Good morning - we've finished the Agenda now! For a Thursday, it's not overly busy today.

Spreadsheet accompanying this report: link.

Finished for now, see you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

3i Infrastructure (LON:3IN) (£3.13bn) | Portfolio companies generally performing in line/ahead of exps. On track for FY26 divi 13.45p. | ||

| Frasers (LON:FRAS) (£3.09bn) | New Term Loan and Revolving Credit Facility | £1.65bn facilities replaced by new 3-year £3bn facility. Can be extended by up to 2 years/£0.5bn. | AMBER/GREEN (Mark) [no section below] |

Baltic Classifieds (LON:BCG) (£1.71bn) | Adj. net income +21% (€54.4m). Outlook: rev growth close to FY25, EBITDA margin maintained. | ||

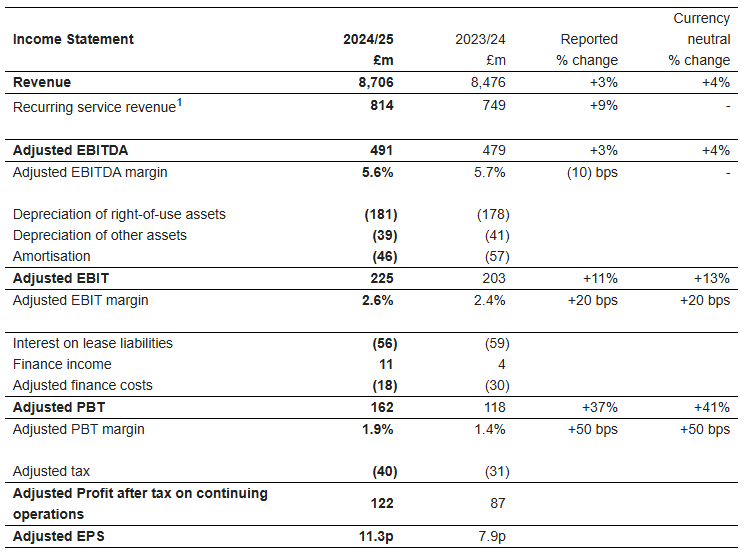

Currys (LON:CURY) (£1.34bn) | Adj. PBT +37% (£162m). Net cash £184m. Early trading in line, comfortable with market exps. | AMBER/GREEN (Mark) Strong improvements in profitability are mostly due to lower amortisation and net finance costs. While good news, this is not as reliable as stronger operating performance. FY26 is guided in line, which means EPS is flat in the near-term on cost concerns. However, I see little reason not to stick with our existing view while it is on a modest multiple and the Momentum Rank remains high. | |

Great Portland Estates (LON:GPE) (£1.38bn) | Strong leasing momentum has continued. £20.6m of new leasing deals, 6.7% ahead of ERV. | ||

Watches of Switzerland (LON:WOSG) (£984m) | Adj. EBIT +12% (£150m). Outlook: 6-10% LfL rev growth, adj. EBIT margin flat to -100bps vs FY25. | AMBER (Graham) Reducing my stance on this down to neutral as these results don't seem to inspire confidence. The adjustments in these accounts are very heavy due to showroom impairments and showroom closures, and the tariff picture is uncertain but decidedly negative as things stand. Perhaps not all that much has changed, but I think some caution is warranted. | |

Chesnara (LON:CSN) (£444m) | Acquiring HSBC Life (UK) for £260m. Funded through internal cash, RCF debt and £140m equity raise. The effects are forecast to include “increased free float and expected eligibility for FTSE 250 inclusion increasing liquidity in the Company's Ordinary Shares.” Chesnara points out that the price of the acquisition is only 83% of HSBC Life (UK)’s “own funds” (£314m) as of Dec 2024. | AMBER/GREEN (Graham) Chesnara is a collection of primarily closed books of insurance business, with some new business lines. It has a long history of steady, growing dividend payments to its patient shareholders (yield is currently c. 9%). Today’s announcement marks a step-change in the company’s progress, bringing in an additional £4bn of assets under administration and >450,000 policies. According to its website, Chesnara finished 2024 with £14bn AUA and 940k policyholders. I can’t argue with the rationale put forward by the company today: the deal seems to be priced at bargain levels (at a discount to the “Own Funds” being acquired), although I would like to see further proof of this. Chesnara says that its investment grade credit rating will be maintained and that leverage will subsequently reduce. It is difficult to say anything with conviction as more detailed research would be required, but I can tentatively give this an AMBER/GREEN colouring. FTSE-250 inclusion will mean more passive funds and international investors buying into Chesnara, which should helpfully raise its profile and make it even easier to do deals like this in future. | |

Peel Hunt (LON:PEEL) (£114m) | “Group revenue for Q1 FY26 is comfortably ahead of the equivalent prior year period, which itself was a good quarter…strong pipeline of M&A transactions…continued to add excellent clients…” | GREEN (Graham) There are signs of life coming back to UK investor appetite, and I'm hopeful of renewed IPO/M&A activity. Peel Hunt says they are "mandated on a number of transactions that are expected to complete in the second half of our financial year should market conditions be supportive". Profits are unpredictable, but I continue to like the risk:reward here. | |

Intercede (LON:IGP) (£110m) | 26Q1 contract wins & renewals worth $1.5m in aggregate. “Group's momentum from FY25 into FY26.” | ||

Activeops (LON:AOM) (£104m) | Rev +14% to £30.5m, PBT +30% to £1.3m, EPS +31% to 1.55p, Net cash £20.6m. “Trading in the first few months of FY26 has been in line with the Board's expectations, including sales of ControliQ to three new customers and expansion within existing customers.” | AMBER (Mark) | |

Crystal Amber Fund (LON:CRS) (£88.3m) | 98% owned Morphic Medical Inc has received CE Mark certification for its RESET® therapy which isthe first endoscopic, non-surgical treatment for both obesity and Type 2 diabetes in Europe. | ||

| Atome (LON:ATOM) (£27.3m) | GCF approves $50m concessional finance for Villeta | “Board of GCF [Green Climate Fund] has approved US$50 million of concessional finance for the Project, through the International Finance Corporation, part of the World Bank Group, as Accredited Entity” | |

| Blackbird (LON:BIRD) (£16.5m) | £2m Placing & £200k Retail Offer | 13.5% of enlarged share capital placed at 3p per share, a discount of around 30%to the closing mid-market price. Directors put in £135k. £200k retail offer on same terms. | RED (Mark) [no section below] |

Kazera Global (LON:KZG) (£16.0m) | “Twelve double-stage spirals, used to improve separation efficiency and concentrate quality, have now been successfully installed at the WHM site. Delivered on time and within budget, the spirals represent a key upgrade to the processing plant.” | ||

Pennant International (LON:PEN) (£12.3m) | Sale of the final two freehold units now completed on a sale-and-leaseback basis at a small loss to BV. Net proceeds to reduce overdraft borrowings. Seeing increased interest in its products and services…2025 revenue anticipated to be significantly H2 weighted ....remain confident will meet market expectations for the full year. | AMBER/RED (Mark) |

Graham's Section

Peel Hunt (LON:PEEL)

Up 5% to 97.75p (£120m) - AGM Trading Update - Graham - GREEN

Peel Hunt Limited ("Peel Hunt" or the "Company") today provides the following trading update in relation to the three-month period ended 30 June 2025 ("Q1 FY26").

I already commented on Peel Hunt in June - here - when it published full year results.

Those results saw revenues grow 6%, but the company did make a £3.5m pre-tax loss, after restructuring costs. Headcount fell 5%.

Let’s see what the company has to say for Q1:

We have had a strong start to our new financial year as market conditions have begun to improve. We have seen higher revenue generation in our Institutional and notably our Execution Services businesses, together with a significant contribution from M&A transactions. Consequently, Group revenue for Q1 FY26 is comfortably ahead of the equivalent prior year period, which itself was a good quarter.

What many investors are really hoping for is an IPO/M&A boom and the windfalls that this provides.

Here are the clues from the company on this front:

We continue to have a strong pipeline of M&A transactions, with a number of situations both announced and in process. It remains to be seen whether a more general pick up in equity issuance and IPO activity will follow. Whilst the macroeconomic background is hard to predict, investor confidence appears to be increasingly resilient, and we are mandated on a number of transactions that are expected to complete in the second half of our financial year should market conditions be supportive.

Estimates: existing consensus forecasts suggest that PEEL’s revenue will increase by a further 9% this year to £99.8m, while adjusted PBT will improve to £3.8m (perhaps relying on fewer adjustments this time?).

Graham’s view

It’s plain to see that current earnings do not support the valuation here. What does support it is balance sheet net assets of £89m, and the hope that the IPO market can recover. The IPO boom of 2021 saw Peel Hunt generate after-tax net income of £11m in FY March 2022.

(That IPO boom caused Peel Hunt itself to float on the market, at an IPO price of 228p. It currently trades at less than half of that.)

I do think that in recent weeks, there has been a return of “animal spirits” to the UK stock market.

This can be seen with the likes of Smarter Web (OFEX:SWC), where I think that based on the current share count, the valuation is close to £800m. This is an Aquis-listed web design company that owns £60m of bitcoin and has £38m of cash “available to be deployed into bitcoin”.

While it might seem crazy, the positive aspect of the bubble in “bitcoin treasury” companies is that it shows there is some element of retail investor appetite that has come back to the UK. This does at least lay a foundation for IPOs and other corporate activity - although the likes of Peel Hunt will need some proper institutional investor appetite, too.

Overall, I’m happy to stay GREEN on this one.

Rather like Numis (taken over by Deutsche Bank in 2023), I think a larger bank might see strategic value in Peel Hunt. And with a large chunk of the market cap supported by tangible assets, it might not be the riskiest takeover target.

Watches of Switzerland (LON:WOSG)

Down 8% to 389.2p (£909m) - FY25 Results - Graham - AMBER

It’s quite a harsh share price reaction to these FY April 2025 results, which are in line.

Turning to the outlook statement, we find this table:

The revenue growth projection seems fine - it’s even better than the revenue growth forecast currently on the StockReport, for example.

However, the possible reduction in the EBIT margin stands out as a clear negative. The company says its guidance is informed by the following assumptions (plus some others):

Current US tariff rate of 10% maintained beyond the 90 day pause

Currently announced margin changes from brand partners in response to the 10% tariffs remaining in place. As it stands today, the 10% tariff on imported goods from Switzerland has led some of our brand partners to put through mid-single digit price increases in the US, alongside reducing their authorised distribution network's margin percentage…

So it boils down to how the cost of the tariffs will be borne. If I’m reading it right, the brand owners are saying that the consumers should take half of the hit (“mid-single digit price increases in the US”). And the distributors - such as WOSG - are also being asked to take some of the hit, with a lower margin percentage.

We don’t yet have total clarity on the situation:

The outcome of US tariff developments remains uncertain. We are in regular dialogue with our brand partners, but it is too early to comment on the potential sector impact of further changes. We will provide a further update as to the potential impact on FY26 guidance once the situation becomes clearer.

CEO review snippets

I note that 48% of WOSG’s revenue came from the US in FY25. Perhaps this is a stock that might benefit from a US listing or could attract US takeover interest at some point?

More broadly, the luxury watch market is something I’ve liked to comment on in recent years, as it’s been a source of great drama. But it’s calm now:

The luxury watch category is strong, resilient and offers long-term consistent growth. In recent years, the impact of the global pandemic has resulted in a period of unprecedented volatility. We believe the market has now normalised and secondary market prices have stabilised at above pandemic levels.

WOSG’s new flagship Rolex boutique on Old Bond Street “has exceeded expectations”.

Net debt has jumped to £96m (from a net cash position) with the main reason for that being the $130m acquisition of Roberto Coin Inc, which is the US distributor of the Roberto Coin brand.

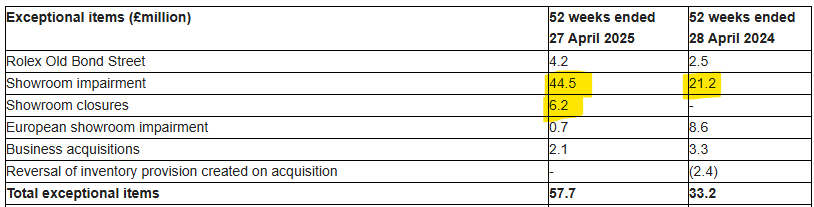

Exceptional items

Adjusted PBT is £136.1m (FY24: £128.9m), but actual PBT is only £75.9m.

The “exceptional items” creating this disparity are very large, and look like this:

I struggle to think that showroom impairments or the closure of underperforming showrooms should be ignored as “exceptional”.

In balance sheet terms, the showrooms appear in PPE and right-of-use assets. Aside from inventories (watches and jewellery), these are WOSG’s most valuable assets. And when their value gets written down, whether that’s due to external macro factors or something else, I think it’s important to take this seriously.

The impairments do show up on the balance sheet, and the balance sheet doesn’t strike me as particularly strong: while the company does have tangible net assets of £235m, PPE/right-of-use assets stand at £551m. So there is plenty of scope for further impairments and closures to take chunky bites out of tangible NAV.

Graham’s view

The WOSG share price is only a little lower than it was when I looked at it in May and reiterated my AMBER/GREEN stance.

I am wondering if a switch back to AMBER would make sense?

Some of the positives are:

P/E multiple only 10x

US exposure tends to be a positive

Further top-line growth expected and a stable watch market.

Some of the negatives are:

Dirty accounts with heavy adjustments, even heavier than last year.

Capex-heavy balance sheet and now carrying some financial net debt (although it should be manageable).

Margin pressure in this tariff environment with continued tariff uncertainty.

If the company was a little higher up the quality spectrum I’d be more confident, but this is a retailer and distributor that does not own any of the underlying brands. Given its exposure to numerous factors beyond its control - including the strategies of the brand owners themselves - I’m therefore inclined to take this opportunity to downgrade my stance to neutral.

I think it’s very important to be selective in the retailing sector, given how frequently things can and do go wrong. WOSG is making me a little nervous with these results and outlook statement, so I’d rather be neutral

Mark's Section

Pennant International (LON:PEN)

Flat at 28.5p (£12m) - Business Update - Mark - AMBER/RED

Sale-and-leasebacks:

I have been critical of IFRS 16 in the past. This accounting standard aims to ensure lease assets are not treated separately from owned assets. The asset is included in the balance sheet, but so is the liability that arises from a lessee having agreed to make a series of payments over time. The lease liability is treated as debt. This has a knock-on effect that many companies that lease property, such as retailers, appear to be heavily indebted, whereas they often profitably operate a number of stores that they don’t own the building.

When analysing a company, I often find it more accurate to treat the net lease liability as debt, rather than the entire amount. Where this has been caused by impairments, this provides a more accurate reflection of the additional cash losses that will need to be paid by the business due to the initial trading assumptions when they took out the lease proving false.

The other downside of IFRS 16 is that it inflates EBITDA, as lease costs are treated as depreciation and interest. EBITDA is no longer a proxy for the possible cash generation of a business if it got in trouble and has to cut all capex (which is why banks often have covenants based on this metric).

However, today’s announcement from Pennant highlights why IFRS16 may be useful:

The Company is pleased to report that the sale of the final two freehold units at Staverton Connection (Units D1 and D2) has now completed on a sale-and-leaseback basis.

The aggregate sale consideration for the final two units is £1.125 million (excluding VAT). Pennant remains in occupation of the two units under a full repairing lease which has been entered into for a five-year term, with a three-year 'tenant only' break clause. The annual rent is £95,000 (exclusive of VAT, utilities and related outgoings).

Here, Pennant has sold freehold units but still wants to use them, so they have agreed to rent them back. They are still responsible for the maintenance and upkeep of the properties and are paying rent equivalent to 8.4% of the property's value. A quick look at the balance sheet reveals why this is:

In their annual results, they said:

On 31 December 2024 the Group had available bank overdraft facilities, for use by its UK trading entities and provided by HSBC UK, of £3.5 million (2023: £4 million). During April 2025 the facility was extended for a further 12 months at a lower facility limit of £2 million which reflects the reduction in secured assets (sale of Land & Buildings).

Any overdraft arising from the facility is repayable on demand and carries interest at 2.50% (2023: 2.50%) plus the bank's base rate. Any facilities used are secured by fixed and floating charges over the assets of Pennant International Group plc, Pennant International Limited and by cross-guarantees between those companies.

I wouldn’t be at all surprised if this property realisation strategy has been pushed upon them by a bank only willing to renew their overdraft if they sold their freeholds and significantly reduced the amount owed. HSBC say their business banking base rate matches the BOE base rate, currently 4.25%, so the overdraft is currently costing 6.75%. This makes the 8.4% equivalent lease yield look expensive. Especially as this won’t benefit from an interest rate cycle that is forecast to be downward in trend. Overall, this transaction looks a lot like swapping one form of debt for another, but at a higher interest rate. In this respect, IFRS 16 actually does a good job of revealing the underlying nature of the transaction.

Trading:

With remaining non-lease PP&E on the balance sheet at less than £0.5m and net current assets barely positive, a lot now rides on the company’s ability to trade profitably. Things sound positive:

The Company is seeing increased interest in its products and services and, together with a growing pipeline of opportunities for 2025 and beyond, the Q2 2025 outcome of the UK Government's defence spending review augurs well for the remainder of the financial year and in the medium term.

However, when it comes to the details, the dreaded H2-weighting raises its ugly head:

As expected, 2025 revenue is anticipated to be significantly second-half-weighted, particularly noting the likely award date for the GenFly contract and delayed project work through Q2 within the Company's Track Access (rail) business.

The Directors remain confident that the Group will meet market expectations for the full year, with the second half revenue weighting achievable through the continued delivery of existing contracts, execution of Pennant's 'go to market' strategy for the Auxilium suite, and successful conversion of the GenFly contract (which is expected to contribute circa 15% of 2025 revenue).

They say that this significant H2-weighting was expected, but in the final results in April, this was not mentioned. At that time, they said:

We have made a solid start to 2025 and the Board is pleased with the buoyant bid activity to date which should set us up for success in the current year and beyond. The board is confident that the trading remains on track with market expectations.

Market expectations here are Cavendish’s forecasts of 0.12p EPS for FY25 and 1.7p for FY26. There must be some doubt now as to whether they will achieve these. And even if they do, a 2026 P/E of 17 looks expensive. It is no wonder that what little Momentum the shares had is ebbing away, and the algorithms rate this as a Momentum Trap:

Mark’s View

When I looked at this briefly following their annual results, my view was that this company was AMBER/RED, saying, “It always amazes me that this company manages to keep going with net debt and ongoing losses. This time, it is the sale of commercial properties for around £3m post-period end that gives them some breathing room. However, this is the last hurrah, as they look to be out of anything else they can sell. This means that they will need to generate positive cash flow from trading relatively soon. History suggests they will struggle with this endeavour.” Today’s trading statement reinforces this view.

Activeops (LON:AOM)

Up 3%to 150p - Final Results - Mark - AMBER

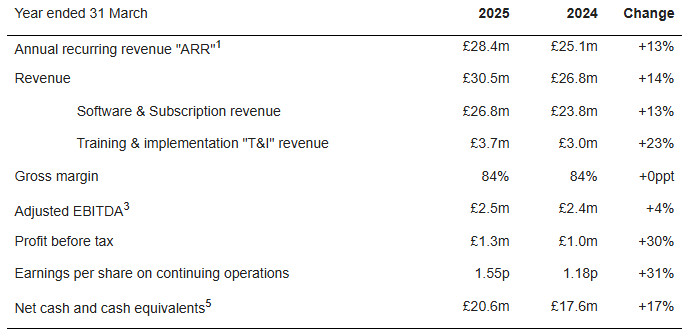

These are strong results, with revenue up 14%, and with decent gross margins this means significant operational gearing and EPS rising by an impressive 31%:

ARR and SaaS have become investor buzzwords over the last few years, so I can’t help but note that non-ARR revenue is actually growing faster than ARR. However, this may actually be good news when this is related to training and implementation. They say:

T&I revenues have increased to £3.7m (2024: £3.0m) returning to more normalised levels, predominantly driven by increased new customer acquisitions during the year

So this could well be a leading indicator for accelerating revenue growth. Adjusted EBITDA is less impressive, growing just low single-digits. The reason given is that:

The targeted investment in the Group's sales capability and leadership functions meant Adjusted EBITDA rose by 4% to £2.5m (2024: £2.4m)

The market often doesn’t like it when a company enacts a strategy of prioritising sales and marketing headcount over short-term profitability. Elsewhere, I’ve seen this cause a significant sell-off in a company’s shares. However, here the market seems willing to give them the benefit of the doubt. Personally, I don’t mind this strategy. It is tempting to think that good products sell themselves, but there are many examples that suggest that the reality is far from this. This is their definition of adjusted EBITDA:

Adjusted EBITDA is used by management to assess the trading performance of the business. Defined as Operating profit before depreciation, amortisation, share-based payment charges and exceptional items and includes FX differences.

It is all pretty standard. However, adjusted EBITDA isn’t a great measure for a company that capitalises intangibles, and it is better to focus on EPS, in my opinion. Here things get a little muddy, and it is actually quite hard to work out if these results are in line or not. On the surface, 1.55p EPS is a miss on the Stockopedia consensus of 2.17p. However, the only brokers’ note I can see from Canaccord has them delivering 2.9p adjusted EPS. The company themselves don’t provide their view on an adjusted EPS, and Canaccord don’t provide details of how they get to their adjusted EPS figure. Canaccord’s adjusted EBITDA figure doesn’t match the company’s adjusted EBITDA figure. So, realistically, I have no idea if these are in line or not. The lack of share price reaction suggests they are, but at the end of the day, who knows?

Balance sheet:

Another notable aspect is the significant net cash position, which accounts for approximately 20% of the market capitalisation. However, the bulk of this represents customers paying in advance for software services:

SaaS contracts delivered over time are mostly invoiced in advance and incomplete performance obligations at the year-end are recorded in deferred income in the statement of financial position. T&I revenues are invoiced once the T&I is completed or earlier if contractually allowed with contract assets or contract liabilities recognised in accordance with performance obligations satisfied. The Group has recognised the following assets and liabilities related to contracts with customers.

Here are the figures:

That they have such a large contract liabilities suggests that SaaS customers are paying yearly, not monthly. This upfront payment structure is responsible for the bulk of their operating cash flow, and while the top line is growing, this is likely to increase. However, it also means that billing cycles may lead to significant cash level changes during the year.

Acquisitions:

This has given them the financial flexibility to make acquisitions, though:

On 30 June 2025, the Group announced the acquisition of Enlighten, a competitor business, for a total maximum cash consideration of up to USD 21.5m (approximately £15.9m)...The acquisition brings an expanded offering, new enterprise customers and significantly increases ActiveOps' presence in North America and APAC. It is expected to increase ActiveOps' ARR by approximately USD11.0m (approximately £8.1m) on a pro forma basis and be earnings enhancing, with an anticipated EPS accretion of no less than 15% in the first full year of ownership, being the financial year ending 31 March 2027.

In today’s note, Canaccord include Enlighten’s revenue and expected synergies for the first time. This means that FY26 revenue soars to £40.6m, up from £32.8m. However, they also see PBT and EPS dropping in FY26, both from previous estimates and the prior year. It takes until FY27 to see a return to bottom-line growth, where they upgrade EPS to 3.9p from 3p. This leads them to upgrade their price target to 220p from 185p. We shouldn't read too much into Price Targets, though, as brokers like to keep these at a reasonable premium to the current share price.

Valuation:

The company is clearly performing well, but the problem is the valuation. Even taking Canaccord’s adjusted EPS figure as gospel, the shares are on 38x FY27 earnings. This means that despite Canaccord pointing out that they are forecasting 29% CAGR EPS growth from 2025 to 2028, the shares are on a PEG greater than 1. To many growth investors this means that the stock will be considered fully valued. It requires making assumptions outside of the forecast window, and maybe even into the 2030s to make the company appear good value on an earnings multiple. Making any predictions this far out is as much a statement of faith than judgement.

The quality of the company, and recent share price strength mean that both the Quality and Momentum Ranks are strong, which for some investors may overcome the lack of valuation support:

Mark’s View

While this is rated as a High Flyer, it makes sense to view this stock in a positive light. However, the Quality and Momentum Ranks are not in the top decile, which means the overall Stock Rank is somewhat mediocre. With the current valuation largely a statement of faith in growth outside the forecast window, AMBER seems about right.

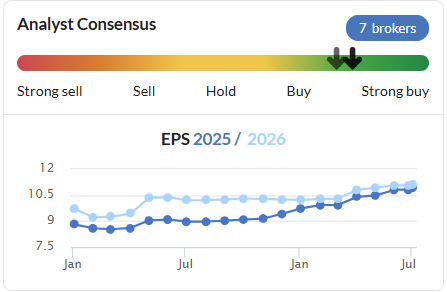

Currys (LON:CURY)

Up 6% to 125p - Final Results - Mark - AMBER/GREEN

Firstly, let me get my gripe on record. The title of today’s RNS is: “Strengthening performance drives profit & cashflow”. But frankly, this could be anything; a trading update, an article in the trade press, an acquisition. What this actually is, is their Final Results. This is not some overly promotional nano-cap company. This is a FTSE250 company and they should be clear about what they are RNSing IMO.

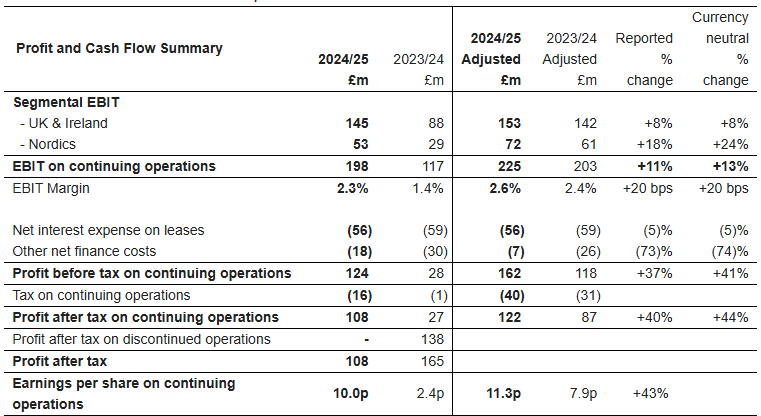

With that out of the way, these are good results. For such a large retail business, sales growth is never going to be excessive. They report just 2% like-for-like revenue growth. However, profitability measures have shown much better performance:

PBT +40% and EPS +43% are the key numbers here. Stockopedia consensus was for 10.9p EPS so this is a modest beat. This comes on top of continuous upgrades during the year:

Although it is worth noting that adj. EBITDA is largely flat,with the gains in profitability coming from lower amortisation and lower net finance costs:

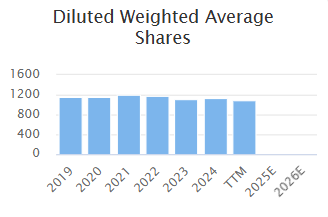

EPS will also have been helped by EBT share purchases reducing the sharecount, at least temporarily:

Cash flow:

Many retailers generate significant cash when they are performing well, and this is the case here:

Operating cash flow was up +13% to £176m due to higher operating profit, slightly offset by lower lease costs. Capital expenditure more than doubled to £50m due to the planned resumption of investment during the year, with spend focused on channel improvements and a variety of small-scale IT and system upgrades.

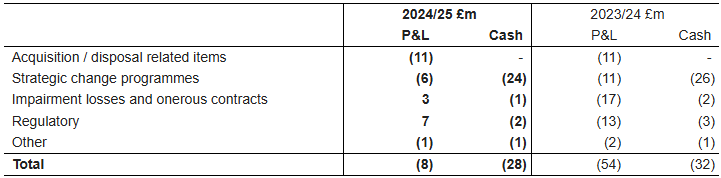

There are a number of adjustments here and it is worth noting that the cash impact exceeds EPS impact this year:

Even including these, cash increased by £96m in addition to funding £15m of share purchases by the EBT. With these results they have started to pay a dividend again, and will continue to buyback shares in the EBT to offset option dilution.

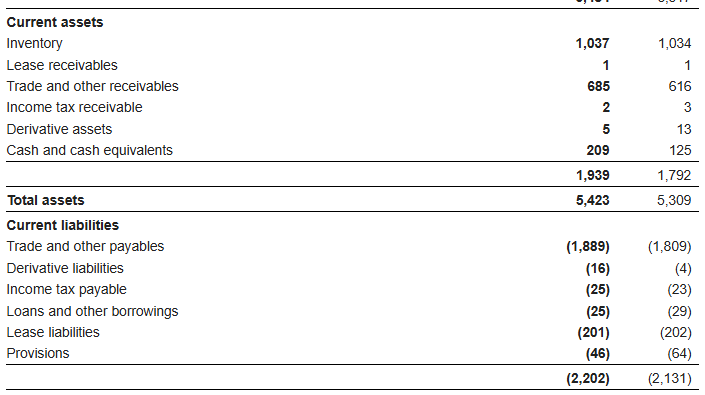

Balance sheet:

The balance sheet looks like the typical large retailer. With goodwill and lease assets making up the bulk of the assets. Lease liabilities exceed lease assets by around £200m so there is an onerous aspect to a number of their leases. Current liabilities exceed current assets, and trade payables are larger than inventory and receivables, perhaps suggesting some window dressing here:

None of this puts them under immediate risk of insolvency, but it adds to the risk if trading should take a downturn. It also means that there is no tangible asset backing to rely on, in extremis.

Outlook:

This is what they say:

The Group is facing into several headwinds this year, including cost increases driven by the UK government's recent budget, general cost inflation, and the weaker Norwegian Kroner reducing reported profits. To counteract these, the Group is pursuing cost saving measures and is well placed to take advantage of growth opportunities…In line with usual practice, the Group will update the market on full year profit expectations after the Peak trading period, but at this early stage in the year it is comfortable with market expectations.

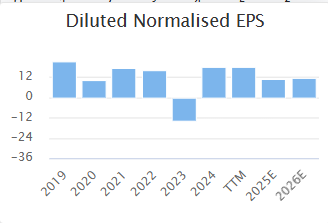

Given the small beat today, this actually means that that FY26 consensus declines, given this has been narrowing to the FY25 figure:

I expect brokers will make some modest upgrades to FY26 figures today, though. In a longer-term historical context, the near term is still some way off historical EPS figures:

This gives the opportunity for higher EPS if we see a recovery in consumer sentiment.

Valuation:

Despite recent strong share price performance, the valuation metrics here are largely green:

Only the lack of growth and dividend payout let the side down. Overall the Value Rank is 83 suggesting further upside to come, especially if EPS can recover further with any improvement in consumer sentiment.

Mark’s View:

The improvement in EPS is impressive, although it is less so once you get into the details of where it comes from (lower net interest and amortisation charges). However, this doesn’t take away from the fact that this business is performing well in difficult market conditions. While the Momentum Rank and overall Stock Rank remain so high, I see little reason to change our AMBER/GREEN view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.