Good morning, it's Paul here with Wednesday's SCVR.

Estimated timings - should be finished by 2pm.

US markets sold off late, last night, so we can expect a poor open today. I'm feeling decidedly nervous at the moment. The news re Covid-19 seems negative - there's talk of a new virus strain which is appearing in children apparently, which sounds ominous. Also, I feel that the bubble in tech & healthcare shares seems inappropriate in its extent, with valuations looking very stretched.

Most UK shares I look at seem very expensive, given the appalling economic situation, and lack of visibility on earnings. This feels like the calm before the storm to me. I wouldn't be at all surprised to see markets lurch down again, and have re-opened my index shorts, to hedge my long portfolio.

Trade Credit Insurance

Yet another massive bazooka looks to have been wheeled out (do bazookas have wheels? I thought they were shoulder-borne?) this morning - the Government is guaranteeing trade credit insurance;

... the Government will temporarily guarantee business-to-business transactions currently supported by Trade Credit Insurance, ensuring the majority of insurance coverage will be maintained across the market despite the challenges posed by Covid-19.

The guarantee will be delivered through a temporary reinsurance agreement to be agreed with insurers currently operating in the market. The scheme will cover trading by domestic firms and exporting firms and the intent is for agreements to be in place with insurers by end of this month.

For anyone not aware, trade credit insurance is where company A sells goods or services to company B, and raises an invoice requesting payment, which is usually paid about 30-60 days later. The trade credit insurance company guarantees that the invoice will be paid. If company B goes bust with the invoice unpaid, then the insurance company coughs up the money instead. It obviously charges a fee to company B for this insurance arrangement.

Unless company A is dealing with blue chips, then it can make sense to insure invoices, providing the fees are reasonable.

It is often the case that, when company Bs go bust, it can be because the trade credit insurer has withdrawn cover, knowing that company B is in financial trouble. Company As then refuse to deliver goods or services, because they cannot get insurance that their invoice will definitely be paid, and instead Company A demands cash up-front (pro forma invoice). This puts a cashflow squeeze on Company B, which has no choice but to cease trading and call in administrators like Begbies Traynor (LON:BEG) or Frp Advisory (LON:FRP) .

This guarantee by the UK Govt is a big deal. This will help oil the wheels of trade, and if badly handled, could also land the taxpayer with a substantial bill. Let's hope the UK Govt drives a hard bargain on fees, otherwise it could be a nicely lucrative deal for the trade credit insurance companies, if they're passing on the risk to the Govt.

It should certainly give a significant boost to UK companies. Therefore a positive move, providing risk is managed properly.

As my old solicitor used to remind me, "All sales are a gift until the invoice has been paid!"

Furlough scheme extended

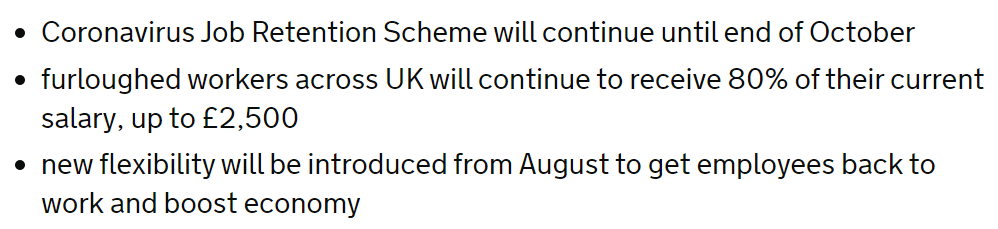

Very important news yesterday, that the furlough scheme which is currently paying the wages of 7.5m UK employees that are on gardening leave, or furlough, is being extended to October.

Here's the Government's announcement. Key points;

.

There was talk of the 80% subsidy being reduced to perhaps 60%, which I think would have probably resulted in mass redundancies, and many workers being paid less that minimum wage. So I think keeping it at 80% was the right decision for now. This avoids a cliff edge at end June, with the possibility of millions of people being made redundant. The enormous cost of this scheme is a worry.

From August, the scheme will allow part-time working, with employers paying for time worked, and the furlough scheme making the pay up to 80% of normal salary.

Some interesting stats from the Govt here;

Today the government is also publishing new statistics that show businesses have benefitted from over £14 billion in loans and guarantees to support their cashflow during the crisis. This includes 268,000 Bounce Back Loans worth £8.3 billion, 36,000 loans worth over £6 billion through the Coronavirus Business Interruption Loan Scheme, and £359 million through the Coronavirus Large Business Interruption Loan Scheme.

Taylor Wimpey (LON:TW.)

(I'm long)

This large cap housebuilder updates the market today. This sounds encouraging;

Housing market conditions have remained stable with signs of increased sales activity and customer interest since the re-start of site activities...

Cancellation rates have fallen and our orderbook has continued to grow.

During the lockdown period we have sold 408 homes net of cancellations, averaging a net private sales rate of 0.30 homes per outlet per week.

Cancellation rates have averaged 27% for the period and represented only 2.5% of the private order book.

Our total orderbook as at w/e 10 May has increased to 11,033 homes (2019 week 19: 10,489), with a value of £2.7 billion (2019 week 19: £2.5 billion).

That confirms my hunch that people still want new houses, despite economic uncertainty, with mortgages dirt cheap (if you can come up with the deposit).

Businesses everywhere are having to adapt & innovate. This is interesting -

... energised by new skills developed in serving customers digitally over the last 7 weeks...

We have remained in active and open discussion with landowners. As we look forward to future land opportunities and housing delivery, we are also encouraged by new Government guidance on opening up the planning system, including the use of social media to conduct consultation processes...

We have enhanced our digital offering to allow customers to complete their entire homebuying journey remotely, from registering their interest through to completion of purchase. We have also introduced a new series of digital tours so our Sales Executives can complete digital viewings, which we will continue to expand.

More detail is given.

My opinion - I'm encouraged by this, and intend sitting tight on my 3 housebuilder long positions - I couldn't chose which one, so bought the 3 main ones, namely Taylor Wimpey (LON:TW.) Persimmon (LON:PSN) and Barratt Developments (LON:BDEV) .

Even in terrible economic conditions, there will always be enough people around who want to buy new houses, and can afford to do so - especially when mortgages are so cheap.

Ten Entertainment (LON:TEG)

Share price: 150p (down 2.6% today, at 08:50)

No. shares: 68.25m

Market cap: 102.4m

Ten Entertainment Group plc ("Ten Entertainment" or "The Group"), a leading UK operator of 45 family entertainment centres, today announces its audited full-year results for the 52 weeks to 29 December 2019 which are below.

This bowling alley company was trading well before Covid-19 effectively shut it down.

2019 results look really good, with LFL revenues up a strikingly (geddit?!!) good LFL sales growth of +8.0%, which seems to have been driven by 4 site refurbishments, and improved food. This improved to +9.3% LFL sales growth in the new financial year (11 weeks to 15 March 2020).

Covid - the company says it's prepared for re-opening, with PPE secured (presumably for staff, and possibly for customers, I'm guessing?), and configuring sites for social distancing. As the company says, its sites are large, hence I imagine social distancing would be more feasible than for bars or restaurants.

Looking back at my notes here on the Govt paper yesterday, I imagine that bowling companies would fall within "Step three", which means they might be allowed to open after 4 July. The big question mark is whether customers are likely to return in sufficient numbers to make the business viable?

Probably the best indicator is China - given that it went into, and came out of, the covid crisis first. We need to look into this, have any readers done so? I can't seem to find much from doing a quick google, but one article from April says that retail footfall was down 66% initially on re-opening a shopping mall, but quickly rose to 80%. That's not bad.

Rough forecast - If TEG could achieve 80% of normal revenues, then gross profit (based on FY 12/2019 actual results) would drop by £14.7, which assuming everything else stays the same, would drop adj EBITDA (as a proxy for cashflow) from £23.6m to £8.9m - still a respectable level of performance. Deducting the £7.4m deprecation charge, and net interest, would take the adj PBT down to about £0.8m. So, in a nutshell, a 20% drop in revenues would put the business around breakeven, but still nicely cash generative.

If revenues fall below a 20% drop, then the business starts losing money at the PBT level. We need to do these sort of sums before buying anything in the retail, leisure, and hospitality sectors.

Liquidity - obviously of paramount importance, it reassures;

Our focus since closure has been on cash conservation and securing the future of the business, and I am pleased to say that we have had very strong support from our shareholders, employees, business partners, banks and the Government. On 26th March we issued an additional 5% of equity, raising an additional £5m of funds. This, combined with our £25m revolving credit facility with the Royal Bank of Scotland, meant that we began the crisis with just over £30m of liquidity headroom.

That sounds fine to me. With the furlough scheme now extended to October (99% of its staff are currently on furlough), cash outflows should be fairly modest, until it can re-open. Cash burn is currently £1.4m per month.

HMRC dispute - note there is a £0.8m exceptional provision for some tax issue, and associated fees. Scant details are given, so I'm not sure what that is about.

Escape Room - it invested £300k for 50% of an escape room business. I imagine that's likely to be a write-off, given the new world of social distancing - which is the complete opposite of what escape rooms are all about.

Divis - on hold for now, as you would expect in the circumstance, which is fine by me.

Balance sheet - looks OK, provided trading can resume at a cash generative level in due course.

My opinion - this looks potentially interesting, but the share is illiquid, so I'd be reluctant to buy anything more than a scrap of them, taking a longer term view that business might recover over time. With low footfall once it is allowed to re-open being likely, then 2020 figures seem likely to be a write-off. That could leave it needing to do another top-up placing in 2021 perhaps?

Overall then I think I'm best described as moderately positive about this share. It might be worth looking at larger rival, Hollywood Bowl (LON:BOWL) which is about twice the size. This sector is a straightforward bet on them being able to re-open soon, not being closed down again by a second wave of covid, and customers returning in sufficient numbers for profits to be decent. So a fair few things need to go right there, hence I understand why many investors would want to avoid this space for the time being.

Connect (LON:CNCT)

Share price: 19.2p (up 6% today)

No. shares: 247.7m

Market cap: £47.6m

Connect Group is today announcing its Interim Financial Results for the 26 weeks ended 29 February 2020, together with a further update on the impact of the COVID-19 pandemic, and subsequent restrictions imposed by the UK Government (the 'lockdown').

The results are pre-covid obviously, so not of that much interest. Connect is a distribution business specialising in newspapers & magazines. It's never interested me. The only attraction used to be big dividends, but these were cut back drastically between 2018-19. Although with the share price now very low, the yield would be just below 5%, even if it only continues paying out 1p per share. That's probably unlikely now, post-covid. There's no interim divi.

H1 adjusted profit before tax was down 12.4% to £16.3m -in line with expectations, and not bad for a half year, at a company with a market cap of only £47.6m. But is the profit sustainable? Probably not. It was already on a downward trajectory, and covid is likely to have done serious damage. Note that the adjusted H1 profit is about £10m higher than statutory profit, so there must be some exceptionals. Yes, it relates to the disposal of Tuffnells.

Net debt (excl. IFRS) is £68.0m (down 12% on prior year). £14.6m was raised from doing a sale & leaseback of Tuffnells properties prior to disposal. Although it looks as if Connect then lent the money back to Tuffnells, if I'm reading it correctly?

.

.

Covid - quite a bit of detail is given. This is the most important bit;

Ongoing operations continue to be profitable and cash generative...

Reduced sales, but many outlets remain open (newsagents, convenience stores, I assume).

Substantial mitigating actions taken, to reduce costs & conserve cash.

No guidance on full year profit/(loss) - this is a cop out, they will have internal forecasts, they just don't want to tell us. Even if it is uncertain, a rough figure, or a range of possible figures, is better than nothing at all.

The COVID-19 pandemic will clearly have a material impact on the Group's performance in the second half of the year, the quantum of which remains unclear. However, our markets and business model are well placed to recover as lockdown restrictions ease.

We know that retailers should be able to re-open in about 3 weeks, so the market might start pricing that into the mix.

Bank facilities are up for renewal in autumn 2020, with a 31 Jan 2021 expiry date of existing facilities. This is clearly a risk factor, and might require an equity fundraising to go alongside bank facilities, possibly? Another concern I have is the size of the bank facilities. If it can get a Govt guarantee, then this may solve this problem.

Outlook - sounds reasonably OK in the circumstances;

Meanwhile, the Group continues to stress test a range of scenarios that consider the length of current restrictions, the lifting of these and any additional measures which may be necessary, and differing levels of recovery against pre-lockdown volumes over varying time periods. While it is not possible to quantify the impact of the lockdown on FY2020 full year Adjusted PBT, the Board is of the opinion that Smiths News can continue to trade profitably through this sustained period of disruption and that its markets and business model mean it is relatively well placed to recover as and when restrictions are lifted.

Going concern note - anyone considering buying or holding this share should pay close attention to this, which sounds rather worrying;

The Group has appointed debt advisors to support them in achieving the most appropriate refinancing arrangement and had entered into preliminary discussions with its existing lenders and was exploring alternative refinancing models earlier in the year, prior to the disposal of Tuffnells. The Directors concluded that the Group was not able to refinance on commercially acceptable terms, and therefore decided to defer the refinancing process until after the disposal of Tuffnells. The Group therefore does not currently have committed facilities for the next 12 months and would not have sufficient resources to repay the facilities on their maturity date.

That's very worrying actually, as it sounds like the existing lenders may not be too keen to renew the facilities at the current level, or at all maybe? Will their attitude improve post disposal of Tuffnells? Directors reassure us below, but talk is cheap;

...the Directors, having considered realistically possible outcomes, anticipate that the Group will be able to secure the refinancing and at an adequate level to support the debt requirements of the Group.

But...

Whilst the Group anticipates completing the refinancing over the coming months following the disposal of Tuffnells (which represented a financial drag on the Group), there is, however, a risk that the Group may not be able to refinance. This indicates that a material uncertainty exists that may cast significant doubt on the Group's ability to continue as a going concern and therefore it may be unable to realise its assets and discharge its liabilities in the normal course of business.

I wish I knew what the probabilities are, of the group being able to refinance or not. Without knowing that crucial information, this share is impossible for me to value. If it cannot refinance, then the only options would be: to sell the business (which might not leave any surplus for shareholders, once debt is cleared), an equity fundraising which would probably more-or-less wipe out existing holders unless they were prepared to put in the new money needed, or insolvency - which would be a zero pence outcome for the share price.

Tuffnells was heavily loss-making, so with that now gone, the chances of a refinancing being possible should be considerably improved from before.

Balance sheet - looks grim. NAV is negative, at £(85.8m). NTAV is £(91.0m).

Receivables could become a problem - how many customers are likely to go bust? Are the receivables insured? (if so then it's OK. If not, then there's clearly an elevated risk of write-offs being needed as customers fail).

Note 9 explains that the £69.7 assets held for sale relates to Tuffnells, and needs to be seen in conjunction with £83.8 liabilities held for sale. So both these items will disappear from future balance sheets, now the sale has completed. The £15.0m proceeds is all deferred, so seems quite likely to turn into a bad debt.

My opinion - this is quite complicated to unpick, but I've come to the conclusion that it's a high risk special situation.

What's the upside? If it can renew bank facilities, and rebuild profitability post-covid, then I could see this share double or triple maybe from here. Downsides - heavy dilution if it needs to raise equity, and some risk of insolvency, if bank won't renew facilities. Although it's rare for banks to pull the plug in situations like this. Given how low interest rates are, it's usually better to gradually reduce facilities, allowing the company to continue trading & use its cashflow to pay down debt. For that reason I suspect divis may not return any time soon, if at all. Hence what's the point in owning this share, at any price?

I can't see enough upside potential to want to risk 100% of my money, hence it's not for me. As a rule of thumb, I only take on high risk shares if I can see a potential 5-bagger+ upside. Good luck to holders. There's still a reasonably decent business here, but woefully under-capitalised. The big dividends of the past were irresponsible, as that hollowed out the balance sheet.

Share price:

No. shares:

Market cap:

Share price:

No. shares:

Market cap:

Share price:

No. shares:

Market cap:

Share price:

No. shares:

Market cap:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.