Contrarian Quality: A stock market strategy for the shrewd

In investing, as in life, there are two types of bargain hunters.

In one camp are the bargain hunters who simply like to buy things as cheap as possible. A package holiday with all inclusive food and drink, for example. A shopping spree in Primark or a trip down the middle aisle at Aldi. In investing, we like to call this approach Deep Value - stocks that are picked purely for their cheap valuation multiples.

On the other side of coin are the bargain hunters who like to look for discounts on quality goods. The holiday maker who searches for 5* hotels on last minute websites, for example. And the shoppers who like to peruse branded outlet stores or wait for the yellow stickers to be placed on M&S food which is soon to go out of date. In investing, these discount hunters are known as Contrarians - they pick high quality stocks which, for one reason or another, are currently being overlooked by the market and are trading on attractive valuations.

In the latest in our series on investment strategies, we’re going to be taking a closer look at this investment style. Read on and you’ll learn:

How you can use market mis-pricing to make money

Whether you have the right mindset and investment goals to be an effective contrarian

How to implement this strategy successfully

Why does market mis-pricing happen and how can it make you money?

Weathered investors know the whims of Mr Market (or, as one astute reader pointed out to us last week, The Market is probably a more appropriate personification of the stock market in this day and age, after all, women can be investors too!)

The whims of the The Market are caused by the very human behaviours which influence share prices: panic, ecstasy, an absolute belief in being correct, a fear of missing out. The list could go on.

But while these behaviours cause stock market valuations to change very quickly, the underlying intrinsic value of the companies listed on the stock market tend to change slowly. Many famous and incredibly successful investors point to this discrepancy as the ultimate strategy for making money from the stock market: buy high quality shares that are trading at a discount to the underlying price of the asset.

Do you have the stomach to be a contrarian?

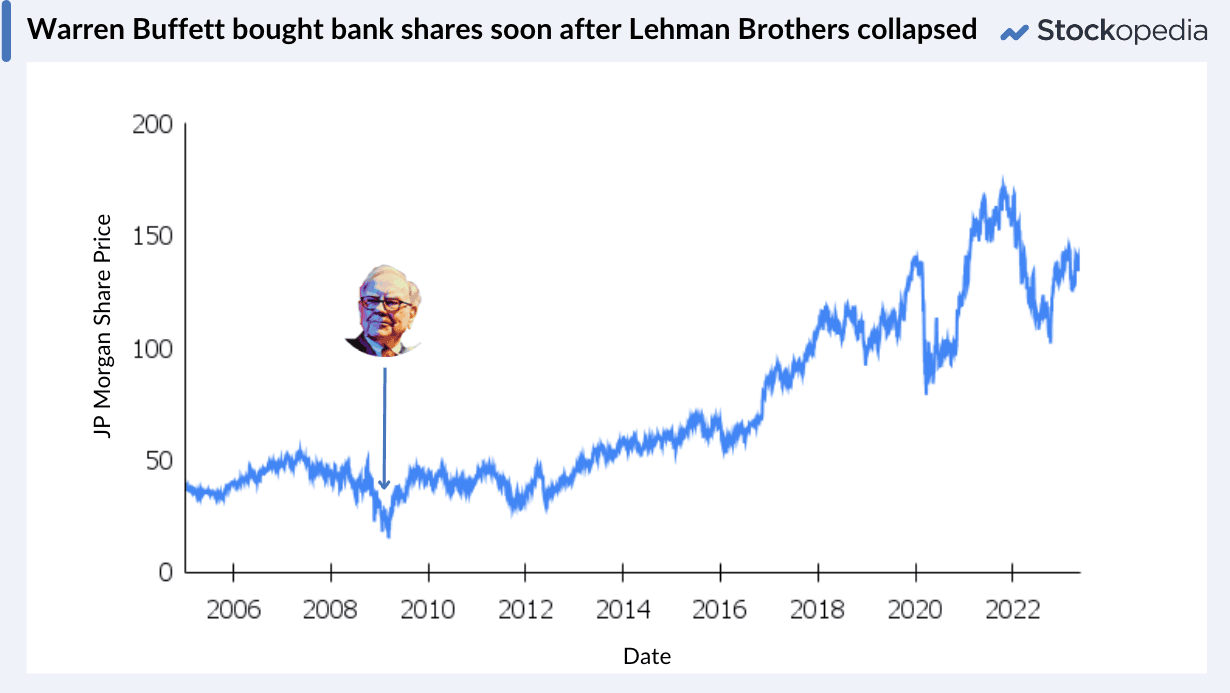

Contrarian stocks have made some investors incredibly wealthy. Like Warren Buffett, who bought shares in JP Morgan at the peak of the 2008 financial crisis, soon after Lehman Brothers went bust.

And hopefully me, when I bought shares in The Walt Disney Corporation immediately after the company’s disastrous earnings call at the end of 2022 (time will tell if that was a Buffett-esque manoeuvre or a woefully bad investment decision!)

But picking high-quality stocks when the market has fallen out of love with them is not easy (as my Walt Disney investment might soon attest). Investors who pursue a contrarian investment style need to have confidence in their ability to identify value discrepancies. Those that don’t could easily fall into one of the contrarian investing pitfalls listed below:

Freaking out

“The real key to making money in stocks is not to get scared out of them” Peter Lynch

The first pitfall, as renowned contrarian investor Peter Lynch says, is not getting scared out of stocks if they don’t immediately generate a return. Some companies can take a long time to recover from whatever caused their share price decline (and investors can take even longer to forgive them). But this is unfortunately a tricky tightrope to walk because if you are wrong and your contrarian stock selection was not, in fact contrarian at all, you might end up with a major loss.

Falling for a value trap

“You must never delude yourself into thinking that you’re investing when you’re speculating” Ben Graham

Which leads us onto our second pitfall. Investors who get attracted by good valuations might fail to properly analyse a company’s quality. A purely value stock without the quality metrics to support it might be a deep value stock - genuinely underpriced, despite weak fundamentals - but it might be a value trap. Getting it wrong could be costly.

Getting attached

The opposite problem is a psychological one - getting attached to stocks and failing to pick the right time to sell. Unlike compounding quality, contrarian stocks aren’t designed to be bought and held forever - they generate returns for their holders because they are momentarily mis-priced. But once they have recovered, investors shouldn’t be afraid to sell and look out for new opportunities. Attachment bias can leave investors hanging on for too long and watching the returns that have been generated, fall back again.

With all this in mind, we can sum up the contrarian mindset as:

Controversial - suited to investors who aren’t afraid to go against the status quo.

Opportunistic - for investors who have the mindset and ability to capitalise on short-term share price fluctuations. These investors might have a watchlist of stocks with price targets and a subset of their portfolio in cash ready to invest as opportunities arise.

Shrewd - suited to investors who can dissociate the underlying investment case from the popular narrative and have an ability to identify whether stocks are under or overvalued.

How to identify contrarian stocks

1. Financial metrics

Contrarian stocks score high on both quality and value metrics and many discretionary and experienced investors will have a favourite metric for both. Some say quality companies are those with consistently high profit margins, while others look for reliable cash conversion. On the value front, some investors favour the price to earnings ratio (which compares a company’s share price to its profit per share) while others like to use the enterprise value to sales ratio (which compares the market capitalisation of a company including its debt to the revenue generated).

By using the screening tools and StockReports of companies in your watchlist, you can look at any number of quality and valuation metrics on Stockopedia. But to keep things simple here, I am going to run you through my (and Joel Greenblatt’s) favourite metrics for identifying quality and value: ROCE and earnings yield (respectively).

ROCE (or return on capital employed) is a measure of the profits a company can squeeze out of its investment. Let’s say the company in question is a retailer which spends £1m on opening a new shop. The following year that shop generated £250,000 of profits. That’s a healthy return on capital of 25% (£250k divided by £1m). But let’s say its rival spends the same amount on a new shop but makes just £10,000, or a return on capital of 1% - not good enough.

ROCE is calculated by taking a company’s operating profit (from the income statement) and dividing it by total assets minus current liabilities (from the balance sheet). Ideally investors should look for a long-term average ROCE of 15%.

Earnings yield is a measure of the returns you might be expected to make on share, compared to how much you paid for it. Let’s say you bought shares in the retailer for £10 and the following year the company generated earnings per share of 75p - that’s an earnings yield of 7.5% (75p divided by £10). But let’s say the rival (the one which generated a ROCE of just 1%) only generated 2p of earnings per share. If you’d paid £10 for each share you’d be looking at an earnings yield of just 0.2% - hardly worth it.

There are a few ways of calculating a stock’s earnings yield (as companies report different profit metrics), but at Stockopedia we divide the operating profits (or EBIT) by the enterprise value (market capitalisation plus debt).

It is quite tough to compare earnings yield for companies in different sectors - some (like those in the tech sector) lend justify lower yields because of the higher growth that investors can expect. A general rule of thumb is that investors should seek companies with an earnings yield which is at least as high as current bond yields.

2. Alternative contrarian signals

In addition to financial analysis, some investors like to use contrarian signals from beyond the market to determine whether there might be buying opportunities. My favourite is the magazine cover indicator.

The magazine cover indicator suggests that by the time an editor promotes a bad news story to the cover of their magazine, the story has already been around for some time and that bad news has already been baked into market sentiment.

The phenomenon was first spotted in 1979 when Business Week ran a cover called the ‘Death of Equities’ - just a few years later, the major bull run of the 1980s really got going. The same applied to The Economist’s cover story ‘Drowning in Oil’ in 1999, which claimed peak prices for the oil market mere months before the surge in the price of the commodity. So strong was the pull of the magazine cover indicator that in 2016, a group of analysts looked at 44 Economist covers printed between 1998 and 2016 and found that after 360 days, 68% of those covers were indeed contrarian indicators and that buying an asset which is the basis of an especially bearish cover generated an 18% return over the following year.

There are, of course, many reasons to doubt this analysis. The Economist itself ran a counter piece to the research which claimed that the content in many of the titles which the analysts had claimed to be bullish or bearish was in fact not so and the covers were provocative simply because journalists like to be provocative.

Still, for investors who like to go against the grain, the magazine cover indicator is an interesting piece of additional research.

Implementing a contrarian strategy

There are many ways to be a successful contrarian investor. Some employ a bottom-up strategy - scouring the market for companies whose valuations are seemingly mis-priced. Others look for sectors which have fallen out of favour and pick stocks from a sector-specific shortlist.

At Stockopedia we favour the use of systematic strategies driven by factor data. This investment process has generated remarkably successful results, as a dive into the literature will attest. We recommend grabbing a copy of Joel Greenblatt’s ‘The Little Book that Beats the Market’ - very few investors who have perused this (very readable) tome have been left in any doubt of the potential of a systematic strategy that combines both Quality and Value.

Indeed, the thinking behind these gurus (and others) has powered our own factor-driven StockRanks, which have outperformed the market since their inception.

Here is our step-by-step guide to contrarian investing:

Define your timeframe and investment goals. The length of time you plan to be invested for and your personal financial goals will impact the type of stocks you buy. As a contrarian investor, you shouldn’t be under pressure to spend your investment savings within five years.

Assess your tolerance to risk. The risk level for contrarian stocks varies. Decide what level of risk you are comfortable with and use this to set your definitions for size and volatility metrics. If you’re uncomfortable with too much risk, you’ll probably want to remove any tiny companies.

Build a screen to identify a long-list of potential stocks. Screening helps to take the emotional edge out of investing by providing you with a list of stocks based purely on quantitative metrics. We have some screening ideas for you below.

Select the stocks from your screen. There are two ways utilise your screen.

The first is to add a layer of discretionary analysis. For this you can use your screen to identify companies for further research. Assess whether they fulfil your quality and value criteria - if they do, add them to your portfolio. If they don’t, add them to a watchlist and wait for them to hit the valuation or quality measure that you require.

Alternatively, you can employ a full systematic strategy and let the screen do all the work for you. For this, pick one of the ranking screens below and add the highest ranked stocks from across the sectors to your portfolio.

Diversify to boost the power of averages. Identifying enough stocks which hit all your criteria to build a portfolio is not easy (some might say it is impossible). Instead you’re better off building a diverse portfolio of companies whose metrics average out to provide the perfect criteria. Perhaps no single stock in your portfolio will have the perfect combination of EV/Sales, earnings yield, ROCE, operating margin and cash conversion, but combined your full portfolio will have a perfect average. For this reason, you should seek to build your portfolio to between 20 and 30 stocks across all financial sectors.

Assess and rebalance. Set yourself a date for assessing your portfolio performance - if your liable to pitfall number one (freaking out) it’s best not to do this too regularly! On assessment day, check your portfolio stocks for drift - do they still match the criteria which prompted you to add them to your portfolio? If not, it might be time to sell. Also check your portfolio for weighting: are you overweight in certain sectors or geographies? Always attempt to keep your portfolio suitably diverse.

Contrarian screens to support your portfolio

To identify a long-list of potential contrarian stocks you can, of course, set up your own screen which filters for your desired quality and valuation metrics.

I have a ‘Quality at a Reasonable Price’ Screen which identifies companies which:

Have strong profitability metrics: 5yr average ROCE greater than 18% and 5yr average operating margins greater than 10%

Are growing earnings: 3yr EPS CAGR of at least 5%

Have a strengthening balance sheet: Current net gearing is lower than net gearing at the same time last year

Are valued at lower than their own history and the sector average: A current P/E ratio of less the historic P/E ratio and the sector average

Have an earnings yield of at least 5%

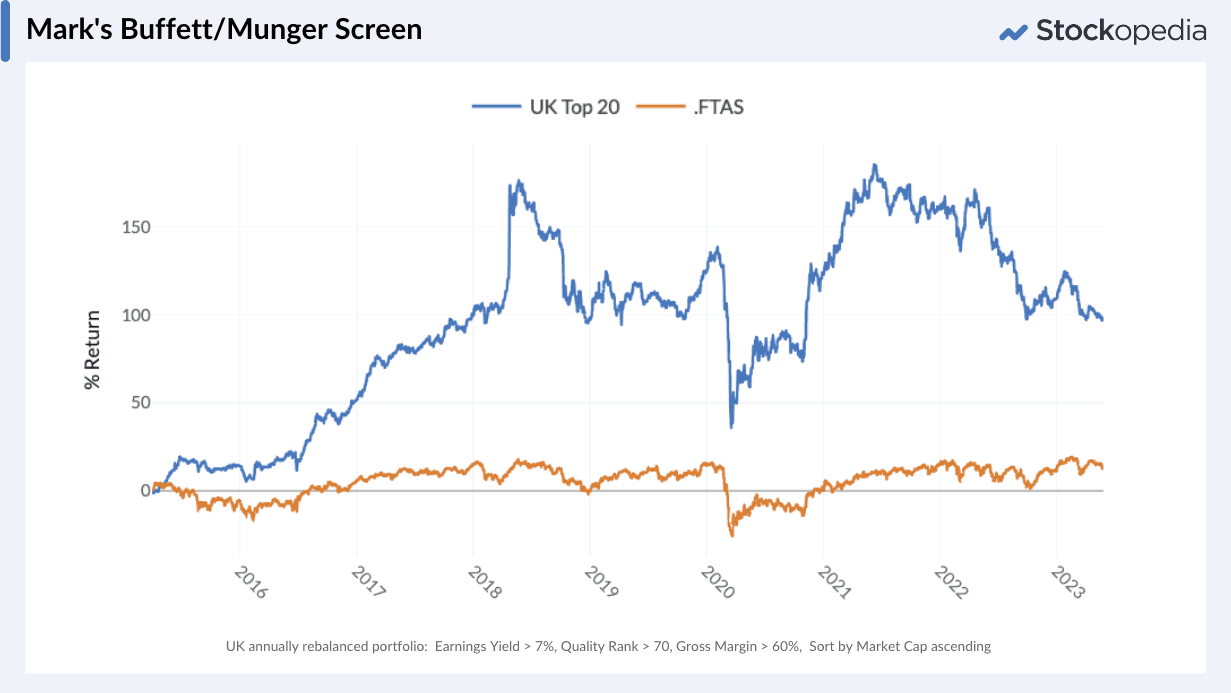

Mark has created a ranking screen based on the priorities of Warren Buffett and Charlie Munger, which utilises Stockopedia’s Quality and Value StockRank tools:

Companies are among the top 30% of quality stocks, shown by a Quality Rank greater than 70

A gross profit margin which is among the top 30% in the market

An earnings yield of at least 7%

Only in the sectors favoured by Buffett and Munger and therefore excluding Oil & Gas stocks, Metals & Mining stocks and Residential & Commercial REITs

We also have a large library of screens created by (or based on strategies employed by), legends of the investment industry. These are called the Guru Screens and you can find the ones to suit contrarian investors in the Quality, Value and Growth libraries. Here is an overview of my favourite.

Joel Greenblatt’s Magic Formula

The Little Book that Beats the Market (which provides the story behind Joel Greenblatt’s Magic Formula screen) is essential reading for all Stockopedia employees.

In his screen Greenblatt has come up with his own algorithm for analysing stocks based on their ROCE and earnings yield. He then uses this algorithm in a screen which identifies the top ranked shares according to this ‘magic formula’.

The thinking behind this methodology is to use the screen to build the whole portfolio. The stocks that come out at the top of the screen should be added and the portfolio should be monitored and rebased periodically to ensure that the stocks still match the criteria. Greenblatt is a strong advocate of the idea that "most people have no business investing in individual stocks on their own." He claims that beating the market is difficult even with the power of an asset management firm behind you, so private investors have very little chance. Instead, by building a well diversified portfolio built on the quality and value factor that drive the market, he believes that he can build winning portfolios that are easy to construct, no matter what level of knowledge you have.

Buy when there is blood on the streets and sell when…?

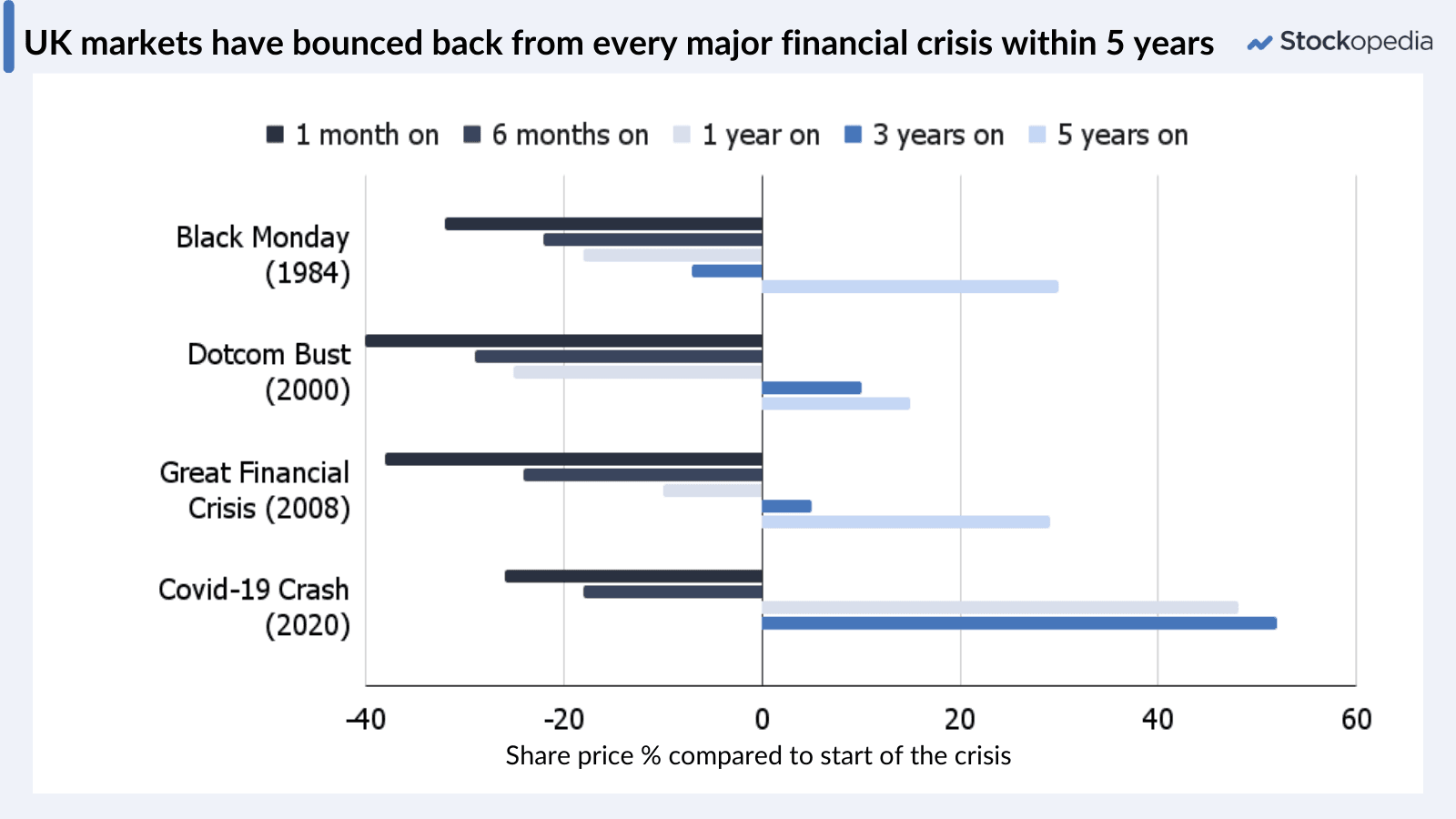

Nathan Rothschild is credited with coining the phrase “buy when there is blood in the streets” some time around the turn of the 19th century. It has been wise counsel for contrarian investors during every major stock market crash since then.

But when should contrarians sell?

The theory states that investors employing this strategy should sell their stocks once they become over-valued because the market will eventually realise its over-exuberance and self-correct, sending prices down again. In practice that means contrarian investors should sell the shares in companies whose market price has overtaken the inherent value of the company.

But in recent years, investors who have made that decision have missed out on some pretty spectacular gains. Many (myself included) said Apple was over valued when its market capitalisation hit the $1trn mark in 2018. Two years later, the company was worth $2trn and, for a brief period at the start of 2022, it became the world’s first $3trn company.

On the face of it, selling Apple shares in 2018 was a mistake, the returns since then have been spectacular. And while that is true for pure quality investors (who seek stocks to buy and hold forever), it’s perhaps untrue for contrarians. Selling when a stock is overvalued is key because it frees up capital to re-invest in other undervalued stocks, which might appreciate even more.

The real question that contrarians must ask is what is the inherent value of the company and has the market got it wrong?

Recommended Reading

The Little Book that Beats the Market - Joel Greenblatt

The Intelligent Investor - Ben Graham

The Sceptical Investor: How contrarians bet against the market and win - and you can too - John Stepek