Good morning! I'm back in the UK, but didn't get home until 4am this morning, due to a delayed flight, so might have to curtail this report a little, depending on how things go.

ED Investor Forum

A diary note for Wed 24 Jun (next week) - it's the next Equity Development private investor forum. The companies presenting are Staffline (LON:STAF) , Cranswick (LON:CWK) , and OptiBiotix Health (LON:OPTI) .

The hospitality is always good at these events, but on this occasion a little bird tells me that Cranswick will be bringing along samples of their products for investors to try.

It's the usual venue behind Oxford Street tube, in central London. The booking page is here.

The biggest faller of the day so far is;

Flowgroup (LON:FLOW)

Share price: 15.4p (down 37% today)

No. shares: 317.5m

Market Cap: £48.9m

Update - this company is trying to commercialise a new type of domestic boiler, which produces electricity at the same time as heating radiators. Today's announcement is really a stroke of very bad luck for the company - the European Court of Justice has ruled that the UK's lower rate of 5% VAT for energy saving products is illegal. This seems a perplexing judgement, given that one of the EU's biggest priorities has been pushing member states to improve the environment, and reduce energy consumption.

It's surprising that the stock market had apparently not noticed this announcement, despite it being reported widely in the press on, and shortly after 4 Jun 2015. Flow today says that it will have a significant negative impact on them;

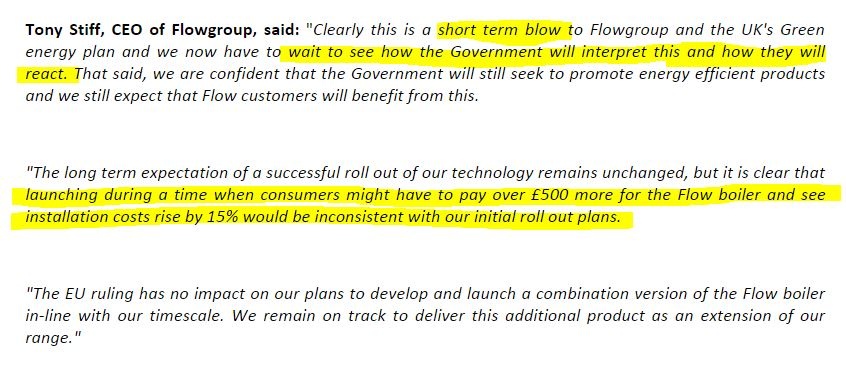

This is clearly a serious blow, as the final price to consumers will now rise by 14.3%, due to VAT being charged at 20% instead of 5%. Given that the product was already more expensive than conventional boilers, this additional cost is undoubtedly going to hit sales, as the company suggests.

Although the cynic in me thinks that the company would have struggled to commercialise this technology anyway - it's so difficult to dislodge existing, tried & tested technology in any field. So maybe this VAT bombshell provides a convenient excuse for disappointing sales?

Cost reductions - Flow says that it will accelerate its focus on driving down the cost of production with its outsourced manufacturing partner, Jabil, in an attempt to offset the VAT rise.

Government stance - doing a bit of googling, it seems that the UK Govt has not yet responded to the ECJ's ruling. There is some suggestion that the ECJ ruling could be circumvented by the UK, if the Govt reclassifies the purpose of the lower 5% VAT rate. Alternatively, the UK Govt might increase subsidies for energy efficient products, to offset some or all of the impact of higher VAT.

So it sounds as if the position is fluid, and if the UK Govt does what it should do, but so rarely does - i.e. play the game like everyone else in Europe does, and get round the EU rules, instead of slavishly following them to the letter, then maybe FLOW might possibly regain some benefit from the lower VAT rate?

Financial position - reviewing the accounts for 2013 and 2014, FLOW burned about £9-10m p.a., and had net cash of £6.2m at 31 Dec 2014. However, it raised an additional £22.2m before expenses, so perhaps £21m net of expenses, in May 2015. Timely! Therefore it looks as if the company has adequate cash resources for the next, say, two years. That should be long enough to determine whether this project is commercially viable or not.

Directorspeak - the CEO's comments today make it clear that this is a serious blow, and not something to be brushed off lightly;

My opinion - I looked into the economics of the FLOW boiler earlier this year, and came to the conclusion that it didn't really stack up, at least not convincingly enough to make it worthwhile for owners of larger houses to take the risk of installing a completely new type of boiler. The cost savings look a bit manufactured to me - i.e. perhaps more about clever marketing, than actual savings?

To my mind, the company has invented a solution to a problem that doesn't exist, because conventional boilers are already so efficient, and relatively cheap, that it's difficult to see why anyone would seek out an alternative.

The market cap is still nearly £50m, which doesn't strike me as a bargain, given that this project is commercially unproven, and has just been dealt a hammer blow by the ECJ with this VAT ruling.

There again, people who are convinced that the product is the best thing since sliced bread, and think that the VAT issue might be circumvented, could see this as a buying opportunity perhaps?

It's another reminder though that virtually every blue sky stock that comes to AIM either ends in total failure, or at best will take years longer, and consume far more cash than originally planned, to achieve the original business plan. If investors were rational, we would just stop investing in this type of stock altogether, as risk:reward is so absolutely dire - they nearly all fail! Yet many of us love a good story, and with endless optimism we get sucked into a few of these story stocks each year, and undermine our overall investment performance accordingly.

Some of my friends are in this stock, so I'm sorry (but not surprised) to see that, so far, it hasn't worked out. Still, the company has no immediate cash worries, so it lives to fight another day.

EDIT: I see that Entu (UK) (LON:ENTU) has been marked down about 5% in sympathy with FLOW, since it is an installer, and also sells other energy saving products. However, on checking the Govt website, it transpires that Entu's main products, double glazing & conservatories, are already taxed at 20% VAT, so the impact of the VAT change on them are likely to be limited.

Accsys Technologies (LON:AXS)

Share price: 70.8p (down 5% today)

No. shares: 88.8m

Market Cap: £62.9m

(at the time of writing, I hold a long position in this company)

Results for y/e 31 Mar 2015 - this is an interesting growth company, which sells the "Accoya" and "Tricoya" wood products. The market seemed unsure how to react to the results, as there was a sharp spike down in the first hour of trading today, down to as low as 57p, but the price has since largely recouped those early losses.

The full results announcement is a whopper, and published in a frustratingly tiny font for the narrative. It's too small for me to read comfortably on the computer, so am having to print it off in landscape, which comes to 60 pages. So this afternoon will mostly be going through the detail with my highlighter.

A quick snapshot of the headline numbers though;

Revenue - up 38% to E46.1m for the year (to 31 Mar 2015). This is ahead of forecast shown on Stockopedia of E43.5m.

Underlying EBITDA - has improved from a E5.0m loss last time, to a E2.4m loss this time. More encouragingly though, note that H2 was close to breakeven, with a E0.4m loss.

Underlying loss before tax - has reduced from E7.5m to E5.0m, so some progress, but still negative.

Financial position - loss-making companies are fine, as long as they are heading towards profitability, and are not going to run out of cash before they get there!

In this case, I've reviewed the balance sheet and cashflow, and it seems to me that the company should be fine. It had E10.8m in cash at 31 Mar 2015, down from E15.2m a year earlier, but importantly, there were no equity fundraisings during that whole two year period. Therefore Accsys seems to be doing a good job in having raised the cash it needs, and operating within its budget. I like that.

A smallish top-up fundraising is a possibility, but with good growth & strong demand for the product, I reckon it would be fairly straightforward to top up the coffers with a say E5-10m placing, if needed. So that's not a worry for me. The expansion plan seems to be revolve around out-sourcing production to partners such as Solvay, which is building a manufacturing plant for Accoya in Germany. There is another deal with a large international chemicals group to build a Tricoya plant.

Outlook - all sounds upbeat. The company says it will "build towards becoming cash-flow positive in the year ahead, and longer term, achieving profitability" - cleverly worded, so it doesn't actually say they will be cashflow positive this year!

Supply constraints - what is most striking in the narrative, is the potential market size for these products, which is many times current production levels. The main issue at the moment is supply constraints. The existing Arnhem factory has a production capacity of 40,000 m3 p.a., whilst sales in 2014/15 were 33,483 m3, so there is not much additional headroom to increase sales in the short term.

However, once production by partners ramps up, then things could start to look very interesting.

My opinion - most growth companies struggle to convince people to buy their products. In this case, it's the other way around - they can't make enough of it! That's a quality problem to have, in my view, because over time it can be fixed.

Therefore this share seems to have passed from being overtly speculative, into being a play on how well management are able to manage growth. The cash burn is modest, and there doesn't seem to be any need for additional equity. Broker forecasts are for a small profit this year, but it's what happens after that which intrigues me, once the bigger third party factories come on stream.

Overall, my view is that this stock has the potential to be a multi-bagger in several years' time. In the meantime, it looks reasonably priced to me, given the potential. Certainly out of the two growth stocks I've written about today, with roughly similar market caps, I think Accsys looks a far better investing proposition than FLOW, in terms of likely risk:reward. That's just my personal opinion, and you may have a different view, which is fine - feel free to add comments in the comments below.

Trifast (LON:TRI)

Share price: 129p (up 1% today)

No. shares: 116.2m

Market Cap: £149.9m

Results for y/e 31 Mar 2015 - shares in this industrial fastenings group had been bouncing around above & below 100p over the last year, but have recently made a push higher, to 129p. That looks justified, when reading the results published today.

I've only done a quick review of the main numbers, and it looks good to me.

Underlying diluted EPS - drops out at 8.68p (up 45.9% on prior year), which looks to be ahead of analyst forecast of 8.09p, assuming that the forecasts are prepared on a comparable basis to the reported EPS. Note that there are some separately identified items, which mean that basic EPS is lower, at 7.39p.

So a really strong result, although note that the company is making acquisitions, and has taken on some debt to fund them, so that helps boost the growth figures.

Net debt - is reported at £13.4m, versus net cash of £2.0m a year earlier. This level of debt looks fine to me, and is not a worry. There doesn't seem to be a pension deficit, which is good.

Overall the balance sheet looks fine to me, no issues there.

Dividends - a 50% increase to 2.1p for the full year, but coming from a low base, so the yield is only 1.6%. The company comments that it intends paying divis that are 3 to 4 times covered, so it's effectively retaining most of its cashflow for expansion. Given that this strategy has worked well so far, then I think this policy makes sense.

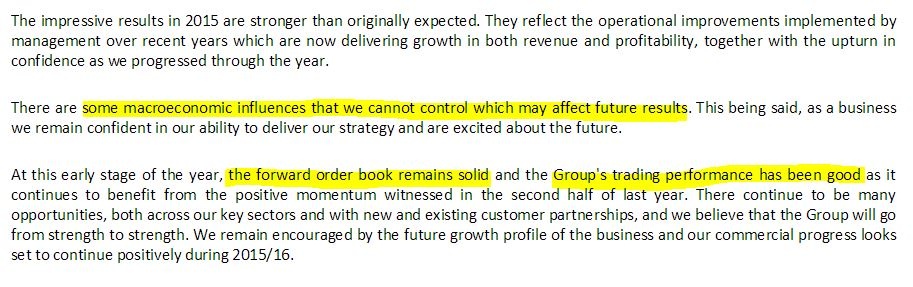

Outlook - this sounds mostly upbeat, with a note of caution about macro factors, which is fair enough:

My opinion - this looks like a well-managed business, that has been performing well for several years now. I like the comments in the narrative about their customers streamlining their supplier bases, to fewer, but good quality suppliers.

The recent surge in share price looks justified in my view, and I would say that these shares look priced about right for now at 129p, which looks to be about 14 times current year earnings estimates. However, if they keep out-performing, and making sensible acquisitions, then there could be continued longer term upside in these shares.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.