Good morning and welcome to today's report.

Update 13:45: that's all for today, see you tomorrow!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

J Sainsbury (LON:SBRY) (£6.7bn) | Q1 like-for-like sales +4.7%. Continues to expect retail underlying profit c. £1bn and retail free cash flow of >£500m. | AMBER/GREEN (Roland) [no section below] A solid performance with LFL growth ahead of inflation and market share gains. The group is reallocating non-food space to higher-performing grocery, but also reports improved performance from clothing and Argos. Nectar is also doing well and is on track to launch an in-house ad network later this year. Broker ShoreCap has left forecasts unchanged today, but I think good operational momentum and a forecast FCF yield of 7.5% justify upgrading to a moderately positive view. This is also reflected in recent StockRank gains. | |

Burford Capital (LON:BUR) (£1.9bn) | A New York court has ordered Argentina to transfer its shares of YPF. A positive development. | ||

Supermarket Income REIT (LON:SUPR) (£1.1bn) | £215m term loan. SUPR will receive 50% of the proceeds. SUPR’s loan-to-value is c. 31%. | ||

PayPoint (LON:PAY) (£594m) | Second tranche of buyback programme for up to £30m, ending no later than March 2026. | AMBER/GREEN (Roland - I hold) [no section below] | |

Judges Scientific (LON:JDG) (£590m) | Will support CEO as Judges continues to execute its strategy. He was most recently at Oxford Instruments (LON:OXIG). | ||

Warehouse Reit (LON:WHR) (£480m) | “No increase” statement regarding Blackstone’s offer is no longer in effect. Considering its options. | PINK | |

Elixirr International (LON:ELIX) (£326m) | Cancelled from AIM, admitted to the main market. “Reflects our continued ambition.” | ||

CLS Holdings (LON:CLI) (£279m) | Total €41.3m. Office/industrial and office. 10% discount to Dec 2024 valuations. New LTV 47%. | ||

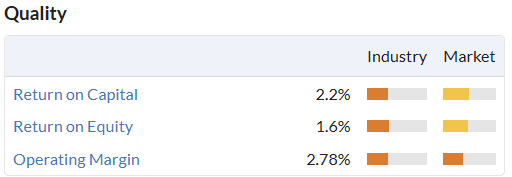

Kitwave (LON:KITW) (£269m) | PW. Consumer fragility. Unable to offset higher NICs. Now expects adj. operating profit £38-40.5m. | BLACK (AMBER/RED) (Megan) A weaker outlook for the seasonally important second half has sent investors scurrying. This may prove to be an over-reaction, but I am uncomfortable with the fact that this profit warning comes less than two months after a trading update which said everything was good. | |

Supreme (LON:SUP) (£241m) | Robust trading. PBT +3% (£30.9m). Positive start to FY26, trading in line with exps. FY25A EPS: 21.6p FY25E EPS: 17.9p (average of 3 estimates published today) | AMBER (Roland) This is a good set of results, but I’m reluctantly downgrading our view on Supreme. Today’s outlook and updated broker estimates suggest to me that earnings could fall by a double-digit percentage this year. There’s also continued uncertainty about the outlook for vaping sales, in my opinion. In fairness, I think the enlarged drinks and wellness business has the potential to make an improved contribution that may offset any decline in vaping over time. However, overall uncertainty means I think a neutral view is appropriate for now. | |

Synthomer (LON:SYNT) (£179m) | Agrees with banks to extend covenant relaxation to end of 2026, given weaker macro conditions. | ||

Augmentum Fintech (LON:AUGM) (£170m) | NAV per share after performance fee 161.5p (last year: 167.4p). Seeking ways to narrow discount. | ||

Mercia Asset Management (LON:MERC) (£136m) | Third-party FUM +10% to £1.8bn. Adj. op profit £10.2m (last year: £9.7m). NAV per share 43.6p. | ||

Eurasia Mining (LON:EUA) (£134m) | Rev +220% to £6.6m, net loss increased to £8.7m. NAV £12.6m. Focus on sale of Russia assets. | (RH) Results to Dec 2024 being published in July are a red flag. | |

MPAC (LON:MPAC) (£129m) | PW. Q2 orders down due tariff uncertainty. FY rev to be significantly below exps. ShoreCap FY25E adj EPS -24% to 33.5p. Buy-in for DB pension. | BLACK (AMBER/RED) (Roland) A shortfall in Q2 orders seems likely to have a significant knock-on effect. Broker notes translate today’s revenue warning into a c.25% cut to profit expectations for 2025. I’m also a little concerned by the decision to downsize US operations that were previously lauded. Mpac has a mixed track record and poor quality metrics. The StockRanks appear to have spotted a weakness in April’s results and had already downgraded the shares to a Value Trap. Given the risk of further downgrades, I’d be inclined to steer clear until some clarity emerges. | |

John Wood (LON:WG.) (£128m) (shares suspended) | Lenders have agreed to extend debt waivers to 31 July 2025. Remains in talks re. Sidara bid. | ||

Wynnstay (LON:WYN) (£85m) | Rev -7.2%, gross profit +7.1% to £42m. PBT +25% to £5.5m. On track for full year forecasts. | GREEN (Roland - I hold) [no section below] Today’s results suggest to me that Wynnstay’s turnaround and cyclical recovery under CEO Alk Brand is on track. Profitability is improved in H1, despite mixed performance on volumes. The balance sheet also remains strong, with net cash of £10.3m at the peak point for working capital (i.e. low point for cash). There’s no change to broker forecasts today. With the stock still yielding nearly 5% and trading c.25% below tangible book value, I’m happy to maintain our positive view. | |

Anexo (LON:ANX) (£81m) | Discussions with DBAY party remain ongoing. PUSU deadline extended to 5pm 15 July 25. | PINK | |

Kooth (LON:KOO) (£67m) | California DHCS has published a report into the use of Kooth’s Soluna service by 13-25 year olds. | ||

Windar Photonics (LON:WPHO) (£52m) | 2024 rev -8%, record shipments of €5.8m. EBITDA loss €0.5m, net loss €0.9m. €7.1m cash at 31 Dec. | (RH) Results to Dec 2024 being published in July are a red flag. | |

Gelion (LON:GELN) (£42m) | System now in advanced commissioning. 92.5% revenue (£900k) recognised in H1. | ||

Challenger Energy (LON:CEG) (£19m) | Sale has made “considerable progress” but not yet finalised. New longstop date 30 Aug 25. | ||

Itaconix (LON:ITX) (£15m) | BIO*Asterix can be used to replace fossil-based products used in paints, coatings & adhesives. | ||

Westminster (LON:WSG) (£12m) | Personnel screening solution for a leading global science at chemicals company at a UK site. |

Megan's Section

Kitwave (LON:KITW)

Down 25% to 238p (£268m) - Interim Results - Megan - (BLACK) AMBER/RED

It’s not the numbers being reported on in these interim results that have sent investors scurrying out of Kitwave this morning, but the outlook. After a slowdown in volumes and the additional costs arising from national insurance contributions, management has confirmed annual adjusted operating profits between £38m and £40m.

It’s worth breaking down why that is problematic.

For a start, the last update from the company was 7 May and then management suggested that everything was ticking along nicely. The bulk of that update focused on the seasonally less important first half of the year, but chief executive Ben Maxted did note the second half weighting and confirmed his confidence in the group’s ability “to meet full year expectations”.

Secondly, management has said this morning that it no longer has confidence that the £2m of additional national insurance costs can be offset. The trouble is that the market sentiment has weakened and with volume lower, the company is less likely to be able to hike prices.

The fact that it has taken less than two months for such a sharp turnaround in sentiment seems a little worrying.

Then there is the fact that the second half is seasonally so important to Kitwave. In 2024, the company reported £10.8m of operating profits in the first half and £23.2m in the second. This morning, management has reported £13.2m of operating profits in the first half, a 22% increase on the previous year. Taking the low point of current forecasts, second half operating profits could be as little as £24.8m - just a 6% improvement on the second half of last year.

And finally there are the material downgrades from brokers. Now, it wasn’t clear before today exactly what management at the company expected for the full year, but brokers at Canaccord Genuity were forecasting EBITDA of £61.1m in 2025, compared to £45.2m last year. The annual forecast has now been downgraded to £54.3m, with cuts to both FY26 and FY27 forecasts as well.

Beware the fate of multiple profit warnings

Despite management’s previous insistence that the company would be able to offset higher NI costs, brokers had already downgraded forecasts this year. Another big cut today, plus the major share price sell off will have disrupted the momentum which had recovered strongly in Q2.

Profit warnings don’t always come in threes, but the fact that this one seems to have come out of the blue doesn’t instill a great deal of confidence that management have got a grip on things.

Added to the fact that this profit warning is a reflection of fundamental weakness in the market, rather than a one-off miscalculation, and I wouldn’t be surprised if we see another disappointing announcement before the year is out.

There are also still relatively heavy adjustments going on after the slew of acquisitions made in the last few years. Reported operating profits were £10.3m, which is an operating margin of less than 3% - not a lot of wiggle room for further disappointments.

Megan’s view:

This has been a strong performer since its 2021 IPO so this morning’s announcement will no doubt be disappointing.

Following this morning’s sell-off and broker downgrades, shares are trading on 8.8x adjusted diluted forecast earnings, which looks tempting. But I would be wary of things getting worse before they get better. AMBER/RED

Roland's Section

MPAC (LON:MPAC)

Down 26% to 318p (£95m) - Trading Update & DB Pension Update - Roland - (BLACK) AMBER/RED

This high-speed packaging and automation group has warned today that a shortfall in orders during the second quarter means that full-year revenue will now be “significantly below the Board’s previous expectations”.

Brokers have slashed their earnings forecasts for the year and the market reacted brutally in early trading:

What’s gone wrong?

Mpac says that performance during the first half of the year was in line with expectations, thanks to a strong order book in January and good performance from last year’s acquisitions.

However, the core Mpac business saw a slowdown in order intake during the second quarter. Management says this was due to uncertainty over US tariffs and low consumer confidence.

As a result, the closing order book for June is expected to be c.£90m, compared to £118.5m at the end of 2024.

The second quarter is generally an important period for this business as it lines up production volume for the second half of the year, to which profits are normally weighted.

As a result of this shortfall, management now expects FY2025 revenue to fall significantly below the Board’s previous expectations.

Net debt is now also expected to increase “marginally” from the £37.5m position reported at the end of 2024.

Unhelpfully, Mpac has not provided any comment on the expected shortfall in revenue or the likely impact on profit. The company has not included details of previous consensus estimates in today’s RNS either. All of this means that investors without access to broker notes are left in the dark.

Updated estimates

Fortunately, Shore Capital and Equity Development have both provided updated forecasts today through Research Tree – many thanks for making this coverage available.

Updated estimates suggest earnings in 2025 and 2026 will now be significantly lower than previously forecast, although I would guess the outlook beyond the current year remains uncertain and may depend on tariffs and broader macro issues.

Shore Capital:

FY25E EPS -24.6% to 33.1p (prev. 43.9p)

FY26E EPS -31.9% to 36.8p (prev. 54.1p)

Equity Development has taken a slightly more bullish view on prospects for 2026:

FY25E EPS -29% to 32.2p (prev. 45.1p)

FY26E EPS -22% to 42.9p (prev. 54.7p)

US restructuring

To address low capacity utilisation in the US, Mpac is planning to close its Cleveland Ohio factory and consolidate its operations to its Boston location, which was acquired in 2024. Capacity is also being cut at a location in Canada.

This restructuring is expected to incur a non-cash impairment charge of c.£11.5m. I assume there will be cash costs too, but these aren’t mentioned today.

However, assuming the changes are executed successfully and Mpac retains sufficient capacity, the reduced cost base resulting from these changes could result in stronger positive operating leverage when demand does recover.

UK Pension Buy-In

Mpac has agreed a pension buy in transaction with Aviva (I hold) for £249m. No further contributions will be needed and the company expects to receive a surplus of £5m when the buy out is completed (around two years).

Roland’s view

Mpac’s position seems to be that the company has maintained its market share, but that customers just aren’t buying. Time will tell if this is true, but near-term profitability seems likely to take a serious hit as a result of this disruption to order flow.

I don’t know the history of the group’s North American operations, but I’m a little surprised they are being downsized so quickly. Today’s update talks about taking the opportunity to “accelerate its plans to consolidate its operational footprint in the US”.

However, checking back to the full-year results (published just two months ago, at the end of April), I don’t find any mention of this. Instead, the company talks about the opportunity created by its enlarged manufacturing footprint:

Notably, the expanded operational footprint of the Group now includes two build facilities in the US, along with facilities in Europe, Canada and the UK, positioning Mpac well to respond flexibly to these long-term trends.

I may have missed something, as I don’t follow this company in detail. But the comment above doesn’t suggest to me that Mpac was thinking of consolidating its US operations at that time.

This leaves me wondering if today’s decision to close the Ohio plant is actually being driven by fears of a prolonged loss of business in the US, or perhaps by cost/debt concerns.

Today’s share price fall largely reflects the reduction in earnings forecasts for this year, leaving Mpac on a forward P/E of around nine.

Personally, I don’t see much attraction here. This business already had very poor quality metrics prior to today and is styled as a Value Trap by the algorithms.

I think this is a situation where it makes sense to follow the StockRanks. I’m also intrigued to see that this is another example of where the algorithms picked up on potential weakness at the time of Mpac’s results, before the market seemed to sense any problems:

This pattern is something I discussed in more detail in an article in May – it’s not the first time I’ve seen this happen this year.

Mpac has a chequered history with periodic disappointments. I can’t help feeling this might be the latest of these to hit shareholders. History tells us that an initial downgrade is often followed by further disappointments. Mpac’s debt burden is an added concern for me. AMBER/RED.

Supreme (LON:SUP)

Down 5% to 195p (£231m) - Full Year Results - Roland - AMBER

Supreme (AIM:SUP), a leading brand owner, manufacturer, and supplier of fast-moving consumer goods, announces its audited results for the year ended 31 March 2025 ("FY25" of "the Period").

I have an interest in well-run distribution businesses and I know I’m not alone among Stocko subscribers in having followed Supreme’s progress with interest.

Like many of you, I’ve always been slightly unsure just how much of a valuation discount is appropriate to reflect the group’s dependency on vaping products. This issue doesn’t seem likely to go away, as I’ll discuss. But today’s results look solid to me and do not seem to flag up any other concerns.

I think this morning’s modest share price weakness is probably due to uncertainty over the impact of the June 2025 UK ban on selling disposable vapes and some caution on the outlook. Let’s take a look.

FY25 results

Revenue for the year rose by 4% to £231.1m, supporting a 3% rise in pre-tax profit to £30.9m. Adjusted earnings are reported up 3% at 21.6p per share, which appears to be slightly ahead of Stockopedia consensus for 20.7p per share.

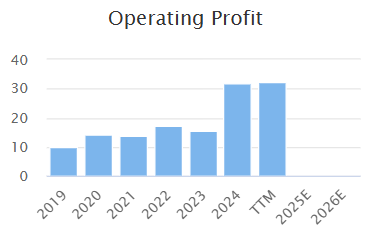

While Supreme ended the year with modest net debt of £12.3m, this reflects c.£25m of acquisition spend during the year and doesn’t look a concern to me. My sums show the business generating almost £21m in free cash flow excluding acquisitions, demonstrating excellent conversion from net profit of £23.5m.

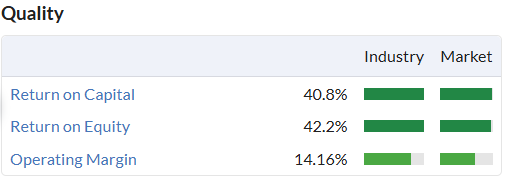

Profitability also remains strong, with an operating margin of 14.1% and return on capital employed of 35.7%. Both figures are consistent with last year, with lower ROCE reflecting the addition of new assets through acquisitions that have not yet contributed a full year to earnings:

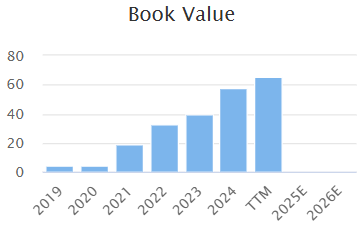

If Supreme can continue to increase capital employed while maintaining this level of profitability, then this should create value for shareholders as the group’s earning power will improve. We can see this has happened to some extent already since the group’s 2021 IPO:

Dividend: shareholders will receive a total dividend of 5.2p for FY25, a 10% increase on the previous year. This gives the stock a trailing yield of 2.6%. Not that exciting, but well covered and supportable alongside growth investments.

Divisional trading: growth vs decline?

Supreme has used these results to debut its new operational structure:

Vaping

Drinks & Wellness

Electricals

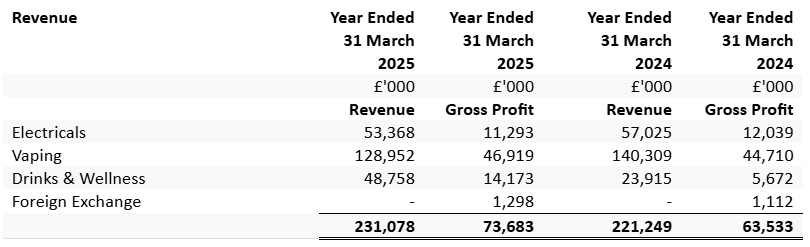

This table from the footnotes to today’s shows the performance of each category last year:

A few points I’d note from these segmental results.

Vaping: sales fell by 8% to £129.0m, but gross profit from this division rose by 5% to £46.9m, giving a gross margin of 36.4% (FY24: 31.9%).

This improvement in profitability reflects a 23.5% fall in disposable vape sales to £54.1m, partially offset by 8% (£5m) increase in sales of non-disposable vapes and margin expansion in the group’s core 88vape business.

Supreme prudently wound down stocks of disposable products last year, but the ban on disposable vapes in the UK only came into force in June. This means it isn’t yet reflected in these figures and we can’t be sure how sales patterns may change over the coming year.

The expected introduction of new taxes on vaping from October 2026 adds another unpredictable variable to the equation, as does the suggestion I’ve seen in some recent data (not from Supreme) that vaping adoption may have peaked in many markets.

On the other hand, I accept the company’s suggestion that impending tighter regulation in this market could lead to sector consolidation that would be beneficial for Supreme, as a larger player.

The reality is that vaping still accounts for 55% of group revenue and 64% of gross profit, so remains highly material to the equity valuation despite growth elsewhere.

Drinks & Wellness: CEO Sandy Chadha seems to be positioning this division to take over the growth mantle from vaping. Last year saw the acquisition of Clearly Drinks and Typhoo tea, which brought with it a number of other potentially attractive brands to sit alongside the company’s existing wellness and sports nutrition products.

Clearly and Typhoo are both brands with c.£20m annual sales and account for the majority of last year’s sales growth.

Supreme says Clearly is now generating “an almost 40% gross margin” while loss-making Typhoo has been returned to profit at an EBITDA level. Management have clear plans for further improvements at this iconic tea brand:

In the four months under Supreme's ownership, the business reported revenue of £6.1 million and contributed positively - albeit modestly - to the Group's Adjusted EBITDA position. In these four months, the priority has been to stabilise the brand and its positioning in the market, determine a cost-effective and ethical supply chain, and re-establish inhouse manufacturing.

I am inclined to see this as an attractive opportunity. My impression is that Supreme’s product development and distribution capabilities could deliver attractive results here.

Electricals: this division was previously Batteries & Lighting. Perhaps unsurprisingly, both of these product ranges are seen as being in structural decline. Supreme says its offerings outperformed the wider market, gaining share.

Even so, revenue fell by 6% to £53.4m last year in this segment. Profit contribution was also weaker, with a lower gross margin (21%) than either Vaping or Drinks & Wellness.

Outlook unchanged

The outlook commentary sounds positive:

Supreme has made a positive start to FY26 and expects to deliver another profitable and highly cash-generative year, trading in line with current market expectations.

However, the problem is that current market expectations suggest a modest fall in profits this year.

Consensus forecasts provided in today’s RNS are for revenue of £236m and adjusted EBITDA of £36.5m. This adjusted EBITDA figure is 10% below the £40.5m FY25 figure reported today.

Forecasts on Stockopedia ahead of today also reflected this expectation, with a consensus EPS figure of 19.6p for FY26:

Checking through broker notes shows a range of forecasts, two of which are notably below current consensus:

Zeus - FY26E EPS: 17.4p (unch)

Shore Capital - FY26E EPS: 16.7 (newly introduced)

Equity Development - FY26E EPS: 19.5p (prev. 19.7p)

Assuming the Zeus and ShoreCap figures form the consensus provided by Stockopedia’s data provider, I suspect we could see a modest downgrade feed through to the StockReport in the coming days.

Taking the average of these three estimates gives me a figure of 17.9p, 17% below today’s FY25 result. That would leave Supreme trading on a FY26E P/E of 11.

Roland’s view

I think these are a good set of results from a well-run and reasonably-valued business. The elephant in the room remains the outlook for the vaping business, in my view. Given that this contributes nearly two-thirds of Supreme’s gross profit, investors can’t afford to ignore this risk.

My view is that Supreme is relatively well positioned to handle increased regulation and consolidation in this sector. But the likely impact of greater regulation and tax levies on vaping sales is not clear to me.

I was AMBER/GREEN on Supreme when I last covered the shares, but I don’t think I can maintain this view today. The combination of vaping uncertainty and the seeming likelihood of a fall in earnings for FY26 means I am going to moderate our view to neutral.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.