A factor portfolio is greater than the sum of its parts

Many investors believe that long-term share price returns are primarily the result of each company's individual performance. Therefore beating the market comes down to each individual investor's stock-picking ability. But this isn't always true.

Individual stocks do behave very idiosyncratically. If they release good or bad news at any time the share price can rise or fall accordingly. But when you own a portfolio of different shares the individual, news-driven performance of each share tends to cancel the others' out. What is left over is the portfolio's exposure to factors - which become the driver of portfolio returns.

Why stock picking matters less in a factor-driven portfolio

If you break down a share's price performance in the market, you can think of it as having a large component driven by its own company-specific return, and other components driven by the market's demand for its more general characteristics. For example, if value stocks are in demand, then shares on low P/E ratios will continue to be accumulated regardless of their unique news flow.

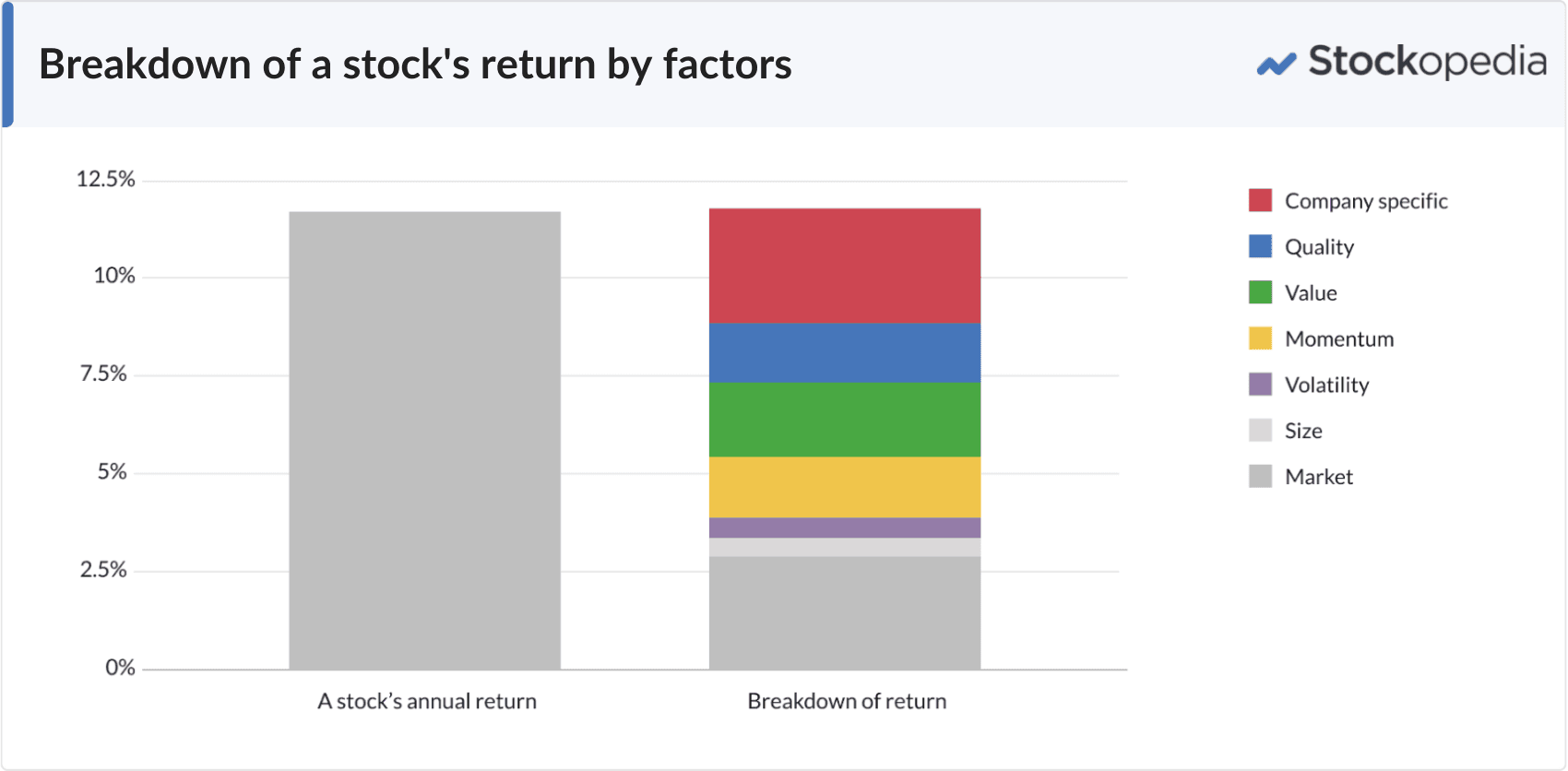

Each stock is influenced by these factors in varying degrees. Let's imagine a stock has returned 12% in a year, the breakdown might be something like shown below - with contributions from general market demand for factors like quality, value and so on. A rising tide for these factors lifts all boats that have those characteristics. The stock's unique, company-specific return, unexplained by those more general factors, is displayed in red.

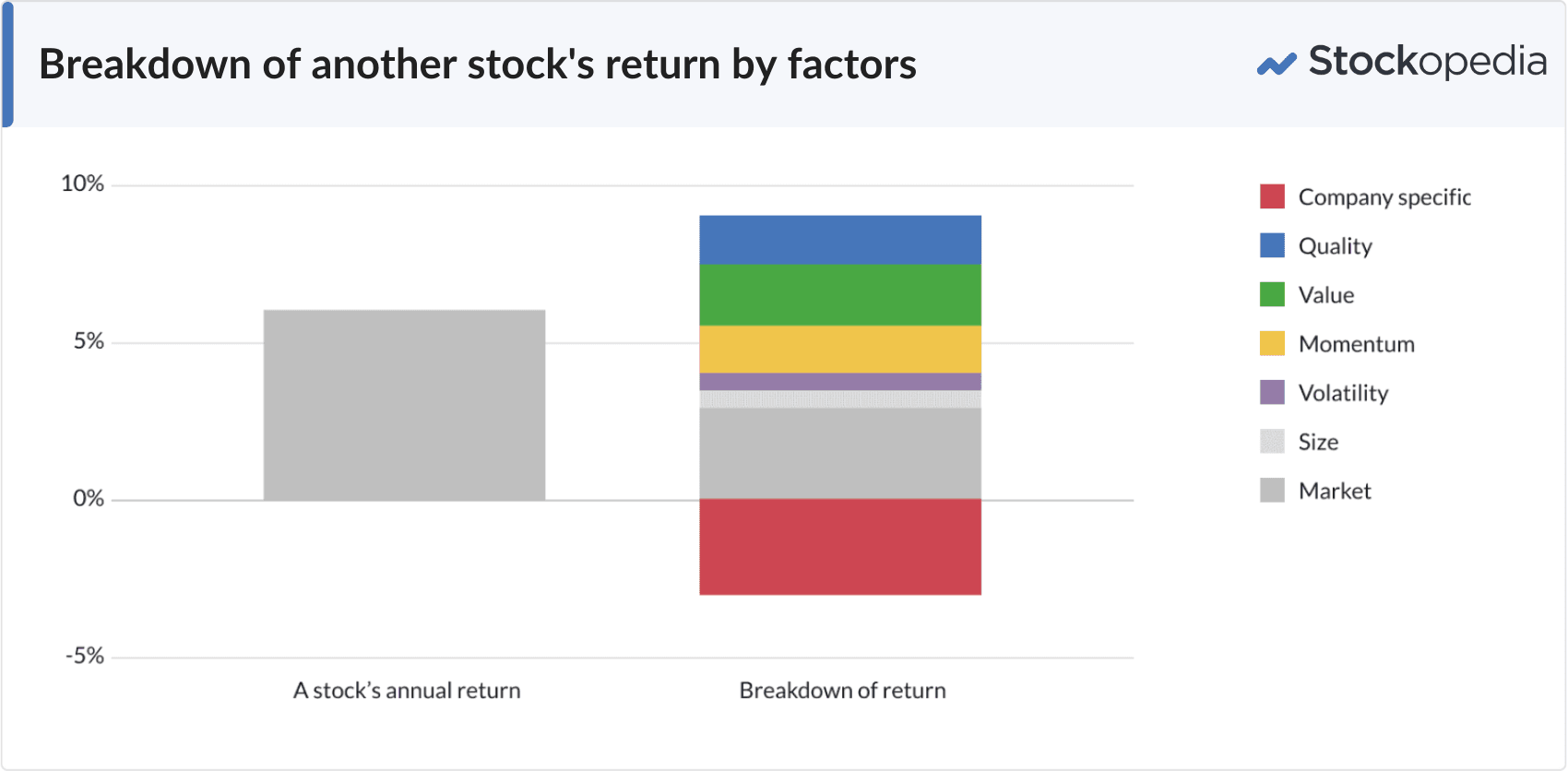

But as individual stocks are highly idiosyncratic the company specific return can be surprisingly random, news driven and unpredictable up or down. So a similar stock might look like this - with a negative company-specific (news driven) return - but with an overall positive return due to demand for some of its other traits.

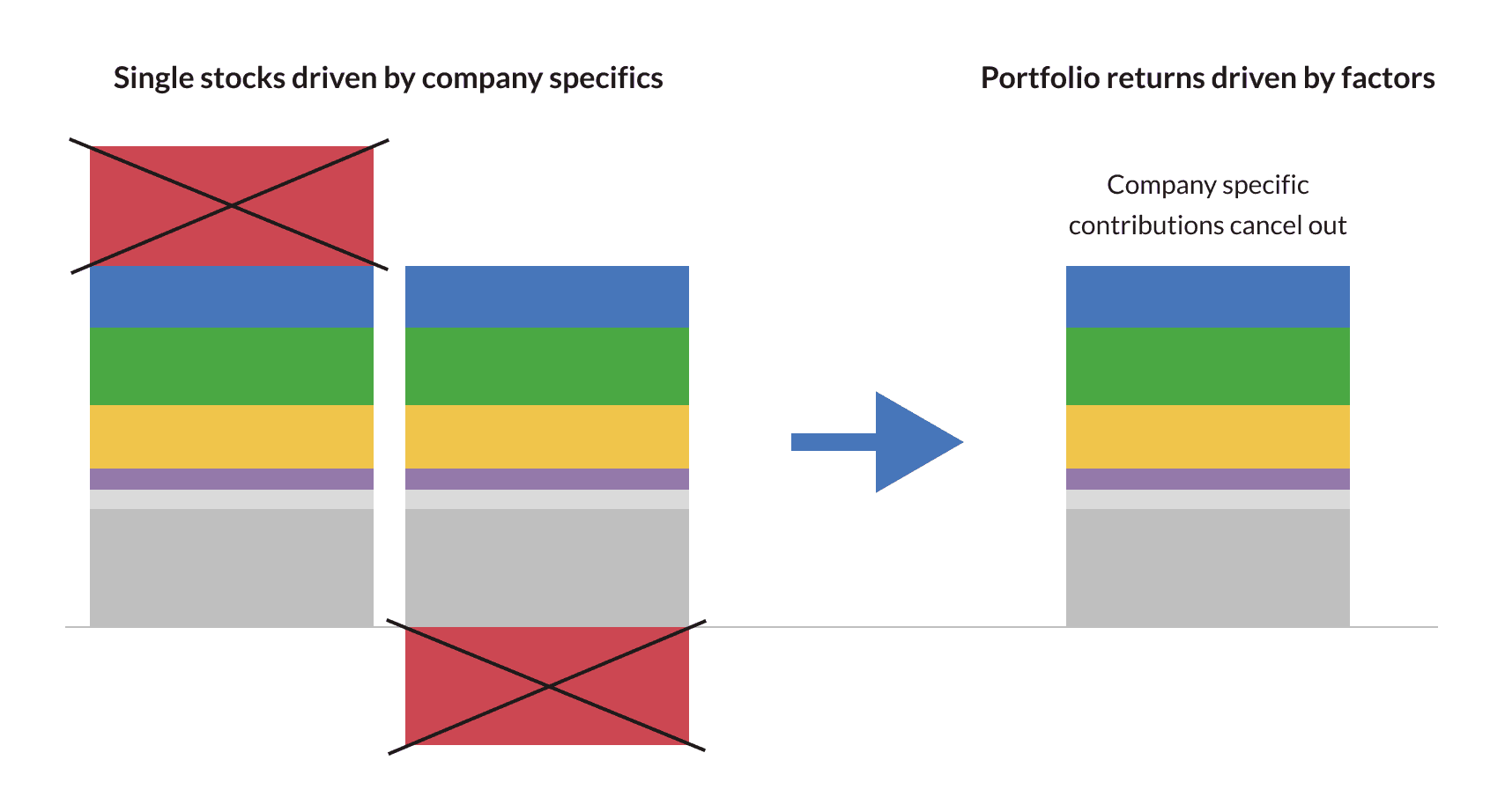

The fascinating thing is that as you add more and more stocks to a portfolio, these random company specific returns (in red) cancel each other out. In a large enough portfolio, all that you are left with is the factor returns. In technical jargon - the unsystematic risks of each individual company has been diversified away to be left with the systematic risks of factors. An idealised two-stock situation is illustrated below.

This is a key principle of factor theory and a truth that the fund management community is trying to come to terms with. Fund managers with big, diversified portfolios often really struggle to add any value with their stock picking - even though their entire operational and marketing strategies are designed around it.

They travel extensively all around the world to meet company management and build relationships to gather unique insights. They hire and train teams of expensive MBAs, CFAs and PhDs to pore over company accounts, build financial models and gather intelligence to predict the future. They spend hugely on industry research. But most of this effort is wasted due to the brutal arithmetic illuminated above. In large funds, the value generated from company specific insights is mostly diversified away.

Research does show that the handful of best conviction ideas of fund managers do outperform by up to 4.5% per year.[1] It's just that they are often forced, by their mandates, to own too many stocks to benefit from their best ideas. The organisation of the money management industry appears to make it optimal for managers to introduce stocks into their portfolio that are not outperformers.