Good morning from Paul & Roland!

Govt energy measures

Press reports are saying that a huge series of support measures are in the pipeline from the Govt, to cap household energy bills at around the current level. Plus big support for business. All at a massive cost of somewhere between £100-170bn. People will have different views, but mine is strongly supportive (although we don't know the details yet).

The biggest driver of high, and rapidly rising inflation, is energy costs (per the Bank of England analysis I copied here recently). Therefore putting a hard cap on these energy costs is the most effective way to stop inflation in its tracks.

The knock-on effects of another winter of discontent, with the usual culprits going on strike demanding (say) 15-20% pay rises, should instead now be easier to deal with at a lower level, since inflation might even begin to fall in a few months' time, possibly. Instead pay rise deals might now be struck in a more palatable range of say 5-10%, and be one-offs, rather than getting into a hyperinflationary spiral, which would have happened if energy bills had been allowed to soar to say £6k per household. So it looks as if household concerns should greatly reduce, which should help restore some level of consumer confidence.

The next big question, is what happens for business? Clearly it's going to bankrupt many small businesses, if there is no relief for the huge increases in energy bills we're hearing about. Presumably something similar is in the pipeline, because I can't see that Govt would throw everything at households, but do nothing for businesses. They tend to favour small business though, so I hope the expected assistance will also filter up to our small caps sector of the market. We wait with baited breath, but so far anyway, the news seems exactly what I was hoping for - big, bold action, to stamp on inflation, and support households from what would have been, for many, completely impossible energy cost increases.

How will financial markets react to this huge increase in borrowing, which looks set to soar back to 10% of GDP p.a., or even above? (typically the peak level of annual spending deficits in recessions). Who knows? In any case, gilt yields can be tuned to anything the Govt wants, using QE - as we've seen since QE started in the 2008/9 crisis. So personally, I'm not worried about how this is all funded. In a crisis, we need bold, decisive action, not hand-wringing over how to pay for it. That was very much proven in both 2008, and 2020. The cost of inaction is worse than taking bold action. Other opinions are available of course, from other people, this is all quite subjective.

If you want to worry about another sovereign debt crisis, then I think Europe has far bigger problems to deal with, especially Italy - where debt to GDP is 150%, and the only buyer of Italian bonds has been the ECB, which is now holding an astonishing E700bn. How will that ever be repaid? That's their problem to worry about, but a re-run of serious problems over Euro looks a bigger problem than anything we have here, in my opinion.

All the above is clearly bullish for shares, as the worst case scenario of something akin to economic collapse is clearly now not going to happen. So we could see some buying interest in bombed out small caps now. Selectively, I think this might be a good point to put some cash to work. It reminds me a bit of a previous key tipping point, e.g. when the vaccines were announced, when disaster looks to be averted. That started a very strong recovery in many shares, that lasted about a year, starting in Oct 2020. We could be at a similar point now, where decisive action to tackle energy costs, transforms the economic outlook for the better. So dust down those buying lists, if you agree with me!

Agenda -

Paul's Section (brief comments first) -

Loopup (LON:LOOP) [no section below] - there’s an update on its deal with PGi Connect, which is to migrate its conferencing customers over the LoopUp, in return for a revenue share agreement. I might have missed something, but it doesn’t seem to have anything meaningfully new in it, the figures look the same as last time this deal was announced.

When small, cash-strapped companies start recycling the same positive news, it does arouse my suspicion as to why? The obvious thought is that they possibly want the share price up, to make another placing more do-able. To reiterate my thoughts on this share, it looks potentially interesting, but it’s uninvestable for me, until the cash position is sorted out with another placing - which needs to be big (relative to the market cap), to clear the £8m net debt, and provide the funding for continuing, heavy cash burn. So a speculative, but risky share, I’d say. I'm holding back until it sorts out the funding problem.

Paul - longer sections:

Halfords (LON:HFD) - a scheduled update for the first 20 weeks trading of FY 3/2023. This seems surprisingly resilient, with full year guidance reiterated. The shares have collapsed, along with the sector, over the last year. This looks a potential buying opportunity to me.

Headlam (LON:HEAD) - interims from yesterday are exactly in line with guidance provided in July. Self-help measures mean HEAD is trading OK, and it reiterates full year expectations. The balance sheet is superb, including loads of freehold property. Crucially it has more than passed on cost inflation on product, with a rise in gross margin. High dividends & dividend paying capacity. Short term uncertain due to macro factors, but long-term shareholders should be fine, I see 100% upside here longer term.

Roland's Section:

James Fisher And Sons (LON:FSJ) - this family-owned marine services group is going through tough times. Today’s half-year results appear to include (another) profit warning and a rather mixed trading outlook. However, I think the foundations are being put in place for a turnaround. I’d be interested to learn more here, as I think there are some attractive elements to this business.

Somero Enterprises (LON:SOM) (I hold) - another solid set of results from this US-focused concrete-levelling specialist. Somero reports record half-year revenue and a strong non-residential construction market in the US. Full-year guidance has been confirmed, with a caveat about supply chain disruption. I remain happy to hold.

Avon Protection (LON:AVON) - [no section below] - shares in this fallen high flyer are up by 18% as I write, after the company announced a $15.1m US defence contract to supply 380,000 M61 filters (gas masks). Deliveries are expected to begin in early FY23 (Avon has a 30 September year end).

Today’s release also includes a positive trading update. As guided in May, trading during the second half of the year has improved. Full-year results are now expected to be “at least in line with market expectations”, excluding the armour business, which is being wound down.

The company also says that it’s making good progress with the search for a new CEO, following the resignation of current boss Paul McDonald. He leaves at the end of September.

My view: looking ahead, I think Avon could offer some value. FY23 forecasts put the shares on 11 times forecast earnings, with a possible 5% dividend yield.

However, I think it’s worth noting that while the company left the interim dividend unchanged, it warned that the full-year dividend would not be determined until the end of the year.

Net debt has also mounted over the last couple of years. Leverage reached 2.6x EBITDA at the half-year point (31 March). Avon has covenant limits at 3x EBITDA, so I wouldn’t be completely surprised if the board uses the recent turmoil as an excuse to reset the dividend.

On balance, I’m encouraged by the outlook here. My feeling is that the worst is over and the group is now well-positioned to resume growth as a specialist defence supplier. However, I’m uncomfortable with Avon’s debt levels. For this reason, I’d be inclined to wait for the full-year results later this year before deciding whether to invest.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Halfords (LON:HFD)

133p - mkt cap £292m (pre market open)

This covers the 20 weeks to 19 August 2022, of FY 3/2023.

The summary looks encouraging -

Full year profit guidance unchanged following good performance across the business, and market share gains across Motoring and Cycling products and services.

This announcement looks a lot better than I feared it might have been. So this could be a good entry point for this share.

Key points (for 20 weeks) -

Revenues down -1.9% on a like-for-like (LFL) basis, against strong LY comparatives.

Total revenues up 9.2%, reflecting acquisitions.

LFL revenues well ahead of pre-pandemic (up 11.7%)

Autocentres are stand-out performer, up 28.2% vs pre-pandemic, suggesting that acquiring and rebranding autocentres is a good strategy.

Changing shape of the business - due to acquisitions, services are now 42% of revenues, as opposed to just 22% pre-pandemic. So it’s not just a retailer now.

Guidance for FY 3/2023 is unchanged at £65-75m (down from £90m LY) - this strikes me as pretty resilient, given the macro situation.

BUT the outlook section says this guidance assumes no further deterioration in macro & consumer confidence, which seems imprudent to me!

Loyalty club - has done well, with 500k members since launch.

70% of revenues are motoring, and tend to be needs based, i.e. essentials - makes the business resilient in a downturn.

Balance sheet - nothing said, but I’ve checked back, and it looks OK, with NTAV of about £110m.

My opinion - I’m be tempted to buy after this unexpectedly robust trading update.

Headlam (LON:HEAD)

282p - mkt cap £240m

Figures out yesterday, and triggered a bounce in the share price. This is one of my favourite value shares (no current position), so am keen to circle back to it, in order to decide whether to buy back in at some stage.

Headlam Group plc (LSE: HEAD), the leading floorcoverings distributor, today announces its interim results for the six months ended 30 June 2022 (the 'Period') and an update on current trading.

Company headlines -

Improved profitability despite economic backdrop

Pleasing progress in delivery on the strategy

The numbers today look familiar, and that’s because the H1 trading update told us what to expect - see my bullish commentary on it, here.

H1 revenues are £323.8m, exactly as previously guided, with UK down, and Europe up.

Underlying PBT is also exactly as guided for H1, at £17.3m (which is up slightly against H1 LY of £16.7m - impressive).

Pricing power - a key point here is that gross margin actually rose at 33.7% (from 32.7% H1 LY) - which indicates to me that HEAD has the ability to pass on higher product costs successfully to its customers - very important, and clearly a positive.

An insurance claim boosted reported H1 PBT to £21.6m - helpful, but I would ignore this for valuation purposes, as a one-off.

Net cash is healthy, at £6.0m, plus £74m of undrawn bank facilities, so HEAD remains superbly strong financially - this business could weather pretty much any storm I reckon.

Outlook - sounds a little cautious, albeit in line -

· Revenue performance year to date continuing to be only marginally below the prior year period

· Company remains on track to meet market expectations4 for the year, although trading remains challenging and operational cost inflation continues

4Company-compiled consensus market expectations for revenue and underlying profit before tax, on a mean basis, are available on the Company's website at www.headlam.com.

Balance sheet - is fantastic. It’s now almost £200m of NTAV - so the £240m market cap is largely supported by tangible assets, which is very unusual, and really positive. It’s the freeholds which provide about half of that NTAV, which I love. It means you don’t have to worry, and even if the business needs to borrow in a lean patch, the banks are happy to lend against freehold property, because it’s secured, hence close to zero risk from the bank’s point of view.

My opinion - remains very positive. I think this share could double in the long-term, once economic conditions are more normal, and it still wouldn’t be expensive even then.

Obviously in the short term, times are harder, but it’s still performing resiliently - that’s because there are a lot of self-help measures underway, in an extensive rationalisation of the business, which seems to be absorbing softer demand.

Why does a carpet distributor exist? For a very good reason - that the product is bulky, and with huge product ranges, it’s not possible for retailers to stock all the products they need. So it’s out-sourced to Headlam, which also gives Headlam better bulk buying power. Headlam then charges a reasonable mark-up, sensibly not too high to encourage competition or being sidelined by customers buying direct.

There’s always the risk of an H2 profit warning, if demand nosedives, but that shouldn’t matter to long-term shareholders.

Meanwhile, this share gives a nice divi yield, and seems to offer inflation protection too, since it has demonstrated that cost increases are being passed on to its customers. That's ideal in current circumstances, in my view.

A thumbs up from me!

Smashing value metrics -

.

Roland's Section:

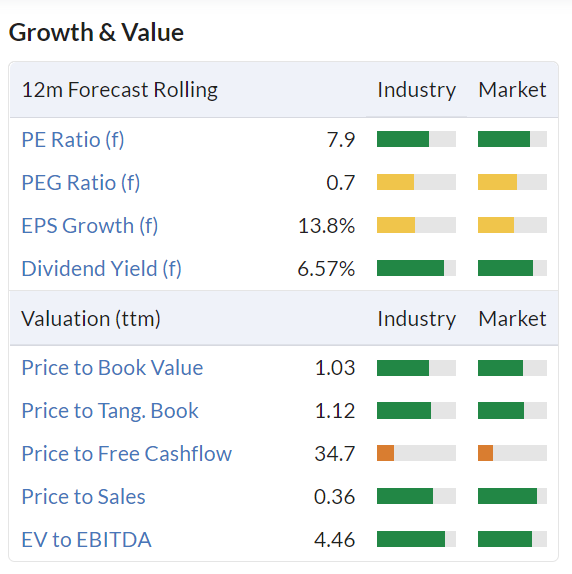

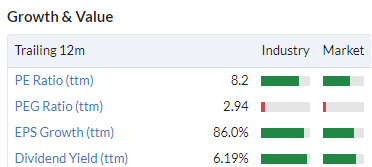

James Fisher And Sons (LON:FSJ)

280p (-9% at 08.10)

Market cap £142m

Long-term investors who’ve continued to back this family-controlled offshore services and engineering group have had their patience severely tested over the last three years.

Unfortunately, today’s half-year results appear to include a further (mild) profit warning. The shares are down nearly 10% in early trading.

Updated guidance: Today’s share price drop appears to have been triggered by guidance that “full-year operating underlying operating profit is now expected to be broadly in line with 2021”.

Checking back to last year, underlying operating profit was £28m.

There are no broker notes on Research Tree. The only forecasts I can find for FY22 operating profit suggest a figure of £29m. So today’s cut to guidance appears fairly mild, but unwelcome nevertheless.

Financial highlights: a recovery is not yet visible in the numbers. Fisher’s half-year results show continued decline compared to the same period last year:

- Revenue +2% to £238.4m

- Underlying pre-tax profit -47.8% to £4.8m

- Statutory pre-tax profit -60.5% to £3.2m

- Underlying earnings per share -48% to 6.7p

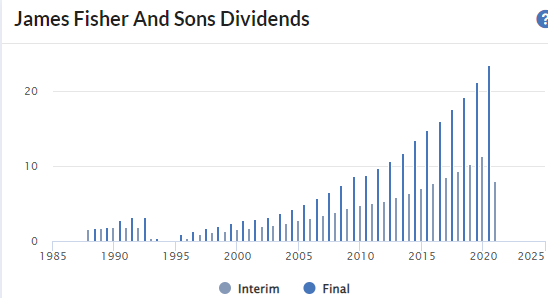

- Dividend suspended

- Net debt £172m (June 2021: £189m)

- Leverage: 2.9x EBITDA

Despite the suspension of the dividend, leverage does not seem to be falling very quickly.

As a side note, suspending the dividend after more than 20 years of unbroken growth is a tough blow, especially for a family firm. As Jack commented in March, it does suggest something has gone seriously wrong here.

Profitability: I’m always encouraged when companies report return on capital employed. Even if it’s poor, it shows that the board recognises the importance (in my view) of this profitability metric.

Fisher reports both operating margin and ROCE. Unfortunately the figures are poor:

Operational highlights: This group is made up of a number of operating companies, each with their own brands.

Trading during the first half was strong in the group’s offshore oil (well services) and tankships (ship chartering) businesses. Marine contracting (subsea services for offshore energy) is said to have continued to improve.

The weak spots seem to have been Fendercare – which supplies ship mooring products and ship-to-ship oil transfer services – and ‘Specialist Technical’. This includes diving, defence and nuclear decommissioning (an odd fit?).

Management warns that Specialist Technical projects are cyclical and budgets are under pressure. So I’m not sure about the near-term recovery prospects here.

Outlook: Fisher’s business does have some seasonal weighting and management expects the second half of the year “to be materially stronger than H1”. Seasonal cash flows should cut net debt and leverage by the year end. Further disposals are also a possibility.

However, with full-year profit now apparently expected to disappoint, the tone of the outlook is cautious.

The commentary in today’s results was provided by chairman Angus Cockburn, who was appointed last year. There was no comment from new CEO Jean Vernet, who only started work on 5 September.

Fisher normally issues a trading update in late October – perhaps we’ll hear from the new CEO then.

My view: There are a lot of moving parts in this situation and I’m not sure a turnaround will be quick or easy.

However, Fisher does seem to have some strong, specialist franchises. With a new CEO and chairman now on board, my hope is that historic issues can gradually be resolved.

The Fisher family continues to control 23% of FSJ stock, with fund house Schroders in second place, with around 10%. That suggests to me that Schroders (also family controlled) sees value in this business.

Broadly speaking, I see this as an interesting turnaround situation that could deliver attractive returns over time.

However, if I was thinking about investing, I’d want to do more research into the history of the group’s operating divisions and its record of acquisitions and disposals. This would hopefully help me to understand when things started to go wrong, and what the solution might be.

Definitely a DYOR situation – but with a 175-year history and family ownership, I think James Fisher is definitely worth further research.

Somero Enterprises (LON:SOM) (I hold)

406p (-6% at 08.45)

Market cap £229m

“Record H1 revenue translated efficiently to strong profits and operating cash flow”

Today’s interim results from this concrete floor-levelling specialist report record revenue and are in line with expectations for the full year. But that hasn’t stopped the share price falling this morning!

Trading commentary: Investors appear determined to price in a bearish outlook, and perhaps that’s appropriate at the moment.

But Somero says it’s seeing a “strong, active non-residential construction market” in the USA, together with encouraging growth in Australia and Latin America.

Financial highlights: Revenue hit record levels during the six months to 30 June, but there was some slight margin weakness, causing profits to slip slightly. This was attributed to cost inflation and increased headcount. Even so, today’s half-year figures look very respectable to me.

- Revenue +6% to $68.5m

- Pre-tax profit -5% to $22.4m

- Adjusted earnings -3% to $0.31per share

- Cash flow from operations -20% to $12.8m

- Net cash -17% to $27.2m

- Interim dividend +11% to $0.10 per share

Outlook: The momentum seen during the first half of the year is said to be carrying over into the second half. This is supported by a strong non-residential construction market in the US, with “extended customer project backlogs” and opportunities for international growth.

The board recognises the risk that supply chain shortages could “slow our ability to fulfil customer orders”. This could impact 2023 trading if unabated.

However, based on the strength of H1 trading, Somero feels able to confirm that 2022 results should be in line with market expectations. Helpfully, the company specifies what these are:

- Revenue: $138.8m

- EBITDA: $47.7m

- Year-end net cash of $39.9m

These numbers translate into some very attractive forecast valuation metrics:

My view: As a shareholder, I don’t see any reason to change my view on Somero following today’s results. Cyclical risks will always be a factor and I do expect a slowdown at some point. Succession is also a potential concern, as CEO John Cooney is in his mid-70s and chair Larry Horsch is nearly 90.

However, the balance sheet looks bulletproof to me and the company appears to be continuing to execute well. Somero shares don’t look expensive to me at current levels and offer an attractive yield. I remain happy to hold (and buy) this stock.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.