In this chapter, we’ll share the hard research, maths and statistics that show how investing in dividend paying stocks has been a market beating strategy whatever the environment, with the added benefit of lowering portfolio volatility and risk. While there is ongoing disagreement about the exact level of contribution that dividends make to stock market returns, there’s one thing that can be agreed on - dividends, and their reinvestment, drive the majority of the returns that investors receive in the stock market, especially over the long-term.

The evidence is incontrovertible. The trouble is that finding it requires digging through volumes of generally rather dry and little known research notes on the subject written by obscure, ivory towered, academics and quants. This is not a task for the faint hearted at all and is one of the reasons you will find that your average journalist or stock broker has almost zero knowledge on the subject (while continuing to promote story stocks at readers or clients on a daily basis)!

But the legendary value investing firm of Tweedy Browne Inc has done investors a huge service. They have gathered and collated the results of many of the greatest studies into stock market re- turns offered by dividend paying stocks into a single paper titled The High Dividend Yield Return Advantage. Some of the startling conclusions taken from the research that it references and others that we have gathered include the following:

Dividends and dividend growth provide nearly 80 percent of stock returns

The esteemed Robert Arnott published a paper titled Dividends and the Three Dwarves in 2002 in which he analysed stock market returns over a 200 year period ending in 2002. He found that the total compound annual return for stocks over the period to be 7.9 percent per year. This broke down into a 5 percent return from dividends, a 0.8 percent return from real growth in dividends, a 1.4 percent return from inflation, and a 0.6 percent return from rising valuation levels. Essentially the return from dividends ‘dwarfed’ the return from all other sources – “dividends are the main source of the real return we expect from stocks”.

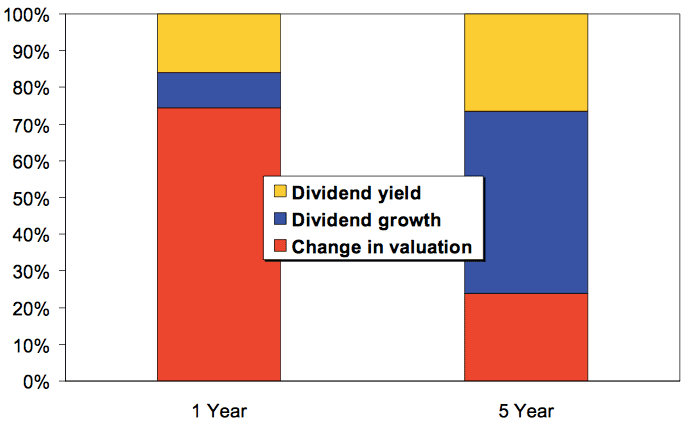

This finding has been verified more recently by another legendary strategist, James Montier. He showed in a 2010 paper (A man from a Different Time) that, while in the average single year period nearly 80 percent of the market return has been generated by changing valuations, on a five year timeframe dividend yield and dividend growth account for almost 80 percent of the return – the complete opposite! Now, if everybody in the market is chasing the speculative year to year return rather than the far more certain steady 5 year return, what should the smart investor do?

Dividend reinvestment strategies provide blistering compound gains

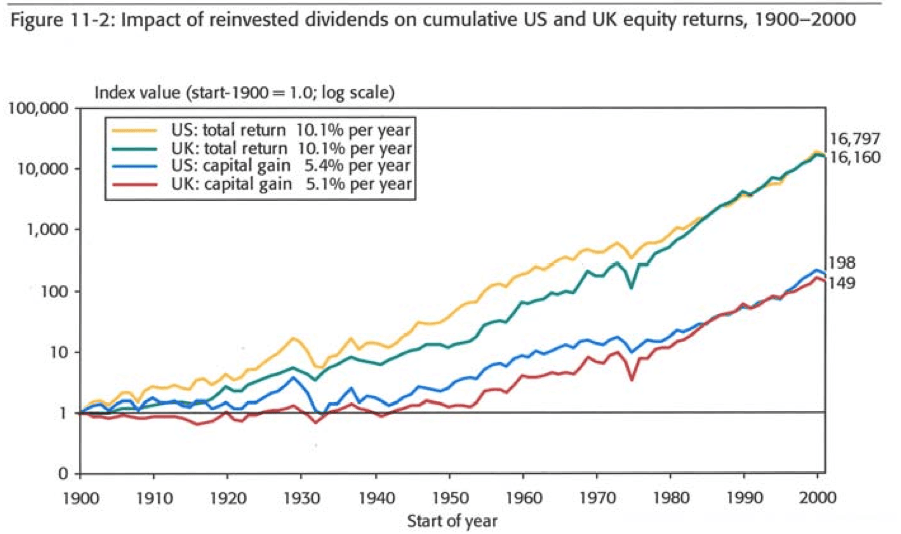

The dramatic effects of compounding gains - by pumping dividends back into the stocks from which they came - plays a pivotal role in dividend investment strategies. A 2002 book titled Triumph of the Optimists published by Princeton University Press showed that, over 100 years, an investment in the market portfolio with dividends reinvested would have produced 85 times the wealth generated by the same portfolio relying solely on capital gains.

Just as startling are the findings in the annual Barclays Equity Gilt Study. £100 invested into stocks at the end of World War II would have been worth just £5,721 at the end of 2008 in nominal terms, but by reinvesting the dividends the same £100 would have grown to £92,460 – an astonishing 16 times the value!

Now granted, those not reinvesting dividends would have been en- joying extra disposable income during those years, but nonethe- less the cumulative impact of this strategy illustrates the awesome power of compounding available through dividend reinvestment.

High dividend yield strategies trounce the market… all over the world

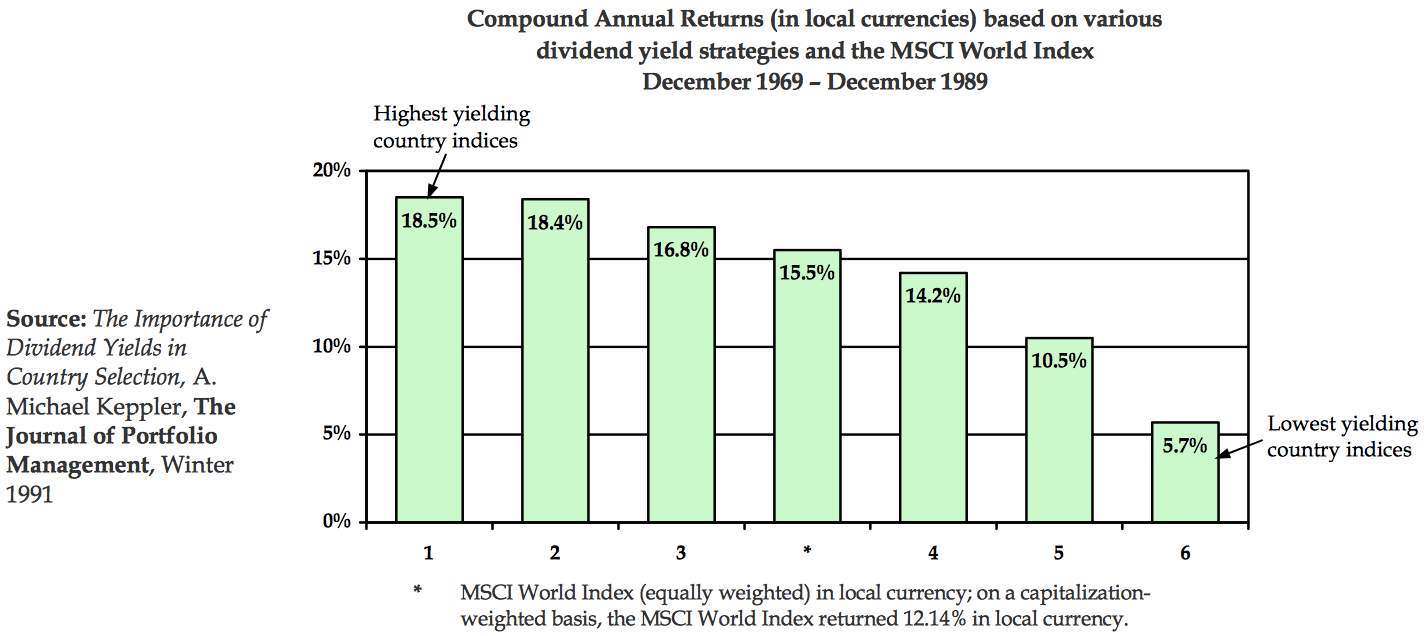

While much dividend research is biased towards US stocks, the results are magnified in the few studies into international stocks. Michael Keppler in 1991 set up a test to compare investing in high dividend yield stocks compared with low dividend yield stocks ranked in deciles across an equal weighted portfolio of 18 international indexes. The results were astonishing. The highest yielding portfolio returning 18.5 percent annually, compared with only 5.7 percent for the lowest yielding portfolio. And these weren’t emerging market indexes – all were developed world portfolios.

These results will not be surprising to readers who have read our book How to Make Money in Value Stocks. The Dividend Yield is a classic value ratio and the ‘value premium’ earned by investors in the higher yielding portfolios is paralleled in low Price to Earnings and Price to Book portfolios. Again there are many other studies into high yield effects that back up these claims by commentators the world over including Jeremy Siegel in The Future for Investors, and David Dreman in Contrarian Investment Strategies.

Dividend stocks provide 90 percent of the market return in bear markets

We shall dedicate an entire chapter to this topic shortly but the point needs to be highlighted here too. The twin bear markets since the dotcom bubble have laid waste to the portfolios of many investors that put their money into the speculative corners of the market. In bear markets, the dips from peak to trough can be vicious as the market averages fall at least 20 percent, but of all the segments of the market, it’s high dividend stocks that perform most robustly in such an environment.

In a study from 1970 to 1996 titled When The Bear Growls: Bear Market Returns, David Dreman calculated the average performance of different segments of stocks in all the down quarters and compared them with the overall market. It was high yielding stocks (low price/dividend) that fared best, only declining half as much as the overall market. In fact, more generally, Vitaly Katsenelsen discovered in Active Value Investing that through ‘sideways’ markets dividend stocks actually account for up to 90 percent of the returns on offer from the stock market. In the light of that, it’s worth asking who would want to invest in anything else during those times?

Dividend stocks are a great inflation hedge

Fixed income streams – such as the interest you receive from a corporate or government bond – can suffer greatly during times of higher inflation. The reason is simply that the coupon received and principal returned is fixed and can’t grow as the inflation rate grows. Studies into equities have proven that the dividends paid by higher quality stocks do grow with inflation and sometimes even outpace it. Companies are often able to pass on their higher input costs to their customers allowing greater flexibility in raising dividend payments and greater potential for capital growth. The chart below from Societe Generale’s research team shows how the dividend growth rate has tracked the inflation rate over many years.

There are plenty who believe that global money printing can only lead to higher inflation in the years ahead. While all assets may suffer in such a scenario, high quality dividend paying stocks may provide some of the best protection.

Dividend stocks are stronger and less volatile

Companies that pay dividends have committed themselves to a higher level of financial discipline and capital allocation. These companies have made a public display of confidence in their own long term health. Indeed, the risk that cutting a dividend will upset shareholders means most dividend policies are pitched conservatively: you can fudge earnings but you can’t distribute cash returns to your shareholders if you don’t have the money.

Dividend paying stocks also tend to have less volatile share prices for two reasons. Firstly, many ‘lottery ticket’ seeking investors ignore dividend paying stocks as they see them as mature and unexciting businesses, but secondly the passive income stream dividend stocks offer provides some insurance and stability when share prices fall. It’s no surprise to find that dividend stocks can often offer some of the highest returns at the lowest risk in the market as a result - a very attractive pairing for mature investors.

But it’s not all rosy…

While we have certainly painted a rosy picture of dividend returns in this chapter, there are a great number of mistakes that investors make in attempting to replicate these results. The biggest reasons why investors fail come down to their own risk and portfolio management mistakes, most notably overtrading, failing to diversify effectively, failing to use tax efficient accounts, and failing to reinvest dividends. We shall cover these issues in far more detail in the latter half of Part 3.