Good morning!

Trinity Mirror (LON:TNI)

Share price: 154p (down 3.3% today)

No. shares: 257.7m

Market Cap: £396.9m

Trading update - this covers H1, the 26 weeks to 28 Jun 2015.

The revenue trend seems very poor to me. Revenue for H1 is expected to fall by 11%, with what they call underlying revenue (i.e. like for like) down 9%.

More strikingly, print advertising revenue is down a colossal 19% in the period. To my mind this clearly demonstrates that advertisers are reallocating budgets to other forms of advertising, especially online, social media, etc.

Once again TNI has been able to mitigate the drooping top line with yet more structural cost cutting, targetted at £20m for this year, up from £10m announced in Mar 2015. This is continuing the same pattern of cost reductions to maintain profits, which has been happening for years now.

Although cost cutting also comes at a cost - £15m restructuring charges are expected.

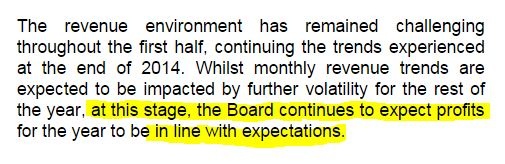

On profitability, they're sticking with full year expectations (for now - note the "at this stage" qualification);

Phone hacking - a potentially very serious issue, in my view. There's no new info today on this, with the company confirming that "there remains uncertainty as to how matters will progress". I suggest the news is more likely to be bad, than good - because there is already information in the public domain that TNI were heavily involved in phone hacking, and that management very much tried to cover up this issue in the past. So costs are likely to mount, in my view.

Valuation - the bizarre thing with TNI is that, whilst most people accept that the business is in terminal decline, it's still generating astonishing amounts of cash. It's very difficult to think of any other industry which is dying out due to technological & fashion changes, yet is still churning out huge profits.

The big question is, how long can this continue? Valuing a dying company on a PER basis is clearly meaningless, and the current year PER of 4.9 reflects the probably short life remaining for this business, in its current form anyway.

I think it can only really be valued as a special situation, effectively on a winding up - how much cash will it generate before the business has to be shut down? Is there any residual value in the digital businesses, once the newspapers close? Or, if you're an optimist, could some newspapers continue on a free to customers basis, as the Evening Standard & Metro seem to have successfully done?

Then there are the assets and liabilities to consider. The pension scheme here is huge, and will probably consume a lot of the remaining cashflow that the business generates in its last handful of years. However, TNI also has some valuable freehold property assets - so it might end up becoming a property company once the papers have shut down?

Dividends have recently resumed, but only 5p is forecast for this year, so a yield of only 3.1% is nowhere near enough to get me interested. I think this share would only make sense as a last puff of the cigar butt, if the yield was >10%.

My opinion - I loved this share in 2012, at 25p per share, when it was my best investment of the year. However, at 154p there is no appeal in my view. True, the debt has been cleared (as I correctly predicted), from the amazing cashflows of the last few years, but at some stage (certainly under 5 years, in my view), profits & cashflow are likely to really tank. I think we could be near to that tipping point, as the 19% reduction in print advertising revenue should be setting alarm bells ringing with investors here - that's not a steady decline, it's plummeting - suggesting that a major structural change in advertiser behaviour is occurring.

So a big thumbs down from me - this looks a value trap, in my opinion - revenues are now declining too fast to hold out much hope of a decent shareholder return.

Tungsten (LON:TUNG)

Share price: 61.5p (up 8.4%)

No. shares: 125.4m

Market Cap: £77.1m

Buyout speculation - there's an article in the FT today, suggesting the Edi Truell might take Tungsten private. It's possible, but that would be such a kick in the teeth to all the people who bought into the heavily ramped (by Truell himself!) story at much higher prices.

After all the big talk, that lured in many investors, including me (until I realised that I'd made a mistake, and reversed my view of the shares in Jan/Feb 2015, and was on the receiving end of some misguided abuse I might add), Truell's execution so far at Tungsten has been appalling, incompetent even - cash burn far higher than expected, several more fundraisings (the last one at a distressed level), and the original targets for profitability were missed by a mile, yet as usual PIs were the last to find out.

So a very unhappy tale, which has justifiably seriously damaged his reputation. This puts me in mind of my favourite quote from Bill Gates;

"Success is a lousy teacher. It seduces smart people into thinking they can't lose."

What happens to Tungsten then? Who knows? Perhaps Truell will take it private, but at what price? There would have to be a premium to the current price to persuade people to sell, but would long term investors be happy to sell out below their original purchase price?

Or, if you're more sceptical, you might think that putting out a rumour of a buyout might be a good way to trigger a short squeeze!

Here is the latest data from the FCA website on disclosed short positions in TUNG, which total up to 5.94% of the whole company:

My opinion - I got this one wrong originally, and hence have no plans to revisit it, either as a long or a short position.

In my view this is yet another example of how the stock market is just not suitable for early stage, speculative growth companies. The problem is this - the stock market swings from wild optimism to great pessimism - Ben Graham's famous analogy springs to mind.

So if a speculative, cash burning company like Tungsten, or on a smaller scale Synety, runs of cash at a time when the market is depressed, then it is in a full-on crisis. Often, to get a fundraising away, the price has to be a deep discount - half or less the prevailing share price before the market woke up to the reality that more cash was needed.

Therefore in my view, speculative shares should only be floated on the stock market if they raise enough cash up-front to reach breakeven, with a large contingency reserve on top, for the inevitable cost over-runs, and delays that always happen.

Poor execution, and not raising enough cash, scuppered the big story at Tungsten - plus I think also a realisation that what they are doing is not unique at all, other companies are doing the same thing.

Tungsten might yet succeed, but as I mentioned in a previous blog here, in my view the company needs to raise A LOT more money, maybe £100m, to really go for it, in terms of hoovering up market share.

It never should have been floated, the stock market is the wrong place for it. High growth, heavy cash burning companies should be privately owned, by entrepreneurs, VCs, etc. They should only be floated once they are past the cash burning stage, in my view.

I should add that I'm sorry if any readers lost money on TUNG and were influenced by my previous bullishness on the company. As a general rule, just ignore me when I write about speculative companies, as most of them will go wrong.

As this is a Value/GARP focussed column, I'm trying not to include any speculative companies now, or at least not completely blue sky stuff, as they nearly always go wrong - blue sky investing is a complete mug's game, except when you're in a roaring bull market & you can catch a speculative wave - but that's trading, not investing.

The other lesson is - listen to the shorters! It may be unpleasant to read negative opinions on a share you own, but it's absolutely vital to understand the negative case, as well as the positive one. People who close their minds to downside risk usually end up paying a heavy price for that stupidity.

Investing has to be rational to succeed - the moment we fall in love with a share, and think about it emotionally, we're half way to a disastrous loss. I'm very much talking from extensive personal experience on this point! Fighting those emotional responses is probably the single biggest key to better investing, in my experience - as very often your emotions will be telling you to do the exact opposite of what you should be doing.

Essenden (LON:ESS)

Share price: 80p

No. shares: 50.1m

Market Cap: £40.1m

(at the time of writing, I hold shares in this company)

Recommended cash offer at 80p - what a let down! In my view this 80p bid for the company is a complete stitch-up. It follows a pattern I'm afraid, of an aggressive major shareholder (Harwood Capital) bullying management into submission, then taking the company private at a derisory price, pocketing the upside for themselves.

Essenden has been a terrific turnaround, and there's no reason at all why it cannot continue as a successful listed company. This bid is all about self-interest for the bidders, who are nicking the upside from existing shareholders, in my view.

I'll certainly be voting against the proposal. Trouble is, the institutions will probably accept it, as they don't have any liquidity - so getting out cleanly with a cash payment, might be seen positively by them.

The take out price is far too low - a forward PER of only 11. Management should not have recommended this bid, and have failed in their duty to shareholders, in my view. The exit price should have been 120p+ to be considered a fair price, in my view.

I've noticed that Harwood are very good stock pickers, they're in some very good, undervalued micro caps. However, their modus operandi seems to involve making opportunistic, under-priced bids, thus capping the upside for other shareholders.

Stanley Gibbons (LON:SGI)

Share price: 255p (up 2.2% today)

No. shares: 46.8m

Market Cap: £119.3m

Results for y/e 31 Mar 2015 - these results look potentially interesting, although they're not the easiest to interpret as the prior period comparatives are 15 months, due to a change in year end.

Checking back in my notes here, my report on 2 Apr 2015 commented on the company's profit warning - triggered by several high value sales not completing by the year end. This emphasises that SGI is vulnerable to large individual sales.

Adjusted EPS of 12.9p for y/e 31 Mar 2015 has come in way below pre-profit warning forecasts of 20.2p, but bang on more recent forecast of 12.9p. So the historic PER drops out at a rather high 19.8.

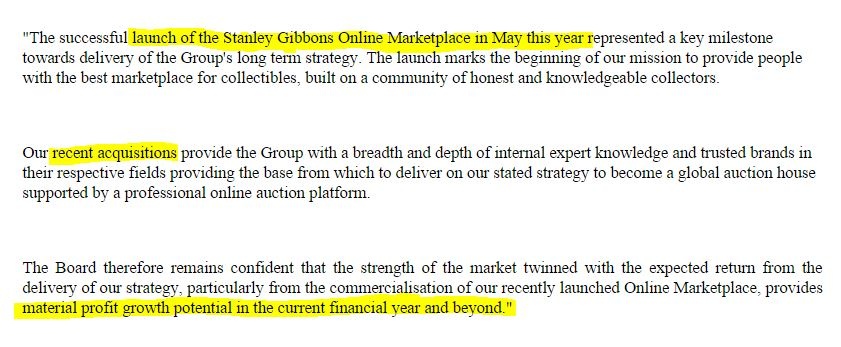

Outlook - it's obviously more important to look at what EPS & cashflows the group is likely to generate in future. SGI has made two recent acquisitions, so that should push up future earnings. Also it makes interesting noises about its new online marketplace, which could be a catalyst for the shares to re-rate. I can see the attractions of a SG-branded ecommerce site for collectibles, rather than taking the risk of unknown Ebay sellers.

EPS of 17.0p is forecast for this year, which equates to a PER of 15, which looks about right.

Balance sheet - this looks in good shape, and as you would expect, is dominated by the inventories balance of £53.8m. The company says there is additional value over this figure, as stock is stated at cost, but has significant unrealised profit potential.

The current ratio is great, at 2.96, with a surplus of £49.8m in cash terms (i.e. that is the amouny by which current assets exceed current liabilities).

Long-term creditors are not excessive, at £17.2m, which is mostly £9.2m bank debt, and a £5.8m pension deficit.

So overall, I'm very happy with this balance sheet, it looks fine.

My opinion - I'm in two minds about this. Conceptually, I find huge prices for stamps utterly ridiculous. The worry is that, at some point, collectors dwindle, and the prices collapse. But that process is not likely to happen overnight.

A PER of 15 for an established, profitable business, with a fantastic brand name that is known globally, and a growing internet presence, sounds potentially interesting.

It has a strong balance sheet too, which protects the downside, so overall I would say this one is worthy of further, more detailed research possibly.

Spaceandpeople (LON:SAL)

Share price: 78p (up 25% today)

No. shares: 19.5m

Market Cap: £15.2m

(at the time of writing, I hold a long position in this share)

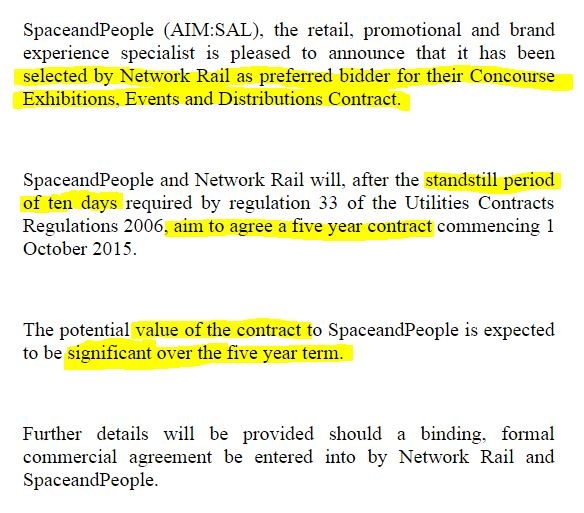

Award of preferred bidder status - I don't normally comment on contract win announcements, unless they look material. Since this announcement came 25 mins before the market close, and moved the share price up 25% on the day, then it's worthy of a mention!

Although I have to mention the highly suspicious flurry of trades which began late morning today - quite obviously insider dealing, especially whoever paid 3p above the offer price of 65p, to acquire 17,627 shares at 68p, printed at 11:08 this morning. That person is quite obviously an insider dealer, and needs to be hauled in front of the Courts. Will the FCA do anything? Not a chance!

Really, what is the point in having insider dealing rules, if they are so widely flouted?! Someone was clearly in possession of price-sensitive information, and traded on that information. That is illegal, so they should be punished.

I seem to have spent the whole day on my high horse, getting wound up by bad things happening! So it was nice to end the day with a few extra £ profit (well, more like recouping previous losses) from the bullish sounding SAL announcement, which reads:

My opinion - I don't want to jinx it, as things are not formally signed yet, so let's wait to see what the outcome is. Of course, this sounds a potentially important deal.

As I've maintained right through the profit warnings last year, this is a fundamentally good business, with entrepreneurial management, which just ran into a whole series of problems last year. They needed time to fix things, and it looks as if management are getting the business back on track, and I think potentially on to greater success, as there are other bullish things in the pipeline, e.g. the new mobile promotional kiosks beginning a roll out.

We're clawing back some of the losses from last year anyway.

It's worth noting that when everyone absolutely loathed this stock, late last year, would have been a great time to buy! Worth bearing in mind, that. It's the contrarians who catch the worms early, sometimes.

OK, I'll leave it there for today. No video today, as I covered everything I wanted to in the main report above. To recap on the two videos I've done earlier this week, please see my YouTube channel.

Have a smashing weekend & see you back here on Monday morning!

Regards, Paul.

(of the companies mentioned today, Paul has long positions in ESS and SAL, and no short positions. A fund management company with which Paul is associated may also hold positions in companies mentioned.

NB. Paul NEVER gives recommendations, or financial advice. This blog is his personal opinion only, and the emphasis is on readers to DYOR, and make your own investing decisions).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.