Good morning from Paul & Graham!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Paul's 2023 share ideas, with live prices.

New SCVR summary spreadsheet from July 2023 to date, updated at weekends (very useful quick reference tool, search for ticker using CTRL+F). Hover over cell for pop-up notes.

Frozen SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Morning Movers -

Animalcare (LON:ANCR) - up 16% to 223p (£134m) - Disposal of Identicare - for £24.9m cash, selling a “non-core asset”. ANCR net cash after this deal with be £27m (c.20% of mkt cap), says this will allow it to “accelerate our organic and inorganic growth initiatives” . Looks a good deal, as Identicare was only trading slightly above breakeven. TU 25/1/2024 was in line. Paul’s view - this looks an interesting company, skimming its H1 results. Nicely profitable. Has some smart instis (eg Harwood) on the register, and a NED Marc Coucke owns 25% (pharma expert). Worth a closer look I think.

EnSilica (LON:ENSI) - up 11% to 68p (£56m) - “Significant $20m supply win” - sounds impressive, as $20m over 2 years (2025 & 2026) is material vs historical numbers. Says it hopes to secure more orders from USA. Not clear if this deal is already in the forecasts or not?

ENSI we reviewed H1 numbers here on Monday - exciting pipeline/commentary, but weak balance sheet & needs more cash. Shares shot up 20%, and it did a cheeky £1.1m placing yesterday at 50p. I think it needs more, but with great momentum in the newsflow and a rising share price, it should be able to get another placing away. Tricky to value at this stage, as no track record of proper profits. Sexy sector, so share price could go anywhere!

Sondrel (Holdings) (LON:SND) - down 10% to 9.25p - still no news on its urgent refinancing. Remember it told us yesterday that it has to raise fresh funds TODAY to meet its payroll. If a company cannot meet its liabilities as they fall due, then that is the legal definition of insolvency, so there’s a possibility the Directors could find themselves obliged to place the company into administration imminently. Let’s hope a last minute deal can be sorted. Although a pre-pack administration could also be a possibility, in order to ditch onerous liabilities - especially expensive commitments to software licensing. Super high-risk until we know more, but good luck to everyone involved - I hope to be able to update this section later with some good news, but am very glad I don't have any of my money hanging by this thread.

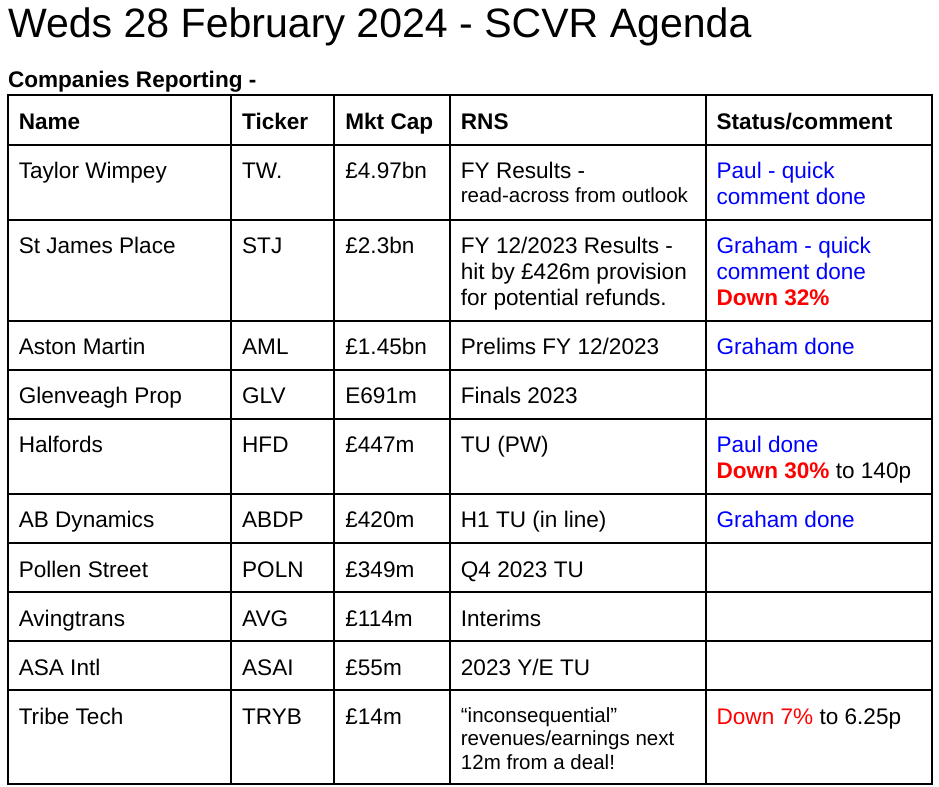

Taylor Wimpey (LON:TW.) - down 3% to 136.6p (£4.8bn) - FY 12/2023 Results - in line with expectations. Revenue down 21% to £3.5bn, and PBT almost halved to £474m. Adj EPS halved to 9.9p, so PER is about 14x. Stunning balance sheet with £4.5bn NTAV (only a bit below the market cap), mostly inventories, but also containing £678m net cash.

Outlook - macro uncertain. “Some signs of improvement in the market”, from reduced mortgage rates. Planning system “remains challenging”. “Significant underlying demand”. “Poised for growth from 2025”. Expecting a further (modest) drop in completions for 2024. Opening order book in 2024 c.10% down vs LY. Build cost inflation now down to zero. Paul’s view - nothing new here. Sounds like we should be thinking about 2025 rather than 2024 for an earnings upgrade cycle to start? Maybe the strong sector recovery in share prices recently has been a little too early, who knows? Similarly for building supplies companies, if price rises have stopped, and demand unlikely to properly pick up until 2025, again maybe it’s too early to start hunting for bargains there too? Tricky to get the timing right, as markets are supposed to anticipate things c.6 months ahead.

Political risk also worth pondering. With the CMA looking into planning restrictions, alleged price collusion, and shoddy build quality, might a new Govt attack the bumper profits & shareholder returns in this sector?

Direct Line Insurance (LON:DLG) - up 18% to 193p (£2.53bn) - Bloomberg reports that DLG has rejected a takeover approach from Belgian insurer Ageas. I don’t have any more details at present, will add more when it becomes available.

UPDATE: Ageas has issued a statement - possible offer for DLG, mixture of cash (100p/share) and newly issued Ageas shares. Implied value is 233p per DLG share, a 43% premium - but of course that price is variable, depending on the share price movements from now of Ageas shares, and £:Euro exchange rate (which is usually quite stable). Ageas shares are slightly down (2%) so far today. Presumably Ageas has gone over the heads of DLG management, with this market announcement, to appeal directly to DLG investors, given that it sounds like it's been rebuffed by DLG's Directors. Yet another UK mid-cap is now "in play".

St James's Place (LON:STJ) - down 26% to 458.6p (£2.5bn) - Final Results - Graham

It’s still not a small-cap but today’s results from St. James’s Place have resulted in a calamitous share price fall. The company leads the announcement with “robust underlying financial performance” and a “pre-tax underlying cash result of £483m”, which doesn’t really help investors to understand the company’s position. In fairness to the company, its focus on this so-called “cash result” metric isn’t anything new.

STJ has now conceded that “evidence of ongoing client servicing was less complete in the years preceding investment into our Salesforce CRM system in 2021”. I suggest that you google “how to get a st james’s place refund”, and you will find law firms seeking to help customers with claims, e.g. if they did not receive annual reviews. They have made a £426m provision without appearing to admit that clients failed to receive the services they were paying for, instead only admitting that there is a deficiency when it comes to the evidence of service provision.

The final dividend has been slashed to 8p (last year: 37p) and the company is now anticipating lower profit growth in the years ahead as it changes its charging structure. It has received a media battering for excessive charges over the past year. STJ shares may offer value at this level but I am neutral as it’s not clear to me how much brand damage the company has suffered and where profitability might sit once the dust has settled.

Summaries of Main Sections

Halfords (LON:HFD) - down 22% to 156p (08:25) - £342m - Trading Update (PW) - Paul - BLACK (profit warning) - AMBER/GREEN on fundamentals

Profit warning, with PBT guidance reduced from £48-53m to £35-40m. Weak consumer confidence, and exceptionally wet weather are blamed for reduced footfall. Also the cycling market is having a tough time, which we already knew. I'm seeing the glass half-full here, as I think the market cap could now be attractive to a bidder, and we might see a consumer recovery in 2024. But a more negative view can also be argued justifiably, so take your pick from bull or bear!

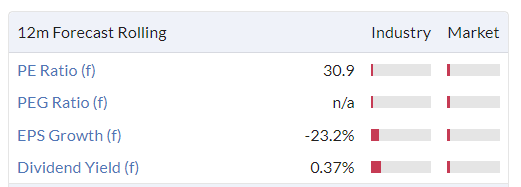

Ab Dynamics (LON:ABDP) - down 3% to £18.47 (£424m) - Trading Update [in line] - Graham - AMBER

These shares are soft this morning despite an in-line update, which to my eyes highlights the demanding expectations baked into ABDP’s valuation. Trading at 30x earnings despite only 5% revenue growth in H1 and ordinary historical ROCE returns, I must stay neutral.

Aston Martin Lagonda Global Holdings (LON:AML) - down 2% to 173p (£1.4 billion) - Preliminary Results - Graham - RED

Losses have reduced and guidance for the current year includes positive free cash flow in H2, with profit margins continuing to improve. Historic financials are very poor and debt levels remain high; perhaps this one is about to turn the corner but I wouldn’t bet on it.

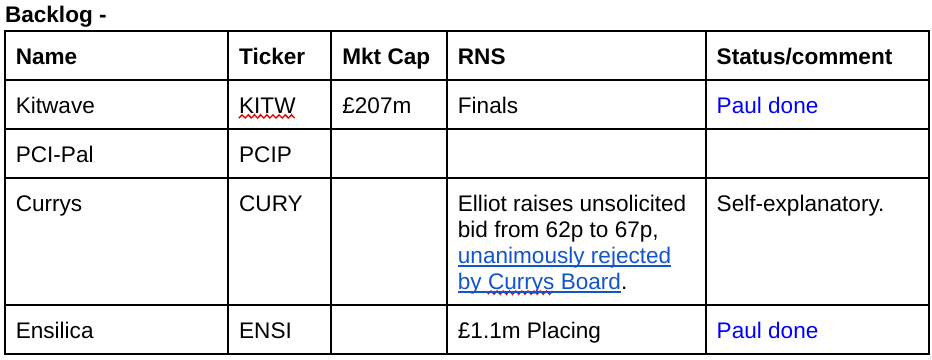

Kitwave (LON:KITW) - down 3% to 297p y’day (£207m) - Final Results [in line] - Paul - GREEN

I run through the FY 10/2023 results, and it all looks fine to me. Reasonable valuation, I think this remains a decent GARP share.

Halfords (LON:HFD)

Down 22% to 156p (08:25) - £342m - Trading Update (PW) - Paul - BLACK (profit warning) - AMBER/GREEN on fundamentals

Halfords Group plc (“Halfords” or the “Group”), the UK’s leading provider of Motoring and Cycling services and products, today issues the following trading update.

Halfords current financial year is FY 3/2024.

Commendably clear reduced guidance is provided today -

At our Q3 trading update on 25 January 2024 we indicated that we expected Underlying Profit Before Tax1 (“PBT”) for the 52-week period ending 29 March 2024 to be between £48m and £53m, assuming markets did not weaken further in Q4. Since that update, we have seen a further material weakening in three of our four core markets (i.e. Cycling, Retail Motoring and Consumer Tyres), resulting in a significant drop in like-for-like (“LFL”) revenue growth in our Retail business.

As a result, we now expect PBT to fall in the range of £35-40m.

Clearly that’s a setback, and shares have taken a tumble today.

Reasons given -

Unusually mild & very wet weather.

Weak consumer confidence (not hugely convincing, given that plenty of other consumer businesses are seeing sales rise - eg holidays, pub chains)

Challenging & competitive cycling market, hence lower margins.

Outlook - FY 3/2024 -

Our FY24 PBT forecast assumes the same challenging market conditions continue for the rest of Q4, including through our peak Easter cycling period in March. We have continued to take decisive action on cost, but in the short period between now and the end of the financial year this will not be sufficient to offset the significant market deterioration we have seen.

Outlook - FY 3/2025 - strange wording here, is it saying PBT £35-40m (flat) for this year too? It sounds to me as if they could be preparing us for another profit warning, if market conditions don’t improve -

Looking ahead to FY25, we remain cautious on market recovery in the short-term, and the current significant volatility in market conditions means that forecasting accurately is challenging. Notwithstanding this, we anticipate that underlying PBT in FY25 will be broadly in line with that forecast in FY24 assuming that: 1) There is marginal year-on-year growth in our core markets, with trading conditions seen in Q4 proving anomalous; and 2) The Cycling market normalises and margin pressure dissipates through the year. FY25 PBT will be supported by cost savings that more than offset net inflationary headwinds.

Paul’s opinion - I was hopeful of Halfords attracting a takeover bid, especially after the recent interest shown in CURY (despite it also being only marginally profitable (as a percentage of revenue) at the moment. Bidders seem to be looking ahead to a consumer recovery, and a lower share price after today’s profit warning could allow a bidder more room to offer a premium to a bombed out share price.

That said, investing purely on hopes of a takeover bid can be risky.

Halfords has an OK balance sheet, with very little interest-bearing debt. You can see that from the notes to the accounts, where nearly all the finance costs on the P&L relate to leases, with only £1.4m interest paid on bank borrowings in FY 3/2023.

Shares are down 23% to 155p in early trades today, which makes sense given the reduced outlook for both this year and the new year starting in April.

However, I think the lower HFD shares go, the more likely a takeover bid becomes. It’s soundly financed too, and still modestly profitable, so I don’t see today’s update as a cause for alarm. I also like the strategy of diversifying into autocentres, doing MoTs & repairs, etc, which leverages its brand strength.

It’s up to you whether you focus on the negatives today, or the upside potential from a consumer recovery and a possible takeover bid.

Roland was AMBER when reviewing H1 results here on 29/11/2023, astutely flagging concern over the expected H2 weighting.

I’ve obviously got to mark it as BLACK today, for a profit warning. Although on fundamentals, personally I see good potential upside here, so I view it as AMBER/GREEN.

Shares are now back down at the low part of the 150-250p range they seem to have settled in over the last 2 years -

Kitwave (LON:KITW)

Down 3% to 297p y’day (£207m) - Final Results [in line] - Paul - GREEN

Kitwave Group plc (AIM: KITW), the delivered wholesale business, is pleased to announce its final results for the twelve months ended 31 October 2023.

Revenue £602m (LY: £503m)

Three acquisitions have been made since IPO in May 2021 (11 since 2011)

Profit is in line -

“... results in line with the significantly upgraded market expectations that were established after the Group's interim results, published in July 2023.”

As you can see - very impressive -

Dividends -

The Board has declared that it is recommending a final dividend of 7.45 pence per ordinary share, subject to approval at the Annual General Meeting ("AGM") to be held on 22 March 2024, which will, if approved, result in a total dividend for the financial year ended 31 October 2023 of 11.20 pence per ordinary share.

Yield is 297p share price divided by 11.2p = 3.8%

Balance sheet - NTAV is only about £20m, but that looks OK to me.

Note that net debt has risen from £18.5m to £33.2m, which is probably high enough for my taste, but the company says it’s only 0.8x adj EBITDA.

Outlook - doesn’t say much of any consequence, is more general, concluding -

There remain many more acquisition opportunities in the UK's fragmented wholesale market, and Kitwave is well-positioned to capitalise on these opportunities and deliver further value to the Group and its shareholders.

Broker note - many thanks to Canaccord. It’s showing adj EPS of 28.7p actual for FY 10/2023, with only small forecast rises to 29.3p and 30.6p in following years. Hopefully that’s set conservatively, and might be beaten, especially if more bolt on acquisitions are done.

If we say it’s about 30p, then at c.300p the PER is 10x - I think that looks decent value.

Paul’s opinion - I like this a lot. The only fly in the ointment was some Director selling last year, so you can make up your own mind if you think that’s significant or not.

On fundamentals, I’m happy to go GREEN, as I think this is a decent GARP share, growing through sensible acquisitions.

Graham’s Section:

Ab Dynamics (LON:ABDP)

Share price: £18.47 (-3%)

Market cap: £424m

Today’s update from AB Dynamics, the vehicle testing and simulation group, is in line with expectations.

Key points:

H1 revenue +5% to c. £51m

Improved adjusted operating margin (H1 last year: adjusted operating margin was 15.9%

“Good demand” for Testing Products, and a return to growth for Testing Services

Simulation will be H2-weighted as systems manufactured in H1 will be delivered to customers in H2.

Net cash rises year-on-year to £27m. The company signals an intent for “further value enhancing acquisitions”.

Outlook

The Group delivered strong order intake during the first half and has a solid order book, providing good visibility into the second half of the year. The Board remains confident that the Group will make further financial and strategic progress this year, with its expectations for FY 2024 performance unchanged at this stage. Future growth prospects remain supported by long-term structural and regulatory growth drivers in active safety, autonomous systems and the automation of vehicle applications.

Graham’s view

Nothing new to add here, and I don’t want to come across as a broken record. For example, see my comments in September.

In summary, I think I understand some of the attractions of this share - in particular the long-term structural growth drivers from the increased proliferation of autonomous driving and advanced driver-assistance systems. It has been profitable for many years, and has funded acquisitions without diluting its shareholders.

Unfortunately I still can’t get over the valuation here, especially considering that it’s not really growing very quickly in the short-term.

So far, I do think we’ve been right to be cautious on ABDP’s valuation. Here’s the 5-year chart:

There’s an interesting note from Zeus Capital, published at the end of October 2023, where they argued that the shares finally offered good value on a forward P/E multiple of 21x, or 19x on a cash-adjusted basis.

However, you would have needed very good timing to catch that low, maybe involving some clever price alerts. Here’s the 1-year which clearly shows that spike lower towards the end of October 2023.

Maybe the lesson is that if this stock gets to a PER of 20x or less, it could be a rare buying opportunity! At 30x or more, “I’m out”.

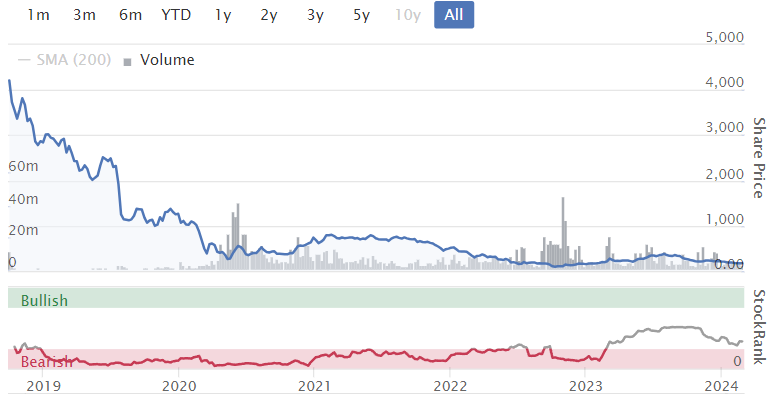

Aston Martin Lagonda Global Holdings (LON:AML)

Share price: 173p (-2%)

Market cap: £1.4 billion

I’m opening up today’s full-year results from Aston Martin with very low expectations.

Here is the share price since flotation in late 2018:

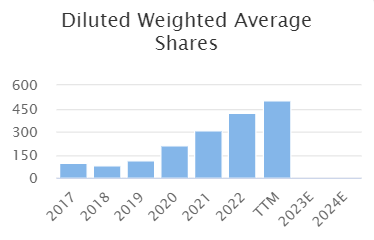

And here is the share count:

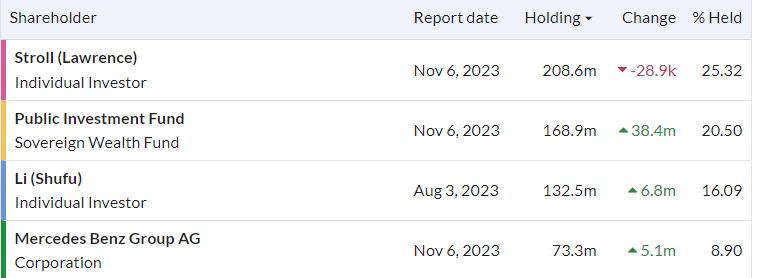

This stock has been a money pit for its major investors, who are now arranged as follows:

Public Investment Fund is the sovereign wealth fund for Saudi Arabia, while Shufu Li is a Chinese billionaire.

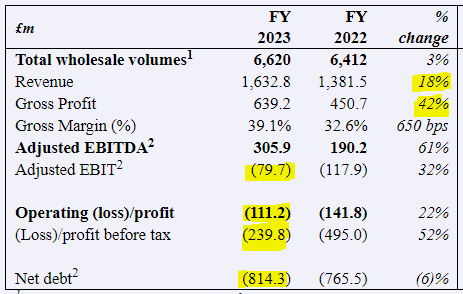

Today’s highlights show revenues and gross profits picking up, but it’s still loss-making:

Being a luxury brand, total delivery volumes are tiny.

Comment by Executive Chairman Lawrence Stroll (excerpt; bold is mine):

"In 2023, Aston Martin delivered significant strategic milestones and further financial progress, driven by continued strong demand for our ultra-luxury, high-performance products. The rich mix of sales, driven by our ongoing commitment to product innovation, supported growth in average selling prices to record levels. This, combined with our ongoing portfolio transformation, resulted in a significantly enhanced gross margin, remaining on track to achieve our longstanding target of around 40% gross margin in 2024.”

They were very close to this gross margin target (39.1% in 2023).

Continuing, he says the new line-up of front-engine sports cars, along with other advances, “will support the delivery of the Company's near- and medium-term financial targets, including positive FCF generation in H2'24”.

Let’s skip down to today’s cash flow statement and see how it looks.

Key elements are as follows:

Net cash inflow from operating activities: plus £146m.

I see that this includes a £66m decrease in “advances and customer deposits”. Perhaps not very important and something that could reverse in future years, but it can’t be a good thing to see a decline in this cheap form of financing.

Net cash used in investing activities: outflow of £383m.

The great argument against investing in any car company is the capital intensity of the sector. Interestingly, AML didn’t spend all that much on PPE (£91m). It spent far more (£306m) on “technology and development expenditure”.

Cash flows from financing activities: these were positive, thanks to over £300m raised from the issuance of new shares and warrants. The interest bill on outstanding debt was £122m.

Overall, therefore, it’s a pretty poor cash flow performance. Of course the company is betting that its enormous tech/development spending will yield strong results in the years ahead. But for investors who want to see strong performance before investing, this cash flow statement doesn’t support that.

I also don’t see the performance for 2023 as an improvement over the performance in 2022, from a cash flow perspective. In 2022, the company spent £100m less on investing activities (£285m spent in 2022, vs. £383m spent in 2023).

Balance sheet is weak, as expected: net assets of less than £1 billion, with negative tangible net worth after deducting c. £1.6 billion of intangible assets.

Let’s now consider the debt mix.

From the going concern note:

The Group meets its day-to-day working capital requirements and medium term funding requirements through a mixture of $1,143.7m First Lien notes at 10.5% which mature in November 2025, $121.7m of Second Lien split coupon notes at 15% per annum (8.89 % cash and 6.11% Payment in Kind) which mature in November 2026, a Revolving Credit Facility (£99.6m) which matures August 2025, facilities to finance inventory, a bilateral RCF facility and a wholesale vehicle financing facility.

I’ve always viewed Payment in Kind (PIK) notes with suspicion. They involve adding on interest costs to the principal, instead of actually making the interest payment. I see them as the corporate equivalent of paying your debt “on the never-never”.

As described above, AML has a large senior note maturing next year, along with a junior note at a much higher rate (15%) where the PIK strategy has been deployed.

The directors are satisfied that even in a “severe but plausible downside scenario”, they would be able to take actions to safeguard the company’s financial position.

Outlook for 2024.

Near- and medium-term guidance is maintained:

2024 is expected to deliver another year of significant strategic and financial progress as we continue the ongoing product portfolio transformation. Enhanced profitability and EBITDA will be driven by high single-digit percentage wholesale volume growth, gross margin further improving to achieve our longstanding target of c. 40% and EBITDA margin expansion continuing into the low 20s%.

This year, there will be another £350m of “capital investment in product developments”, i.e. another large investing cash outflow.

Even so, free cash flow (FCF) is expected to “materially improve”, with positive FCF in H2 of this year, thanks to the timing of wholesale volumes.

They will attempt to refinance their debts in H1 and improved financial performance should see net leverage (net debt to EBITDA) reduce towards c. 1.5x. This multiple was 2.7x in 2023, which is uncomfortably high.

Graham’s view

I was hoping that I might not give this one the thumbs down, but I don’t see how I have any other choice.

Readers should bear in mind that I tend to be very bearish on unprofitable car companies; I was bearish on Tesla for a long time and the market disagreed with me.

If AML had a positive tangible net worth, or a large cash pile, maybe I’d be willing to think in terms of valuation multiples on forecast earnings or even a multiple on forecast sales.

But with a large net debt position (even after raising huge amounts of equity) and with profitability still some time away, I’m afraid I can’t do that. Even the promise of positive FCF in H2 seems more like an accident of timing rather than sustainable success.

I would leave this share to Formula One fans and drivers of luxury vehicles who will enjoy being part of the Aston Martin story. When it comes to making money, I’m afraid to say that I have no faith in this one.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.