Good morning! The FTSE is set to open up by nearly 2% this morning, above 8100.

12.40pm: thanks for your input everyone, I'll wrap up the report there. A pleasant start to the week!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| Greatland Gold (LON:GGP) (£1.78bn) | March 2025 Quarterly Activities Report | 90,172oz at AISC of A$2,126/oz. FY25 Guidance (7 months of full production): 196-210k oz. Broker Canaccord has left EPS forecasts unchanged today, suggesting this performance is in line with expectations. | AMBER/RED (Roland) [no section below] Today’s quarterly update seems to suggest GGP is making good progress with its strategy. Gold recovery levels are higher than budgeted in the pre-acquisition plan, contributing to higher production. At the same time, record gold prices are providing operating leverage, resulting in strong cash generation. However, earnings forecasts are unchanged and are expected to be broadly flat in FY26 due to further dilution. With no established track record of production and gold already at record highs, GGP shares look expensive to me on c.30x earnings. My impression is that near-term upside might depend on the gold price – I can see some risk of a correction if gold weakens. I am not convinced the stock offers value at current levels and share the algorithm’s view that this could be a momentum trap. |

Ashmore (LON:ASHM) (£953m) | SP down 6% Q3: AuM falls 5% to $46.2bn, positive investment performance with $3.9bn of net outflows. | GREEN (Graham) | |

Kainos (LON:KNOS) (£784m) | Solid Q4. Full year in line (adj. PBT £64.1 - 68.2m. Robust backlog and pipeline. | AMBER (Graham) [no section below] After a major profit warning last year, the market is perhaps breathing a sigh of relief that this update is in line. In their Workday Products division, they now have an ARR of £72m, targeting £100m by 2026 and £200m by 2030. However, I’d be reluctant to value this “expertise” ARR as I would value pure software ARR. As the stock continues to trade at a moderately high earnings multiple (PER 16x), I maintain my neutral stance. | |

Cerillion (LON:CER) (£383m) | H1 revenue falls from £22.5m last year to £20.9m in FY Sep 2025. There is an anticipated higher H2 weighting in the current year. “Very well-placed to meet market expectations”. | AMBER (Graham) [no section below] A second-half weighting is often the precursor to a profit warning although I am minded to give some credence to management's insistence that they are well-placed to meet market expectations. Their track record in expectations management is seemingly rather good. Any anyway, large contract renewals and extensions to licenses can be a lumpy type of business. So I'm not overly suspicious here. Overall, we've been neutral on this provider of telco software and I believe it remains fair to hold that stance today, given that the valuation remains rather punchy. For quality and long-term growth potential it might deserve deeper study, as it steals business from incumbents in the space. | |

Polar Capital Holdings (LON:POLR) (£370m) | AuM down 2% year-on-year. Net flows were flat. Negative market movement/inv performance. | AMBER/GREEN (Graham) I feel obliged to temper my bullishness on the back of a c. 30% cut to Polar's EPS forecast at Equity Development. The market had already priced in a large EPS cut following negative market movements in the quarter which saw AuM fall by 10%. I do still rate this company very highly - its flow performance is excellent relative to other managers. | |

Aquis Exchange (LON:AQX) (£195m) | Net rev down 11%, adj PBT down 79% to £1.1m. “Economic headwinds”. Takeover continues. | PINK (under offer) | |

John Wood (LON:WG.) (£173m) | Sidara has made a conditional cash offer of 35p per share and would also provide $450m of new debt financing. | RED (Roland) [no section below] | |

Concurrent Technologies (LON:CNC) (£129m) | Rev +27%, adj PBT +40% to £5.2m. Order intake +45% to £41m. FY25 outlook in line. | AMBER/GREEN (Roland) Revenue and PBT appear to be in line with expectations today, but EPS misses 2024 estimates due to a higher tax charge. Tax is also the theme of a major adverse restatement of FY23 earnings. I am discouraged by further accounting niggles but can’t deny this defence-focused business appears to have strong underlying momentum. US exposure and customer concentration are perhaps more of a risk than in the past, but I think I can justify a modestly positive stance when viewed through a High Flyer lens. | |

Serabi Gold (LON:SRB) | Gold prod +11% to 10koz, net cash $21.1m. On track to meet FY prod guidance of 44-47koz. Company to consider returning capital to shareholders. | AMBER/GREEN (Roland) [no section below] A rising tide lifts all ships and I think it’s prudent to be aware of the impact record gold prices will be having on miners’ profits. Even so, today’s update from Serabi looks pretty solid to me and suggests there could be further scope for growth here. This group has an established track record and a healthy balance sheet. If gold stays at current levels, I think a valuation of 1.5x book value could offer value. On this initial inspection, I’m happy to take a moderately positive view. | |

| Rockwood Strategic (LON:RKW) (£95m) | Trading Update | NAV +21.1%. Increased share count 25%. “A material buying opportunity” in UK small caps. | |

Argo Blockchain (LON:ARB) (£20m) | Financing structure announced 26 March is no longer proceeding. Other discussions underway. | RED (Roland) [no section below] A proposed deal to acquire GEM Mining LLC and secure a new $10m convertible loan from GEM shareholders appears to have fallen through. The company says discussions are continuing with GEM and others, but this is the second time in two months that a financing deal has fallen through. Despite high bitcoin prices Argo has not recaptured its 20/21 profitability. With net debt of c.$40m I think there’s a risk the equity could go to zero. One to avoid, in my view. |

Graham's Section

Polar Capital Holdings (LON:POLR)

Up 1% to 370p (£351m) - AuM Update - Graham - AMBER/GREEN

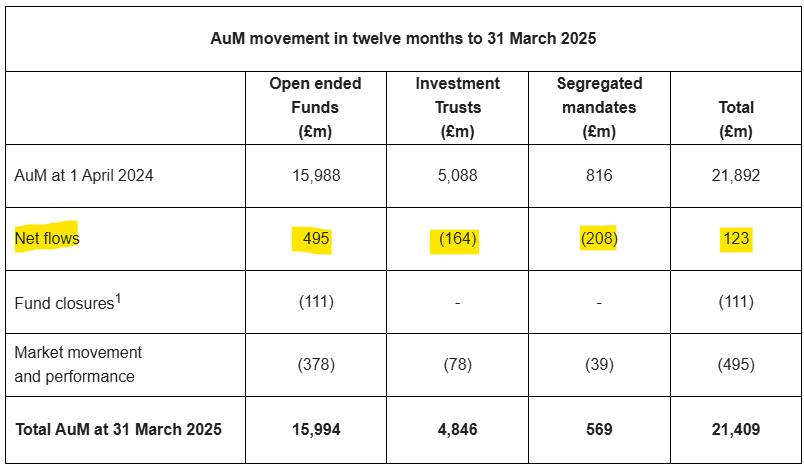

It’s the usual quarterly AuM update from Polar, this time for Q4 and therefore for the financial year ending March 2025.

AuM finished the year at £21.4bn, down 2% year-on-year as it states in the opening paragraph of the RNS, but also down 10% quarter-on-quarter.

And things haven't gotten any better since the start of the new financial year on April 1st.

Let’s skip ahead to the CEO’s commentary on Q4:

The start of calendar year 2025 has been difficult for global equity markets with increased volatility and uncertainty introduced by the possibility of a tariff induced global trade war. With investors selling out of risk assets, it is no surprise that during the quarter total AuM decreased by £2.4bn from £23.8bn at the end of December 2024 to £21.4bn at end of March 2025, a 10% decrease, of which net outflows were £0.1bn and market movements and performance made up the remainder.

Market movements are beyond their control; net flows are what I focus on.

As noted above, net outflows in Q4 were slim at just £0.1bn.

They finish the year with positive net flows of £0.1bn.

In a very depressed environment for active managers, that strikes me as a fine achievement.

The breakdown below shows how the £0.1bn was achieved: a £495m inflow into Polar’s open-ended funds, a £164m outflow from Polar’s investment trusts buying back their own shares, and a £208m outflow in segregated mandates.

Let’s turn back to the CEO comment for his conclusion:

"While volatile equity markets may impact AuM levels and profitability in the near term, we remain confident that with our diverse range of specialist active fund strategies, we are well-positioned to perform for our clients and shareholders over the long term."

Estimates: Paul Bryant at Equity Development suggests this morning that Polar’s flows were strong relative to its peers both in terms of Q4 and the year as a whole. I wholeheartedly agree with this: I’ve been consistently impressed by Polar’s flows and for the second year running I included it in my watchlist for this year.

However, Paul does cut his earnings estimates for FY26, due to the sharp fall in AuM at the end of FY March 2025, and a more conservative assumption that net flows for FY March 2026 will only be flat. The previous assumption was for £500m-£1bn in net inflows.

A 15% reduction in the end-of-year AuM forecast for FY March 2026 (to £22.6bn) feeds through to a nearly 30% reduction in the EPS forecast, from 47.5p to 33.8p.

Graham’s view

This stock is again trading at 11x earnings, the same multiple it was trading at in December.

The difference is that both the market cap and the earnings forecast are down by c. 30%!

I’ve been positive on fund managers on the basis that they provide a geared return on the stock market, and have been trading at levels that are very depressed against their prior valuations, providing scope for a powerful rebound.

However, with the ongoing flight to passive managers, it has been very difficult to choose active managers with good prospects and improving sentiment - the trends are deeply negative for the sector as a whole.

Clearly, I’ve been too early with Polar, as the sudden 10% drop in AuM has taken a huge bite out of profit forecasts.

Similarly, I bought a few shares in Impax Asset Management (LON:IPX) for my personal portfolio and have witnessed what feels like an almost immediate 50% decline in the share price. A reminder that no matter how low we might think something has already fallen, it can still very easily fall another 50% or more!

At Polar, however, their flows continue to hold up really well. I can’t emphasise enough how impressive it is to have a flat flow performance in this environment. They have vastly outperformed their peers over the past year, having outperformed most of them in prior years, too.

Polar shares now provide £60 of AuM for every £1 invested in the stock. This is a very large increase on the £46 of AuM that they offered 3-4 months ago. So it is now trading a little bit more like a “value” fund manager stock, instead of having the premium rating that it had before.

The StockRanks see it as offering excellent Quality and Value, but poor Momentum, which makes it a Contrarian pick - that sounds about right.

I’m going to downgrade my stance to AMBER/GREEN to reflect the fact that we’ve seen this very significant EPS downgrade. I still view it as GREEN for value and wouldn’t mind owning some in my personal portfolio. But at the same time, a c. 30% EPS downgrade is a serious issue for any stock and so I do need to temper my bullishness whenever this occurs, even for a stock that I strongly believe in.

Ashmore (LON:ASHM)

Down 6% to 125.1p (£898m) - Trading Statement - Graham - GREEN

This is a Q3 AuM statement, and the market doesn’t like it.

It’s not as bad as Polar in terms of the quarterly percentage reduction in AuM. However, bear in mind that Ashmore is still predominantly a fixed income manager, and so its AuM should be more stable compared to a manager that invests in growth-oriented equities.

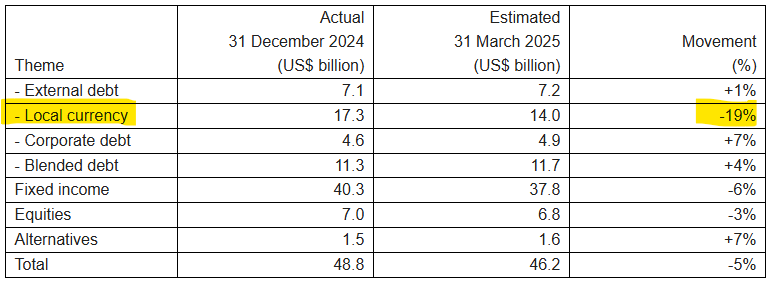

Ashmore’s AuM has fallen by 5% in three months, from $48.8bn to $46.2bn.

That masks a very poor net flow movement, as it includes positive market movements. Net outflows were $3.9bn or 8% of starting AuM - a really bad figure for a single quarter.

"Local Currency" - the segment that includes bonds issued in the domestic currencies of emerging market countries - saw a 19% fall in AuM in a single quarter:

This reflects “a small number of large institutional redemptions towards the end of the period in the local currency theme, reflecting client specific asset allocation decisions”.

CEO comment from Mark Coombs, who owns 29% of Ashmore, who addresses the outflows:

…individual institutional asset allocation decisions resulted in a net outflow for the quarter. These decisions do not appear indicative of a broader pattern of client activity and encouragingly, levels of investor interest in Ashmore's Emerging Markets fixed income and equity strategies continue to be strong.

He also comments that emerging markets have not underperformed the United States since the tariff issue has arisen:

Against a 1% decline in the US Treasury index and a 2% decline in US HY bonds, Emerging Markets fixed income is down by less than 2%, and Emerging Markets equities performance is in line with the US.

Graham’s view

As with Polar, this stock is ranked as “Contrarian” by Stockopedia’s rules.

The institutional redemptions announced today are going to hit the bottom line - the latest in a series of earnings downgrades.

Therefore, as with Polar, perhaps I should respect the trend and moderate my view to AMBER/GREEN?

As I noted in February, the dividend is not covered by earnings and so it should be considered unsafe:

One major point in Ashmore’s favour is its balance sheet, with about £730m of tangible equity. I calculate that after the payment of a recent dividend, tangible equity might be c. £700m.

Stockopedia's calculations also suggest that it trades at only a modest premium to book value:

So even though I do think earnings at Ashmore remain vulnerable to further downgrades, the stock is now close to deep value territory in my view, with a market cap largely backed by tangible assets.

Of course there is nothing to say that it can't trade at a discount to tangible NAV. But from an analyst's perspective, I think I can treat this as something of an exception and leave my GREEN stance on it unchanged. In theory, the balance sheet should have an increasingly large influence on the share price from here.

Roland's Section

Concurrent Technologies (LON:CNC)

Up 5% to 158p (£137m) - Final Results - Roland - AMBER/GREEN

Concurrent Technologies Plc (AIM: CNC), a designer and manufacturer of leading-edge computer products, systems, and mission-critical solutions used in high-performance markets by some of the world's major OEMs, announces its audited final results for the year ended 31 December 2024.

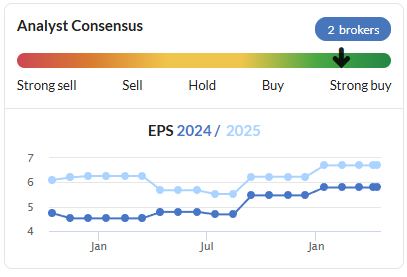

I think today’s results from Concurrent are essentially in line with January’s upgraded forecasts, but the earnings per share figure provided today is below both Stocko consensus and broker Cavendish’s January estimate.

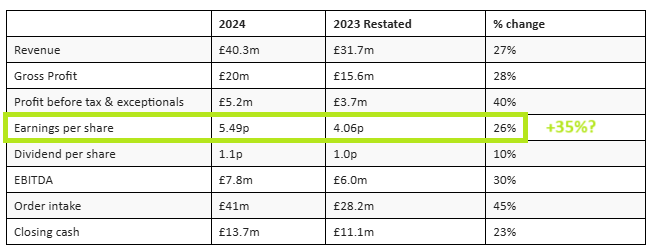

The group saw revenue rise by 27% to a new record of £40.3m in 2024, with adjusted pre-tax profit up 40% to £5.2m. Both of these numbers are in line with January estimates.

Cash conversion lagged profits as the group continues to capitalise significant levels of R&D spend. However, net cash improved to £13.7m at the year end, representing nearly 10% of the market cap.

Profitability also improved last year. Gross margin rose to 49.5% (FY23: 48.4%), while my sums show operating margin rising by 1.3% to 12.9% (FY23: 11.6%). I calculate that return on capital employed rose to 12.4% last year (2023: 9.2%).

Hopefully these improved margins reflect operating leverage from growing scale – if so, then further increases could be possible, helping to justify the stock’s premium valuation.

The only fly in the ointment in Concurrent’s headline figures was an apparent earnings per share miss.

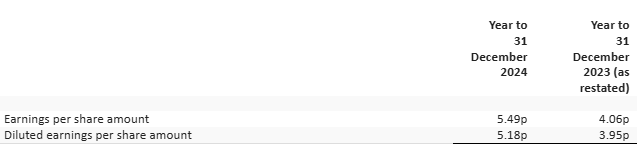

FY24 earnings per share appear to be well below consensus forecasts of 5.8p:

FY24 basic EPS: 5.49p

FY24 fully diluted EPS: 5.18p, reflecting Aug 23 equity raise & additional options

From what I can see, this shortfall is due to a higher tax charge for 2024 than previously expected. Concurrent’s tax calculation is complicated for a small cap and previous broker coverage suggested a near-zero tax charge for FY24, rather than the c.£0.5k charge reported today:

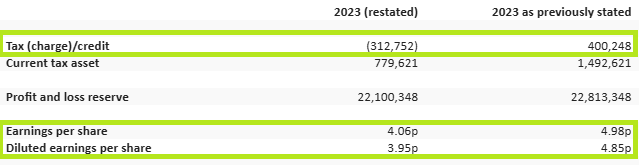

FY23 restatement: the complexity of Concurrent’s tax situation is perhaps hinted at by the restatement to FY23 results in today’s accounts, due to a previous error in calculating tax assets:

A prior year restatement has been included for corporation tax as a result of an erroneous tax asset being included in the 2023 accounts. The impact of this adjustment is to increase the tax charge in 2023 by £713,000 and decrease the corporation tax asset in 2023 by £713,000.

Correcting this error has resulted in an 18.5% drop in Concurrent’s FY23 earnings, as last year’s £400k tax credit is transformed to a tax charge of £313k:

Accounting confusion? To continue this theme, my impression is that today’s published numbers also include one or two inconsistencies relating to earnings per share.

First of all, the percentage change for EPS in the highlights table doesn’t add up – the difference between the two EPS figures in this table is 35%, not 26%:

The 26% increase applies to the increase in diluted earnings that’s mentioned in the CFO’s financial review (my emphasis):

Earnings per share (EPS) was 5.12p (FY23: 4.06p). This reflects the increased number of shares, in full, following the equity raise in August FY23.

I assume the 5.12p EPS is fully diluted, but I can’t find any other mention of this in today’s accounts. I wonder if this is a typo, as a slightly different diluted figure of 5.18p is mentioned in the Income statement.

The basic and diluted EPS pairings shown in the Income statement are also different to that mentioned in the CFO’s review, possibly suggesting that the 5.12p/5.18p figure should have been paired with a restated FY23 figure of 3.95p:

In the Week Ahead on Friday, Mark commented that Concurrent has suffered from some accounting issues in recent years. Further evidence of past accounting errors (and possible typos) in today’s results is a little disappointing, in my view.

However, I’ve spent too much time trying to untangle these niggles. Let’s move on and take a look at the bigger picture and the outlook for 2025.

Trading commentary & tariffs: Concurrent says it made continued progress with its growth strategy last year:

Continued investment in R&D led to “several new product launches”, including progress with the company’s roadmap for its Systems business

New partnerships including Parry Labs, Eizo Rugged and “a fast-growing defence prime contractor in the US”

Restructured the group into two business units, Products and Systems

Secured 22 design wins, including the largest-ever contract to date for a US client, valued at $6m – this is expected to contribute from FY27

Further progress has been made already in 2025, including a £3.4m order for “VME-based 6U computer boards from a long-standing European customer”.

Outlook: Concurrent generated 45% (£18.3m) of its revenue in the US last year and acknowledges the potential uncertainty relating to tariffs and possible changes to US defence spending plans:

The Group aims to navigate the rapidly evolving tariff arrangements being implemented by the US administration with efficiency and pricing measures, as well as monitoring any impact of longer-term tariffs on the Company's programmes and markets.

As things stand, the company says its outlook is unchanged:

Board expects trading for the full year to be in line with market expectations.

Updated estimates: with thanks to house broker Cavendish, we have updated earnings estimates today. Cavendish’s analysts have tweaked their forecasts slightly, cutting FY25E EPS to 6.6p (previously 6.7p).

I probably wouldn’t call this a downgrade, but it’s definitely not an upgrade!

Even so, investors seem to have taken a bullish read on Concurrent’s results today.

That leaves the stock trading on 24 times FY25 forecast earnings. I share the algorithms’ view that this is not necessarily good value:

Roland’s view

My guess is that Concurrent’s High Flyer style and strong Quality and Momentum metrics will remain in place when Stocko’s algorithms digest today’s results. I respect this and acknowledge the recent momentum in earnings upgrades:

However, I can’t help feeling there are some risks here. In addition to the factors I’ve mentioned above, I think it’s also worth noting that customer concentration is fairly high:

Largest customer generated 15% of revenue in 2024

Top three customers generated 29% of revenue

The heavy exposure to the US market is also a risk, in a way that wasn’t evident a year ago, in my opinion.

The valuation creates an additional risk, in my view. On a forward P/E of 24, I would argue that any disappointment could be quickly punished.

I’d like to go AMBER here, but out of respect for Concurrent’s High Flyer credentials and recent strong growth momentum, I am going to go with AMBER/GREEN

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.