Good morning, it's Paul here with the SCVR for Wednesday.

It's quiet again for news today.

Timings - 2pm finish, them I'm off to walk the dogs to the De Beauvoir Arms for a £7 lunch meal deal!

Update at 14:16 - today's report is now finished. I'll take my chromebook with me to the pub, to read/respond to any interesting reader comments. There have been some excellent comments today, thank you! It's always great when readers with detailed knowledge on shares write up your thoughts, as inevitably, covering c.500 companies, I can't dig that far into the detail for everything.

Agenda - just a few small cap results & trading updates today;

Sosandar (LON:SOS) - Half year trading update

Vertu Motors (LON:VTU) - Interims to 31 Aug 2020

Kromek (LON:KMK) - Final Results

Cambridge Cognition Holdings (LON:COG) (I hold) - contract win

This one is too small & illiquid for a separate section. It's picked up another reasonable-sized contract win (£750k). Noteworthy points: the client is doing clinical studies on a part-virtual basis, which COG's service is ideally geared up for (it tests the impact of experimental drugs on cognitive capacity, using tests on iPads). Caregivers can input information using an app, again this is ideal in a covid world. COG is configuring existing modules, rather than designing bespoke software - that should be good for profit margins, as it's recycling existing work. My view - it's starting to look as if COG could be getting there, after years of not quite managing it. Shares are ridiculously illiquid unfortunately.

Sosandar (LON:SOS)

16p (up 7%) - mkt cap £30.8m

(I hold)

Strong performance through a challenging trading environment

Sosandar, the online women's fashion brand, is pleased to provide the following trading update covering the six-month period ended 30 September 2020.

The bullet points come across well. Overheads have been slashed, which together with furlough assistance, has seen a remarkable fall in cash burn. Net cash has remained level at £4.3m, over the last 3 months. I was sceptical that SOS would make it through the busy autumn/winter season without another fundraising, but it's looking possible now. This is a reminder of how flexible online retailing is - the costs can be cut drastically if required, because they're nearly all variable costs (marketing spend, and people basically).

Gross margin is down a bit, but at 52.3% is still very good for the small size of company.

Customer returns are tracking usefully lower than last year, at 42% vs. 49%.

The new sales channel, through Next, and John Lewis is doing well.

Decent growth in revenues, but a pity we're not given any figures on profitability;

Revenue of £4.3 million, a 52% increase against the same period in the prior year, with a substantial improvement in EBITDA loss

Sept 2020 revenues up 36% year-on-year - good, but nowhere near enough to hit very aggressive full year targets, now that we're coming into the peak autumn/winter period.

My opinion - I remain of the view that Sosandar is definitely going to succeed. The only questions are how long will it take, and how much more cash will it need to raise? I'm very impressed with how management drastically reduced spending when covid struck, and have conserved cash much more tightly than I thought would be possible, hence avoiding another fundraise this year.

The problem now is that forecasts for H2 look unachievable. I can't see Sosandar getting anywhere near £21.4m full year revenues. More realistic is probably somewhere between £12-15m full year revenues for FY 03/2021. If achieved, that should mean a reduced loss, as costs were slashed so much in H1, but we'll see when we get the interim results in early Dec.

The product range is broader than last year, for A/W, although I imagine there's bound to be some impact from fewer Xmas parties, and other get-togethers requiring new frocks. Although as SOS management has told us before, never under-estimate the propensity of women to buy new clothes just to cheer themselves up, and everybody needs a bit of that, in this annus horribilis as the Queen might describe it.

It's good to see that SOS shares are a little above the original listing price of 15p, so this has been quite a reasonable performance, given the mountain to climb, of creating a new brand from scratch, and overcoming the enormous barriers to achieving scale in online fashion.

Let's see what the crucial autumn/winter season looks like. After that, I reckon we're probably looking at another fundraise, but maybe only 10% dilution, which isn't the end of the world, then the company should be (in 2021) on the home straight towards breakeven. That's when it starts to get exciting, because from that point onwards, growth becomes self-fuelling.

In conclusion, there's everything still to play for here. You couldn't wish for a more dedicated, and tenacious management team either. They've proven the doubters wrong, in terms of whether two women from a fashion magazine background could create an online fashion retail business. They've done it, albeit at considerably higher cost than the original business plan. But show me any startup that achieves the original figures!

.

.

Vertu Motors (LON:VTU)

31.1p (down 1%) - mkt cap £115m

Emerging strongly from the Lockdown

Vertu Motors plc, the automotive retailer with a network of 135 sales and aftersales outlets across the UK, announces its interim results for the six months ended 31 August 2020 ("the Period").

This looks impressive;

· The Group delivered Adjusted1 profit before tax of £4.7m with no exceptional items in the Period, on sales of £1.12bn, despite 10 weeks of closed sales showrooms:

o Quarter one saw a loss of £14.3m due to the lockdown

o Quarter two, in contrast, generated a profit of £19.0m, significantly in excess of the prior year period profit of £3.8m, emerging from lockdown with a very motivated team

o Result aided by government support in the form of the furlough grant and business rates relief

Current trading/outlook also looks impressive;

· Record trading performance delivered in key month of September

· The result for the 7 months to September 2020 gives the board confidence that a strong financial outcome will be delivered in the full financial year

Other bullet points also impress;

· Very strong cash flow performance - operating cash flow of £80.0m in the period and period end net cash2 of £36.5m

· Net tangible assets per share of 46.5p (2019: 46.1p)

· Delivered £10m of annualised cost savings

In the past I've described Vertu as a hybrid - part property company (with lots of freehold properties) and part car dealers. Hence the downside risks are covered by assets, and you get the upside thrown in almost for free, a very nice investment proposition.

FCA review of vehicle finance - potential risk here, but doesn't sound serious;

Our current modelling suggests that the changes will not have a material impact on Group earnings from finance commission. Ultimately, however, this will be, to some extent, impacted by how competitors in the market react to the changes. The changes do therefore pose a future earnings risk, which the Board will monitor.

Brexit - changes to VAT invoicing arrangements are likely to have an adverse cashflow impact;

... the change is anticipated to reduce the Group's current cash flow advantage in respect of VAT by up to £15m, depending on seasonality.

That's not serious, given the strength of Vertu's balance sheet.

It's possible there could be disruption to supply of vehicles from the continent, or even import tariffs, who knows. When push comes to shove, the idea that the EU would cut itself off from a major export market (the UK) is ludicrous, so it wouldn't bother me if I held VTU shares. These things always get sorted out in due course. It doesn't look as if the stock market is bothered either, with Vertu shares up strongly in recent weeks.

.

.

Outlook - the usual covid uncertainties are mentioned.

This bit sounds particularly interesting;

The Board is actively considering several opportunities for the expansion of the Group and expects such consolidation opportunities will be significant over the coming months and years. At the same time, dealership numbers in the UK are likely to face downward pressure. This should improve the profit potential of those that remain, with more scaled operations gaining from cost and marketing synergies.

My opinion - I've always been positive about this company. Today's update sounds excellent. It's very reassuring that the company coped with lockdown with such aplomb, which gives confidence that it could cope well with any future covid restrictions.

Despite the recent rise in share price, I think this still looks decent value. Now might be a good time to buy up weaker competitors, and it sounds like something along those lines could be in the pipeline.

As before, this share gets another thumbs up from me.

.

Kromek (LON:KMK)

9.35p (down 10%) - mkt cap £32m

This is bouncing a little from an earlier intra-day low of 8.0p. I see the Chairman has bought 100k shares at 8.6p today (total holding now 300k), which is too small to affect my view of the share.

Checking my previous notes, I covered Kromek's FY 4/2020 profit warning here on 1 May 2020. My conclusion then was that the £60m market cap looked inexplicably high, considering lacklustre performance over 6 years as a listed company. The share price has almost halved since then.

Kromek (AIM: KMK), a worldwide supplier of detection technology focusing on the medical, security screening and nuclear markets, announces its final audited results for the year ended 30 April 2020.

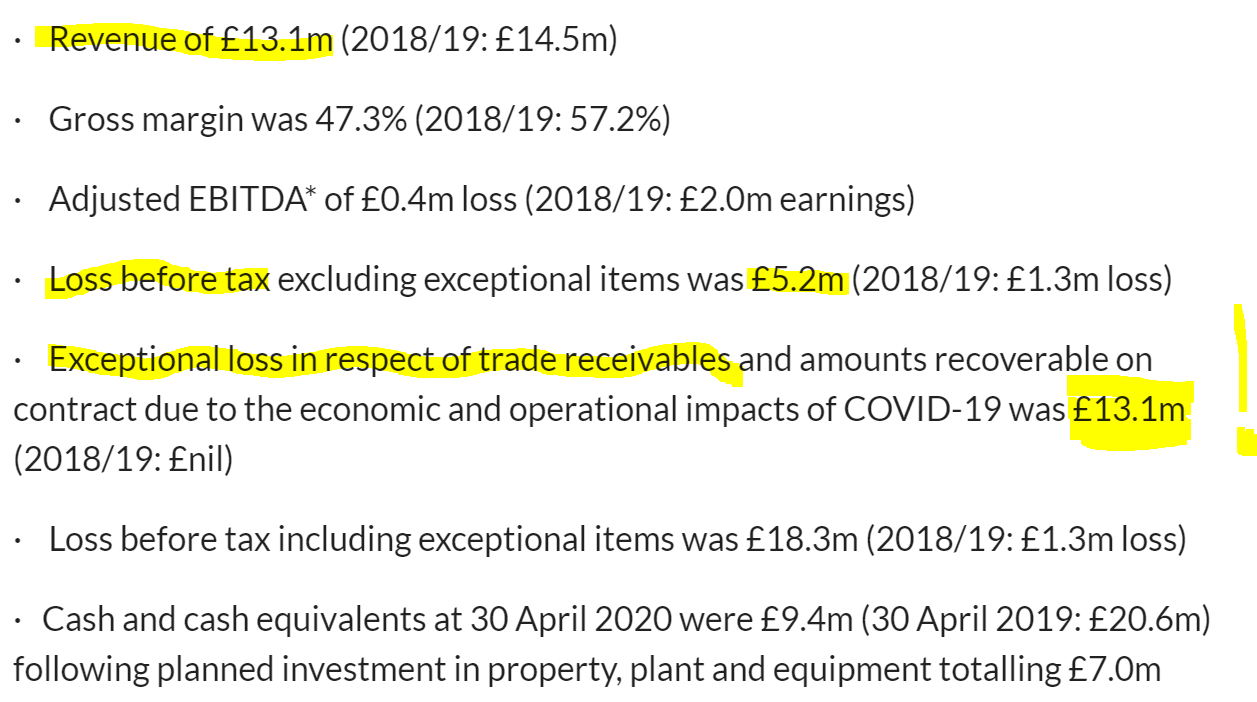

As you can see below, the standout item is a huge loss (an entire year's revenues) on receivables. This is absolutely horrendous;

.

.

Note that revenues of £13.1m seems to be 10% below the £14.5m estimate given in the year end trading update. The notes say that Kromek gave away a £0.7m discount, to secure early payment from a customer (clearly being desperate for cash, or something went wrong with the product/service maybe?).

Also the loss before tax of £5.2m is worse than the £4.6m estimate given on 1 May 2020.

Massive receivables write-off is the bigger issue. The commentary explains that uncertainty over whether its Chinese customer is going to pay up, has resulted in a full provision being made. I find this explanation unacceptable. It clearly shows a serious lack of financial control at Kromek. How on earth could it build up such a large exposure to one customer? A good CFO would surely have ensured that work only commenced, and continued, on receipt of stage payments, giving only a small bad debt risk at any time? Even if some or all of the money is eventually collected in, this shows an alarming lack of control. I suppose an optimist might say that, having made such a disastrous mistake, it shouldn't happen again.

Outlook- various encouraging details are given, but it also says that covid has continued to impact FY 04/2021. The conclusion says;

It is greatly encouraging that we are now starting to see a return to normal business patterns, and this is feeding through into increased activity from our customers around the world. As a result, the Board is cautiously optimistic for the year ahead and will provide updates to the market as the outlook becomes clearer moving forward."

Given the poor track record, how much reliance would I want to put on management comments? I'm not sure.

It has commenced deliveries on a particularly large contract;

The contract is expected to be worth a minimum of $58.1m over an approximately seven-year period.

That should underpin things somewhat, providing Kromek can work out how to actually get paid!

Going concern note - always worth scrutinising. Under its "revised base case" scenario, bank covenants would have been breached, but waivers have been secured to avert this.

In the severe but plausible stress test, the bank covenants would be breached from July 2021 onwards. This results in a material uncertainty over going concern - a serious warning to shareholders that this share is very high risk.

Balance sheet - I was expecting worse. NTAV is £21.9m, which should be OK if it can collect in the large receivables, and turn inventories into cash. There's £9.4m of cash, less £3.7m current borrowings, and £1.9m long-term borrowings, giving net cash of £3.8m - that looks tight, for a cash-burning business.

Liquidity - I'd say another equity fundraising looks a foregone conclusion. How much market appetite would there be for that? Probably some, because the company clearly has some good products, it just can't seem to sell enough of them, and the clock is ticking, with multi-year disappointments being racked up. At some point investors get sick of hearing the same people giving the same story about jam tomorrow which never materialises.

It seems capex hungry, with £7.0m spent in FY 04/2020, plus £5.3m of development spend capitalised.

My opinion - the products do sound interesting, but it looks too risky to me, and a serial disappointer.

The £13.1m receivables write-off is a massive disaster, which very seriously undermines the credibility of the company.

On balance I think I'll avoid this one, unless/until it has refinanced with fresh equity (again).

.

That's it for today, see you tomorrow!

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.