Good morning! Lots of results announcements today - the Agenda is now complete.

1pm: that's all for today, thank you.

Motor Finance Review

Breaking news: the FCA have published a helpful RNS to clarify their progress when it comes to the motor finance review.

It was back in January 2024 when the FCA said they were going to undertake work in the motor finance market, to review discretionary commission arrangements. This has caused a great deal of uncertainty in the market as investors have no idea what sort of compensation scheme, if any, might be enacted.

This has been combined with activity in the courts which have found that car dealerships, acting as brokers, have a fiduciary duty to customers, which would imply the need to provide extra levels of disclosure around commissions, with the potential for yet another compensation scheme.

The result has been investor flight from the sector.

The FCA has now weighed in with an attempt to clarify its thinking:

We want to provide as much certainty as possible to firms, consumers and stakeholders. So, we are confirming that if, taking into account the Supreme Court's decision, we conclude motor finance customers have lost out from widespread failings by firms, then it's likely we will consult on an industry-wide redress scheme. We previously said it is more likely than when we started our review that we will introduce an alternative way of dealing with complaints...

A redress scheme would be simpler for consumers than bringing a complaint. We would expect fewer consumers to rely on a claims management company, meaning they would keep all of any compensation they receive. It would also be more orderly and efficient for firms than a complaint led approach, contributing to a well-functioning market in the future.

Next steps: the FCA will confirm within six weeks of the Supreme Court's decision if they are proposing a redress scheme.

They also note that Supreme Court case covers both discretionary and non-discretionary commissions, and "our next steps on non-DCA complaints will also be informed by the outcome of the Supreme Court case".

Graham's view

This announcement is better than nothing - it's always better to have some degree of certainty, rather than total uncertainty. However, I don't view it as good news for the sector. We still don't know how large the payments under a redress scheme might be, and a redress scheme seems to be increasingly likely.

Also, we can now see how the FCA's work is going to interact with the findings of the Supreme Court. If the Supreme Court finds that greater levels of disclosure were required in the first place, this seems likely to empower the FCA to create a bigger redress scheme.

On top of that, the FCA are now talking about taking "steps" when it comes to non-discretionary commissions. I previously thought the FCA was going to take no action when it came to non-discretionary commissions. But if the Supreme Court finds that these commissions should have had additional disclosures too, then the FCA might take action.

Overall, then, I do view this announcement as negative for the industry. At least we are inching closer towards a conclusion!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Spirax (LON:SPX) (£5.2bn) | Full Year Results | Organic rev +4% to £1,665m, PBT +6% to £259m. 2025 rev outlook similar, w/ margin progress. | |

Persimmon (LON:PSN) (£3.8bn) | Full Year Results | Comps +7% to 10,664, rev +16% to £3.2bn. PBT +2% to £359m. Outlook +ve, fwd sales +27% | |

Jet2 (LON:JET2) (£2.8bn) | Repurchase of convertible bonds | Invites all holders of its convertible bonds (£304m outstanding) to sell back to JET2 at premium to par. | |

Rotork (LON:ROR) (£2.7bn) | Full Year Results | Comps +7% to 10,664, rev +16% to £3.2bn. PBT +2% to £359m. Outlook +ve, fwd sales +27% | |

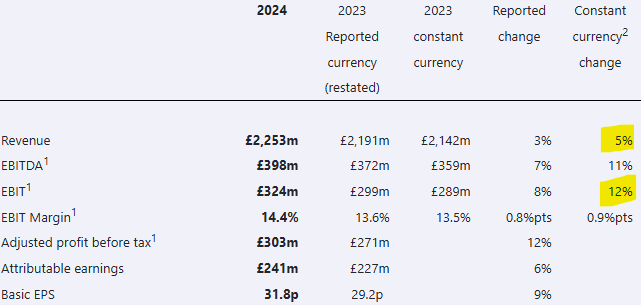

TP Icap (LON:TCAP) (£2.0bn) | Final Results | Rev +3%, EBIT +89% to £236m. Adj EPS +9% to 31.8p. Mgt is comfortable w/ FY25 mkt exps. | GREEN (Graham) This is a "Super Stock" with some very nice qualitative features including a long history of success and leading market share at a number of its business units. A forthcoming US IPO of one of these units may provide a short-term catalyst. Shares trade at a PER of just 8x. |

Domino's Pizza (LON:DOM) (£1.2bn) | Full Year Results | FY24 Sys sales +2%, rev -0.4%. Adj PBT +8.4%. Exp FY25 EBITDA to be in line with exps. | |

TI Fluid Systems (LON:TIFS) (£976m) | Full Year Results | Rev -3.5%, adj EBIT +1.9%. Volumes lower due to EVs. 2024 bookings €2.7bn (2023: €3bn). | PINK (under offer) |

Supermarket Income REIT (LON:SUPR) (£906m) | Interim Results | Ann.rent +13%, adj EPS +3% to 3.0p. Div +1% to 3.1p. NAVps +1% to 88p. Cost savings underway. | AMBER/GREEN (Roland holds) Today’s numbers are in line and suggest portfolio valuations remain realistic. Efforts to cut costs are sensible and proactive and should help offset rising debt costs. With an 8% yield and 17% discount to NAV, I think SUPR is attractive for income and is probably trading slightly below fair value. |

Genuit (LON:GEN) (£897m) | Final Results | Rev -4.3%, PBT -4.3%. 2024 “challenging”. Outlook improving, ‘25 started in line with mgt exps. | |

Kier (LON:KIE) (£634m) | Results for HY25 | Rev +5%, PBT +6%. Avg monthly debt reduced, order book +2% to £11bn. H2 in line with exps so far. | |

Craneware (LON:CRW) (£616m) | Interim Results | Rev +10%, adj PBT +21%. Positive H2 trading, Board expects FY results in line with mkt exps. | |

Nichols (LON:NICL) (£479m) | Preliminary Results | Rev +1.2% to £173m, adj PBT +15.6% to £31.4m. Further improv. in FY25, trading in line with exps. | GREEN (Graham) [no section below] See our coverage of the full-year trading update in January. Today's results show a modest (1%) increase in revenues but a 15.6% increase in adj. PBT. My positivity on this stock has been based on the idea that its profit margins can recover, and I'm pleased to see more evidence of this. Adj. ROCE moves from 26% to 31%. My main disappointment is that £7.4m of costs have been classified as "exceptional" (replacing operational and IT systems). But a report from Singers today says that FY24 EPS is 4% ahead of their estimate. They go on to upgrade FY25 EPS by 5% (67.6p) and FY26 EPS by 4% (72p). This stock is not cheap at a PER of about 19x but the bull thesis is playing out. QualityRank 98 with net cash £54m. |

Ferrexpo (LON:FXPO) (£418m) | Final Results | More time is needed to finalise 2024 results, due to Ferrexpo Poltava Mining legal situation. | |

Boohoo (LON:BOO) (£382m) | TU | Rebranding to Debenhams. FY25 rev -16% to £1.2bn. Exp FY25 adj EBITDA of c.£40m. CFO replaced. | RED (Megan) There is a lot of wishful thinking in this slightly dubious update from the company which will henceforth be known as Debenhams. But not enough substance to make me at all tempted. |

Care REIT (LON:CRT) (£337m) | Recommended cash acquisition at 108p | Acq by CareTrust REIT (NYSE) values CRT at £448m, vs EPRA NAV of £492m/119p (Sept 24). | PINK (Roland) |

Costain (LON:COST) (£280m) | Results for Year ended Dec 2024 | Rev -6.1%, adj op profit +7.5% at upper end of exps. Record fwd work of £5.4bn (+£1.5bn). | GREEN (Roland) This infrastructure construction specialist reports improved profitability, good cash generation and a strengthened pipeline of work. I don’t see any reason to change our positive stance at this time. |

Synthomer (LON:SYNT) (£227m) | Final Results | Trading in line (muted start to 2025). Confident of earnings progress, +ve FCF, deleveraging. | |

Somero Enterprises (LON:SOM) (£153m) | Final Results | Rev -9.5%, adj. EBITDA -24.1%. In line. Challenging conditions to continue to some extent. | AMBER (Megan) Continued economic uncertainty has dented the normally phenomenally high quality metrics. It’s an interesting cyclical play or potentially a takeover target, but it’s not yet cheap enough to tempt me. |

Solid State (LON:SOLI) (£99m) | $25m order for FY26 | Order for comms equipment. Was expected in FY24/25, delayed by change in UK govt. | |

Headlam (LON:HEAD) (£89m) | Full Year Results | 2024: rev down, EBITDA loss. Outlook: rev -6% in Jan/Feb 2025. Timing/pace of recovery uncertain. | |

STV (LON:STVG) (£84m) | Full Year Results | Rev +12%, adj. op profit +3%. 2024 “good year”. Outlook: macro backdrop will impact budgets. | SP down 6%. |

Facilities by ADF (LON:ADF) (£30m) | TU | PW. 2024 rev “broadly flat”. 2025 is subdued, rev and profitability to be materially below exps. | BLACK (AMBER/RED) (Graham) This might be trading at or around book value now, but I no longer have conviction that it's worth more than book. Insiders cashed out at 50p and trading has been awful since then. No material profits are expected in 2025 after today's profit warning. This company is too unlucky for my taste. |

Aptamer (LON:APTA) (£7m) | Interim Results | Revenue £0.7m, adj. EBITDA loss £1.1m, cash £2m. Material uncertainty re: going concern. | RED (Graham) [no section below] |

Graham's Section

TP Icap (LON:TCAP)

Down 2% to 254.5p (£1.92bn) - Final Results - Graham - GREEN

This is a large inter-dealer broker previously known as “Collins Stewart Tullett” and then as “Tullell Prebon”. Terry Smith, the fund manager, was Chief Executive until 2014.

Today’s results are positive: 5% revenue growth and 12% adjusted EBIT growth (using constant exchange rates), with profit margins growing:

CEO comment

"We delivered record profits in 2024… All divisions traded well… underlining the power of our diversified business, and the continued delivery of our strategy."

Dividends/buybacks: the final dividend is proposed to be 11.3p (last year: 10p) with a full-year dividend of 16.1p (last year: 14.8p).

The shares offer a useful yield:

The company also offers its fourth £30m buyback in 18 months.

The leverage ratio is 1.6x which in normal circumstances is not a worry. In fact, TP ICAP’s definition of “leverage ratio” uses total debt, rather than net debt. It doesn’t have a net debt position - it has net funds of £254m as of Dec 2024.

Parameta Solutions

This is their market data business. It's preparing for an IPO in the United States, with TP ICAP retaining a majority stake. Other options for it are still possible.

I like the rationale for this potential IPO as it pertains to TP ICAP shareholders, who it seems are likely to continue being showered in cash by the company:

Establishing baseline value of the business for TP ICAP shareholders;

Would expect to return most of the proceeds of any Parameta listing to our shareholders;

Majority of future potential value upside would indirectly accrue to TP ICAP shareholders;

Underpins close relationship with Group's broking businesses, through exclusive, long-term agreements, providing an annual income stream for TP ICAP.

Outlook

ICAP might serve much larger customers than the likes of IG group (LON:IGG) (in which I have a long position) and other trading platforms, but they all share one thing in common: volatility is good news.

Geopolitical tension, and the uncertain outlook for trade policies, inflation, as well as interest rate movements, should continue to drive volatility that is supportive for our business.

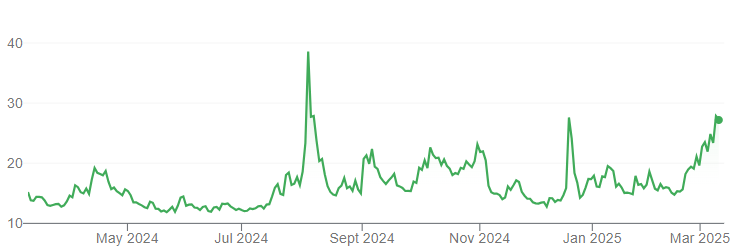

As noted in today's comment thread, volatility has been picking up recently, although it’s still within what I’d consider a “normal” range:

TP ICAP notes that the GBPUSD exchange rate will continue to impact results (they report in pounds and have costs largely denominated in pounds, but earn 60% of their revenues in US dollars).

They are “comfortable with current 2025 market expectations for adjusted EBIT”.

I believe that market expectations are for adjusted EBIT of c. £332m (vs. £324m in 2024). With such a modest rate of revenue growth pencilled in and with volatility on the rise, perhaps we can reasonably expect an earnings beat against that number? TP ICAP's shares are down 2% this morning, suggesting that some investors may have expected an upgrade already.

Adjustments

The 2024 results are much cleaner than 2023, with much fewer adjustments, resulting in an 89% increase in reported EBIT.

A search through the footnotes shows me the reason: 2023 saw large impairments of intangibles worth nearly £90m, which were absent in 2024.

Graham’s view

I like trading platform businesses with high market share and so it’s natural that I would like TP ICAP!

Parameta is said to have 70% market share of the OTC (over-the-counter) data market, with a recurring revenue business model. Revenue growth in 2024: 8%.

Similarly, TP ICAP’s Liquidnet - a trading network for large institutional investors - is ranked #1 or #2 by market share, depending on the source used. Revenue growth in 2024: 15%.

“Global Broking” is the largest revenue source for TP ICAP, contributing 57% of the total. Growth there was more modest at 4% in 2024.

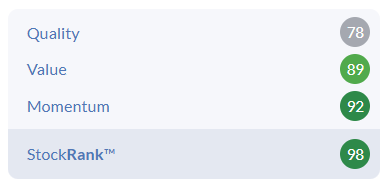

I note that this is classified as a Super Stock by the algorithms:

Value is indicated to me by a PER of just 8x.

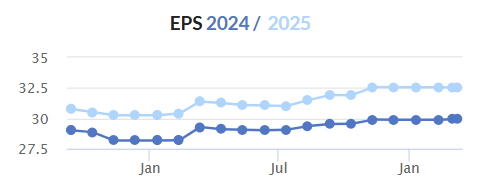

I note that earnings estimates have been sturdy:

Overall, I see a lot to like and very little to dislike. This is a business with which I have some familiarity - it's a very big player in the City, but it has global influence. And I'm surprised it's trading at such a modest valuation. I can therefore wholeheartedly agree with the StockRank and give this a GREEN.

Facilities by ADF (LON:ADF)

Down 27% to 20.5p (£22m) - Trading Update - Graham - AMBER/RED

Relieved to see that I cut my stance on this to neutral last November although perhaps I should have been even more cautious and turned negative after a severe profit warning that saw the revenue forecast for 2024 cut by 28%.

Today we get another profit warning - they do tend to appear like buses.

As you may know, this company hires out trailers to support the production of TV and film content.

Firstly a quick review of 2024, which was in line.

Revenue £35.2m (2023: £34.8m). This includes £2.6m of revenue from an acquisition, so there has been an organic decline. As we’ve discussed here before, the Hollywood strikes by writers and actors in 2023 resulted in less activity in 2024.

Adj. EBITDA £7.2m (2023: £7.3m).

Cash at Dec 2024 is £2.5m, with net debt £13.7m - mostly hire purchase on ADF’s vehicles.

I’m a little surprised to read that they intend to pay a final dividend in line with the prior year. That will be 0.9p, or in pound terms nearly £1m.

Outlook

The outlook section starts well - H1 in line with expectations.

They also say that H2 will see “improved visibility and return to more normal levels of activity”, including various blockbuster films and high-end TV productions.

Unfortunately, this hasn’t translated into good prospects for ADF (emphasis added):

However, FY25 to-date has seen the segments in which the Group operate remain relatively subdued in terms of activity and this, in conjunction with an increasing client focus on project budgets, has resulted in more challenging market conditions. Whilst at this early stage in the year revenue and profitability for FY25 are expected to be materially below current market expectations, the Company still expects to report revenue and profitability for FY25 significantly ahead of FY24.

CEO comment:

A slower than expected return to pre-strike levels of activity, frozen budgets, reduced production spend, and rising costs have all combined to present short-term challenges. However, the long-term market outlook remains favourable for ADF, buoyed by sustained high levels of investment in the UK HETV and Film industry. The Board remains confident in the long-term prospects of the Group as the market returns to more normal levels of activity."

Estimates

Many thanks to Cavendish for publishing a clear update this morning.

They have now slashed their 2025 revenue forecast by another 25%. They had already reduced it by 16% at the time of the November profit warning.

The compound effect is a 37% fall in the 2025 revenue forecast, from £67.3m to £42.3m.

This results in a write-off of the profit forecast, with adj. PBT moving from £7.9m to only £2.1m.

Graham’s view

I still think there is great scope for a recovery here, but it’s not something I’d be willing to bet on.

According to Cavendish, the company is enjoying fleet utilisation of only 55% (in 2024 and forecast for 2025), vs. previous utilisation of 75%. At that percentage it’s no surprise that profits will be slim to none.

If or when utilisation recovers, we can reasonably expect a bounce-back in profitability.

Against that, we need to accept that some companies are just unlucky: vulnerable to unpredictable demand (low visibility) and occasional droughts. ADF is now looking like one of these “unlucky” companies, after a dreadful few years.

The latest bout of bad luck is that certain segments of the TV and film industries have returned to normal levels of activity, but not ADF’s segments.

At some point I think we have to accept that unexplained bad luck is a permanent feature of a company’s performance, and just move on.

I also think it’s reasonable for existing shareholders to have a sour taste in their mouths after the company raised £10m at 50p last August, to help fund the initial cash cost of an acquisition. Simultaneous with that placing, insiders cashed out another £10m at 50p.

I’m going to downgrade my view on this further, to AMBER/RED. This may be harsh but there are no material profits expected in the current year and the balance sheet has little cash to support it. This could still be interesting to those of a highly contrarian nature. At a market cap of around £22m, it might be trading below book value. But at this stage I no longer have a lot of confidence that it’s worth more than book.

Megan's Section

Somero Enterprises (LON:SOM)

Down 6% to 265p (£153m) - Final Results - Megan - AMBER

Challenging market conditions for concrete equipment specialist Somero have been something of a drain in the last few years.

North America (which contributes three quarters of the group’s total sales) hasn’t reported an increase in revenues since 2021 and, in these numbers, has once again been hit by stateside economic gloom. In the year to December 2024, North America sales fell 7% to $82.2m as rising interest rates, labour shortages and concrete rationing meant that customers failed to operate at full capacity.

The far smaller Australian region also suffered quite badly in 2024. After hitting record high revenues in the previous year, sales fell by a third to $6.6m. And even in Europe, where demand for environmentally friendly products is strong, sales were pretty much flat at $14.6m.

The good news is that demand from Somero’s customers remains strong. In the US, there is a rising need for more domestic electric vehicle, battery and chip manufacturing plants thanks to chief sponsor of the US onshoring project, Donald Trump. If stateside companies can weather the economic challenges, they should be in a good position to invest in the coming years. And given Somero’s market-leading position (with an estimated 80% market share), the company should be well placed to benefit from any uptick.

Short-term dent to quality. It is worth noting that some of the quality metrics that normally shine at Somero have been a bit bruised by the ongoing market weakness. Gross margins were slightly lower at 54% as sales fell faster than sales costs. Higher administrative expenses (related to the establishment of the Belgian service centre) hiked operating costs which sent operating margins down to 22% (from 29% last year).

Return on Capital Employed (ROCE), which has averaged 49% in the last five years, thanks to the company’s strong market position, fell to 22% in these numbers.

Operating cash inflows were also materially lower at $17.6m (compared to $24.5m last year), equivalent to an operating cash conversion of 72%. With capital expenditures of $2.4m, the company’s free cash flow didn’t cover the $15.8m of dividend payments.

Rising receivables. It is also worth nothing that despite a decline in total sales, company receivables were higher at $9.3m, compared to $8.8m the previous year. The company is perhaps having to be more generous with the terms on which it sells its products to customers.

Uninspired outlook. Despite an uptick in the second half of 2024, management remains cautious about the outlook for 2025. The overall message is ‘more of the same’ - underlying demand from clients will remain strong, but geopolitical and economic turbulence might hamper the flow of orders. Overall, management is guiding to “moderate” revenue and profit growth in 2025 with “corresponding improvements” in profitability and cash flow.

Megan’s view: I like Somero - it’s a high quality business in a niche market in which it continues to be immune from competitors. It’s also a good example of a high quality stock in a cyclical sector which should be well placed to grow if economic conditions improve.

But while awaiting those improving economic conditions, which may stimulate a swing on momentum, is there a value argument to be made here?

Shares are trading just under 10x forecast earnings, which is hardly prohibitive for a company which hits the kind of quality metrics of Somero. And there is also the fact that this is a US company which trades its shares on the unloved UK market. In 2025, that surely makes it a potential takeover target.

On balance, I am remaining neutral. Although I don’t think there is any reason for alarm, the declining quality metrics are worth caution and I don’t think the price is yet cheap enough to be considered a decent value stock. AMBER

Graham adds: while I agree with the AMBER stance on Somero, I do think that competition has become a problem for the company. Industry rival Ligchine was founded in 2007 and offers very similar products (laser guided concrete screeds). If you search online, you will find industry chatter that Ligchine is far cheaper than Somero. Ligchine's products might not entirely match the quality of Somero and the customer support might not fully match up either, but this is direct competition and I do think it could go a long way towards explaining Somero's drop-off in performance in recent years. For this reason I no longer rate Somero as highly as I did before and I think a more modest valuation, perhaps around the current level, makes sense.

Boohoo (LON:BOO)

Down 2% to 27p (£377m) - "Debenhams is Back" - Megan - RED

Boohoo’s star has finally been extinguished.

Between 2006 and 2020 the company climbed to the heights of the online fast-fashion world, demolishing the bricks and mortar retailers which got in its path. But with cheaper international competitors taking its domestic market share and the post-Covid last gasp surge of high street retailers (not to mention some questionable corporate governance), Boohoo has been in a downward spiral for the last five years.

And now it will be Boohoo no longer. Going forward the company will be rebranded as Debenhams, leaning on the legacy of the high street department store which it bought out of administration in 2021. Debenhams was consigned to administration because of the impact of Boohoo and its peers - it’s funny how things turn out.

It’s hard not to read this morning’s announcement as desperate. “Debenhams is back,” reads the headline.

Our ongoing business review has confirmed that Debenhams, its business model and its technology is at the epicentre of our Group going forward. It is the driving force of the business and will lead the Group recovery. It is at the heart of the investment case.

It’s not a great sign that the company at the ‘heart of the investment case’ can’t give normal retailer numbers in its trading update. The company has chosen to report Gross Merchandise Value (GMV) and EBITDA rather than sales and profits. And although those figures seem quite positive, I am not sure how to unpick what is surely a mountain of adjustments.

In the year to February 2024, the group as a whole reported GMV (pre-returns) of £2.6bn, this fell to £2.3bn in FY2025. Quite why the company feels the need to report pre-return GMV figures is beyond me. These aren’t sales, but merely a distraction.

GMV post-returns was £1.8bn last year and it’s fallen to £1.6bn in 2025, owing largely to the woeful performance of the ‘youth brands’ (Pretty Little Thing, Boohoo and MAN) which make up more than three quarters of the total group sales.

The difference between the pre and post-return figures show a major problem with the company’s business model. In 2025, customers returned £682m worth of items. And because of the company’s free delivery and refund policy, it won’t have cost the customer anything and it’s the company that has had to bear the burden of the cost of selling items just to be returned. There’s also a worryingly large disparity between GMV and group sales. Why is the company only making £1.2bn from £1.6bn of merchandise sales?

There is also an element of wishful thinking in the claim that Debenhams is stock and capital light. That’s all well and good, but Boohoo isn’t. The company has been sitting on an increasingly heavy burden of debt (£82.7m at the year end) and its stock management has been appalling. Once again in the financial year to date, the company has had to discount heavily to get its stock levels to the correct levels. Management says that the leaner Debenhams operating model will help drive profitability and cash generation in the beleaguered Boohoo business - as if changing the name is going to magically fix the problems of the broader group.

Megan’s view:

Sometimes a business needs a big kicker to turn things around. A new name, new management and a renewed focus could well be that kicker. The debt burden, though still high, is on its way down. But I am being generous.

This update is a lot of words which hide the actual underlying problems which persist. Graham was tempted to temper his negative view in December, but stuck with RED. I am going to do the same.

Roland's Section

Supermarket Income REIT (LON:SUPR)

Down 0.4% to 73p (£907m) - Interim Results - Roland - AMBER/GREEN

At the time of publication, Roland holds a long position in SUPR.

UK REITs are attracting bids at an impressive rate, but this supermarket specialist has not attracted any offers that we know of (yet).

Instead, SUPR’s management appears to be taking decisive action to slim down the cost base and prepare this REIT for life as an independent property company.

A few days before today’s interim results, SUPR released an RNS with the unusual title of “Proposed Management Internalisation”.

REITs commonly use external investment advisors to run their investments, but SUPR’s board has decided that they can achieve significant cost savings by buying out the current management team from advisor Atrato Group and bringing them in house.

According to the company, this arrangement will cost £19.7m but will result in £4m annual savings, delivering a potential yield on cost of c.19%. Looked at differently, this could deliver a c.5% increase to run-rate annual profits based on current forecasts.

If these assumptions prove correct, this plan could boost the REITs profitability by generating a superior return on capital to most other transactions SUPR might consider right now.

This focus on cost savings runs through today’s results, with a number of mentions of closing the discount to NAV.

Half-year results: both earnings and the dividend reached c.50% of expected full-year levels during the six months to 31 December, with results showing an improvement in annualised rent reflecting recent lease renewals and acquisitions.

Annualised passing rent up 13% to £118.5m

Adjusted earnings +3% to 3.0p per share

Dividend per share up 1% to 3.1p

EPRA cost ratio reduced to 13.6% (HY24: 15.1%)

Key metrics for the portfolio show a modest increase in valuation and rental yields:

Portfolio valuation up 3% to £1,833m

Net initial yield: 6.0% (HY24: 5.9%)

EPRA net asset value per share up 1% to 88p

Loan to value ratio: 39% (HY24: 37%)

Recent leasing and disposal activity appears to support SUPR’s valuations:

Lease renewals on three of its shortest-leased stores at average rents of 13% above its valuer’s estimated rental values (ERV)

£63.5m sale of Tesco Newmarket store to Tesco at 7.4% above book value

Perhaps these results also support the company’s strategic position that its assets are “mission critical” to its tenants.

Balance sheet/income safety

SUPR’s portfolio now has a weighted average unexpired lease term (WAULT) of 12 years, with no major lease renewals due for seven years.

More than 80% of rent is index-linked and 79% of income comes from Sainsbury’s, Tesco and France’s Carrefour. Realistically, I see no risk that these tenants will default.

Instead, my main concern is that SUPR’s borrowing costs might rise to a level where they put pressure on the affordability of its dividend.

We can already see that dividend cover is slim – today’s results show 0.99x earnings cover and the full-year figure is expected to be 1.0x – barely enough.

There’s no doubt debt costs are rising, too. Today’s results show 93% of drawn debt was hedged at an average cost of 4.0% at the end of 2024. This compares to an average cost of 3.7% at the end of June 2024.

Recent refinancing has mostly taken place at rates between 4.0% and 4.5%. However, use of hedging has helped to cap the REIT’s overall rate.

As of today, SUPR reports an average debt maturity of 3.7 years and a weighted average debt cost of 4.0%.

My estimates suggest the dividend remains safe at this level. But the contrast between these short maturity loans and SUPR’s long leases mean that several refinancing rounds will be needed while current lease terms remain unchanged.

If borrowing costs fall as expected, this could work out well for SUPR. But in the event that borrowing costs remain elevated or rise further, there could still be some risk to the dividend.

I am not surprised SUPR is placing a strong emphasis on cost savings. Proactive self-help is sometimes the best strategy.

Outlook & Estimates: today’s numbers appear to be in line with full-year expectations.

The company confirms that it’s on track to deliver the FY25 dividend target of 6.12p per share. That’s equivalent to a useful 8.3% yield at current prices.

Forecasts for FY26 show a useful increase in earnings that’s expected to strengthen dividend cover.

Roland’s view

Today’s numbers seem broadly reassuring to me and I have no issues with SUPR’s strategy.

These results appear to validate the worth of SUPR’s portfolio and give me confidence in the stock’s tangible asset value of 88p per share.

The current share price of 73p represents a 17% discount to today’s NAV figure. I think there’s some scope to close this gap, but I don’t expect the gap to close entirely unless borrowing costs fall sharply.

The reason for this is simply that I think the market will continue to expect significantly higher yields from risk assets such as REITs than from UK government bonds, which are considered risk-free.

The StockRanks were taking a neutral-positive view on SUPR ahead of today’s results:

I remain positive on SUPR as a high-yield income opportunity, but dividend cover remains tight and could potentially come under further pressure. I’m going to maintain my previous AMBER/GREEN rating.

Care REIT (LON:CRT)

Up 33% to 108p (£448m) - Recommended Cash Acquisition - Roland - PINK

Care REIT (previously Impact Healthcare REIT) owns a portfolio of 137 UK care homes managed by 15 different tenants. Today we learn that it’s received a cash takeover offer of 108p per share (£448m) from New York-listed CareTrust REIT (NYQ:CTRE).

The buyer is a much larger operator with over 400 properties and a market cap of £3.8bn. CareTrust (note the similar name!) would like to enter the UK market and has chosen to do so by acquiring Care REIT.

Offer details: there has been much discussion in these pages recently about whether REITs should be accepting offers below net asset value. Graham touched on this topic yesterday with regard to Assura, another UK healthcare REIT being targeted by US bidders.

Today’s offer for Care REIT is below its last-reported book value:

Recommended cash takeover offer: 108p per share / £448m

30 Sept ‘24 EPRA net tangible asset value: 118.7p per share / £492m

Today’s offer is at a 9% discount to Sept ‘24 NAV

Is the price fair? In principle, I agree with Graham that REITs should seek to be taken over at or above their tangible net asset value.

But I think there are a couple of points that suggest to me Care REIT may be in a weaker negotiating position than Assura, for example – or indeed SUPR, which I’ve also discussed today.

Financing: Care REIT’s average cost of drawn debt is 4.56% compared to 2.3% for Assura.

While Care REIT has some long-term fixed-rate debt, my initial impression is that >50% of its debt is dependent on relatively costly short-term interest rate caps.

Tenant quality: I haven’t researched Care REIT’s tenants specifically, but in general the UK care home sector is prone to regular tenant failures. I would argue that Assura’s portfolio of mostly NHS facilities comes with much less default risk.

Roland’s view

CareTrust will probably be able to refinance Care’s portfolio more cheaply and perhaps make other savings to improve returns. But it’s not clear to me that Care REIT can achieve this as a standalone entity.

Nor is it clear that Care will be able to expand further while its traditional source of funding (equity placings) is unavailable.

One other point I think is worth considering is to look at the valuation in terms of dividend yield. In January, Care REIT set its 2025 dividend target at 7.2p per share.

Applying this dividend to today’s offer price gives a forecast yield of 6.7%.

As a potential equity investor, would I accept a lower yield than this? Probably not. Care REIT is relatively small for a REIT and operates in a sector with a mixed record of tenant profitability.

6.7% doesn’t seem that high, when I can easily get c.4.5% from UK gilts with zero risk.

(Yesterday’s possible offer for Assura also implies a 6.7% FY25 yield, but as discussed I think this is a higher quality proposition.)

For all the reasons outlined above, I am leaning towards thinking that today’s offer for Care REIT is reasonably fair.

Costain (LON:COST)

Up 8% to 112p (£300m) - FY24 Results - Roland - GREEN

The successful execution of our strategy has delivered a record increase in our forward work position of £1.5bn to £5.4bn.

An upbeat set of results from this infrastructure construction group has received a positive reception today.

The company says that on one measure at least, 2024 adjusted operating profits have come in at the upper end of expectations. These were guided at £41.9m to £43.3m in January, so today’s figure of £43.1m is indeed at the upper end.

The other big highlight of today’s results – a £1.5bn increase in Costain’s order book to £5.4bn – was also flagged in January but has received headline billing again today. Understandably – if profit margins are as expected, this represents an impressive level of new business awards in key markets such as water and rail.

2024 results summary: today’s numbers are strong:

Revenue down 6.1% to £1,251m

Adjusted operating profit up 9.7% to £43.1m

Reported operating profit up 16% to £31.1m

Adjusted earnings up 19.7% to 14.6p per share

Dividend up 100% to 2.4p per share

Year-end net cash of £158.5m (2023: £164.4m)

These are very solid numbers and my sums show a good level of free cash flow conversion, too.

Trading commentary reveals growth in the company’s Natural Resources division last year (Water, Defence, Nuclear, Energy).

In Transportation, performance was more mixed. There were lower volumes in Road and Rail, but some growth in work at Heathrow and new contracts with Transport for London.

Costain’s adjusted operating margin improved to 3.4% (2023: 3.0%) driven by improvements in both divisions.

My sums suggest a respectable return on capital employed of 12.4% (2023: 11.4%), with both figures based on reported operating profit – see below.

Exceptional costs: I do need to flag up some large adjusting items. These may be one-off but I suspect they were largely cash costs. Items of a similar nature may yet recur, too. I’d view them as a hazard of being in business in this sector:

Fire safety claims: £6.7m - includes one completed claim and a provision for one further claim

Transformation costs: £5.4m - 2024 was the final year of this restructuring programme

Interest income/net cash: one thing I’m starting to see more of is companies reporting pre-tax profit that’s higher than operating profit. We have this today – reported PBT of £36.5m is £5.4m higher than operating profit of £31.1m.

This represents net interest income received during the year. This income also provides implicit evidence that Costain’s probably maintained some kind of net cash position throughout the year. It’s a pity the company doesn’t report daily net cash, but this evidence is the next best thing, in my view.

As always with this type of business, I think it’s worth emphasising that Costain’s net cash is not surplus to requirements – strong liquidity and creditworthiness are essential to win new work and be able to mobilise new contracts. There’s a reason why the dividend is covered c.5x by earnings!

Estimates: with thanks to broker Panmure Liberum, we have updated earnings forecasts today. Interestingly, Panmure’s estimates for 2025 and 2026 have not changed. 2027 estimates are newly introduced today:

2025E EPS: 14.3p

2026E EPS: 15.5p

2027E EPS: 17.3p

The 2025 estimate of 14.3p is higher than the consensus figure of 13.7p shown in Stockpedia ahead of today’s results. But this still implies a slight fall in earnings in 2025 relative to 2024’s adjusted earnings of 14.6p per share.

These forecasts appear to be based on revenue remaining broadly flat in 2025 and 2026, but supported by improved profit margins of over 4%. Interest income is expected to be lower, going forward, too – I suspect this accounts for the expected fall in 2025 EPS.

These forecasts price Costain on around eight times 2025 forecast earnings, falling to seven times in 2026. This broadly maintains the forecast valuation in the StockReport:

Outlook: CEO Alex Vaughan sounds confident today, although the emphasis on 2027 seems to suggest there may be a medium-term weighting to further growth:

The successful execution of our strategy has delivered a record increase in our forward work position of £1.5bn to £5.4bn. This, together with growth on existing frameworks, gives us increasing visibility and confidence on delivering further progress in FY 25 and FY 26, with a step change in performance in FY 27 and beyond. We have already secured approximately 80% of our forecast revenue for FY 25 and our current levels of bidding activity remain high.

Roland’s view

Costain is a company I’ve always had some respect for, although it’s not escaped the classic problems in this sector:

However, these issues (and the resulting shareholder dilution) now appear to be firmly in the past. Costain is trading well and continues to look reasonably valued.

The balance sheet looks fine to me, given the supporting evidence that suggests a year-round net cash position. Reporting average daily net cash would not do any harm though – it’s the gold standard of reporting for this type of business, in my view.

There is clearly plenty of opportunity for problems to arise between now and 2027. But Costain’s recent progress and modest valuation mean I can’t see any cause for concern at this time. I’m going to maintain our GREEN view following today’s results.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.