Good morning!

I've noticed many comments in recent days, both here and elsewhere, along the lines of "Stock XYZ is up 10% recently, does anyone know why?"

What this says to me is that we've been in a depressing bear market in small-caps for far too long, and investors have forgotten that shares can go up sometimes!

Stocks are still being taken off the market, and are not being replaced by fresh IPOs, because foreign markets and private markets are willing to give higher valuations to businesses than investors on the LSE.

And the only way this is going to change is if we get a lot more of these unexplained increases in share prices. Long may it continue!

The Agenda is complete.

Spreadsheet accompanying this report: link.

13:50: wrapping this up for today, thanks!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Rentokil Initial (LON:RTO) (£8.9bn) | Sold for €410m, exp cash proceeds c.€370m. Now focused on Pest and Hygiene & Wellbeing. | AMBER (Roland) [no section below] This disposal looks sensible to me and was something I had half expected to see. However, it doesn't seem likely to have much impact on the difficult turnaround that’s underway following Rentokil’s ambitious (unwise?) $6.7bn acquisition of US rival Terminix in 2022. This deal left the group with elevated debt levels and an enlarged share count. Unfortunately, combining Terminix with Rentokil’s US business has proved more difficult than expected. However, I see that the CEO who oversaw the deal is now retiring and I think the worst of the problems may now have passed. I think there could be an opportunity here, but at this time and price I share the StockRanks’ position that a neutral view makes most sense. | |

Kingfisher (LON:KGF) (£5.3bn) | Full year guidance reiterated for adj PBT of £480-540m. Q1 LFL sales +1.8%, further share gains. | GREEN (Roland) Strong Q1 sales in the UK were offset by weaker performance in France and may have received a boost from the spring weather. But my view is that Kingfisher is doing the right things and is positioned to deliver improved profitability when external conditions improve. The valuation looks reasonable to me and I’m comfortable taking a positive view, reflecting the StockRank of 99. | |

Softcat (LON:SCT) (£3.6bn) | SP +2% | GREEN (Graham) [no section below] Roland was GREEN on this High Flyer in March and it has delivered today with another earnings upgrade. The muted share price reaction may reflect the high growth expectations already baked into an earnings multiple of 25x. This IT infrastructure service provider is enjoying strong growth which is entirely organic; I’m backing the trend by staying GREEN. | |

Pets at Home (LON:PETS) (£1.21bn) | FY25 in line, with revenue +0.1% and adjusted PBT +0.7% to £133m. FY26 YTD trading in line. | AMBER/GREEN (Roland) Today’s results do not highlight any fresh problems and show the group continuing to develop its integrated pet care offering. While the CMA review (due July) and falling earnings remain a risk, I think there’s just enough here to justify a moderately positive view. | |

Playtech (LON:PTEC) (£998m) | German operator pferdewettten.de is being given the opportunity to take over HAPPYBET shops. | ||

C&C (LON:CCR) (£583m) | FY25 net rev flat, adj PBT +44% to €55.9m. FY26 outlook unch. “Current trading encouraging”. | AMBER (Graham) These numbers are still not clean enough for my liking. The transformation is under way and I still have a generally positive view of the company and its brands. But given the poor returns in recent years, the reliance on the weather, the debt load and the lack of balance sheet equity, I doubt that it's worth much more than the current market cap at this time. | |

LSL Property Services (LON:LSL) (£305m) | Expect profit growth in FY25 in line with expectations. End markets performing as expected. | ||

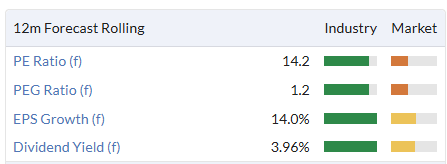

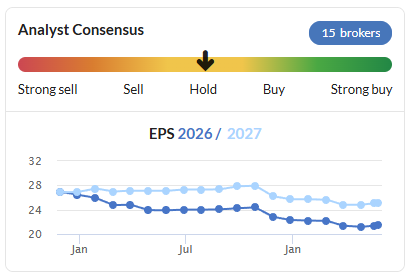

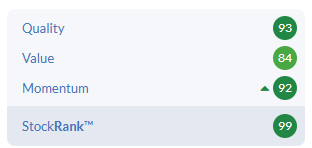

| Thor Explorations (LON:THX) (£249m) | First Quarter Financial and Operating Results | 22,750 oz of gold sold, avg. gold price $2,720. Quarterly record net income $34.4m. Maiden dividend. | AMBER/GREEN (Roland) [no section below] This Canadian gold miner is focused on Africa. The shares trade on a tempting FY25E P/E of 2, but I would note that Thor is also trading at 1.7x NAV and 7x trailing free cash flow, according to Stockopedia. These metrics look more relevant to me, given that revenue and earnings are expected to halve in 2026 and Thor only appears to have six years of commercial reserves at Segilola, its sole producing asset. While the company has significant resources elsewhere, spending will need to continue on exploration and development to convert these to reserves. If the gold price remains high, I think there’s the potential for further gains. But on this brief initial review, my feeling is that Thor is relatively speculative for a gold producer and may be trading close to fair value. |

Science (LON:SAG) (£207m) | SAG has increased RCDO stake to 21.8% (avg 239p). Open letter issued ahead of GM on 18 June. | ||

Aptitude Software (LON:APTD) (£155m) | Confident FY25 will be in line despite economic uncertainty. “Improved Fynapse pipeline”. | ||

Integrated Diagnostics Holdings (LON:IDHC) (£151m) | Q1 rev +35%, adj net profit +114% to EGP100m. Patient numbers -8%, revenue per patient +46%. | ||

Avingtrans (LON:AVG) (£132m) |

SP +3% FY May 2025 adjusted EBITDA ahead of expectations. Revenues in line. Significant broker upgrades for FY25 (but no change to FY26). Cavendish: FY25E EPS 18.7p (prev. 14.8p). Singer Cap: FY25E EPS 19.1p (prev. 14.3p). | AMBER/GREEN (Roland) [no section below] Today’s update has prompted impressive 25%+ FY25 EPS upgrades from Avingtrans’ brokers. Sadly, no detail is provided by management except to say that the Advanced Engineering Systems (AES) division performed ahead of expectations. With revenue in line but a significant increase in profit, my reading is that costs have been lower than expected and/or the company has benefited from a more favourable (higher margin) mix of sales. There’s no change to FY26 forecasts today, but these already show a significant increase in earnings vs today’s upgraded forecasts. Low statutory profitability remains a concern for me, but given the scale of today’s upgrade I’ve changed my view to be moderately positive ahead of the FY25 results. | |

Frontier Developments (LON:FDEV) (£90m) | FY March 2025 revenue £90m is ahead of exps (£85-89m). Profits and cash therefore also ahead. | AMBER/GREEN (Graham) Upgrading this to AMBER/GREEN, consistent with a high-value/high-quality StockRank where there has been a positive earnings surprise and where momentum may start to improve. Future earnings are inherently speculative, as it’s impossible to predict the popularity of new game titles. Let’s hope Frontier can apply learnings from the mixed launch of Planet Coaster 2 to the upcoming launch of Jurassic World Evolution 3. | |

Creo Medical (LON:CREO) (£57m) | The establishment of new reimbursement codes is said to encourage use of Creo’s products. | ||

Jersey Oil and Gas (LON:JOG) (£41m) | Cash £12.3m, cash run rate of c. £1.5m p.a. Funded for execution of Buchan redevelopment. | ||

Kromek (LON:KMK) (£38m) | Two orders valued together at approximately $900k, for immediate delivery. | ||

Angle (LON:AGL) (£31m) | Loss reduces 29% (£14.2m). Cash to Q1 2026. Macro uncertainty has impacted YTD revenues. | ||

Inspiration Healthcare (LON:IHC) (£18m) | Rev +1.7%. Adj. op loss £1.9m. New CEO. FY26: starts with a strong order book. Net debt £8m. |

Graham's Section

Frontier Developments (LON:FDEV)

Up 9% to 248.9p (£98m) - FY25 Update - Graham - AMBER/GREEN

This is a very brief update for FY May 2025:

Revenue for FY25 is expected to be approximately £90 million (FY24: £89.3 million), which is ahead of expectations through strong performances across Frontier's game portfolio.

The better-than-expected revenue performance, further boosted with a gain of £3.5 million on the sale of the publishing rights for the Foundry game Stranded: Alien Dawn (which is not accounted for as revenue), will deliver stronger-than-expected profitability in FY25 and a higher-than-expected cash position.

“Expectations” are confirmed in a footnote as £85-89m.

Zeus helpfully published a note back in January, which had a revenue forecast of £87.5m, a PBT forecast of £0.1m, and a net cash forecast of £28.3m.

The next major catalyst is supposed to be Jurassic World Evolution 3. This Youtube video (published three days ago) discusses how long the game release is taking: it notes that given the lack of news flow around the game so far, JWE 3 is not going to be released in time for the release of the new film, Jurassic World Rebirth.

The only official deadline given by the company (e.g. in the H1 results, discussed by Roland here) is that the game will be released “in FY26”, which means before the end of May 2026.

Graham’s view

We’ve been AMBER on this as it’s a turnaround story with the potential for the company to look cheap against future earnings - but where future earnings are highly uncertain.

Stockopedia’s calculations have noticed positive potential, giving it a “Contrarian” (high quality and high value, but poor momentum) style:

The company retains a strong cash balance - covering nearly 30% of the market cap - and hasn’t diluted its shareholders for many years, which for me helps provide quite a lot of reassurance.

I’m therefore able to give this an upgrade today to AMBER/GREEN.

I think it's worth noting that the last major release from Frontier, Planet Coaster 2, is thought to have improved considerably since its release. Again turning to YouTube to find influential reviews, I note this channel says (five days ago) “pretty much all of my complaints have already been remedied”, with bugs having been largely eliminated and with an “incredibly impressive” commitment to free content updates from Frontier.

The comments under that video are also very positive, leading me to think that Frontier has generated a great deal of goodwill with how they reacted to the mixed launch of that title.

Let’s hope they can bring what they’ve learned from this to make for a more successful launch of JWE 3!

C&C (LON:CCR)

Up 1.55% to 157.2p (£592m) - Final Results - Graham - AMBER

C&C Group plc ('C&C' or the 'Group'), the premium drinks company which manufactures, markets, and distributes branded beer, cider, wine, spirits and soft drinks across the UK and Ireland, announces final results for the 12 months ended 28 February 2025 ('FY2025').

I like to keep track of the drinks companies as they are usually some of the higher-quality names we cover.

However, C&C hasn’t been all that impressive in recent times; I was neutral on it when it published interim results last year. I said at the time “the results have been messy, returns are mediocre, and growth is limited”.

The share price collapsed 25% in March on the back of a profit warning, but has since recovered and is now back where it was before:

Today’s results for FY February 2025 show revenues only slightly higher than the prior year, at €1.67bn.

Adjusted operating profit of €77m, vs. the €80m that was expected prior to the March profit warning.

A bugbear of mine has been the level of adjustments in C&C’s accounts. For FY 2025, there are €36m of such adjustments, vs. €150m in 2024 (admittedly most of that was goodwill impairment).

This year, the main item is €24m of “restructuring costs”. Looking into the details of this, it’s the type of “exceptional item” that I’m always wary of. I have to assume that businesses generally need to be restructured in some way or another every few years, so I don’t automatically assume that the associated costs are “exceptional”.

I’m also concerned that sundry costs can get thrown in here sometimes, masking the real performance.

C&C’s unadjusted operating profit is €45.8m, and unadjusted PBT is €19.6m after some large finance expenses.

It’s unfortunate that finance expenses were so large (at €24.4m) despite the company’s modest debt load. Net debt (excluding leases) finished the financial year at €80.9m, giving rise an official leverage multiple of only 0.9x.

CEO comment excerpt:

"The Group has progressed on a number of fronts over the last year, despite the ongoing challenging macro and market backdrop. Our two leading brands, Tennent's and Bulmers gained market share and we see future growth opportunities for both. Our Premium brand performance is encouraging, benefitting from ongoing consumer appeal for premium beer and cider which is driving growth in this segment.

"Within Distribution, Matthew Clark Bibendum continued to deliver positive momentum, achieving consistently improved service levels, growing its customer base by 8%, providing great range and value.

The Outlook statement is confident, looking forward to continued improvement.

Balance sheet: tangible balance sheet equity has declined since I looked at this last year, and is now less than €30m.

Graham’s view

The StockRanks are neutral on this and I’m inclined to stay neutral on it, too. I have little doubt that the company is working hard to transform itself, and hopefully the restructuring costs will bear fruit.

Their CFO is not just their CFO - he is their “Chief Financial and Transformation Officer”, underlining how serious they are about rebooting.

To me, given the difficulties faced by the company - including reliance on the weather - these shares are fairly priced.

Roland's Section

Pets at Home (LON:PETS)

Up 3% to 271p (£1.2bn) - FY25 Preliminary Results - Roland - AMBER/GREEN

Today’s results from Pets at Home strike a more confident note than recent updates. Reassuringly, they also confirm that both FY25 results and FY26 guidance remain in line with expectations.

This is a welcome improvement from the company’s last two updates, both of which included profit warnings (for more history on this, see our 31 March coverage):

FY25 results summary: today’s accounts cover the 52 weeks to 27 March 2025. Let’s start with a look at the headline numbers:

Revenue up 0.1% to £1,482m

Reported pre-tax profit up 14.1% to £120.6m

Underlying pre-tax profit up 0.7% to £133.0m

Underlying PBT margin: 9.0% (FY24: 8.9%)

Free cash flow up 21.5% to £83.8m

Net cash (exc leases): £6.2m

Underlying EPS +1.6% to 21.0p

The group’s performance seems to have stabilised over the last year, despite ongoing headwinds from subdued growth, competition, cost inflation and the uncertainty imposed by the CMA review of large vet chains.

Adjustments to profit total £12.4m (FY24: £26.3m) and largely relate to the ongoing restructuring programme. Investors can decide whether to include or exclude them, but I don’t think they significantly change the overall picture here.

One reason why I’m relaxed about the adjustments is the group’s excellent free cash flow conversion, which represents nearly 100% of statutory net profit.

With net cash excluding lease liabilities, the only slight concern I’d highlight is that lease liabilities exceed right of use assets by £63.7m. This may suggest that Pets at Home has some loss-making stores, in addition to the disclosed impact of closed stores and its disused distribution centres (leased until Mar 26).

However, this situation could reverse over time if trading improves and looks manageable to me if it doesn’t.

Trading commentary: Pets’ business model is differentiated from peers by its integrated retail+vet model, with online retail and loyalty benefits. CEO Lyssa McGown wants to continue to broaden this offering and says the company has made significant progress over the last couple of years:

During this period of transformation, we have completely replatformed our digital infrastructure, built new capabilities around our data, brand & marketing, and simplified our distribution network to a single distribution centre fulfilling stores, online and subscriptions, and we have achieved this against the backdrop of a normalising pet care market and low consumer confidence.

Of course, it remains to be seen whether this investment will actually allow Pets at Home to increase its margins or its already-high 24% share of the UK pet care market.

Key operating metrics from last year highlight pressure on sales but show continued development of the group’s loyalty and subscription offerings:

Number of active Pets Club members +5% to 8.2m

Average Consumer Value -1.7% to £175

% Consumer Revenue from Subscriptions +3% to 13%

Clinical full-time equivalent headcount (i.e. vet staff) +6% to 3.5k

The company’s segmental reporting highlights the main challenges the business is facing – and the key risks for investors.

Retail: conditions for retailers in this sector are not easy at the moment. The pandemic pet boom is over, competition from online retailers is tough, and cost inflation from higher employment costs remains a challenge.

Pets at Home retail sales fell by 1.8% to £1,306m last year, representing a 2% like-for-like decline. Against an inflationary backdrop, presumably this suggests a fall in volumes.

However, pet care retail remains more profitable than running a big supermarket – Pets’ retail underlying PBT was £72.9m last year, giving a margin of 5.6%. Tesco’s adjusted operating margin was 4.5% last year.

Vet: the group’s in-store vet practices are split between being joint ventures and company-managed practices. For JVs, Pets receives a share of the revenue only. This explains the difference between the group’s statutory revenue of £1,482m and “consumer revenue” of £1,962m.

Pets generated £175m in revenue from the vet segment last year, converting this into £75.9m of adjusted PBT – equivalent to a 43.3% margin.

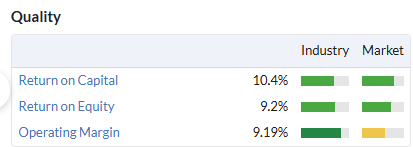

The vet business is key to the group’s profitability – without it, I suspect the retail segment alone would struggle to generate sufficient returns on capital. Today’s results show a ROCE of just over 10% for the whole group, consistent with past performance:

In this light, the CMA investigation into the veterinary sector remains a risk, ahead of the release of provisional findings in July 2025. The CMA’s initial guidance on potential remedies seems to suggest the impact will be manageable, but it’s not always easy to tell exactly what drives margins from outside a business.

Insurance: Pets at Home is launching a pet insurance offering that it hopes will leverage the size and loyalty of its customer base:

Our new insurance venture will bring a disruptive, Pets branded proposition to the c£2bn pet insurance market. Pet insurance is the largest vertical outside of Pets at Home's current core operations. It is expected, by Mintel, to grow at c4% per annum reaching c£2.5bn by 2029.

Insurance is expected to be loss making “for around 2 years”, reaching break-even during FY28. However, management believes insurance could contribute c.10% of group profits over time.

The company says it’s secured an experienced team with a 20% minority stake in the insurance venture to develop this business.

Outlook & Estimates: the good news is that FY26 guidance is unchanged today from March’s update, when management cut expectations for the year ahead.

The bad news is that Pets at Home’s profits are still expected to fall during the FY26 financial year.

Pets’ FY26 guidance is for underlying PBT of £115-125m, slightly below last year’s figure of £133m

Consensus forecasts on Stockopedia suggest FY26E EPS of 19.4p, 8% below today’s FY25 figure of 21p

These estimates price the stock on a FY26E P/E of 14, with a potential 5% dividend yield.

Roland’s view

I took an AMBER/RED view on Pets at Home in March, following its second profit warning.

I don’t see any need to maintain this negative view following today’s results. The company’s outlook seems to have stabilised and its financial position remains healthy, in my view.

Prior to today’s results, the StockRanks were styling Pets at Home as a Super Stock. Personally, I don’t think I can get onboard with a fully positive rating, for a couple of reasons:

Uncertain impact of CMA review

Expectation for falling earnings in FY26

That leaves me with a choice between AMBER and AMBER/GREEN.

This situation is not without risk. But on balance, I’m encouraged by today’s results and strategy commentary. I’m going to revert to a moderately positive view in the belief that this business can continue to develop and expand. AMBER/GREEN.

Kingfisher (LON:KGF)

Down 3% to 288p (£5.2bn) - Q1 Trading Update - Roland - GREEN

Our market outlook scenarios and guidance for FY 25/26 are unchanged to those set out in our FY 24/25 results

Today’s update from the owner of B&Q and Screwfix highlights a common historical problem with this business – France and the UK rarely seem to perform well at the same time.

In this case, sales improved in the UK but remained weak in France. Poland, the other main market, saw its performance weaken slightly from last year:

UK: Q1 figures look strong here, but Kingfisher’s management warn that strong sales of seasonal goods were “largely due to favourable weather conditions” and probably included some sales that have been pulled forward from Q2.

France: -3% LFL is not encouraging and probably implies lower volumes in some segments. However, Kingfisher says that the Brico Dépôt business has seen LFL growth in kitchen sales, while Castorama is on track with modernisation and has achieved 17% online penetration after just one year.

Outlook: guidance for the 25/26 financial year is unchanged. Helpfully, management include details of this in the footnotes:

FY26 adjusted PBT of c.£480-540m (FY25: £528m)

FY26 free cash flow of £420-480m (FY25: £511m)

Analysts have translated this to a consensus forecast for earnings of 21.5p per share, according to Stockopedia. Forecasts have remained broadly flat in recent months, which is reassuring in my view:

Roland’s view

Kingfisher has unavoidable cyclical exposure to both housing markets and broader economic health. Sales can also (genuinely) be affected by weather and other unpredictable demand drivers.

However, the group has a long track record of strong cash generation and traditionally maintained a net cash position excluding lease liabilities.

Like Pets at Home, Stockopedia’s algorithms are very positive about Kingfisher at the moment, styling it as a Super Stock:

I’m also positive about Kingfisher. While there’s still some uncertainty in my mind over whether profits will return to growth this year, I think the business is in reasonable shape and should perform well when external conditions improve.

With the stock trading on a forward P/E of 13 and showing evidence of improving momentum, I’m going to upgrade my previous neutral view to GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.