Good morning!

12.45pm: that's all for today, thanks!

Spreadsheet accompanying this report (last updated to: 23rd Jan 2025)

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| AstraZeneca (LON:AZN) (£173bn) | Final Results | Rev +18%, Core EPS +13%. FY25 guidance: Rev + high single-digit %, Core EPS + low double-digit %. | |

Compass (LON:CPG) (£47.4bn) | TU | Q1 organic rev +9.2%. Organic growth drivers in line with exps. 2025 guidance unchanged. | AMBER/RED (Graham) I don't think it makes sense to pay a PER of 25x for a caterer even if it is performing well and expected to grow profits at c. 10% p.a. for the next few years. |

Anglo American (LON:AAL) (£28.3bn) | Production Report Q4 | Production guidance delivered. Forward guidance is unchanged in copper, reduced for diamonds. | |

Babcock International (LON:BAB) (£2.7bn) | Q3 TU | Revenue & underlying operating profit to exceed top end of the range. Revenue c. £4.9bn. | AMBER (Graham) A very pleasant trading update and it's not due to success in just one area but in multiple areas, which makes it even better. I think BAB is fairly valued here. |

Watches of Switzerland (LON:WOSG) (£1.3bn) | Q3 TU | In line. Confident in delivering guidance. Refinanced term loan in December, new £150m facility. | AMBER/GREEN (Graham) |

| BBGI Global Infrastructure SA (LON:BBGI) (£870m) | Rec. Cash Offer | 147.5p in cash, 21% Premium | PINK (Mark) |

Sigmaroc (LON:SRC) (£785m) | Secondary Placing | 15.4% of shares sold via bookbuild at 67p | AMBER (Mark) |

Warpaint London (LON:W7L) (£425m) | TU | FY 24 Rev +14% to £102m, PBT +33% to £24m. January Rev +15% | AMBER/GREEN (Mark) |

| Spectra Systems (LON:SPSY) (£104m) | New Security Printing Postal Contract | 5-year contract to produce postage stamps for a new EU customer. $3- $4m value. | Graham's view: This is a “Reach” announcement, so it’s not material. |

Anexo (LON:ANX) (£77m) | TU | In line. Potential settlement of claims against vehicle manufacturers to enhance profits. | RED (Mark) |

Tpximpact Holdings (LON:TPX) (£30m) | Q3 TU | Q3 In line. FY warning: Rev. down 8-10% vs FY24, adj. EBITDA slightly up on FY24. |

AMBER (Mark) |

tinyBuild (LON:TBLD) (£25m) | TU | Rev, adj. EBITDA “broadly in line”. Current trading remains difficult. Cash to trough in summer. | RED (Graham) Tough conditions in the video game industry, and TBLD hasn't helped itself by running its cash balance low for the second time in two years. |

Graham's Section

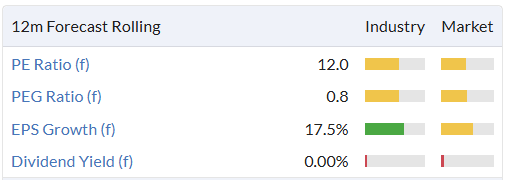

Watches of Switzerland (LON:WOSG)

Up 1% to 562.5p (£1.35bn) - Q3 FY25 Trading Update - Graham - AMBER/GREEN

The market was very pleased with the “in line” update issued by WOSG in December.

Today we have another in line update that leaves guidance unchanged.

Market conditions are supportive:

Over the period, we have seen further stabilisation of the UK market in both luxury watches and jewellery, while the US market has seen continued momentum

Watch revenue was down 2% in H1, so hopefully we’ll see something better than that for the full year?

The company has made some acquisitions which are boosting total revenues. As usual, I’ll place more emphasis on organic numbers when we get more details.

In store news, a new flagship Rolex boutique is set to open in March in Old Bond Street, London.

Refinancing: a $115m term loan (set up to fund the acquisition of Roberto Coin in the United States) has been replaced by a £150m facility.

Outlook: “confident in delivering our FY25 guidance”.

Graham’s view

I’ve been moderately positive on this one for a while - the best part of a year. It’s a stock that makes me nervous, as I worry about the fundamental quality of a retailer that doesn’t own any of the IP it sells. Let’s call this the Currys (LON:CURY) of the jewellery industry.

However, like Currys, WOSG also appears to have its house in order. It has US-based growth opportunities, solid backing from lenders in relation to the acquisition of Roberto Coin, and a valuation at c. 560p that isn’t overly stretching.

It’s not the highest-quality business that we cover in this report, nor the most exciting, but I think I can leave my moderately positive stance unchanged.

It has survived a boom and bust in the secondary watch market, and is forecast to generate almost as much profit this year (c. £96m) as it did in FY2022 (£101m). The share price is still only about half the price now as it was back then:

tinyBuild (LON:TBLD)

Unch. at 6p (£25m) - Pre-Close Trading Update - Graham - RED

tinyBuild (AIM:TBLD), a premium video games publisher and developer with global operations, is pleased to provide a trading update for the twelve months ended 31 December 2024 ("FY 2024").

This is not quite in line, but it’s close - “broadly in line” for 2024.

According to a note published by Progressive in December, they estimated revenues of £35.3m and adj. EBITDA of minus £4.4m for FY Dec 2024.

These were downgraded expectations on the basis of delays to game publication by TBLD but I note that there was no official RNS from TBLD in December. I'm quite amazed by that actually - let me reiterate that there were very large downgrades at Progressive (who are paid by TBLD to cover them), but there was no accompanying RNS from the company. Profit forecasts for 2024 were reduced by nearly £5m.

Turning back to the present, the cash position doesn’t sound very good: “Cash and cash equivalents of low single digit millions at the end of December 2024”, with this expected to reach a trough in the summer of 2025 and improve thereafter following the launch of certain new games.

For context, the last time I covered TBLD was in Dec 2023 when it issued a profit warning after it had burned through nearly $50m of cash in two years. Shortly afterwards, it raised $11m (net) in a placing.

By the time it raised money in that placing, its cash balance had fallen to $2.5m (as of Dec 2023), and perhaps fell lower again before the funds from the placing were received.

And now here we are a year later, with cash back in the low single digit millions. There is a pattern of TBLD running on fumes when it comes to its cash balance, but hoping to fill up again when games are published.

I understand that game development has to be paid for first, before any revenues can be generated. I just think it’s very unfortunate that the company started with such a cash-rich position a few years ago, and then ended up having to dilute shareholders. TBLD’s share count nearly doubled last year, which might have been avoided if the company hadn’t spent so aggressively during the previous two years.

And how can we rest assured that further dilution won’t be necessary?

This appears to suggest that IP could be sold off to avoid further equity dilution:

The cash position will be carefully managed as the Company invests in upcoming game releases in a disciplined manner. The Company has no borrowings and it continues to assess its IP portfolio for strategic opportunities.

Pipeline: some game launches are coming up, with the potential to convert into revenue. One of them is in the top 20 on the Steam platform, in terms of user wishlists.

Outlook: in line for 2025.

Again turning to that note published by Progressive, for 2025 they forecasted revenues of £36.8m, adj. EBITDA of 2.2m, and an adjusted pre-tax loss of £3.3m.

Graham’s view

It might be harsh but I’m inclined to leave this on RED, as I did back in Dec 2023.

The limited cash balance, the delays affecting game publication (and associated downgrades to estimates), and the warning that cash will not trough until Summer 2025 - these do not fill me with confidence.

Yes, the shares are very cheap when measured using something like Price/Sales. Video games companies should trade at a strong P/S multiple, not at less than 1x as TBLD does. But TBLD burned through its cash when it was cash-rich (under existing management), and now I think investors might need to worry about the potential for another fundraising, if things don’t go as planned in 2025.

Checking the most recent balance sheet (June 2024), I note that the company said it had a “significant net asset position” of $70m and that there was no problem in terms of the going concern assumption.

However, $70m was its gross asset position, not its net asset position. Its net asset position was $53m, and of that $49m was intangibles. This figure is largely made up of money that has been spent on game development relating to future title launches. So really, this balance sheet is not as solid as the company made it out to be - it is built on the hope of future success.

I wish the company well and I note that the founder-CEO is well-aligned with a 20% shareholding. But I view this share as excessively risky and not offering a solid investment opportunity.

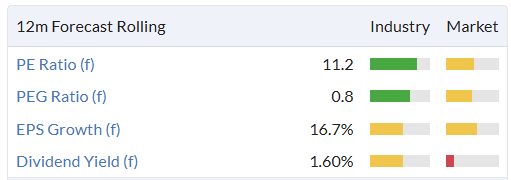

Babcock International (LON:BAB)

Up 10% to 598.9p (£3.03bn) - Q3 trading update - Graham - AMBER

This engineering services group issues a positive update that’s ahead of expectations. Q3 is now over and the company’s financial year-end is approaching in March.

The majority of revenue for the year is now under contract and, having reviewed the delivery forecast for the remainder of the year, the Board now expects both revenue and underlying operating profit to exceed the top end of the range of analyst expectations. Accordingly, we are upgrading our expectations for FY25 to c.£4.9 billion of revenue, with the expected overperformance due to double-digit organic growth in Nuclear and strong growth in Marine.

Prior analyst expectations are given as £4.51 - 4.78bn of revenue and £327.1 - 339.7m of underlying operating profit.

So this is a very pleasant beat: revenues are 2.5% higher than the highest estimate that was published by analysts, and nearly 9% higher than the lowest estimate.

The strong performance is attributed to various factors, from increased nuclear submarine support activity, to the ramp-up of Skynet (the MOD’s military satellite communications system).

The CEO says “our engineering skills and know-how are in ever greater demand”.

A new contract is mentioned: a 17-year, up to €800m agreement to provide military air training for France (the Air and Space Force, and the Navy). It is described as “a significant expansion of our military activity in France, one of our focus countries”.

If the contract reaches its full potential of €800m and was spread evenly over 17 years, that would amount to €47m of additional revenue p.a. But hopefully there is some front loading to these revenues?

Graham’s view - I think this is fairly valued here. It looks to be trading at around 11x underlying earnings, if you calculate earnings by applying a tax rate to a new, higher underlying operating profit estimate (e.g. apply 25% tax to a profit estimate of c. £350m, to get a rough idea).

The StockReport calculates a PER of 11x based on the date prior to this update:

And on that basis, the StockReport finds a ValueRank of 40, i.e. below-average value.

I agree that it’s perhaps a little expensive, but BAB can probably justify that based on its strong trading momentum and its association with landmark projects such as Skynet. My guess is that a neutral stance is fair.

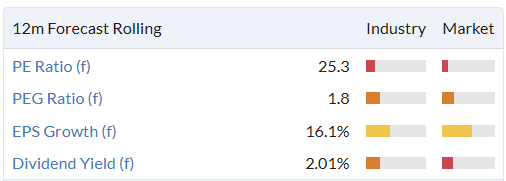

Compass (LON:CPG)

Down 1% to £27.62 ($58bn) - Trading Statement - Graham - AMBER/RED

Another brief trading update from an even larger company. Compass is in the top 15 companies listed in London, according to market cap.

Its year-end is in September, so this is a Q1 trading update for Dec 2024.

Guidance for 2025 is unchanged:

The Group delivered strong organic revenue growth of 9.2% in the first quarter. All regions and sectors performed well, with positive outsourcing trends continuing to underpin our growth momentum. Organic growth drivers were in line with our expectations, with net new business supported by strong client retention, and pricing and volumes trending as anticipated.

Growth was led by North America:

Expected organic revenue growth for the year is “above 7.5%”, and CPG has beaten that with some room to spare in Q1.

Similarly, underlying operating profits are expected to grow at “high single digit” rates. That will be growth vs. last year’s result of $3.0bn. So this metric should get to somewhere in the region of $3.2bn this year.

FX headwind: expected revenues for 2025 are some $45 billion, so investors will look past the current FX headwind of $558m.

Graham’s view

I’m afraid I don’t understand this valuation.

There is a trend of office workers gradually returning to work, perhaps that is the play here?

Even so, I can’t get behind paying 25x earnings for a caterer.

Forecasts for the next few years are positive (up to c. 10% profit growth for the next few years) but even so, there must be much better opportunities than this.

And there is no net cash position to fall back on to help support the valuation; it has a leverage multiple of about 1.3x.

I think I must lean towards a negative view on this one, consistent with the StockRank:

The stock’s positive momentum has been amazing in recent years - and I fear it has been overcooked.

Mark's Section

Tpximpact Holdings (LON:TPX)

Down 19% to 26p - Q3 Trading Update & Revised Outlook - Mark - AMBER

When I last looked at TPX following their Interim Results, they said

No change in FY25 targets: flat revenue growth for the year and Adjusted EBITDA in the range of £7-£8 million, and net debt of around 1x EBITDA

So it is good news that Q3 trading is said to be in line here:

The Board confirms that Q3 trading met management expectations, with profitability and margins aligning with the Company's forecasts. In the first nine months of the year, new business secured totalled approximately £65 million, including approximately £30 million in Q3.

However, the inclusion of the words “revised outlook” in the RNS title reveals that this isn’t, in fact, going to be good news for the outlook:

Management's expectations are that revenues for FY25 will decline 8-10% on the prior year.

Revenues were forecast to be flat year-on-year, so this is a reasonably large miss this late in the year. Blame is put on delays in procurement of large government digital transformation programmes due to a delayed spending review. There is some mitigation on margins:

Adjusted EBITDA margins for the Group are expected to improve by 1-2% year-on-year, as a result of reorganisation actions taken earlier in FY25, and should result in an improvement in Adjusted EBITDA compared to the prior year.

This is also not a one-off, with 2026 also coming in below previous expectations:

We anticipate our final budget will show revenue growth at the lower end of our previous guidance of 10-15% growth in FY26. We also anticipate continued year-on-year Adjusted EBITDA margin progression of 1-3%, noting the 1% headwind of increased employer National Insurance Contribution rates may lead us to the lower end of this range.

This gives me enough detail to calculate the likely impact of these guidance changes on Adj. EBITDA:

So, this is a major impact, especially on FY26 numbers. I can also estimate EV/EBITDA, taking the midpoint of their leverage guidance, which works out to be £9m net debt:

So, what looked like a cheaply rated stock on the previous forecasts…

…now looks fairly priced, at best.

Mark’s view

While the reasons for the miss here are largely out of the company’s control, this update highlights that this isn’t the highest-quality business. They have less control over their destiny than I’d like to see in a business. This isn’t ridiculously expensive, but it no longer looks cheap on the forward numbers despite an almost 20% fall in price today. So, I am downgrading this to AMBER.

Warpaint London (LON:W7L)

Down 4% to 510p - Trading Update - Mark - AMBER/GREEN

A short update on FY24 trading:

Revenue for the year ended 31 December 2024 is expected to be approximately £102 million (2023: £89.6 million) and profit before tax to be approximately £24 million (2023: £18.1 million).

Again, these are showing great operational gearing. Revenue is up 14% but PBT rises a wonderful +33%. These growth rates are in line with the medium term trends here:

It is this ability to grow earnings faster than revenue that has made this a multi-bagger over the last few years despite a fairly lacklustre first five years of being a listed entity.

It is hard to work out exactly how these compare to broker expectations because forecasts are suspended due to Warpaint taking over Brand Architekts. However, the last Shore note from September had £105m revenue and £24.5m adj. PBT. The stockopedia consensus was for £106m in revenue. So compared to these forecasts, the actual results appear to be a few per cent miss on revenue and PBT.

The good news is that 2025 has started well:

The strong trading performance has continued into January 2025, with revenue approximately 15% ahead of January 2024, at an improved margin.

Shore had £116.6m revenue forecast for FY25, so this year appears to be tracking in line with this. However, this is tracking behind the £124m consensus that is in Stockopedia, but this may now be out of date given the pause in coverage. The forward EPS consensus of 26.6p may prove conservative if the margin improvements continue to drive operational gearing. If this is the case, then the current forward P/E of 20 will be lower and look good value again.

Mark’s view

This is a mixed update. While the growth rates and operational gearing continue to be impressive, the numbers themselves appear to be slightly behind the consensus. Could this be the start of a trend for the company missing forecasts rather than exceeding them? Still, the 2025 EPS looks like it may be conservative, even if the revenue consensus isn’t. When I last looked at this in December, I thought the management looked a little keen to issue equity at these levels and rated it AMBER/GREEN until there were tangible signs that the FY25 forecasts would be beaten. Today’s update doesn’t yet provide enough confidence that this is the case, so I will retain the same rating.

Sigmaroc (LON:SRC)

Up 5% to 75p - Secondary Placing - Mark - AMBER

These types of announcements often confuse those who haven’t seen them before. Here is what the company said last night:

CRH announces its intention to sell up to 171,578,948 ordinary shares in SigmaRoc. The Placing Shares represent approximately 15.4% of the Company's issued share capital.

The Placing Shares are being offered by way of an accelerated bookbuild, which will be launched immediately following this announcement.

CRH received these shares as part payment for the lime assets that SigmaRoc acquired from them in November 2023. So the placing here is not the company raising money but major holder CRH wanting to sell their holding. However, the holding is so large that they can’t just sell in the market. Hence, they have asked brokers to place the shares with other interested investors. This morning, we get the result:

…it has sold in aggregate 171,578,948 ordinary shares at the price of 67 pence per share, raising aggregate gross proceeds of approximately £115 million.

Following completion of the Placing, CRH will have exited its interest in SigmaRoc in full.

So they have managed to sell their entire holding but had to take a discount to get them away, much the same as a company placing. The discount is relatively slight, and this is a good sign that there was reasonable demand for the shares at that price, especially when many UK asset managers are facing outflows at the moment. The market has taken this as a positive sign, and the price has risen 5% this morning. The buyers in the bookbuild are locked in for 60 days. This means they can’t immediately sell their shares to lock in a risk-free profit. However, they may well start to sell if the share price remains at these levels in 60-days’ time.

Mark’s view

Roland rated this AMBER following their Trading Update on Monday. While this overhang clearing is good news, CRH had to accept a discount to get it away, and it doesn’t change the fundamentals of the company itself, so I keep the same rating.

BBGI Global Infrastructure SA (LON:BBGI)

Up 17% to 142p - Recommended cash offer - Mark - PINK

This PFI infrastructure fund receives a takeover offer from Canadian infrastructure giant BCI. The offer is relatively modest:

147.5p in cash…represents a premium of approximately…21.1 per cent. to the Closing Price per BBGI Share of 121.8 pence on 5 February 2025 (being the last Business Day prior to the date of this Announcement)

This is a relatively modest premium, but then the discount to NAV was modest, and this offer is effectively at NAV (1/0.83 = 1.205)

This is why the deal is recommended by the board and looks fair, and a done deal.

Mark’s view

This is obviously good news in the short term for holders who get an exit at NAV. However, this also highlights why I don’t tend to invest in listed funds unless the discount to NAV is very large. The near-term upside from an offer such as this tends to give small premiums. Whereas the downside from the ones that go wrong tends to be quite large. Just look at the long-term share chart of Digital 9 Infrastructure, for example. Obviously, the failures are rare. However, the risk-reward seems skewed the wrong way for me to be an equity holder in similar funds.

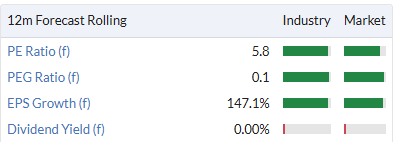

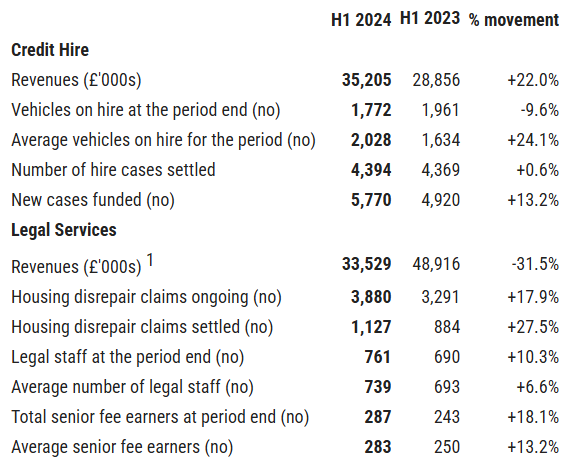

Anexo (LON:ANX)

Flat at 65p - Trading Update - Mark - RED

This stock regularly comes up on some of my bargain screens as it trades at a discount to its Net Current Asset Value. Today, they confirm they are trading in line:

The Group is pleased to announce that trading in FY2024 was in line with the Board's expectations.

So, what could possibly go wrong? Well, lots as it happens. To my mind, this is a terrible business model. They appear to be billing “customers” who simply don’t want their services, or at least to pay for them. So they don’t pay or at least delay payment as long as possible. Hence, the booked revenue stacks up on the balance sheet as huge receivables:

At the half year, this reresepents 1.7x TTM revenues or 632 days on average to get paid. These receivables are funded by around £55m of net bank borrowings. It was this dynamic that caused similar businesses, such as Accident Exchange, to fail.

In today’s update, they are keen to point out that:

Housing Disrepair and serious injury work continue to make an increasing contribution to the Group's overall performance against the backdrop of a solid performance across all Group divisions.

But the H1 revenue breakdown shows an increasing reliance on credit hire:

The update also includes details of a refinancing. They say that “The new agreements have resulted in significant savings in interest costs throughout the lifetime of the facilities.” However, the upfront costs of doing so come to a not insignificant amount of £2m.

Mark’s view

In my opinion, this is such a poor business model that it makes it completely uninvestable for me. Paul agreed and rated it RED. I see nothing in this update that causes me to change that view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.