’s put a full stop on the story of Allied Minds. This was a Woodford-backed venture which at one point in 2015 had a market cap of over £1.5 billion. It’s a collection of blue-sky technology investments, as the underlying companies have typically been in the research phase, i.e. quite a long way from generating any revenues. The thesis was that at least some of these investments would succeed, and that a patient, long-term ALM shareholder would do well. Unfortunately, we have now arrived at the long-run destination and it’s a possible delisting: “the costs of maintaining a premium listing on the Official List and the Main Market of the London Stock Exchange are now prohibitively high”. Cash has dwindled to $9.7m (December 2021 balance sheet) plus a few million dollars from a disposal. ALM’s portfolio now has just five companies and it is surely a matter of time before ALM winds itself up - whether or not it keeps its LSE listing.

Sopheon (LON:SPE) (£68m) ($80m) (-1%) [no section below] - This enterprise software group shows an H1 operating loss, albeit a small loss ($0.8m) in the context of the company’s overall size. I find it frustrating that the company refuses to acknowledge the loss in its headlines, only mentioning that adjusted EBITDA was $2.9m (last year: $2.8m). Management appear overly keen to portray Sopheon in a positive light, despite reported revenues falling (to $15.7m). The type of contract signed with customers has changed, and the company says this is to blame for the lower amount of revenue recognised. Many other factors combine to bring about these poor results: unfavourable currency fluctuations, salary inflation, a small impairment provision against development costs, and large share-based payments ($3.7m, which are excluded from adjusted EBITDA).

Sopheon does have a large net cash position ($23.5m), which is just as well since it has capitalised $3m of development costs in this six-month period, i.e. these are costs that are not included in the latest operating loss. I still suspect Sopheon has a decent underlying business, but it is requiring enormous patience. Annualised recurring revenue has reached $21.9m, so the market cap (ex-cash) works out at around 2.5x recurring revenues. At least this valuation isn’t too frothy; this could make a nice recovery if the company can get back in the black.

Lookers (LON:LOOK) (£306m) (+4%) - Excellent results from this group of car dealerships. Trading so far in H2 has continued in line with expectations and with margins remaining at their unusually high levels. These shares are cheap compared to current profitability and so the big question is how long the stressed car market conditions can continue. I’m struggling to find reasons not to like the shares at this level, on the basis that constrained supply, inflation and high margins could prevail for another couple of years. When a stock is trading at 6x earnings, it doesn’t need many years of continued success in order to justify its market cap!

Time Out (LON:TMO) (£138m) (-5%) - Short term funding secured to bridge the gap before the lenders call in the big loan in November this year. It’s not looking good for Time Out which is now having to lean on its largest shareholder to cough up the capital at a hefty interest rate. More detail below.

Main Sections

Lookers (LON:LOOK)

Share price: 78.13p (+4%)

Market cap: £306m

This collection of 143 car dealerships, representing 31 manufacturers, has produced its interim results. Here are the headlines:

- H1 revenue +3.6% to £2,230m (strength from used vehicles and aftersales, not new cars)

- H1 PBT minus 1% to £49.9m

- H1 underlying PBT minus 5.6% to £47.2m

The company excuses the fall in underlying PBT on an “exceptionally strong comparative”, as £12.7m of government supports was received in H1 of last year. It makes me wonder why these supports weren’t excluded from underlying PBT last year!

More positively, the underlying PBT result is better than the £45m guidance the company provided at the trading update in June.

Balance sheet

The company announces net funds of £78.5m, and cash and property of 95p per share. The excellent balance sheet strength and net asset values at these dealerships are well-known: again, see Paul’s coverage of the trading update in June.

Lookers today reports net assets of £410m, or £224m excluding intangibles. That’s about 57p per share. I haven’t made any adjustments to these figures for the value of leases; if you check footnote 1 today, you will find a long list of errors made to the company’s previous calculations of its lease liabilities and right-of-use assets.

Short note on IFRS 16

While I remain broadly positive on the adoption of IFRS 16, which brought leases onto the balance sheet instead of leaving them off-balance sheet, I must admit that the complexity involved is staggering. Since their introduction in 2019, the new rules have bewildered even some large-ish companies, such as Lookers.

Maybe we just needed a better system of disclosures? Perhaps IFRS 16 could have been voluntary, or could be made voluntary, with companies having the choice to instead provide a detailed schedule of that future lease payments they’ve agreed to?

I do think that the previous system left something to be desired, as huge liabilities were left off-balance sheet and there was little granularity in the disclosures.

Leases were a form of hidden leverage that often led to companies running into financial difficulties or even going bust, despite their balance sheets looking healthy - that was far from ideal, in my view!

But the current system might not be sustainable, as I reckon that few investors or business managers understand IFRS 16, and that most of them would prefer everyday language. If only 1% of users understand and get value from an accounting standard, is there any point to it? There are no easy solutions, I’m afraid.

Lookers’ performance

I’ve mentioned previously how impressed I’ve been by the car dealerships. Their supply of new vehicles has been disrupted, but they’ve managed to raise prices of both new and used vehicles to such an extent that their profitability has been protected. In some cases, their profitability has soared!

If you take into account the loss of government supports in H1 2022, then the “real” underlying performance by Looker is a terrific improvement on last year:

- H1 2022 underlying PBT: £47m

- H1 2021 underlying PBT minus government supports: £37.3m

As the company points out, it has done this despite the inflationary environment which has pushed up its own costs. But the price of vehicles and service has risen even faster!

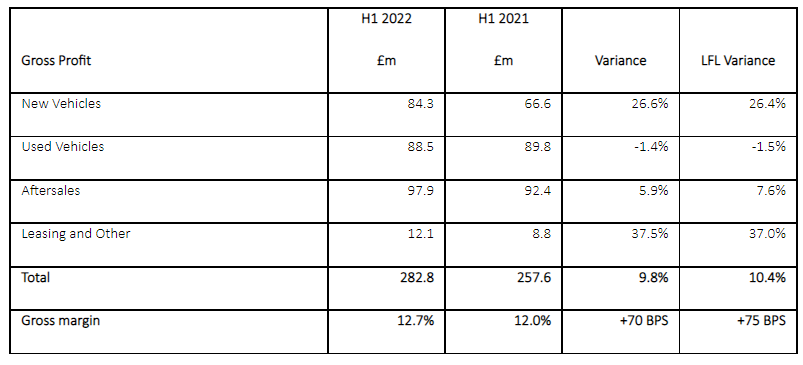

This table illustrates the strong growth in gross profit on new vehicles. When you read this, bear in mind that total unit sales from new vehicles are down by 19%. Unit sales down, but total gross profits up - extraordinary!

Some other interesting aspects of the performance:

- 16,000 warranties on used cars were sold, versus just 5,000 in last year. I wonder what’s driving this - if consumer budgets are stressed, does it increase the demand for this type of insurance?

- “Significant increase in used finance penetration to 48%” - again, this looks like a sign of stressed budgets.

- Enormous cash flow benefits from working capital management. The company generated £80m in net cash flow from operating activities, after stretching out its payables by over £50m. Some of this will unwind in H2.

- Many initiatives are underway including a new centralised procurement team, a new dealer management system, developing relationships with new brands and EV-only manufacturers, “click and collect” locations for used vehicles, and cosmetic repairs.

My view

It can be hard to distinguish between car dealership groups. Where Lookers stands out is perhaps its size - it’s bigger than most of the others we cover in this report. However, it doesn’t match the likes of Inchcape (LON:INCH) (which I would recommend looking at as an alternative).

Indeed, using Stocko’s comparison tool, I’m intrigued to see that Lookers is cheaper than Inchcape on every metric:

Despite its apparent cheapness, Lookers says that it has outperformed the UK new car market by 1.7%, and it’s hard to find much wrong with today’s results.

Outlook - trading so far in H2 (July and August) has been in line with expectations and margins are said to remain at the levels of H1.

So what’s not to like? I suppose that if you take a cautious view on the sector, you would have to suppose that margins will revert back to “normal” at some point.

When that happens, if you view car dealerships as companies lacking in competitive advantages, then you might not want to pay more than net asset value for them. And again, if you are deeply sceptical, then you might not want to pay more than net tangible asset value for them (which I calculated today for Lookers as 56p per share).

But on the other hand, if things don’t return to normal soon, then Lookers is going to earn these extraordinary profits for some time - and it wouldn’t take long for the company to prove that it’s undervalued, given where the PE Ratio is:

It’s possible that I’ve missed something, but I’m scratching my head to understand why this isn’t rated a little higher. Are investors really so sure that the conditions in the car market are about to normalise?

Time Out (LON:TMO)

Share Price: 39p

Market Cap: £138m

Media group Time Out has agreed an unsecured loan facility with Oakley Capital, here are the headlines:

- Time Out can borrow up to £8m at an interest rate of 10%

- The money will be used to help complete the development of the Time Out Market in Porto before long term financing arrangements can be agreed

- Company cash balances are currently at £4.8m, but these are partly ring-fenced by existing financial agreements

- Oakley Capital Investments - the provider of the loan - is the largest investor in the company, with a stake of about 20%

There was a time when Time Out looked like it was on its way to becoming a great company again. The magazine business had moved online and management had realised that the advertising revenue of old would eventually dry up. The business turned to marketplaces - large open-air food halls for restaurants, pop-ups and stalls. “The best of the city all under one roof”, according to a review by the Time Out magazine (perhaps not the most reliable of sources).

Time Out Lisbon opened to much acclaim in 2014 and the company set out an ambitious roadmap for further food halls around the world. In 2019, five more sites were opened in North America and the company reported a 58% jump in revenue that year. The share price peaked in January 2020 at 121p.

First hint of financing worries

But the ambitious expansion project had come at a severe cost to the balance sheet. In December 2019 the company was sitting on £44m of net debt, including £5m due to be repaid within one year and £38m due to be repaid within two.

With countries going into lockdown just a few months after the end of the 2019 financial year, Time Out was forced straight to its loan providers for an immediate boost. The company’s share price crashed with the market in March 2020 and has not yet recovered.

Balance sheet woes continue

In March 2022, the company reported £34.6m of net debt including £22.7m in lease liabilities, reported under IFRS 16 accounting rules. Of the £20m in bank borrowings, £19.2m was owed to Incus Capital Finance and due for repayment in November this year - there have been no covenants on that loan since September 2021. At the time, the company said it was confident it could renegotiate in plenty of time before the loan was due to be settled.

Perhaps this was another moment of overconfidence. Time Out has now had to lean on its largest shareholder for a short term loan to bridge the gap while the Incus loan is being renegotiated. The short term borrowing from Oakley comes with a 10% interest rate - hardly helpful as the company struggles to get back to profitability.

Income statement

Revenue bounced back in the first half of the 2022 financial year (comprising the six months to December 2021) and are likely to continue to do so as the company’s marketplaces shake off the burdens of low global travel. Losses are also narrowing at the operating level, but the company spent £2.5m in finance costs in the first half, which looks likely to spike in the second half now that the company is paying 10% interest on a loan.

My view

There is a lot to like about Time Out’s strategy and ambition in steering away from traditional media. Its expertise and contacts in cities where tourist footfall is high suggests that it is well placed to set up thriving markets.

But the financial discipline needed to set up a thriving business which relies so heavily on expensive property is very different from that needed to run a media company. Setting up five markets in one year was a mistake and Time Out and its investors are still paying the price.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.