Good morning from Paul & Graham! Today's report is now finished.

It was great to hear all your feedback, in yesterday's unusually busy comments section. We read, and take on board, all points of view, and it's good to see there are still plenty of investors out there still interested in small caps.

I've been through a few bear markets over the last 25 years, so I know that things can get a little fraught in the bad times. I bet the vast majority of us wished we'd done a lot of things differently over the past year. That's life isn't it, we just have to learn from our mistakes, and then gradually forget those learnings in the next bull market, which is my speciality!

We cover about 500 companies here, from numerous sectors, so there's something for everyone, and you can hopefully use our reviews to do more thorough research of your own. That's the idea! In normal markets, we spot loads of good stock ideas, and we warn people away from lots of dodgy things too. But ultimately, the buy & sell decisions are entirely yours.

In a bear market like now, most small caps have done badly. That's often when the best buying opportunities emerge for the next bull market, in my experience (e.g. I had multibaggers galore in 2003). So we'll try to sharpen our focus, but essentially the show goes on, and we'll do our best. You'll continue to be able to pick ideas, and details from our reports, to add to your own research process. Agree or disagree with us, when it comes to opinions. Sometimes we're right, sometimes we're wrong - same as everyone.

Agenda -

Paul's Section:

Firstly a few catch-up items -

Card Factory (LON:CARD) - I review its interim results, and can see both bull and bear arguments. Overall though, the weak balance sheet, and total reliance on hefty bank facilities, doesn't give me enough confidence to want to invest as we enter a recession.

Redde Northgate (LON:REDD) - a positive update, and a strikingly cheap valuation, with the dividend yield now above the PER - not something we see very often for businesses that are not in terminal decline. The valuation is now fully asset backed too, on a NTAV basis. Looks a smashing value buying opportunity to me, providing nothing goes wrong.

Finsbury Food (LON:FIF) - I enjoyed an excellent webinar from management yesterday, via InvestorMeetCompany. This is another company that is trading well, taking current macro problems in its stride so far, and has an attractive valuation too. Thumbs up from me. Although it tends not to attract a high valuation multiple, even in the good times.

Pressure Technologies (LON:PRES) - almost halved in price yesterday, on a profit warning. Bad luck to holders. Says it's likely to breach banking covenants imminently, not a good look obviously. However, it only owes the bank £2.4m, so that should be fixable with a waiver, or a small placing, but on what terms? Positive outlook comments on order book & pipeline. I do question though why it is listed? Too small, and with poor performance. Overall, it's difficult to see any compelling reason to hold, or buy this share, based on the information currently available.

On to today's news:

Boohoo (LON:BOO) (I hold) - interim results are poor, with profits largely disappearing. Reduced outlook for the full year also. However, it's not a disaster, and the balance sheet looks robust with plenty of freehold property, and net debt of only £10m. Although the structure of £325m borrowings, and £315m cash, raises some questions. I've been disastrously wrong on this share to date, but with extensive short positions needing to buy back at some point, I reckon we could now be at or close to a low in the share price.

Glantus Holdings (LON:GLAN) [no section below] - this is another disastrous 2021 float. It’s down 61% today to 13.5p compared with a May 2021 IPO at 102p per share. Today it warns that revenue & EBITDA will be significantly below market expectations. Worse than that, it’s almost run out of cash, and is negotiating with high cost lender Beach Point Capital for a $1.5m working capital facility. Looking at its previous accounts, it’s very obvious that this Irish software company was floated with inadequate financial strength (a negative NTAV balance sheet). So it needs to do a placing, but who would be interested, and at what price? Looks very high risk to me, just purely for traders/gamblers now. No section below.

CML Microsystems (LON:CML) - a rare (at the moment!) ahead of expectations trading update for H1 (to Sept 2022). It's also getting a forex tailwind from the strong dollar, as 80% of revenues are priced in dollars. Immensely strong balance sheet, with surplus cash and property, see our archive here for more detail. This share looks very interesting, I like the asset backing, and strong trading (with optimistic sounding outlook comments too).

Graham's Section:

K3 Capital (LON:K3C) (£173m) - yesterday’s final results were very encouraging as K3 Capital continues its mission to be “the leading mid-market specialist advisory business to SMEs” within its areas of expertise. I’ve not looked at this one before but I’m impressed by the company’s organic growth, its marketing strategy, and its financials with solid operating profits regardless of your view on the adjustments applied to it. The valuation is reasonable, too: I get nervous if I ever see a professional services stock at a very high earnings multiple, but K3 Capital doesn’t have that problem! More detail below.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Card Factory (LON:CARD)

45p

Market cap £154m

Card Factory, the UK's leading specialist retailer of greeting cards, gifts, wrap and bags, announces its interim results for the six months ended 31 July 2022 ('HY23').

Here are my notes from a quick skim of the H1 results -

Revenues up strongly to £198m, reflecting post pandemic re-opening of stores.

Note there is an H2 bias to trading historically.

Moved back into H1 profit, of £14.3m, or £10.8m if we strip out one-off items.

Net bank debt of £96.6m still strikes me as a bit too high, but it says this tends to be higher at the half year than the full year. Although intra-year spikes can be higher still.

Cost of debt worries me, if interest rates soar in the current environment, this could become expensive in future.

Products are a value proposition - a positive in these price-conscious consumer times.

Energy costs hedged to Sept 2024 - very good.

Conscious of wage inflation, but plans to raise prices to mitigate this.

Outlook - unchanged full year expectations (pity they don’t say what those expectations are!)

Current trading - sounds OK, with positive LFLs since the half year end.

Online - remains a huge gap, with still negligible online trading. I remain concerned that Moonpig & Funky Pigeon have snapped up this (lucrative) business from under CARD’s nose.

No divis, as focused on debt reduction.

Balance sheet is still weak, with NAV of £237m, less intangibles of £322m, gives NTAV of negative £(85)m. That probably rules it out for me.

Going Concern statement - all sounds OK. But bear in mind this business is entirely reliant on its bank facilities, which the bank clearly wants to gradually reduce, not a comfortable position to be in.

Cashflow - negative, as stretched creditors (e.g. rent & VAT arrears) normalise.

Business rates relief ended in April 2022, so will have been a partial benefit in Feb & Mar 2022 that won’t repeat in future.

Valuation - I can’t find any broker notes. But working on the Stockopedia broker consensus forecasts, see that they have reduced a lot in the last year -

.

Taking this in combination with a weak, negative NTAV balance sheet, with a lot of debt (especially at seasonal peaks), then the PER really should be low, in single digits, which it is -

.

What happens next, given consumers tightening our belts this coming Christmas? Who knows! In my experience, retailers are always nervous about Christmas, every year, but the big, late surge in spending always happens, every year without fail. Even when the economy is struggling.

CARD has a decent value for money product offering, with very cheap multi-buys to lure you in, just inside the shop doors. That is perfect for the belt-tightening times we live in, and recent trading updates seem to show that retail/hospitality offering value for money are still doing well, whereas other weaker offerings are struggling.

CARD’s vertically integrated business model, making the cards itself, maximises profit margins. Trading is recovering, and it’s profitable again now. So there’s a pretty decent bull case for this share.

On the negative side, I’m just not comfortable with the balance sheet & excessive debt. That’s not a good position to be in, when the economy is going into recession. Although to be fair, CARD has managed the situation very well, and its bank has been highly accommodative, but is charging a big lending margin for their patience, which could see lending costs hit c.10% if interest rates shoot up, as expected in the coming months. There might be some interest rate hedging, but I couldn’t find any detail on that, other than a small amount in note 14 of £1.0m in derivatives relating to interest rates. We need more detail on that.

Overall, I’d say the current share price probably looks about right, once you balance the bull & bear points.

Note that the StockRank is high, at 82 -

.

Redde Northgate (LON:REDD)

295p

Market cap £699m

Redde Northgate plc (LSE:REDD), the leading integrated mobility solutions platform providing services across the vehicle lifecycle…

Encouraging start to FY2023

This relates to FY 4/2023.

Continuing to trade well.

UK&I supply of new vans, “remains tight”.

UK&I supply of new cars, “showing early signs of improvement”.

Spain supply of new vans, “better than expected”, and fuelling growth.

Residual vehicle values are still high, but “softening gradually” as expected.

Profit margins “remain strong”.

Inflationary pressures “actively managed”.

Redde division (accident hire cars) has seen a “strong rebound” post-Covid.

“Little impact” on traffic activity so far from higher fuel costs or recessionary fears.

Car fleet continuing to grow.

Previously announced new contracts being implemented.

Completed acquisition of Blakedale (specialist vehicles).

Share buyback increased to £60m in Aug 2022, c. two thirds now done.

Leverage “well within” policy of 1-2x (EBITDA, presumably?)

Refinanced in Oct 2021, with borrowing maturities extended (up to 10 years).

Divis - 15p final divi proposed (on top of 6p interim divi). Total 21p = 7.1% yield

Diary date - 7 Dec 2022 for interims (to end Oct 2022).

Outlook - a bit vague, but seems upbeat -

Whilst mindful of economic uncertainty, the Board remains confident that it has the right strategy to deliver long term sustainable value. The Group is supported by its enhanced mobility solutions platform, the structural growth in outsourcing, a diverse revenue stream and a broad spread of customers providing the business with quality, repeatable long-term contract-backed earnings.

My opinion - this all sounds most encouraging, and makes me wonder if this is a buying opportunity? The divi yield is now above the forward PER, not something we see often for companies in rude health. Plus the share price is fully asset backed with net tangible assets.

REDD looks like a highly attractive value opportunity to me.

The only downside risk I can think of, is of losing a major contract, which did smash the share price a few years ago, but it later recovered.

Also there was talk of profits being boosted by high residual values of secondhand vehicles, which is likely to be a factor that gradually unwinds over the next year or two, as new vehicle supply (constrained by semiconductor shortages) gradually normalises.

The more I think about this, REDD should probably be on my watch/buy list.

.

.

The Stockopedia computers like REDD too -

.

Finsbury Food (LON:FIF)

79p

Market cap £103m

Finsbury Food Group Plc (AIM: FIF) is a leading UK and European manufacturer of cake and bread bakery goods, supplying a broad range of blue-chip customers within both the grocery retail and 'out of home eating' foodservice sectors including major multiples and leading foodservice providers.

These results relate to the 53 weeks to 2 July 2022, so I’ll call that FY 6/2022.

Management delivered an excellent webinar yesterday, on InvestorMeetCompany. Here are my notes from the webinar -

Interesting slide deck is here

Revenues +14% to £357m (volumes up 8.7%, balance is price rises)

Profit before tax £17.0m (up 12.1% on LY)

EPS diluted 10.1p, up 17%

Divis total 2.5p (yield of 3.2%)

10 different macro-economic challenges mentioned in slide 5 - e.g. energy, raw materials costs, labour, supply issues shortages of drivers, etc.

“Not in a bad position”. Food is defensive in a downturn. Our products are affordable treats.

Kids celebration cakes are quite a big part of the business.

Strong balance sheet.

Well invested, efficient business.

Recovered from pandemic.

Split of revenues: 48% cakes, 38% bread, 14% overseas.

80% is sold to retailers (mainly supermarkets), 20% is foodservice (e.g. coffee shops).

Customers - mainly supermarkets (c. 50% of business is to Tesco, Co-Op, and ASDA)

H2 saw improved operating profit margin, as prices increases fed through.

Gross margin was slightly down for FY 6/2022 at 32.4% (LY: 32.9%)

Operating profit margin 5.0% (LY: 5.1%) - but note it was only 3.9% in H1, so stronger H2.

Net bank debt £20.6m, up from £13.1m LY. Only 0.7x EBITDA.

Overseas business: have increased from 50% ownership, to 85%. Planning on acquiring final 15% from the founders.

Capex accelerated, and took advantage of 130% capital allowances. Was £12.5m this year, up from £6.2m LY. Maintenance capex is about £4m p.a.

Free cashflow was £8.8m (down from £16.4m LY)

Major acquisition (similar size business to FIF) was progressed, but put on hold when FIF share price fell back (hence valuation metrics no longer worked). Not gone away, hoping to revive the deal at a lower price. This cost £1.8m in non-recurring costs, adjusted out.

New bank facility of £120m gives lots of M&A firepower. Very strong banking support.

Penson deficit at one subsidiary only, of £6.6m. Annual contributions are £763k, won’t drop as committed to this, agreed with trustees.

Lots of organic growth opportunities, e.g. artisan bread, and “free from” products, being pursued.

Price rises - challenging to implement, but most customers agreed, as the case for price rises is so clear, due to higher costs.

Working with customers to make things more efficient & strip out costs, e.g. optimising pallet sizes.

Question re broker research - yes take your point, MiFiD has made it more difficult for brokers to make research available to private shareholders. There is commissioned research available.

My overall impression of management is that they seem calm, knowledgeable, and competent.

Looking next at the figures in the RNS -

Balance sheet actually isn’t that strong, but it’s OK. NAV is £118.9m, less intangibles of £87.4m, gives NTAV of £31.5m. That’s OK, but there’s a fair bit of bank debt: £37.0m gross, and £29.6m net of £7.4m cash. That doesn’t tie in with the company’s figure of £20.6m net debt. The difference of £9m is explained in note 9 - they’ve included leases within interest-bearing debt, which is a poor way to present the information. I much prefer lease “debt” to be shown on the balance sheet in a separate line, to avoid this confusion. It’s very different to bank debt, so why combine them into one line?

Going Concern note is fine - no concerns here.

My opinion - we’ve reported positively on FIF here before, it’s a decent company I think.

I’m impressed at how resilient FIF has proven itself, in dealing with numerous challenges, especially inflation & supply chain problems. It has proven an ability to pass on higher costs to customers, a key strength right now, that gives me increased confidence in the shares, because I was previously worried it might get overtaken by supply chain costs & problems. Today’s results show that worry was misplaced, FIF is navigating choppy waters with considerable skill, it seems.

I’m not keen on management funding M&A with more debt, which of course is likely to be a lot more costly in future (there are swaps on existing debt to fix the rates). Since FIF’s own shares are on such a low PER, then this really hampers their acquisition ambitions - leaving management with two unpleasant options - either run up dangerous levels of bank debt, or excessive dilution for issuing new shares on a low PER, which would run the risk of acquisitions actually being negative for shareholders.

The other issue, is that even in the good times, FIF shares don’t tend to trade on a PER much over 10. So although the PER of 6.9 currently looks cheap, the upside on a re-rating is probably quite limited, if the past valuations are any guide (see graph 4 below) -

.

Overall though, the valuation metrics below are clearly attractive, for a business that is growing, and more than keeping pace with inflation. So as a long-term hold, I see this as a good share that should do fine over the long-term.

.

.

Pressure Technologies (LON:PRES)

33.5p (down 47% yesterday)

Market cap £10m

Bad luck to shareholders in this small, specialist engineering group, with a profit warning issued yesterday.

It says that H2 has improved from H1, but not enough to recoup the losses from H1, and below previous expectations. A variety of problems have emerged to cause this disappointing performance.

Outlook comments sound reasonably upbeat, with a good order book & pipeline.

Banking arrangements - this will have spooked a lot of investors - bank covenants are expected to be breached at end Oct 2022. Discussions with the bank are taking place. In more normal times, I would expect the bank to give a covenant waiver (for a hefty fee, to reflect the higher risk) and then ask the company to do a placing, to get the bank off the hook maybe?

It looks like bank facilities have already been halved, from £4.8m to £2.4m, and is currently fully drawn. Surely a placing could be done to sort out such a small level of bank borrowings?

My opinion - this doesn’t look a terminal situation, so it should be fixable. Although a placing could come at a deep discount, given miserable macro and market conditions. Or there’s always a risk that a predator could pounce, and force the company into administration, thus wiping out existing equity.

Hence I think we have to see PRES as now high risk.

Also, given a lamentable performance in recent years, I have to question why PRES is listed on the stock market? It doesn’t make any sense to me. They’re probably better off de-listing, and stripping out all the costs & hassle of a listing. Which I’m afraid is another reason to avoid the shares.

Years ago, I recall, PRES had a patch of good profits, and there was a massive spike in the share price in 2014. Since then, it’s just ground downwards. So maybe something needs to happen here - change of management, de-listing, takeover, etc.?

I see from the shareholder list that the top 2 holders are Schroders & Harwood Capital, which can both be activist when needed - not always to the benefit of small shareholders though.

It’s difficult to see much of a reason to continue holding this share, I’d be tempted to ditch it & move on.

.

Boohoo (LON:BOO) (I hold)

33p (down 11% at 08:19)

Market cap £415m

Poor results, but that’s already in the share price, which has fallen over 90% from the highs, along with peer ASOS (LON:ASC) and many other eCommerce companies. It’s incredible how this sector has gone from so highly rated, to completely bombed out. There could now be some nice buying opportunities amongst the wreckage.

So these numbers need to be seen in the context of a share price that’s collapsed - are things really that bad?

Some key numbers for the 6 months to 31 August 2022 -

H1 revenue £882m (down 10% on pandemic-boosted last year H1)

Gross margin also down, at 52.5% (LY H1: 54.6%)

Adj EBITDA £35.5m (LY H1: £85.1m)

Adj profit before tax (PBT) £6.2m (LY H1: £63.8m) - clearly a very poor result, but at least it’s still profitable at a time when competitors have been going bust (e.g. Missguided).

Statutory profit is loss-making, at £(15.2)m before tax.

Guidance - is a profit warning, with previous 4-7% EBITDA range now reduced to 3-5%. In the glory days, it used to be 10%+, which is now looking a distant memory, unlikely to be recouped any time soon, if at all.

Geographic breakdown - a big drop in USA sales of -29% is the main culprit for the drop in revenues, with other regions (UK, Europe, RoW) being around flat, combined.

Ongoing high air freight costs.

Individual brands - are not split out, so it’s a fair assumption to make that the core brands are going backwards, and partially masked by growth in the newly acquired brands.

Balance sheet - includes freehold land & buildings in the books at £131m. The commentary mentions that £96m has recently been spent on freeholds, which includes a new Soho office, which I visited recently when laying some flowers for her Maj - will try to dig out my short video of this. So if things were to get tight, the freeholds are a substantial asset to fall back on, that could be sold or leased back (edit: without much operational impact for the Soho office, as people can be easily relocated to say serviced offices).

Cash & debt is unusual, in that BOO has fully drawn down a newly enlarged £325m borrowing facility (which will incur much larger interest costs than in the past), whilst simultaneously sitting on a cash pile of 315m. So net debt is only £10.4m, not a concern at all. It says this arrangement gives flexibility for investment, and for intra-month cashflow moves, but it seems a rather extreme setup. My main worry is that, if trading deteriorates further, then could any covenants on the borrowings become a problem? Nothing is said about covenants, and the going concern statement doesn’t cover this issue either. So that’s my main query - what are the bank covenants, and what is the risk of a breach? I would work on the basis that the large bank facility might need to be reduced somewhat.

My opinion - when a share price drops by 90%, you already know the numbers are going to be weak, as indeed they are. But these numbers are not a complete disaster by any means. Solvency doesn’t look an issue (although I would like to know more about the bank facility terms). Costs can be scaled up and down, remember that BOO spends a huge amount on marketing for example, and paying influencers. That can be tweaked as required, giving a lot of flexibility compared with traditional retailers and their often ruinous fixed cost bases.

BOO is becoming more efficient gradually, with automated warehouses going live, which should reduce handling & dispatch costs.

As air freight improves, and supply chains generally loosen up again, then margins could improve again in future.

Set against that, this sector is fiercely competitive, but others are falling by the wayside (e.g. Missguided, and ISawItFirst [set up by Jalal Kamani, Mahmud’s brother] - both have ended up in fire sales to Mike Ashley). So there are likely to be fewer, but larger players in this sector, with BOO being one of the last ones standing probably.

Chinese behemoth Shein must be having some impact too, although its slow delivery & returns times are a key competitive disadvantage for customers who want “fast fashion” - i.e. something to wear tomorrow for a night out, not in 2-3 weeks. Speed to market remains a key strength for BOO, but it had to clean up its supply chain (at a considerable cost) whilst Shein and others seem free to do whatever they want, with little to no scrutiny - obviously unfair.

It’s now all about two things - (1) valuation - now down to little more than £400m market cap, for a big group, with close to £2bn revenues, the shares could now be too cheap, and (2) to what extent can it rebuild profits from effectively around breakeven right now?

My opinion doesn’t really matter, because I got it completely wrong over the last year. But for what little it’s worth, I do think BOO should be able to rebuild margins somewhat, over time, and there are good reasons to expect that (e.g. supply chains normalising, freight costs coming down, warehouse automation).

We should also consider the bear side - what if trading continues to deteriorate? Costs would then have to be cut (especially marketing), which would further slow growth. High returns rates are a continuing bugbear (although the introduction of admin charges for returns could alleviate this issue). Bank covenants could become a problem, which might affect future liquidity.

On balance though, I think we could be at or near a bottom for this share price. Remember too, that BOO is being extensively shorted, who will all need to buy back at some point. Hence ironically lots of buyers are already lined up, so if there’s a short squeeze, it could rebound strongly. There’s also the issue of whether the founding family will want to continue as a listed company, with the market cap now in small cap territory? Hence another risk for shorts is if the family decide to buy it back from the market (although they’re not known for over-paying for anything).

With this type of investment, I think it's so important to separate out the emotions of a disastrous share price performance to date, from a realistic assessment of what the future holds. There could be a nice recovery in share price here, at some stage, if fundamentals begin improving. Or there might not, if trading conditions continue to be difficult.

It feels too early to be factoring in an improvement in consumer sentiment. Much too early. But it will happen eventually.

.

.

CML Microsystems (LON:CML)

400p (up 15% today, at 11:10)

Market cap £64m

CML Microsystems Plc (the "Group" or the "Company"), which develops mixed-signal, RF and microwave semiconductors for global communications markets, is pleased to today issue a trading update for the first half of the current financial year (six-month period to 30 September 2022).

Positive momentum, trading ahead of market expectations

Strong trading in H1.

Revenues “well ahead” of last year on constant currency basis.

Further boost from the strong dollar (80% of revenues are in dollars)

Gross margin “robust”.

Costs as expected.

Forward order book is “healthy”.

Overall -

As a result, profitability is expected to be significantly ahead of management's earlier expectations.

At the current rate of trading and based on current exchange rates, the Board expects that for the full year ending 31 March 2023 both revenues and profitability will be ahead of market expectations.

Outlook - this bit sounds interesting -

The Board remains confident in the Group's strategy and its ability to deliver significant, sustainable growth over the coming years.

Valuation - many thanks to Shore Capital for an updated note today. It’s forecasting 15.5p EPS for FY 3/2023, but it sounds like CML is trading ahead of those figures.

Also a key point is that CML is cash rich, and has surplus land (with long-standing plans to develop a small business park on its existing HQ site). When you take all that into account, the apparently high PER looks a lot more reasonable. These are known factors, so already baked into the share price.

Also, this share is a nice place to be hiding in the current market chaos, because the stronger the dollar gets, the more CML’s profit is boosted. So expect sparkling numbers when it next reports.

Graham’s Section:

K3 Capital (LON:K3C)

Share price: 235p (-2%)

Market cap: £173m

In response to popular demand, I’m taking a look at K3 Capital Group.

Disclosure: I don’t recall ever having written about this stock before. Being unable to rely on prior analysis is a disadvantage, but at least I am bringing fresh eyes without any preconceived notions!

From their homepage:

K3 Capital is a multi-disciplinary and complementary group of professional services businesses advising SMEs.

The subsidiaries are involved in services relating to corporate finance (business sales), tax advice and business recovery (i.e. restructuring).

Final results for FY May 2022 were published yesterday. Here are the highlights:

- Group revenue +50% to £70.7m. Organic revenue +24%.

- The two largest divisions by revenue - Restructuring and Business Sales - both saw organic growth of 21%.

- The smaller division - Tax - saw organic growth of 35%.

- Profits are highest in Business Sales (EBITDA £10.8m), despite this division having lower revenues than Restructuring (EBITDA £6.7m)

And in terms of overall profits and cash:

.

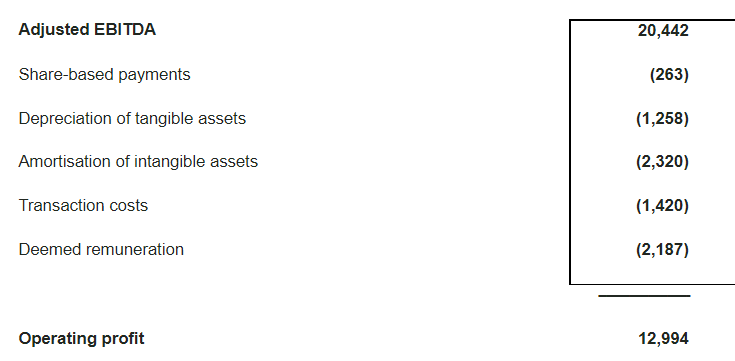

- Group adjusted EBITDA +30% to £20.4m.

- Cash £13.7m

- EPS +11% to 20.64p

- Full-year dividends of 12.1p (last year: 9.1p)

All divisions “performed ahead of forecast, demonstrating strength and resilience of the business model”.

In business sales, the market is resilient and there are “more transactions completed than ever before”. This division is “the number 1 advisor by deal volume” in the UK.

In tax, there have been a “record number of claims submitted to HMRC”. This division benefits from “a high degree of contracted and therefore recurring revenue”.

In restructuring, as we have discussed before (e.g. in relation to Begbies Traynor (LON:BEG) ) the loss of Covid supports and other headwinds are increasing demand for insolvency services.

Outlook - complementary acquisitions are being explored, consistent with the strategy to have both organic and acquisition-led growth. There is a confident outlook for FY May 23, with a “robust pipeline” for the year ahead:

FY23 Q1 has seen continued momentum across the Group, delivering turnover in excess of £20m and Adjusted EBITDA of c.£6.5m* in the three months to 31 August 2022

A simple annualisation of the above figures would see revenues of £80m and adjusted EBITDA of £26m for the year, i.e. continued strong growth. The “mid-term ambition” is to reach £50m EBITDA.

The Chairman says:

"FY22 has been transformational for K3 as it continues to develop. The business has the foundations in place to be recognised as the leading mid-market specialist advisory business to SMEs.”

Acquisition and growth strategy

Six acquisitions were completed since the start of FY 2021. Management appear to be delighted with how they have performed.

The idea is to create synergies and boost each acquired company using K3C’s “unique distribution platforms, incorporating direct marketing, cross-selling opportunities and an ever-expanding professional introducers' network through our K3 Hub platform”.

I suspect that the K3 Hub is an important part of the secret sauce that has helped to accelerate K3C’s growth.

When launched, it was described as being aimed at UK accountants. Read more about it here. It now has over 2,000 people signed up.

For accountants, they get a fresh income stream (referral fees) and a range of helpful benefits designed by K3C. They also get an easy answer to the question of where to send clients who need more specialist advice.

For K3C, they get introduced to new potential customers by people these customers trust.

It’s smart business, and is based on the same flawless logic that sees Boohoo (LON:BOO) paying large fees to its social media influencers. To find new customers, sometimes you first have to find (and pay) the people that these customers trust.

But new businesses acquired by K3C don’t just get plugged into the K3 Hub. They also get onto K3C’s “data-driven marketing platform”. The company has a “leading SME data set and proprietary marketing platform”.

And they get access to the mutual cross-selling opportunities that arise between all of K3C’s subsidiaries. After all, the same companies often need help with M&A, restructuring and tax advice around the same time or within the space of a few short years!

Income statement

There has been a lot of talk about EBITDA.

Here is the translation of EBITDA to operating profit:

Let’s not get into the debate again around adjustments: I will leave it to the reader to decide if they wish to give K3C the benefit of the doubt around the amortisation of intangible assets.

From my point of view, I would only be completely satisfied to allow the following adjustments:

- Transaction costs

- Deemed remuneration

So for me, underlying operating profit is around £17m. But at least this is not a million miles away from the company’s adjusted EBITDA figure. The discrepancy between my view and a company’s view is often enormous!

Balance sheet

I’m not expecting to find much tangible equity. Indeed, net assets are £66m, including £57m of intangibles (tangible equity is the difference between these numbers).

At least this is positive, and the company still has net cash even if you deduct borrowings (£2.2m) and contingent consideration (£6.5m) from the gross cash balance (£13.7m).

My view

As far as the professional services sector goes, this might be one of the best stories I’ve come across in recent years. It looks like K3C has nailed the marketing side of the business, perhaps by putting in far more effort and placing more emphasis on it than their competition.

When customers find it difficult to differentiate between products, it’s the marketing that makes the difference: I think K3C has taken this principle and applied it to mid-market SME advice.

Are the shares a bargain? I’m somewhat biased against the professional services sector, having seen too many horror shows in this sector over the years (remember Fairpoint?), so I’d still be nervous if I saw a high PE ratio here.

But that’s not the case: K3C has a fairly average earnings multiple.

So I’ll take a positive view on this stock, given the average valuation against earnings and some positive features:

- Real organic earnings growth.

- An acquisition process that appears to be working.

- Huge success in marketing and customer referrals.

- Net cash, positive tangible equity, and arguably reasonable earnings adjustments.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.