Good morning and welcome back! Roland and I are with you today.

It's a reasonably full-looking table of news today, but in truth there aren't too many results or trading updates.

Spreadsheet accompanying this report: link.

11:30am: we are going to wrap up the report there for today, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Shell (LON:SHEL) (£155bn) | Profits from gas and refining to be “significantly lower than Q1”. Production guidance tightened. | AMBER (Roland) | |

HALEON (LON:HLN) (£34bn) | Restating historic results to reflect new reporting segments launched in May. No changes to results. | ||

Plus500 (LON:PLUS) (£2.3bn) | H1 rev +4% to $415m, EBITDA +1% to $185m. Active customers +2.3%; record deposits of $3.1bn. | GREEN (Graham) While I’ve never entirely abandoned my reservations around customer churn and the lack of hedging, I’ve been happy to stay GREEN on Plus500 for some time, due to its prodigious cash generation and its ability to return vast amounts of this cash back to shareholders. With an update today that’s at least in line, I’m happy to leave this view unchanged. | |

SSP (LON:SSPG) (£1.5bn) | See Wed 2/7 - SSP’s JV partner has placed an anchor stake at the top end of the IPO price band. | ||

Alpha International (LON:ALPH) (£1.4bn) | The deadline for Corpay to make a firm offer has been extended until 5pm on 24 July 2025. | PINK | |

Primary Health Properties (LON:PHP) (£1.3bn) | Adj earnings +2.2% to £47.3m, dividend +2.9% to 3.55p w/ 100% cover. NTAV +1.1% to 106.2p. |

PINK (AMBER/GREEN) (Roland) [no section below] | |

Smarter Web (OFEX:SWC) (£826m) | Placed 7m shares at 327p, raising £22.9m. Further 14m shares being offered to fund bitcoin purchases. According to today's RNS, the company will have 256 million shares in issue; this is the basis for my market cap calculation. | RED (Graham) [no section below] | |

Pinewood Technologies (LON:PINE) (£459m) | Consideration paid: £2.5m. Acquisition is expected to add £0.5-0.7m in incremental EBITDA. | ||

Rockhopper Exploration (LON:RKH) (£377m) | Insurer confirms loss has been triggered re. Ombrina Mare arbitration. Expects €31m payout. | AMBER/RED (Roland) [no section below] The expected receipt of this insurance payout is good news, as far as it goes. But this result is much less than the c.€80m the company had hoped to receive in a best-case scenario. Looking ahead, a final investment decision on the Falkland Islands Sea Lion field is expected later this year. RKH owns 35% and has loan funding (at 8% interest) from operator Navitas for some of the expected $1.4bn Phase 1 capex. But management has previously said the company will probably need to raise funds to meet its remaining Phase I obligations, which I estimate at perhaps $160m. In addition, the company is involved in an ongoing tax dispute with the Falkland Islands govt that could result in a £59.6m liability due after production starts. Management says this is making Sea Lion financing “significantly more difficult”. Even if everything goes ahead as planned, first oil is not expected until late 2027. | |

Ferrexpo (LON:FXPO) (£292m) | Iron ore output -40% to 1.3m in Q2 due to liquidity problems following suspension of VAT refunds. | ||

Pantheon Resources (LON:PANR) (£281m) | Placing at 21.15p, a 14% discount to Friday’s closing price. Proceeds used to support ongoing activities. | ||

Renold (LON:RNO) (£160m) | Strong FY25. Demand in early FY26 “slightly below” prior year. Pricing to offset higher costs. | PINK (recommended offer at 82p) | |

Guardian Metal Resources (LON:GMET) (£82m) | Acquires additional mining claims 15k from company’s project in Nevada. | ||

| Corero Network Security (LON:CNS) (£74m) | Corero Secures Initial CORE Customer Contracts | $1.5m expansion of a partnership. New $0.3m partnership. | |

1Spatial (LON:SPA) (£52m) | UK: return to more typical activity levels. US: slow. Confident to grow in FY26 and beyond. | ||

MTI Wireless Edge (LON:MWE) (£40m) | Three existing customers order military antennas worth c. $1.6m, for delivery over next 20 months. | AMBER/GREEN (Roland) [no section below] Today’s wins include the provision of antenna for airborne use, anti-jamming GPS and “sophisticated beam forming”. They are said to be for use supporting drone management systems. Encouragingly the orders have come from two international defence firms in addition to a local (Israeli) customer. I’d imagine there’s further scope for growth in the drone market for MTI if these orders are successful. However, unchanged forecasts suggest these wins were already priced into existing forecasts. My previous view (see 27 May) also remains unchanged. | |

Artisanal Spirits (LON:ART) (£35m) | Private individuals will be able to buy an individual cask. Only a handful will be released each year. | Reach announcement. | |

GSTechnologies (LON:GST) (£30m) | Placing raises £1.75m at 120p (sp: 138p). 250k retail offer. Purpose: to build bitcoin treasury reserve. | RED (Graham) [no section below] I'm automatically RED on all companies with a Bitcoin treasury policy. GST jumped on this bandwagon recently, as we noted in this report, claiming that bitcoin "offers liquidity comparable with to cash while serving as a reliable store of value". The adoption of this policy now serves as the basis for equity dilution. According to the StockReport, GST has never made a profit and is categorised as a "Sucker Stock". As noted in relation to SWC, I'm far more bullish (in the short-term) on the companies that can benefit from serving the demand for these stocks, than I am on the stocks themselves. CMC Markets (LON:CMCX are GST's placing agent through their CapX division. | |

James Cropper (LON:CRPR) (£21m) | Loses a significant customer but FY 2026 exps seem unchanged. RNS could be more explicit. Broker estimates: house broker Shore Capital has left FY25 forecasts unchanged today. It will reinstate FY26/FY27 forecasts when CRPR’s FY results are published later this month. | AMBER (Roland) [no section below] I don’t feel much wiser after reading today’s RNS. Cropper has lost a significant customer but provides no detail on the scale of the revenue impact. This news also does not appear to change the company’s expectation for the Paper & Packaging division to return to breakeven later this year. Elsewhere, expected “single-digit” FY26 revenue growth in the Advanced Materials division seems unexciting to me. The company has previously said that efforts to improve the performance of both divisions are expected to yield more impressive results from FY27 onwards. With a FY25E P/E of 18 and no outer-year forecasts from the house broker, I’m inclined to downgrade our view to neutral until this month’s FY results provide some clarity. | |

Plexus Holdings (LON:POS) (£16m) | FY June 2025 in line. Rental fleet growing and Mid East contract progressing. New USA contract. “...whilst the macroeconomic environment remains challenging, opportunities for Plexus are encouraging and the Company remains confident in its strategy for sustainable growth.” | AMBER/RED (Graham) [no section below] We covered the March fundraise by Plexus here. Funds are now being put to work as planned, expanding the company’s fleet of wellhead systems. A note from Cavendish this morning leaves forecasts unchanged (FY June 26: revenue £9.4m, adj. PBT £0.2m). As the company is still at such an early stage in its development and offering very limited profit margins for now, I’ll leave my moderately negative stance unchanged, to reflect the view that this is a high-risk play. | |

Eneraqua Technologies (LON:ETP) (£10m) | SP down 32% FY Jan 2025: revenue £63m (<exps? StockReport says revenue forecast is £81m) and PBT in line. Balance sheet strain: exploring interim funding should it be needed. | RED (Graham) [no section below] | |

| Jarvis Securities (LON:JIM) (£8m) | Sale of Retail Execution-only Brokerage Business | SP +14% (RNS at 9:18am) The sale to Interactive Investor goes through for £11m, with £9m to be paid shortly and £2m deferred for up to c. 18 months. JM’s other operations are being terminated/closed down, which will take approx. 15 months. JIM will become a cash shell. Directors intend to make a distribution to shareholders (if allowed by the FCA) and cancel the listing. | PINK (Graham) [no section below] It's a relief that the sale has gone through, but it's still a sad end to the story and I would not be tempted to buy in here with the goal of receiving a cash payment from the liquidation in due course, as I’ve found this deep value strategy to be very underwhelming in the past. My main learning point is to “run for the hills” when companies announce an FCA-ordered skilled person review (see our previous coverage of JIM here). |

Graham's Section

Plus500 (LON:PLUS)

Up 1% to £33.20 (£2.4bn) - Half Year 2025 Trading Update - Graham - GREEN

Plus500, a global multi-asset fintech group operating proprietary technology-based trading platforms, today announces its trading update for the six months ended 30 June 2025.

When I covered this company’s Q1 update in April, I noted that there had been a year-on-year revenue decline (Q1 2025 vs Q1 2024), accompanied by a slowdown in customer recruitment.

Q2 (and H1 more broadly) show a return to growth:

The tariff-related turmoil must have been a big help. Similar stocks such as IG group (LON:IGG) (in which I have a long position) saw their share prices strengthen during April, as more people looked for ways to trade the market volatility.

Plus500 don’t have much to say about that today, instead focusing on their strategic milestones.

CEO comment:

"Plus500 delivered further operational and financial progress in H1 2025. We expanded our global presence with new regulatory licences in Canada and the UAE, added to our growing list of clearing memberships with ICE Clear US and announced the exciting acquisition of Mehta Equities in India, which will provide us access to the largest retail futures market in the world.

H1 growth is attributed to Plus500’s “proprietary technology and unique system architecture”, rather than to the market’s tariff tantrum!

After recruiting 27,000 new customers in Q1, this improved slightly to 29,000 in Q2. The number of active customers also improved.

The standout figure is customer deposits, which increased from $1.5bn in H1 last year, to $3.1bn in H1 this year. Plus500 remind us that they have been focusing on higher value customers - and numbers like this tell us that it is working! Although again, the importance of the market backdrop should not be discounted.

US futures business: this has been highlighted as a significant growth opportunity, and Plus500 tells us that their total non-OTC revenue (futures and share dealing) grew to 13% of their total revenue in H1.

Cash balance has grown since March, to “over $925m” as of the end of June. The next round of dividends and buybacks will be announced at the H1 results in August.

Outlook:

Following a strong start to the year, the Board of Directors of Plus500 remains confident in the outlook for the Group for 2025 and beyond, reflecting the Group's market-leading technological capabilities, balance sheet strength, earnings resilience and the emerging opportunities, particularly within the B2B (Institutional) futures space.

Estimates

The company helpfully provides a footnote stating that consensus forecasts are for FY26 revenue of $746.2m and EBITDA of $345.2m.

A note from Panmure Liberum this morning leaves their forecasts unchanged - they are below consensus, but they note that H1 EBITDA ($185m) is more than half (54%) of their own full-year estimate.

The H1 EBITDA result is also more than half, again about 54%, of the consensus full-year estimate.

Graham’s view

With most of the full-year EBITDA estimate having already been achieved in H1, you’d have to think that there’s a decent chance of a full-year beat. But I do think that market conditions in H1 were especially favourable, even if Plus500 haven’t acknowledged that today.

(I wonder why they don’t acknowledge it - surely it’s what most of their investors are thinking?)

As a reminder, this what the VIX Volatility Index did at the start of Q2:

On balance, I think it’s fair to leave full-year forecasts unchanged, as there is no certainty that markets will be as exciting in H2 as they were in H1. So there is no point in getting carried away at this stage.

And overall, I don’t see any reason to change my positive view on this stock.

It has probably hundreds of millions of dollars of surplus cash; adjusting for this would give a slightly smaller earnings multiple.

While I’ve never entirely abandoned my reservations around customer churn and the lack of hedging, I’ve been happy to stay GREEN on Plus500 for some time, due to its prodigious cash generation and its ability to return vast amounts of this cash back to shareholders.

With an update today that’s at least in line, I’m happy to leave this view unchanged.

Roland's Section

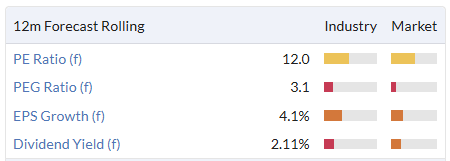

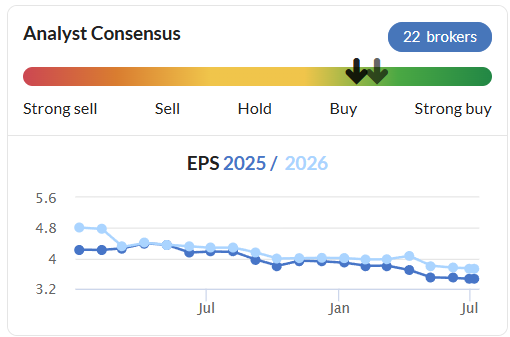

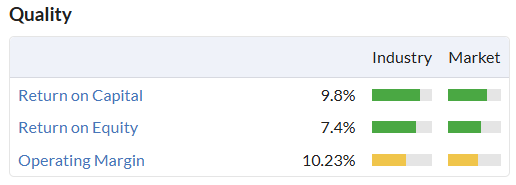

Shell (LON:SHEL)

Down 3% to 2,543p (£150bn) - Second quarter update note - Roland - AMBER

Today’s second quarter update from Shell follows a detailed format that’s decided to give City analysts some advanced clues on the likely outturn in the company’s next quarterly results.

As I commented in April, I don’t model Shell that closely so instead tend to look for any areas of change relative to previous guidance. Today’s update highlights a few points that show some variance from previous guidance at the end of Q1:

Integrated Gas: profits from the group’s gas business are expected to be “significantly lower” than during the first quarter. This appears to be driven at least partly by lower production, with production guidance trimmed this morning

Q2 gas production expected to be 900-940kboepd (previously 890-950koepd)

Q2 LNG production expected to be 6.4-6.8m tonnes (previously 6.3-6.9mt)

Oil production is expected to be towards the top half of previous guidance.

Chemicals & Products: profits are expected to be “significantly lower” than in Q1, despite improved refinery margins and utilisation. The problem appears to be an unplanned outage at one of the group’s chemical plans, resulting in a quarterly loss for the chemicals sub-segment.

Outlook: analysts have trimmed earnings forecasts for Shell this year. The content of today’s update suggests to me that a further slight moderation may be likely, albeit not a significant change:

Roland’s view

Today’s update appears to be mildly negative and Shell’s share price has fallen slightly.

However, as I commented in April and May, I think minor quarterly variations in performance such as those highlighted today are far less important than the cyclical picture – commodity prices and global demand.

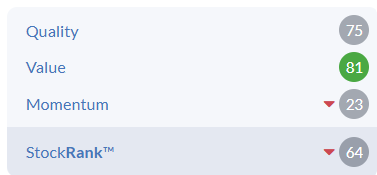

While Shell’s share price has held up relatively well so far this year, given external events, the company’s StockRank has been falling steadily:

Shell’s StockRank was 94 at the start of 2025, but is now down to 64, with momentum now notably weak:

My previous view that the company’s valuation is probably in the upper half of its normal cyclical range remains unchanged.

Indeed, the share price recovery seen since April’s tariff sell-off means Shell’s CAPE10y valuation ratio has now risen to almost 14x (from 12.5x on 7 April):

Personally, I don’t find this a compelling valuation at which to buy a cyclical and capital-intensive business with fairly average quality metrics.

At the same time, I recognise that if market conditions and external events combine to provide support for oil and gas prices, then Shell could continue to perform well and fund further high levels of buybacks and dividend growth.

The StockRanks are neutral at this level and so is my view, which I’m leaving unchanged at AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.