The tech and trading boom of the last 30 years or so has created a breed of investors who disparagingly refer to dividend paying stocks as being for retirees, widows and orphans and who see the payment of a dividend as a sure sign that a company has gone ‘ex growth’. Meanwhile press and broker commentary fuel these atti- tudes by focusing on hope stocks, hole-in-ones and moon-shots. These attitudes are completely misguided. While the bull market years of the 1980s and 1990s certainly rewarded the average mar- ket speculator handsomely, the real winners in the bear markets of the last dozen years have been those that have rediscovered the art of dividend stocks.

A rough guide to surviving market cycles

To understand why dividend stocks perform so well in bear markets, it is worth exploring what actually happens to equity valuations within them. In an excellent book called Little Book of Sideways Markets[1], Vitaliy Katsenelson provides a mental model to help investors think about what drives the market over the long term. In essence, he illustrates with great effect how stock markets have a tendency to move in long valuation cycles from extreme overvaluation to extreme undervaluation.

He begins by making the important distinction between cyclical movements in the market, which last from several months to several years, and secular movements, which last from five to 15 years. These cyclical bull and bear moves may be the prime focus of the media, but really they are just shorter-term waves within broader secular tides that take the market from high valuations (in terms of P/E ratio) to low valuations and back again.

Katsenelsen notes that these secular trends have tended to be what he categorises as either long term bull markets or long term ‘sideways’ markets. The last 100 years have seen four main bull markets, four sideways markets (each lasting 13 to 18 years) and one short secular bear market in the Great Depression. Clearly, our current predicament is a sideways market with a long way still to run.

How and why the P/E ratio drives these cycles: A simple equation to understand stock market return is as follows:

Return = Earnings Growth + Change in P/E + Yield

Historically during bull and sideways market periods the level of earnings growth and dividends haven’t been much different – so the prime reason for the long drift upwards or sideways in price has been a result of the P/E multiple expanding and contracting.

If you look at the historic series of peaks and troughs in P/E ratios, it sets quite a sobering scene. The P/E lows (based on trailing 10 year average EPS) that were reached at the beginning of each bull market in the last 100 years have been 11x, 7x, 13x and 12x, but during the long bull market from 1982 to 2000 the P/E ratio of the S&P 500 expanded enormously to hit 48x earnings! At peaks such as this there’s only one way for the P/E ratio to go – down – and history shows it can take anywhere from one to several decades to bottom.

Dividend stocks – the only bear market winners?

Katsenelsen isn’t entirely pessimistic about the outlook for stocks in such an environment. He illustrates that between 1900 and 2000 the average annual return from the S&P 500 was 10.4 percent, out of which 5.5 percent could be explained by dividends. But these returns were extremely lumpy depending on whether the prevailing environment was a secular bear or a secular bull. He discovered that in secular bull markets dividends accounted for only 19 percent of annual average stock market returns (the rest coming from capital growth), whereas in sideways markets they accounted for 90 percent of the returns.

In fact, many studies of equity markets since 2000 have confirmed that dividend strategies have massively outperformed. Research by Societe Generale has shown that the high quality, high yield segment of the market has more than doubled since 2000 versus mar- ket indexes that have stayed completely flat. Clearly understanding the dynamics of bear markets and which stocks perform within them can have a massive impact on your overall portfolio performance.

These are wake up numbers for the typical equity investor who chases the annual ups and downs in the stock market with the worst timing – buying when markets rise and selling when they fall. The truth is that investors need to start learning to act contrary to their instincts to take advantage of market declines. Not only can dividend stocks provide extra return in lean times, but, as we shall see in the next section, reinvesting those dividends back into the market during market breaks can actually be hugely beneficial in the long run as prices recover.

How to recoup bear market losses dramatically faster through reinvestment

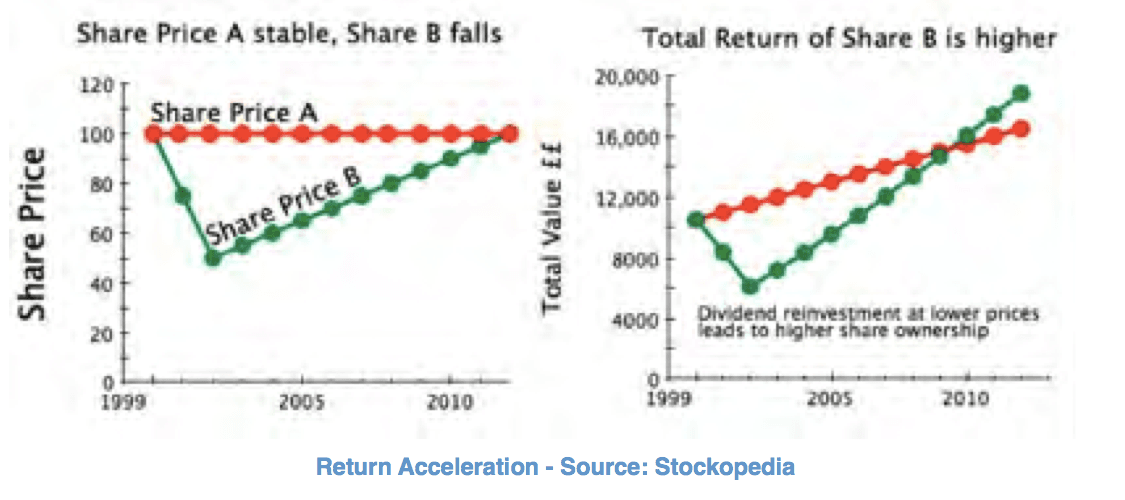

In The Future for Investors, Dr Jeremy Siegel[2], a finance professor at Wharton, shows the extraordinary impact that dividend reinvestment can have on equity portfolios when bear markets recover. Siegel explains that there are two ways that dividends help your portfolio in bear markets. Firstly, the greater number of shares accumulated through reinvesting dividends can help ‘cushion’ the fall in value of the portfolio in a bear market, but also “those extra shares will greatly enhance future returns. So in addition to being a bear market protector, reinvesting dividends turns into a ‘return accelerator’ once stock prices turn up.”

The maths of how this ‘return acceleration’ works are very simple but quite enlightening. Imagine two companies that both pay a stable 5p dividend over a dozen years. Share A holds a steady price at £1, whereas Share B declines over the first two years to 50p before recovering to parity 10 years later. The very counter-intuitive result of such a price decline on total returns to shareholders in B is that they end up wealthier. The greater number of shares that can be bought at cheaper prices with the consistent 5p cash dividend results in the shareholder owning a larger stake of Share B which ultimately ends up being worth more. It may well be that long term dividend investors really ought to welcome bear markets instead of loathing them!