Good morning from Roland and Graham! And we also have a section from Paul. Today's report is now finished.

Charlie Munger RIP - It's the end of an era as the death of Charlie Munger has been announced overnight. Here is sample coverage from CNBC. He was 99.

The official announcement can be read on Berkshire Hathaway's website.

Warren Buffett, CEO of Berkshire Hathaway, wishes to say: “Berkshire Hathaway could not have been built to its present status without Charlie’s inspiration, wisdom and participation.”

Courtesy of Ramp Capital, here are some of the greatest quotes from Munger.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Agenda

Summaries

Supreme (LON:SUP) - up 13% to 125p (£146m) - Interim Results (ahead) - Graham - GREEN

Forecasts got a significant boost yesterday with continued strong momentum in all divisions of this consumer products supplier. ElfBar is doing extremely well and alone is responsible for most of today’s profit upgrade. At a PER of 7x I think this offers very interesting value.

Halfords (LON:HFD) - down 19% to 185p (£405m) - interim results (warning) - Roland - AMBER

A cut to profit guidance from this motoring and cycling specialist. Market share gains in H1 suggest the company’s offering is working well, but I am concerned by the extent of the H2 weighting implied by today’s guidance. On balance, I’m neutral.

Distribution Finance Capital Holdings (LON:DFCH) - down 30% to 18p (£32m) - trading update (warning) - Roland - AMBER/RED

This specialist lender says that it expects to report a loss relating to a large overdue loan where recovery prospects have worsened. Full-year profit guidance has been cut by around 65% but performance elsewhere is said to be strong. I think this should probably only be of interest to special situation investors at this point.

Focusrite (LON:TUNE) - down 4% y’day 458p (£270m) - Final Results 8/2023 (in line) - Paul - GREEN

Looks attractive value to me, for a nice quality business. I don’t know what the future holds though, but at this valuation of PER 12.1x, I’m happy to remain GREEN.

Impax Asset Management (LON:IPX) - up 2% to 437p (£579m) - Final Results - Graham - GREEN

This fund manager has suffered some small net outflows and a large reduction in profits due to an increased cost base. Despite these issues, I remain positive on the stock due to the heavily discounted valuation for what I believe remains a high-quality business

Xaar (LON:XAR) - down 25% to 132p (£104m) - Trading Update (profit warning) - Graham - RED

This manufacturer of industrial printheads heaps another profit warning onto the market. Revenue forecasts are adjusted sharply lower and adjusted PBT for 2024 is now expected to be only around breakeven. I switch to a negative stance on the stock due to the long history of disappointment for shareholders and a shrinking cash position.

Roland's Section

Halfords (LON:HFD)

- Share price: 185p (-19% at 08.20)

- Market cap: £405m

The cycle and automotive retailer has issued interim results today, covering the 26 weeks to 29 September 2023. Half-year performance appears to have been fairly solid:

"Market share gains in all categories, ahead or in line with expectations”

However, the shares have been hit hard by a cut to profit guidance for the year and are down by around 20% as I write.

FY guidance cut: trading patterns this year are said to have been volatile and the company says it has recently seen “some market softening in our discretionary big-ticket categories”. As a result, Halfords has cut its profit guidance range for the full year:

… we believe FY24 underlying PBT will now fall within a narrower range of £48m to £53m

To put this in context, on 6 September, the company issued guidance for full-year underlying pre-tax profit of between £48m and £58m. Prior to that, management said they were comfortable with a consensus figure of £53.3m.

So it looks like the bottom end of the expected profit range is unchanged, but the top of the guidance range has been cut by 9%. This looks like a profit warning to me.

Taking the mid-point of the updated range suggests uPBT for the full-year could be £50.5m, which would be about 6% below previous consensus of £53.5m.

Applying a similar cut to earnings suggests a figure of about 16.7p per share.

After this morning’s fall, that would price Halfords on 11 times FY24 forecast earnings. That could be cheap, if the company can deliver on its “mid-term target” to rebuild underlying pre-tax profit to £90m-£110m.

Let’s take a closer look at today’s results to see if they justify a confident stance.

H1 results highlights: today’s half-year results seem reasonably good to me, in the circumstances:

H1 revenue rose by 13.9% to £873.5m

Like-for-like sales growth of 8.3%

Underlying pre-tax profit up 15.8% to £21.3m

Reported pre-tax profit up 3.3% to £19.3m

Underlying earnings up 13.4% to 7.6p per share

Interim dividend unchanged at 3p per share

Both the retail and Autocentres divisions reported revenue growth. Stronger growth and margins in the Autocentres business highlighted the appeal and apparent growth potential of this business, versus the more challenged retail operation:

Retail revenue +3.2% to £516.6m

Retail gross margin: 45.8% (-3.3%)

Autocentres revenue +33.9% to £356.9m

Autocentres gross margin: 50.6% (-0.6%)

Gross margins fell across the business, but the company says that “the majority” of this was due to currency effects in retail, where Halfords has USD exposure.

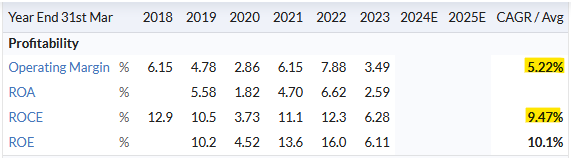

My sums suggest a trailing 12-month operating margin of 2.9%, with a TTM return on capital employed of 5.7%. Both figures are below historic averages for the group:

Cash flow / balance sheet: the balance sheet shows financial net debt of £47m, which looks reasonable enough to me.

However, cash flow deteriorated during H1, with free cash outflow of £21.4m as I calculate it, versus -£4.8m in H1 last year.

One reason for this was that inventories rose by £6.7m to £262.9m, in H1, reflecting cost inflation and investment in Autocentres growth.

More reassuringly, retail inventories fell from £204.8m to £188.8m during the half year, and are expected to fall a little further during the remainder of the year. This should help to free up some cash.

Trading commentary: the company says that discretionary markets such as cycling are “challenging and below expectations” due to the consumer environment.

Wider market volumes in cycling are said to have fallen by 5.8% in H1 versus the same period last year. However, Halfords says its share of this market rose by 1.8%, suggesting the company’s offering remains competitive.

I assume that the big-ticket discretionary items referred to in the updated guidance above are high-end bicycles and e-bikes.

Elsewhere, “needs-based categories” such as motoring accessories and services have seen strong growth and performed in line with expectations.

B2B sales rose by 37% during the period and now represent nearly a third of group revenue. This growth is coming from the Autocentres business – mostly tyre fitting, I think – the company has made acquisitions in this area and now has a mobile fitting fleet in addition to its bricks and mortar locations. Tyre sales were up 29% in H1.

Outlook: management expects an unusual second-half weighting to profits this year, as last year’s inflationary pressures ease:

We continue to expect FY24 profit delivery to be second half weighted as inflationary headwinds annualise, coupled with the delivery of the balance of FY24 targeted cost and efficiency savings of £30m.

Roland’s view

I’m encouraged by the growth of the Autocentres business, especially in B2B markets.

On balance, I think Halfords is performing well where it can and is being fairly well managed, with a sensible strategy. The balance sheet also looks acceptable to me.

The current valuation doesn’t seem too demanding on a medium-term view, unless you believe that the weakness in cycling will persist – i.e. that we’ve past peak cycling for now.

However, I am concerned by the worsening profitability and cash generation, and by the extent of the H2 weighting that’s implied by today’s results.

I accept that last year’s inflation may have had an unusual impact on profits. But as far as I can see, Halfords results have always been H1-weighted, especially prior to the pandemic.

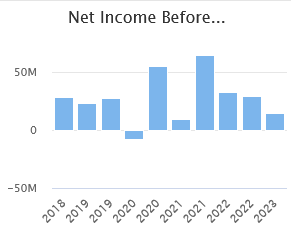

We can see this pattern in Stockopedia’s interim accounts view for the last five years:

It’s possible that the strong performance of the Autocentres business will reduce the historic seasonality of Halfords’ results. It’s also true that a £30m cost saving programme is underway that’s expected to deliver a further £14.4m of benefits in H2, so this could provide a boost.

However, my feeling is that there’s still some risk that H2 profits will fall below expectations, resulting in a further profit warning.

For now, I’m going to adopt a neutral view.

Distribution Finance Capital Holdings (LON:DFCH)

- Share price: 18p (-30% at 10.00)

- Market cap: £32m

Graham last covered this specialist bank/lender in April. Unfortunately today’s update is a profit warning. It seems that a large loss is now expected on one of the group’s biggest outstanding loans.

As a result, DFCH’s 2023 profits are now expected to be much lower than previously guided:

The group now expects to deliver a pre-tax profit of no less than £2.0m for the year ending 31 December 2023

Distribution Finance’s pre-tax profit was £3.2m in H1. Forecasts I can see suggest full-year pre-tax profit was previously expected to be c.£6m. So this is a big warning.

The only potential bright spot is that the company says that due to “the unique circumstances” of this problem loan, no further impact is expected in 2024. I’m not sure why this should be, unless the loan is going to be fully impaired this year.

What’s gone wrong? The problem borrower is caravan park operator RoyaleLife, which went into administration in October. RoyaleLife represented 2% of DFCH’s loan book at the end of September.

Refinancing was already underway and this risk was flagged up in the interim results, when the balance outstanding was £10.4m.

However, the outlook for debt recovery appears to have worsened significantly since then:

The group is aware of a significant number of assets which have been sold out of trust or are missing from confirmed locations and following continued work with various stakeholders, it is now clear that RoyaleLife’s financial situation and operation is much opaquer and more complex than originally determined, adversely impacting, to a greater degree than expected, a larger number of secured lenders and other creditors

The company says it intends to make “an appropriate credit loss provision” in this year’s accounts. Management doesn’t provide any indication of how big this provision might be, but assuming trading elsewhere in the group has been in line with expectations, I would guess that an impairment of at least £4m, perhaps more, is likely.

Based on the £10.4m loan balance reported in the H1 result, that still leaves c.£6m to collect (unless there has been any recovery since June, which seems unlikely to me).

Trading update/capital strategy: broader trading across the group is said to have been strong so far in H2, with good momentum and continued loan book growth.

Today’s RNS also includes a strategy update. This is a little vague, in my view, but suggests to me that the company is scaling back its growth ambitions and will now focus on organic growth, rather than seeking additional capital.

the Company has determined that, in the medium term, it will remain flexible and pragmatic in the pursuit of its growth strategy, balancing this against its ability to generate retained earnings as a route to organic capital accretion.

DFCH’s management says that the group’s current capital position and existing financing facilities will support a loan book of up to £800m. The loan book was reported as £537m at the end of September, suggesting there’s still a reasonable amount of headroom.

Roland’s view

This specialist lender had previously seemed to be making good progress. It achieved profitability last year and had been awarded a banking licence, providing access to lower-cost deposit funding.

The last balance sheet showed a book value of c.£100m, so I would guess that a significant impairment on a £10.4m loan may be manageable, assuming bad debts remain low elsewhere.

At the end of H1, arrears were said to be running at 0.5% of the loan book, excluding RoyaleLife, or 2.5% including this problem customer.

With the market cap now down to £32m, DFCH shares are trading at a discount of about 65% to their last reported book value.

This might be an interesting special situation, but I would want to see an updated set of accounts before taking a view on this. I’d also want to spend some time learning more about DFCH’s loan book and customer profile before considering an investment, after today’s news.

I’m going to go AMBER/RED on DFCH. Although I think there might be an opportunity here, the risks seem quite high to me at this point.

Graham's Section

Supreme (LON:SUP)

- Share price: 124p (+13%)

- Market cap: £146m

These interim results have a great headline:

Record levels of revenue, Adjusted EBITDA and pre-tax profit driven by growth across all product categories, alongside extensive operational progress

Financial highlights:

Revenues +63% to £105m, largely driven by the distribution of “Elfbar” vapes.

Organic revenue growth was £8.7m (around 13%).

Adjusted EBITDA +88% to £15.2m (“very modest investment in overheads to support the reported revenue growth”)

Pre-tax profit +179% to £12.3m

Interim dividend is 1.5p (H1 last year: 0.8p).

Outlook - H2 “has begun very well”:

This strong performance in the core business and the growing breadth of ElfBar distribution, combined with a tightly controlled overhead base have led the Board to, again, significantly increase its expectation of full year profitability for the year ending 31 March 2024 ("FY 2024")

Revenue guidance moves from £195m-£205m to £210m-£220m.

Adj. EBITDA guidance moves from £28-£30m to £32m-£35m.

The extra anticipated EBITDA from the core business is around £1.5m, while ElfBar is expected to contribute an additional £3m.

Regulation:

The consultation on possible new UK e-cigarette regulations ends on 6 December 2023. The Group remains confident that the Government will continue to recognise the important role that the vaping industry plays in delivering the country's 'Achieving Smoke-free 2030' initiative

CEO comment excerpt:

"I am delighted to report another exceptional period of trading for the Group, delivering record revenue and profit growth. This strong performance has been undoubtedly driven by our established vaping activities, alongside solid sales momentum across the remainder of the business including sales growth in Lighting of 21% and Sports Nutrition & Wellness of 17%”

The company has moved into a new warehouse facility without any complications. New offices will open there in early 2024, ready to support organic growth and/or acquisitions. The company reports £35m of unused borrowing facilities, and continues to analyse M&A opportunities.

On the vaping front, Supreme’s own brand 88vape has taken various measures to address concerns around underage drinking. With a government review of vaping underway, it seems to me that they are trying to get ahead of any legislation, and demonstrate that very strict legislation will not be necessary.

H1 cash flow is poor due to a £16m investment in working capital to support Elbar. Let’s wait until we see full-year results before worrying about this. Excluding the Elfbar investment, operating cash flow was nearly £17m.

Net debt is less than £5m, and there are also £15m of leases. This seems reasonable and I agree that they can afford to do some modest M&A if they wish.

Graham’s view

I can see that Paul has been keeping a neutral stance on this one. Personally, I have to say that I’m a bit more positive on it; at a PER of 7x and with great momentum it looks cheap to me:

Some bear points might be:

Regulatory risks around vaping (and ethical concerns)

The company doesn’t actually own Elfbar, which has been the source of most of the good news lately.

We have seen other companies in the lighting and sports nutrition sectors struggle to generate consistent profitability. Demand in the lighting industry can also be highly volatile.

For me, the risks are priced in here given that Supreme has built up a really solid track record in recent years. In addition to being a distributor, it does own a vape brand, and the distribution deal should stay in place for the foreseeable future.

Readers should bear in mind that I accept lots of regulatory risk in my personal portfolio (tobacco, gambling, etc.) and perhaps I take too much of that sort of risk. But I have to say that I think Supreme looks really interesting at this valuation. Of course much will depend on the company’s ability to execute good acquisitions in the future. But so far they seem to be doing well.

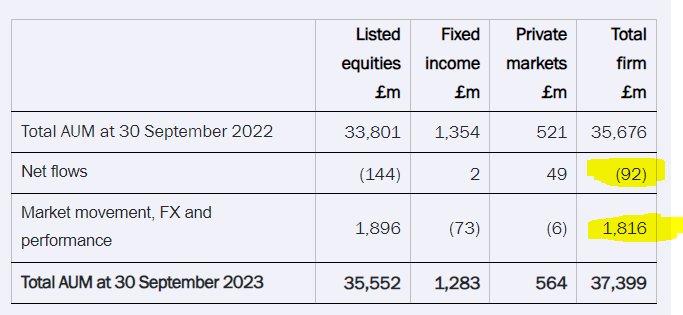

Impax Asset Management (LON:IPX)

- Share price: 437p (+2%)

- Market cap: £579m

This fund manager has published full-year results for the year ended September.

It reports “high client retention despite challenging markets”, “strengthened distribution capabilities” (including a new Tokyo office) and an “increased product pipeline”. It has also expanded its fixed income offering.

Turning to the numbers:

AuM up 5% year-on-year to £37.4 billion

Revenue up 2% to £178m

PBT down 28% to £52m

The fall in profitability is attributed to rising costs:

…operating costs also rose as we invested in our distribution and investment capabilities, technology and operations to ensure that the business is resilient and scalable

The total dividend for the year, including the interim dividend, is 27.6p, which is unchanged on last year.

Earnings per share are 35.2p, so the payout should still be affordable.

Founder and Chief Executive Ian Simm describes it as a “creditable” set of results:

"In a year where we have celebrated Impax's 25th anniversary, our conviction in our investment thesis focused on the transition to a more sustainable economy is stronger than ever. With valuations increasingly attractive, our investment teams have identified several compelling themes that we believe will play out over the medium to long term, for example the adoption of renewable energy, the provision of climate resilient water supply and infrastructure and the deployment of new technology to improve access to healthy food and financial services worldwide."

Market comments - I always like to read comments on the markets from fund managers, and Ian Simm doesn’t let us down. He points to Nvidia as being “one of a narrow range of technology stocks that has contributed significantly to the rise in global equities indices”.

However, despite the strength of a small number of tech stocks:

In other areas of the economy sentiment has been more fragile, contributing to a cyclical derating of Impax's major investment portfolios. Smaller and mid-cap companies in particular have faced challenges in the form of the higher costs of borrowing and supply chain issues.

Additionally, post-pandemic inventory destocking has temporarily disrupted the demand for goods across several sectors that our investment strategies have long-term exposure to, including nutritional ingredients, life sciences tools and solar energy.

This uncertain backdrop and the impact of higher rates has led many investors to delay investment decisions, preferring to benefit from the positive returns currently available in cash.

Much of this will sound familiar to us!

Performance against benchmark has been poor, with the majority of Impax’s strategies underperforming their benchmark over the past year.

However, the same could be said of most active managers, in particular during a year when anyone who was underweight the “Magnificent 7” stocks will have underperformed (the magnificent seven are Apple, Amazon, Alphabet, Nvidia, Meta, Microsoft and Tesla).

Net flows have been marginally negative (a very strange thing to say about Impax), but market movements kept total AuM rising.

Outlook

It’s a long outlook statement, discussing the history of environment investing and current economic challenges, and it finishes with:

Notwithstanding the headwinds that we have experienced during 2023, I am highly encouraged that our client retention has been excellent. Meanwhile, we continue to develop new investment capabilities while enhancing our operating model to ensure that the business is efficient and scalable, and, as a result, we believe we're well positioned to continue to deliver value for all stakeholders.

Graham’s view

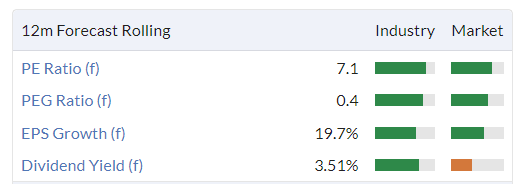

I’ve been positive on this one lately, thinking that it has stumbled into value territory. It has been a mighty fall since the high in late 2021:

That puts it on a PER of around 13x and an attractive yield:

For a business that has earned excellent quality metrics, with lots of growth runway and scalability in theory:

And it passes five bullish stock screens:

It is fashionable now to say that ESG investing has had its day. So for anyone with contrarian instincts, now is an interesting time to bet on ESG’s recovery - and the Impax valuation is offering plenty of rewards when that eventually happens.

Again, I think it’s worth pointing out that AuM is up year-on-year. Costs are up too, of course, but I believe that management here is highly credible, and I expect that the money is being well spent.

CEO Ian Simm still owns 7% of the company.

So I’m still a fan of the risk/reward here.

Xaar (LON:XAR)

- Share price: 132p (-25%)

- Market cap: £104m

I’m relieved to see that I remained sceptical on this one when I last looked at it in September with a neutral stance, leaning “more towards concern than optimism”. If only I had done the same with Frontier Developments!

Xaar is another loss-making business hoping to get back to its glory days of old. The company, which makes industrial printheads, saw its cash balance fall to just £7m as of the end of H1 2023. For a struggling manufacturer, this isn’t as much headroom as I’d like.

Today’s announcement is a profit warning, but it starts out positively before delivering the bad news:

PROFIT AHEAD OF EXPECTATIONS FOR 2023

Adjusted PBT for the current year is now expected at £2.5-£3m. The estimate had been £2.5m, so this is ahead of expectations.

However, this slight beat on profits comes despite a significant reduction in the revenue forecast. Where analysts had previously expected revenues of up to £80m, the new revenue forecast for 2023 is only £70m-£72m.

This brings us to the outlook statement for 2024:

The Board anticipates that weaker demand during Q4 2023 will continue into 2024, and together with delays in some customer product launches, will result in lower revenue and adjusted profit in 2024 than previously anticipated. We are optimistic and remain focused on delivering significant opportunities in our customer pipeline.

They “remain confident in the medium-term outlook”, but I don’t see any reason for shareholders to remain confident at this stage.

Net cash has fallen to £4m, in line with management expectations. They also have an undrawn borrowing facility of £5m. However, personally I am not comfortable with this amount of headroom, given the possibility of further losses.

Estimates - many thanks to Progressive Research for updating their forecasts today. They see year-end cash for 2023 of £5.3m, rising to £6.9m by the end of 2024.

They argue that Xaar “remains profitable at the adjusted PBT level in 2024”, though their adj. PBT forecast for 2024 is now only £0.4m (down from £4.2m). Revenues are barely expected to grow next year.

CEO comment:

"Whilst the external trading environment is challenging, we remain focused on the delivery of our strategy and taking advantage of the significant opportunities we have that will drive profitable growth. Our products continue to generate strong interest from customers, demonstrating our leadership in printing highly viscous fluids with all the performance and sustainability benefits they deliver.

"Due to the current geo-political and macro conditions, bringing these products to market is taking longer than expected, however, we are optimistic about the future, and we are well placed to benefit as trading conditions improve."

Graham’s view

While sometimes I will back a loss-making company to turn itself around, I’m not going to do that in this case.

The reasons are:

Xaar has suffered from volatile demand for many years, more frequently posting losses than profits.

It has a particular exposure to China, making it especially difficult to predict how trading will go.

The cash balance has dwindled away to only a few million pounds.

As a manufacturer, we need to be extra careful with valuation compared with other sectors.

Therefore, I don’t see how a market cap of over £100m makes sense here. I think these shares need to start resembling options on an unlikely success, before they start to look interesting. And I'm now switching to a negative stance, due to the weakened cash position.

Paul's Section

Focusrite (LON:TUNE) - down 4% y’day 458p (£270m) - Final Results 8/2023 (in line) - Paul - GREEN

Focusrite plc (AIM: TUNE), the global music and audio products company, announces its Final Results for the year ended 31 August 2023.

I last looked at Focusrite on 14/9/2023, reviewing its FY 8/2023 trading update, summarising it as:

Focusrite - up 5% to 525p (£311m) - TU for FY 8/2023. Almost in line exps. Negligible net debt. Looks a good quality business, at a reasonable price. Thumbs up from Paul.

It’s now 67p cheaper, so that’s a good start - cheaper is better!

Some key numbers for FY 8/2023 -

Results are in line with expectations.

Revenue down 3% to £178.5m

Gross margin improved from 45.3% to 47.5% - helped by lower freight costs.

Adj operating profit down 12.4% to £30.4m (a healthy 17% profit margin)

Adj diluted EPS 38.4p, down 23%, and giving a PER of only 11.9x - seems cheap.

Dividends total 6.6p, up 10%, yielding only 1.4%

Negligible net debt of £1.3m - so there’s scope to self-fund more acquisitions using its £50m bank facility. Note that seasonal movements caused debt to increase post period end -

…net debt of £9.6 million at 16 November 2023, which is expected to improve following the upcoming 2023 holiday season.

Outlook - the first 2 paragraphs below sounded to me as if it might be laying the ground for a possible profit warning later in FY 8/2024 maybe? But para 3 then sounds more upbeat, about new product launches - so make of this what you will -

Current market conditions for our Content Creation division remain difficult and our revenue year to date has been impacted by a degree of sales channel de-stocking. However, underlying demand for our products, as evidenced by customer registrations, remains satisfactory.

Performance in our Audio Reproduction division remains strong.

Overall, at this early stage and as we head into our key holiday season, our expectations for the year remain unchanged.

Whilst we remain mindful of the significant global economic and political challenges, as well as ongoing cost pressure in the supply chain, we have successfully built our inventory positions back to more normalised levels and have robust plans for future component supplies as well.

With key new products launched towards the end of FY23 and more introductions planned for the year ahead, we remain confident in the organic growth potential of existing brands.

Additionally, with the benefit of our cash generation, the Group has demonstrated its ability to execute on our proactive M&A strategy, carefully considering acquisitions that not only enhance earnings but also expand our market potential, increase our R&D capabilities, and contribute both scale and dynamism to our business.

We remain optimistic about our future prospects.

Note how new product innovation is key to Focusrite, and has been mentioned often before. I think that’s how it achieves strong profit margins - by constantly innovating to stay a step ahead of cheaper competition.

There’s no guarantee that situation will last forever though.

More detailed research on products, markets, and competition would be time well-spent, for anyone thinking about buying this share.

Balance sheet - is healthy overall, even after deducting the hefty goodwill from acquisitions.

Inventories stand out as much too high, at £55m, which compares unfavourably with £94m for the whole year's cost of sales - so it’s got more than 6 months’ of product (at cost) sitting on the balance sheet. Anyone talking to management could query this - it’s seem an inefficient use of capital tied up in lots of inventories, and raises the risk of discounting being required to clear slow-moving lines maybe?

Cashflow statement - the item which stands out (apart from inventory build last year that hasn’t changed this year much) is the very large £9.2m capitalised R&D cost. That’s good in a way, as it drives the business. But just remember to ignore EBITDA, as that ignores these costs.

Note that divis are small, because it’s spending most of the cashflow on making acquisitions.

Paul’s opinion - TUNE looks attractive value to me, for a nice quality business.

I don’t know what the future holds though, but at this valuation of PER 12.1x, I’m happy to remain GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.