Good morning!

On Friday afternoon we published The Week Ahead including the economic calendar and the company reporting schedule for this week.

Today's Agenda is now complete.

1.30pm: out of time for today, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

HgCapital Trust (LON:HGT) (£2.42bn) | Annual Financial Report | Software-focused private equity trust. 10.4% NAVps growth. 13% discount moves to 2% premium. | |

Renewables Infrastructure (LON:TRIG) (£1.8bn) | Completion of German Offshore Wind Sell Down | Sold 15.2% stake in Gode One at 9% above book. €100m received & used to reduce RCF to £228m. | |

GlobalData (LON:DATA) (£1.49bn) | Full Year Results | Results in line. Underlying rev growth 4%. PBT +32% (£54.9m). “Robust” outlook, high visibility. | AMBER (Graham) This is likely to be a high-quality business with strong prospects but that's reflected in an already-high valuation. The accounts are complex and may remain so as management focus on their M&A strategy. I'd like to be more positive but am most comfortable with a neutral stance at this time. |

Clarkson (LON:CKN) (£1.36bn) | Preliminary Results | Adj. PBT +6% to £115m. Adj. net cash £216m. Outlook: markets have softened. Market uncertainty. | AMBER (Roland holds) Today’s record 2024 results contrast with a more subdued outlook that has seen broker Panmure cut its estimates for 2025 and 2026. Uncertain prospects for the year ahead mean I’m taking a neutral view now, but I expect Clarkson’s market leadership and proven ability to navigate market cycles to endure over time. |

Assura (LON:AGR) (£1.3bn) | Possible cash offer | KKR has increased its possible cash offer to 49.4p per share, equivalent to 100% of 30/9 NAV. | PINK (Graham) Well done to the Assura board for holding out until they received a bid at tangible NAV or higher. They were also offered the chance to merge with Primary Health Properties (LON:PHP, underlining the attractiveness of their portfolio. Over to KKR now to firm up their bid, and then Assura shareholders can decide if they wish to cash out. |

Alliance Pharma (LON:APH) (£338m) | Final increased recommended cash offer | The buyers have made a final cash offer of 64.75p per share, recommended by the board. | PINK (Roland) [no section below] Today’s improved and final cash offer from buyer DBAY is a 3.6% increase on the 62.5p recommended to shareholders on 10 Jan 25. This increase is the result of “feedback from Alliance shareholders”. We aren’t told explicitly, but one key shareholder may have been Slater Investments (13.6% holding). Slater has now provided a letter of intent to vote in favour of this scheme – my inference from this is that Slater may have refused to support the previous offer. This deal now looks almost certain to complete, in my view. |

Capital (LON:CAPD) (£151m) | Company Update | FY24 to include Mali provisions, PAT now exp $18-20m. FY25 rev exp $300-$320m vs FY24 $348m. | AMBER (Roland) |

| Zotefoams (LON:ZTF) (£132m) | Strategic Investment in Asia | Investing £26m in a new athletic footwear factory in Vietnam + innovation centre in S. Korea. | GREEN (Graham) A new manufacturing facility in Vietnam will be used exclusively to supply Nike for the next few years. Customer concentration risk is likely to be the main issue for investors to worry about but aside from that I like the value on offer here at an adjusted PER of about 9x. |

| NWF (LON:NWF) (£86m) | Acquisition | Acquired Northern Fuels £8.3m, adding 6% to fuel volumes. Priced at 13.8x EBITDA. | |

Mincon (LON:MCON) (£71m) | Final Results | Rev -8%, operating profit -38% (continuing operations). Increased H2 activity continued in early 2025. | AMBER (Graham) Switching back to a neutral stance despite the company potentially making it through some tough trading conditions into a brighter period of activity. I'm a little worried by the mention of competition impacting margins, and it does carry a small amount of debt. So I prefer to return to a neutral stance for now. |

Graham's Section

Zotefoams (LON:ZTF)

Down 2% to 264p (£133m) - Strategic Investment in Asia - Graham - GREEN

Zotefoams, a world leader in supercritical foams, is pleased to announce its plans to expand its international footprint through the establishment of new, purpose-built manufacturing and innovation facilities in Vietnam and South Korea, respectively.

It’s a significant piece of news from Zotefoams, as they announce a £26m expenditure on these new manufacturing and innovation facilities.

The funds will be spent over the next three years, “funded entirely from existing facilities and within the Group's target leverage levels”.

They believe that they need to be located close to customers’ (especially Nike’s) supply chains:

Being able to manufacture locally, in addition to existing production in the UK, brings a number of clear benefits to the Group including strengthened customer relationships, lower production and transport costs, and significantly improved sustainability metrics.

The manufacturing facility will be in Vietnam while there will also be “a small purpose-built footwear innovation centre” in South Korea.

CEO comment:

This investment in Asia marks a pivotal moment for Zotefoams, positioning us at the heart of the global athletic footwear ecosystem. By establishing manufacturing in Vietnam and innovation capability in South Korea, we are transforming our ability to serve this market with greater speed and innovation. Our new 3D parts manufacturing will significantly reduce production waste, while our proximity to key hubs will accelerate development cycles. Our strong partnership with Nike provides the foundation for growth across its running portfolio and into additional footwear categories.

Estimates

Thanks to Singers for publishing a note today. They note that Zotefoams’ Nike partnership resulted in £65m of Footwear revenues in FY24 - approaching half of the company’s entire revenues.

They also note that under current arrangements, Zotefoams manufactures foam for shoes in Croydon and then ships this foam to Nike’s manufacturers in Vietnam.

For now, their estimates are unchanged and include revenues of £149.8m (only slightly higher than 2024’s £148m) and adj. PBT of £20.3m for FY December 2025 (2024: adj. PBT £15.6m).

Graham’s view

The main risk here is likely to be customer concentration risk, as Zotefoams is increasingly devoted to a single customer (Nike).

That risk aside, I think we like the investment case here.

The shares have been in a downtrend since the middle of last year:

Putting the shares on a modest earnings multiple:

Financial risk doesn’t seem to be an issue, as the leverage multiple is not expected to exceed 1.2x. If it peaks there and then returns below 1x then it shouldn’t be a problem.

I think I’ll leave our GREEN stance unchanged, on valuation grounds.

Where is fair value - perhaps around a PER of 15x?

I don’t think that Zotefoams should ever have a valuation that resembles the likes of consumer brand owners such as Nike ($NKE), which trades at in excess of 30x earnings.

But equally, I don’t think that Zotefoams’ foam materials should be treated like commodities - many of them have been patented, and creating them requires the application of advanced technology. Plans for new 3d manufacturing techniques will open up a fresh wave of possibilities.

So I’m comfortable with our GREEN stance. It’s not a stock in which I hold enormous conviction but based on the facts as they are presented to me today, I think the present valuation could be unreasonably low.

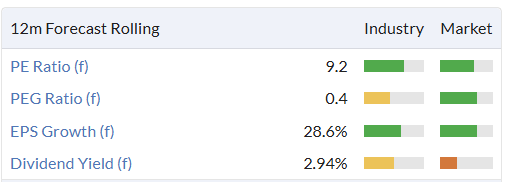

GlobalData (LON:DATA)

Down 1% to 181p (£1.5bn) - Full Year Results - Graham - AMBER

GlobalData Plc (AIM: DATA, GlobalData, the Group), data, insight, and technology company, today publishes its results for the year ended 31 December 2024 (FY24).

These results are in line with expectations.

Rusty in the comments points out that the StockReport shows a forecast for net profit of £65m, while the income statement published today by Globaldata shows net profit for 2024 of only £36.5m.

It’s important to note that the forecasts on the StockReports are typically based on adjusted profit figures, as brokers usually present forecasts on an adjusted basis.

Some of the highlights from today’s results:

Revenue +4.5% to £285.5m

Adjusted PBT +30.6% to £96.1m

Adjusted profit after tax +25% to £68.9m

The adjustments have caused adjusted PAT to come out as nearly double the actual net profit.

So let’s review the adjustments:

Amortisation of acquired intangible assets £9m

Share-based payments £24m

Restructuring and refinancing £5m

Acquisition and integration costs £4m

…plus a variety of smaller items.

As usual, there is no objectively correct way to deal with these adjustments.

My view is that it’s ok to ignore amortisation if you are happy to assume that the company’s intangible assets are already worth zero.

I also think you can ignore acquisition and integration costs if you think the company is adding value with M&A.

However, I do not think that share-based payments should ever be ignored.

I also think that restructuring and refinancing costs can be surprisingly recurring in nature, and therefore should not be adjusted out.

In passing, I will note that GlobalData’s aggregate adjustments have increased from £32m in 2023 to £41m in 2024.

Share-based payments have increased from £19m to £24m.

Restructuring and refinancing costs have increased from nearly £2m to over £5m.

Given the size of all of the adjustments, relative to the Group’s profitability, I will rate these results as highly unclean.

CEO comment

2024 was transformational for GlobalData following Inflexion's significant investment in June 2024, which strengthened our balance sheet and accelerated our growth strategy…

Strategic M&A remains a core element of our growth strategy, with four earning accretive acquisitions completed during the year... With much of the foundational work to re-organise the business and set us up for accelerated growth now completed, we enter 2025 with clear priorities and a strengthened team to deliver. With strong revenue visibility, a clear transformation roadmap, and the financial capacity to execute, we're confidently progressing toward our target of £500m annualised revenue by 2026.

Inflexion is a mid-market private equity firm that invested over £400m in Globaldata’s largest business, its Healthcare division.

Globaldata is still the majority owner of this division but Inflexion now has 60%. The division was valued at £1.1 billion according to the terms of the deal.

Globaldata’s cash position has been transformed from net debt of £244m (Dec 2023) to net cash of £10m (Dec 2024).

Dividend: GlobalData’s strategy has changed to focus more capital on M&A, so dividends have been cut. The total dividend for 2024 is proposed to be just 2.5p (2023: 4.6p).

Outlook: there is a “robust” outlook, with high levels of revenue visibility. As noted by the CEO above, they are seeking annualised revenue of £500m by the end of 2026, “through a combination of high single to double-digit organic revenue growth and M&A”. They are also targeting a 45% adj. EBITDA margin.

For 2024, underlying revenue growth is reported at only 4% - below target.

Adj. EBITDA margin was unchanged at 41%, within reach of their target.

Forward estimates: PanLib are forecasting 5.1% LfL growth for 2025 and 5.8% for 2026. This doesn’t scream to me that they are hitting high single digit organic revenue growth any time soon, but I guess they might not be too far away.

Some FX headwinds have resulted in cuts to forecasts but that’s beyond the company’s control.

Graham’s view

This type of “intelligence” business can be difficult to grasp from the outside, but it can also be a solid investment.

I am going to dock Globaldata a few points due to the complexity of its accounts, and I can’t ignore the very large share-based payments included within the adjustments.

I also note a high earnings multiple - and remember that this earnings multiple is based on its adjusted earnings forecasts. So it’s more expensive than this based on actual earnings.

While this does seem very expensive, the involvement of private equity with Globaldata’s healthcare business shows that very high valuations are possible when it comes to buyouts in this industry. High ratings are possible due to the very specialist services they provide and the large, blue-chip clients they attract.

At one stage in my career I worked for a division of Informa (LON:INF). Informa is arguably a competitor to GlobalData and also a related company as there is a history of transactions between them, although Informa is quite a lot bigger (£10bn market cap vs. £1.5 billion for GlobalData).

On balance today I’m going to be neutral on GlobalData, due to its high earnings multiple and the complexity of its accounts. I’d certainly be open to taking a more positive stance in future - let’s see how its kickstarted M&A strategy plays out.

Assura (LON:AGR)

Up 14% to 46.5p (£1.5bn) - Possible Cash Offer - Graham - PINK

Last month, there was some controversy in these pages around whether or not REITs should accept takeover offers below tangible NAV. I took the view that in general, boards should try to achieve a disposal price of tangible NAV or higher. Ken Mitchell pointed out that takeovers below NAV were sometimes fair.

See the reports of 17th Feb and 18th Feb.

We know that KKR made four previous proposals to healthcare REIT Assura. The last one was at 48p per share, vs. net tangible asset value of 49.4p (Sep 2024 valuation).

Today we learn that KKR has come up with a 49.4p possible cash offer, i.e. they are in fact willing to pay 100% of official asset value.

It’s a joint offer with an American infrastructure and real estate investment firm, Stonepeak.

The Board of Assura is now minded to recommend this offer to Assura shareholders, should a firm offer be made at this price.

But the news doesn’t stop there. We also learn of a proposed combination:

The Board confirms that it has also received an indicative, non-binding proposal from Primary Health Properties PLC ("PHP") regarding a possible all-share combination of Assura and PHP structured by way of an offer by PHP for Assura at an exchange ratio based on each company's last reported NTA per share (the "PHP Proposal"). The implied value of the PHP Proposal based on PHP's share price of 90.1 pence as at 13 February 2025 is 43 pence per Assura share. The Board has carefully considered the PHP Proposal with its advisers and concluded that the Possible Cash Offer is more attractive than the PHP Proposal as it provides shareholders with the opportunity to receive cash consideration at a significantly higher value per share than the proposal from PHP and with materially less risk. Therefore, the Board has rejected the PHP Proposal.

So Assura has been offered a wealth of options: a merger, a cash takeover, or going it alone. I think this only helps to underline the attractiveness of their portfolio.

Graham’s view

I approve of the Assura board’s strategy: they held out for a bid at tangible NAV or higher from KKR, which I think was justified in this case. GP surgeries, primary care centres and treatment centres are an excellent category of long-term tenants, in my view.

And it’s a minor point, but the REIT’s Sep 2024 NAV is six months old now. The balance sheet might have appreciated a little since then! So at 49.4p per share, the buyers might still enjoy a small discount, in reality.

It’s now over to KKR to make a firm offer at the price mentioned today, and then for Assura shareholders to decide if they wish to proceed. In the current environment, I imagine that many Assura shareholders will be happy to take the money and reinvest the proceeds in other REITs that are still trading far below NAV.

Mincon (LON:MCON)

Up 3% to 36.9p (£73m / €87) - Final Results - Graham - AMBER

I turned AMBER/GREEN on this last year, at 44.85p.

Unfortunately this was premature, as Mincon’s share price has remained subdued:

Weak demand from the mining industry for Mincon’s drilling equipment has been the theme, which I hoped might have bottomed out already.

Here are the highlights from today’s results, focusing on continuing operations only. Operational leverage has worked in reverse and resulted in a major step backwards in profitability.

Revenue down 8% to €146m (mining revenue down 7%)

EBITDA down 24% to €40m

Profit down 55% to €3.4m

Worryingly, the company mentions that “increased market competition and some price reduction in H1 2024 impacted gross margin”.

But also, “market conditions improved in H2 2024. This combined with operational restructuring led to a recovery in EBITDA in H2 2024”.

Checking the half-yearly report, I see H1 EBITDA was only €17.4m. So there was about €23m in H2, give or take the contribution from discontinued operations.

Dividend: unchanged at 2.1 cents for the year. Please note that this is not covered by earnings.

Greenhammer. This drilling system has been in the works for years. Is it finally going to transform the fortunes of the company? Here’s the update.

Mincon continues to focus on transformative opportunities like the Greenhammer collaboration. During 2024 there has been an extensive review of the test results with the Group's rig manufacturer partner. This has led to the refinement of the rig conversion design to more efficiently make use of available power to increase drilling output. The Group is in the process of finalising a 24/7 contract with a major copper mining company in Arizona who provided the test site in 2024. Mincon remains confident in the transformational revenue benefits of the system for the Group and its rig manufacturer partners, as well as the cost reduction opportunities for large mining customers.

The CEO comment notes the improvement in H2 2024 as activity increased, and says that this has continued into early 2025.

Broker note: Shore Capital says that these results are in line with their expectations and they believe that Mincon is now “past trough trading conditions”, with an improving outlook.

However, I note that their 2025 forecasts have reduced since October. For example, their new adj. PBT forecast for 2025 is €7.5m (previously €10.4m).

Roughly speaking, it looks like their recovery expectations have been pushed back by a year, as their 2026 expectations are now similar to what their 2025 expectations used to be.

Graham’s view

I’m not sure if I should retreat back to AMBER. The company hasn’t recovered as quickly as I hoped it would, a year ago. There is also the worry about competition - is this going to be a major problem going forward?

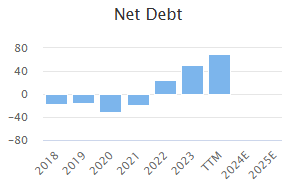

To help me decide, I’ll let the balance sheet guide me. Net debt is reported at €44m as of Dec 2024, but they’ve used total liabilities to calculate this which is a far more pessimistic calculation than most companies use.

Excluding leases, I think net debt is c. €23m.

That provides a leverage multiple of less than 1x and should not cause much stress. However, since the company is in debt, I’d prefer to be neutral on it at this time.

Roland's Section

Capital (LON:CAPD)

Down 20% to 61p (£120m) - Company Update - Roland - AMBER

Capital (LSE: CAPD), a leading mining services company, today provides an update on anticipated profitability for FY 2024, the outlook for 2025 and news of management changes.

Today’s update from Capital appears to contain more bad news for shareholders, following January’s revenue warning.

2024 profits will now include impairment charges relating to the group’s operations in Mali.

2025 revenue expectations appear to have been cut, and the CEO has fallen on his sword.

Let’s take a look.

Trading Update for FY24: Capital’s previous update highlighted an “adverse impact” on profitability driven by startup costs for its US operations.

Today we have news of an impairment charge relating to its operations in Mali, historically an important market for the company:

… the Board has taken the decision to book non-cash provisions in 2024 primarily relating to historical VAT receivables and various laboratory assets in Mali.

As a result of these provisions, Capital expects to report net profit after tax for 2024 of $18m to $20m.

Stockopedia shows a consensus net profit estimate of $14.4m for 2024, so there appears to be a mismatch in how the data is being presented here. I think it’s reasonable to conclude that Capital’s previous expectation for net profit after tax was above $20m.

I think today’s update may be a profit warning - unfortunately I can’t access any broker notes this morning to confirm this.

Revenue Outlook for FY24: the bad news continues. Capital now expects to generate revenue of $300m to $320m in 2025.

Here, we do have a clear comparison with forecasts, with Stockopedia’s data suggesting a previous consensus figure of $345m:

The company says revenues will be H2 weighted due to the ramp up of new projects, with margins also weighted to H2. Does this leave the door open for another downgrade later this year? I suspect it’s a risk.

Some comments on operational plans for 2025:

Drilling business: main focus will be on “core profitability”, particularly in USA – this seems to suggest profitability in the group’s core business may currently be lower than hoped for;

Mining revenue will be down due to conclusion of two large projects, Reko Diq project expected to ramp up through year;

MSALABS is expected to generate $50 to $60m of revenue (vs $43.6m in 2024). The company is consolidating its assay lab operations to improve profitability. This includes opening a “state-of-the-art” lab at Nevada Gold Mines that will “add wet chemistry and multi-element capabilities from 2026”. Management continues to believe MSALABS can achieve revenue of $80m over time.

CEO departure: chief executive Peter Stokes has resigned and will leave after a “brief transitional period”. He is thanked by executive chairman Jamie Boyton, who will be taking full control of the business again.

Mr Boyton is a 10.5% shareholder and ran Capital prior to Stokes’ appointment in 2022. So this change of management could be a positive development:

Boyton’s commentary suggests 2025 could be difficult year, prior to a recovery from 2026 onwards (my emphasis):

We remain positive about the outlook for the business however we continue to face pressures to profitability, particularly driven by our operations in the USA. We do however expect margins to bottom in H1 2025 and expect a resumption of revenue growth in 2026 along with a recovery in margins.

Roland’s view

Capital says it will provide a more comprehensive update on the business with its 2024 results, due on 27 March.

With no guidance on expected profitability for 2025, it’s hard to form a view on valuation.

I would also note that debt levels have risen sharply since Stokes took charge in 2022 (whether coincidentally or not). The company had previously maintained a net cash position:

However, my feeling is that Jamie Boyton’s return to full-time executive leadership at Capital is probably a good thing.

My sums also suggest that unless this business is really coming unravelled – which I see no reason to believe – then the shares could be starting to offer some value.

The company’s net profit figures can be distorted by gains and losses on its investment portfolio, so I prefer to rely on operating profit as a measure of underlying business performance:

The lowest operating margin reported since 2018 is 12.8%

Applying this to the mid-point of today’s 2025 revenue guidance suggests FY25 op profit of c.£31m

This gives Capital shares a possible EBIT/EV yield of 14% – potentially good value

I would emphasise that in my opinion, there’s still considerable uncertainty about the outlook for 2025.

The old stock market adage is that profit warnings tend to come in threes. Our research has found that companies which downgrade expectations often do underperform for a while.

While neither January’s update nor today’s have explicitly cut profit guidance, my view is that they can both be considered profit warnings:

On balance, I’m going to maintain my neutral view ahead of this month’s results. AMBER.

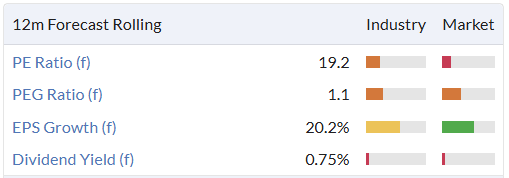

Clarkson (LON:CKN)

Down 17% to £36.65p (£1.13bn) - Preliminary Results - Roland - AMBER

At the time of publication, Roland holds a long position in CKN.

FTSE 250 firm Clarkson describes itself as “the world’s leading provider of integrated shipping services”. At its core, it’s one of the world’s leading shipping brokers, with a history stretching back to 1852.

Today’s results are in line with January’s upgraded expectations and showcase a record adjusted pre-tax profit of £115m, up 6% on 2023.

However, Clarkson’s share price has fallen sharply this morning, due to the company’s warning that market conditions are likely to be less favourable in 2025.

CEO Andi Case warns that a wide range of geopolitical factors are contributing to a softer outlook for the current year (my emphasis):

2025 has started with more uncertainty than most due to political change, ongoing regional conflicts, increased trade tensions, tariffs and sanctions, inflation and changing monetary policy across global economies. As I write this report, the impact of these uncertainties is that freight rates and asset values have broadly fallen, which has meant that the value of spot business done to date is less than the same period last year.

2024 results highlights: Clarkson’s 2024 numbers highlight the company’s ability to generate attractive profitability and plenty of cash.

Adjustments to reported profits are also minimal - these are quite clean accounts:

Revenue up 3.4% to £661.4m

Underlying pre-tax profit up 6% to £115.3m

Reported pre-tax profit up 3% to £112.1m

Underlying earnings per share up 4.3% to 286.9p

Dividend up 7% to 109p - 22nd consecutive year of increase

Splitting out these results across the company’s four operating segments gives us more of an idea of the scale and profitability of Clarkson’s different markets:

Broking (23% margin): rev up 2.4% to £529.3m, profit up 1.2% to £122.6m;

Financial services (12.2% margin): rev down 3.4% to £42.6m, profit down 21% to £5.2m

Support (e.g. port services)(11.8% margin): rev up 14.8% to £65m, profit up 20% to £7.7m

Research/data/software (38.8% margin): rev up 11.8% to £24.5m, profit up 13% to £9.5m

The company generates the lion’s share of revenue and profit from its broking business. However, the others are all attractive profit centres in their own right and help support the breadth and depth of Clarkson’s client offering.

Broking: Clarkson’s forward order book stood at $231m at the end of 2024, up modestly from $217m at the end of 2023. This relates to ongoing time charters and shipbuilding orders.

The diversion of shipping away from the Suez Canal last year caused an increase in tonne miles. This supported higher charter rates as the longer journeys involved had the effect of tightening available capacity.

The transition to alternative fuels and more efficient technology is said to be driving fleet renewal shipbuilding orders. Clarkson says half of all tonnage ordered last year involved alternative fuel.

On the downside, the large “shadow fleet” of tankers and other ships controlled by Russia appears to be having an impact on demand and hampering clients’ ability to make long-term plans. Clarkson expects this capacity to be released back into the mainstream market at some time, but I don’t think there’s much visibility or certainty on this yet.

Profitability & Balance Sheet: today’s results highlight an operating margin of 14.9% (2023: 15.6%) and a return on equity of 17.4%, both on a statutory basis. These may not be quite in the top tier of profitability, but they’re comfortably above average for the UK market and consistent with Clarkson’s long-term performance:

My sums also suggest free cash flow of £106m, representing 122% conversion from net profit. This was helped by almost £15m of interest received on the group’s c.£400m cash balance last year. Excluding this, FCF conversion was almost exactly 100%.

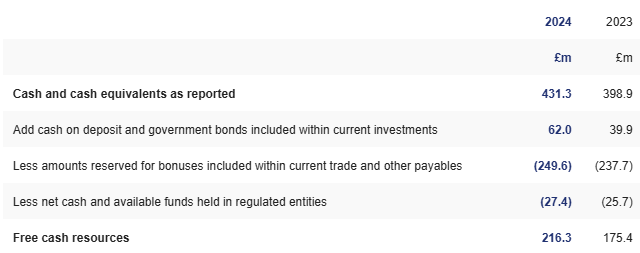

A strong cash performance contributed to Clarkson’s improved year-end net cash position of £216.3m (2023: £175.4m) – this figure excludes cash ear-marked for employee bonuses, which are significant:

For context, Clarkson accrued £32.4m for future bonus accrual last year – about 33% of operating profit. I understand some investors think this is excessive, but in my view this is just the business model – broking is a sales-driven, relationship business.

Generous bonus payments have not prevented Clarkson delivering attractive shareholder returns over a long period – I estimate shareholders have received a 10% annualised total return over the last 20 years.

Outlook: CEO Andi Case suggests that the current level of uncertainty means that 2025 results could be weighted to the second half of the year:

The invoicing profile of this FOB, together with the expected uptick in spot revenues following a slow start to the year, means that 2025 is expected to be second-half weighted, as it has been in most years.

Clarkson hasn’t provided any specific financial guidance today, but an updated broker note is available on Research Tree, with thanks to Panmure Liberum.

Panmure’s analysts have cut their estimates slightly to reflect the uncertain outlook:

2025E EPS -6% to 262.8p (previously 279.3p)

2026E EPS -5% to 274.4p (previously 288.0p)

Based on 2024 underlying EPS of 286.9p, these forecasts imply that earnings are expected to fall by 8.4% in 2025 and remain below 2024 levels in 2026.

This estimate prices Clarkson on a 2025E P/E of 14 after this morning’s decline.

The 2024 dividend of 109p gives the stock a trailing yield of 3%.

Roland’s view

Shipping is intensely cyclical and an investment in this sector does require good timing to maximise returns. Clarkson’s long-term share price history reflects this:

I see this business as similar in its quality and nature to FTSE 250 real estate group Savills.

Yes - Clarkson’s is a service business that’s dependent on fee earners who walk out the door each night.

However, it’s a sector leader with more than 150 years of experience, a strong franchise and an impressive data archive to support its research and software offerings. I think these advantages are likely to endure.

Does today’s price slump provide an attractive entry point? Perhaps, on a longer-term view.

However, given today’s cut to profit guidance and the varied nature of the headwinds facing the business, I think further weakness is possible this year, so I’m more comfortable taking a neutral for now. Graham went AMBER/RED in January – I am going to move up one notch to AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.