While factoring dividend safety into high yield strategies is clearly a smart move in terms of improving returns, another school of thought favours a focus on dividend growth. Rather than prioritising the highest yield plays, Dividend Growth Investors aim to select stocks that may offer a lower initial yield but have a history of growing that payout over time. The emphasis here tends to be less on the absolute rate of compound dividend growth over time and more on the number of consecutive years of dividend increases - known as a dividend growth streak.

Why the Dividend Growth Streak matters

As we’ve discussed, companies with growing dividends are signalling confidence about their future earnings. They tend to be stable businesses, which are well positioned in their industries and are able to perform throughout market cycles. More specifically, a steadily growing dividend streak is an important signal for the following reasons:

It provides a rich seam of information about the stability of company management, the corporate culture and whether the dividend is important to the company even in times of financial stress.

It maximizes the potential for dividend reinvestment.

It is an indicator of management confidence in cash flow.

It provides protection against the dreaded effects of inflation.

In a 1985 paper entitled A Survey of Management Views on Divi- dend Policy, US academics Baker, Farrelly and Edelman found that management were ‘highly concerned with dividend continuity’ and felt that dividend policy affected share value. The findings tallied with the seminal 1950s paper by Lintner we discussed previously which outlined a behavioural model whereby managers typically ‘smoothed’ dividend increases over time and only made upward changes when they were sure that earnings could support the increase.

In other words, companies think very carefully before implementing and then increasing dividends, so this is an important sign to inves- tors in search of dividend longevity, reliability and growth.

The past can be a signal…

Of course, investors are routinely drilled on the risks of extrapolating too much from the past when trying to predict the future performance of a stock – but when it comes to dividends, the past can be a useful guide. Ned Davis Research discovered that over the past 40 years stocks in the S&P 500 index that had increased their dividend payouts annually averaged a 9.4 percent annualised return, whereas companies that paid a dividend but didn’t increase that payout had an annualized return of about 7 percent.

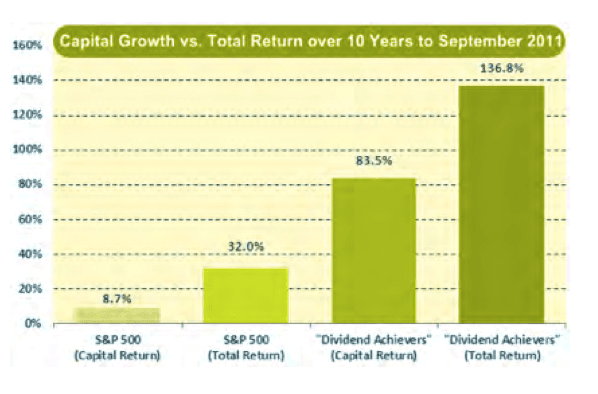

Similarly, the following M&G Investments chart shows the total cumulative return from the S&P 500 Index in the ten years to 2011, including the reinvestment of dividends, as 32 percent. However, if you put cash solely into US companies that grew their dividends for at least 25 consecutive years, the total return was over 136 percent.

As a result of this evidence, a long term dividend growth streak has earned a reputation as a yardstick for effective dividend investing and resulted in big name index providers like the S&P and Moody’s closely tracking companies which boast them. As ex-Fidelity fund manager and investing legend Peter Lynch wrote in his 1994 book Beating the Street:

“The dividend is such an important factor in the success of many stocks that you could hardly go wrong by making an entire portfolio of companies that have raised their dividends for 10 to 20 years in a row. Moody’s Handbook of Dividend Achievers – one of my favorite bedside thrillers – lists such companies.”

The importance of compounding & Rule 72

The related reason to focus on dividend streaks is that the wonders of dividend growth and reinvestment can have some remarkable effects over the long term. A friend once remarked that the dividends he received from his investment in the shares of the UK pawnbroker Albermarle & Bond were now worth more than his entire initial investment. That is a classic example of the real power at the heart of any form of stock market success and something that Warren Buffett has called the “eighth wonder of the world” - the power of compound growth. At a 15 percent growth rate your annual return will be greater than your initial stake in the 16th year.

Investors have an affection for calculating how long it will take to double the value of their investments – and this can be done very easily with dividend growth stocks. Using what’s known in finance circles as Rule 72, you can get an instant fix on how many years it will take a dividend stock to double. In simple terms here’s how it works. If you invest £1,000 in a stock with growth of 6 percent per year, the Rule 72 calculation would involve dividing 72 by 6 ⇒ 12 years. That’s roughly 12 years for the investment to be worth £2,000.

We will look more closely at a few dividend growth strategies in the next section, however, it’s important to note that assessing the future dividend growth prospects of a company should not just be a mechanical exercise based on the company’s historical track record. It also involves focusing on a company’s ability to sustainably increase its cash flow – which requires hard graft and diligence to understand the quality of the underlying business franchise.

Opposing pillars? The trade off between growth and yield

Of course, it would be ideal to combine a very high yield with a long dividend growth streak. Unfortunately, those kinds of opportunities don’t come around very often. So – if given the choice - how should an investor decide between, say, a stock with a 2 percent yield increasing at 10 percent a year, versus a stock with a 6 percent yield increasing at only 5 percent a year. Which is better?

The answer rather depends on your timeframe. Given a long enough time horizon, the dividend growth will compound out to make up for the shortfall in initial yield. However, many folks that plan on retiring may not have the time to wait for a dividend growth stock to make its original 2 percent dividend yield high enough to live off. A general rule of thumb sometimes used is that, if your time horizon is less than twenty years, a higher beginning yield is likely to be more important, but if it’s twenty plus, higher growth tends to win out.

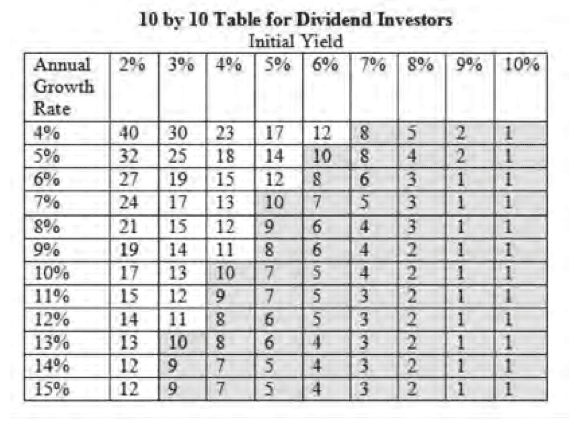

To better understand the relative trade-off between growth and yield, David van Trapp of Serious Stocks has developed a useful table (above) which looks at the number of years that would be required to achieve a 10 percent return on your investment. Across the X axis, the table has Initial Yield and down the Y axis, it has the Annual Growth rate. The values in the table are the numbers of years of compounding required to achieve the target return. The 10 percent targeted return is an arbitrary number but it is used on the basis that it’s a healthy return, almost equal to the long-term total return of the stock market.

If we take the scenario discussed above, the table suggests that a 2 percent yield compounding at 10 percent a year would take 17 years to reach a 10 percent return on investment. By comparison, a 6 percent yield increasing at 5 percent a year would take just 12 years.

As Van Knapp notes: “An additional 1 percent in initial yield reduces by 2 percent to 4 percent the growth rate needed to reach 10 percent yield on cost in a given time”. He argues that this is important since, the faster you hit your targeted yield on cost, the fewer years you are subject to the risk that you have overestimated its rate of dividend growth. This analysis suggests that it simply isn’t worth chasing stocks with yields as low as 1-1.5 percent, however fast they are growing. It will just take too long to get to the targeted return. Admittedly this analysis doesn’t factor in the impact of reinvesting dividends and it ignores the rising share prices that are often associated with growing dividends. Still, one of the key conclusions from this table is that, percent-for-percent, the initial yield carries more weight than the dividend growth rate.