Good morning! The Agenda is now complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Unite (LON:UTG) (£4.0bn) | Sales momentum (85% beds sold). Reiterates FY25 guidance for adjusted EPS 47.5-48.25p. | ||

Victrex (LON:VCT) (£684m) | Sales volumes +8%, revenue -3%. Adverse mix. H2 adjusted PBT may be broadly similar to H1. | BLACK (AMBER/RED) (Graham) There has been a relentlessly downward trend in EPS forecasts and now we have a profit warning. Consistent with what we know about profit warnings, I take a moderately negative stance until there is evidence of stabilisation. But the reasons for weaker trading sound like they are potentially very serious, and could be difficult to address. | |

Niox (LON:NIOX) (£286m) | Rev +20%, ahead of exps. Too early to say if this will continue. Adj. EBITDA +30%, cash £11.8m. | ||

Optima Health (LON:OPT) (£187m) | Rev -5%, adj. PBT -4% (£12.8m). Actual PBT £2.6m. Net debt £2.2m. Well positioned for FY26. | ||

Begbies Traynor (LON:BEG) (£177m) | Rev +12% (+10% organic). Adj. EBITDA +11% (£31.7m). FCF £19.4m. Outlook in line. | ||

SIG (LON:SHI) (£171m) | 1% LfL rev growth = market outperformance. H1 adj. op profit c. £15m. 2025 outlook unch. | ||

Frontier Developments (LON:FDEV) (£131m) | David Braben (32.7% shareholder) will sell such that his % holding will remain broadly unchanged. | ||

Springfield Properties (LON:SPR) (£120m) | FY25 rev £280m. PBT in line with exps. Net debt reduction in excess of exps to £21m. | ||

Solid State (LON:SOLI) (£118m) | FY25 marginally ahead: rev -23.4%, adj PBT -67.9% to £5.0m. Strong order book, outlook in line. | ||

| Distribution Finance Capital Holdings (LON:DFCH) (£65m) | Trading Update | H1 loan book +20.7% to £728m. Arrears of 0.9% (H1 24: 0.5%). FY outlook in line with exps. | GREEN (Graham) Not only is it pretty cheap against earnings about (5x or 6x, depending on how you measure it), it’s also cheap against its balance sheet - net assets were £115m at the last full-year results. Reflecting their own belief that they are undervalued, they have been buying back their own shares. I have no reason to change my GREEN stance on this. |

Metals One (LON:MET1) (£60m) | Will terminate FinnAust acquisition and prioritise other projects, including US gold & uranium. | ||

Celebrus Technologies (LON:CLBS) (£59m) | Rev -5%, ARR +13.9% to $18.8m. PBT +4.3% to $7.3m. Recent wins but slower customer decisions. | AMBER (Roland) These results confirm what I suspected in April – a major revenue reset is taking place to reflect an exit from third-party sales and a change in revenue recognition. Today’s forecasts suggest it will take three years for revenue to return to FY25 levels and that even in FY28, profits will be lower than in FY25. A hefty cash balance means I think that the outlook remains fairly secure and the company should have time to make this new model work. However, I’d argue the valuation is up with events until there’s more concrete evidence of progress. | |

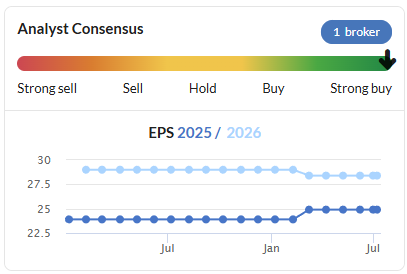

Synectics (LON:SNX) (£58m) | Rev +35%, adj op profit +48% to £3.3m. Order book £35.1m. FY25 outlook comfortably in line. ShoreCap FY25E EPS unch at 24.9p. | AMBER/GREEN (Roland - I hold) | |

Audioboom (LON:BOOM) (£54m) | Rev +5%, adj EBITDA $1.2m (2Q24: $0.2m). Cash: $2.5m. $70m revenue booked for 2025. | ||

Gelion (LON:GELN) (£42m) | Grant for sulfur battery development. Will require matching spend by Gelion. | ||

Angle (LON:AGL) (£21m) | Study found using Parsortix for CTC assessment may provide extra insight vs standard methods. | ||

DSW Capital (LON:DSW) (£15m) | Rev +110%, adj PBT +182% to £1.4m (inc acquisitions). Net assets £10m, outlook in line. |

Graham's Section

Victrex (LON:VCT)

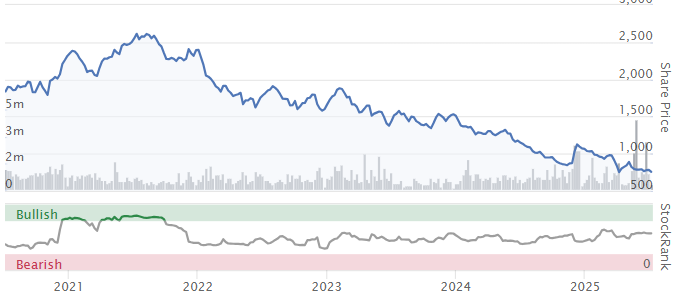

Down 8% to 723p (£629m) - Q3 Trading Update - Graham - AMBER/RED

Victrex plc is an innovative world leader in high performance polymer solutions, delivering sustainable products which support CO2 reduction and enable environmental and societal benefit in multiple end-markets. Today's trading update for Q3 covers the period 1 April 2025 to 30 June 2025.

I’ve never felt like I've had a very good understanding of Victrex’s business: I know they make polymers, including a polymer called “PEEK”, which are considered highly useful in various industries. But chemistry being my weakest subject, I’ve struggled to deepen my understanding beyond that.

For many years, its market cap has been over £1 billion, so it has not been a priority for us at the SCVR/DSMR.

But the valuation has declined in recent years:

And it’s lower again today on the back of a profit warning.

The key points.

Q3 revenue down 3%

Q3 volume up 8% but average selling price down 11%

Nine month performance: volume up 13%, average selling price down 10%.

Q3 is therefore noticeably worse than H1 and the company says:

Continuation of Q3 sales mix and ASP trends in Q4 would lead to a broadly similar H2 underlying PBT result, versus H1

H1 underlying PBT was £23.2m (itself down by 17% against the prior year).

So a repeat of that would give £46.4m of underlying PBT for the year.

And it’s what the company expects: “A continuation of similar ASP trends during Q4, versus the prior year, is expected.”

I believe this is a miss of about 8% against current forecasts. So this morning’s share price fall by a similar percentage makes sense.

The main weakness seems to be in the Medical sector, and the reasons for the weakness sound like they could be difficult to address:

Medical performance was lower than our expectations. Whilst we continue to see good growth in Non-Spine, this was not sufficient to deliver overall divisional improvement during the period. Spine remains the most impacted application area within Medical, including impacts from industry destocking, the effects from Volume Based Pricing (VBP) in China and alternative materials in the US Spine market.

Net debt at the end of June was £42.8m, which should be easily manageable, so I agree with the company that their financial position is “robust”.

Outlook:

Overall Q3 trading saw continued volume momentum, offset by a softer than expected performance in Medical and further adverse sales mix within Sustainable Solutions.

"The Group is well positioned to deliver at least high single digit volume growth for the full year, in line with guidance, although the remainder of FY 2025 sees a tougher comparative and we are mindful of ongoing macroeconomic uncertainty. At profit level, our range of outcomes reflect the impact of an adverse sales mix in both divisions, a weaker Medical performance and the headwinds from our new China manufacturing facility, as well as a c£9m currency headwind. Whilst we are targeting H2 underlying PBT to be slightly improved on H1 underlying PBT of £23.2m, a continuation of Q3 sales mix and ASP trends for the remainder of the year, particularly in Medical Spine, would result in H2 underlying PBT being at a broadly similar level as H1.

CEO Succession: after eight years, the current CEO has announced his intention to retire. His successor is the current CEO of Ab Dynamics (LON:ABDP) but “a definitive start date has not yet been agreed”. Overall, this seems to be an orderly and reasonable transition.

Graham’s view

Roland downgraded his stance on this to neutral in May and I think it’s appropriate for me to downgrade again today, to AMBER/RED. At Stockopedia, we’ve found that that profit warnings tend to be followed by more profit warnings. So in the short-term at least, I’d be wary that this is vulnerable to further weakness.

Remember as well that the reasons for today’s profit warning are potentially very serious. “Destocking” can be written off as a short-term issue, but the availability of “alternative materials” cannot. If the medical industry has found cheaper or superior alternatives to Victrex’s polymers, this is not a problem that is just going to go away!

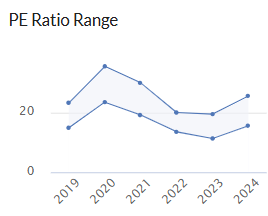

Not just in market cap terms but also in P/E terms, these shares are trading cheaper than I remember seeing them before, but it may be justified:

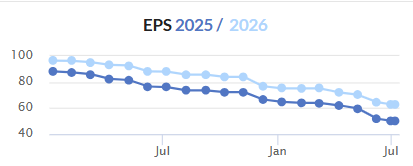

The downward momentum in EPS forecasts has been relentless:

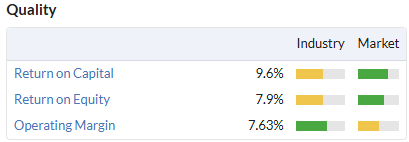

Gross margins have been sliding in recent years and the company’s quality metrics have deteriorated, although it does still have a QualityRank of 92:

I do consider Victrex to be a very reputable company, even if it is challenged in the short-term, and I would be inclined to bring our stance back up to neutral as soon as there is evidence of stability. For now, though, consistent with what we know about profit warnings, I’m AMBER/RED.

Distribution Finance Capital Holdings (LON:DFCH)

Up 5% to 40.88p (£68m) - Half Year Trading Update - Graham - GREEN

Distribution Finance Capital Holdings plc, a specialist bank providing financial solutions that support dealers and manufacturers across the UK, is pleased to provide a trading update for the six months ended 30 June 2025 (the "period").

I’ve been GREEN on this and am pleased to see that it appears to be going from strength to strength.

Full year results are expected to be in line.

Key bullet points:

New loans in H1 +16.8% to £828m.

Loan book +20.7% year-on-year to £728m.

Number of dealer customers 1,491 (a year ago: 1,250).

There’s a small increase in arrears to 0.9% of loan brook (a year ago: 0.5%).

New product: asset finance. No longer just supporting dealers and manufacturers, DFCH is now making loans to end-users in the motorhome and caravan sector, and it will broaden out from here.

This “unlocks entry into significantly larger addressable markets than the Group's current offering.” 50 dealers have already signed up to originate lending.

A key point here is that DFCH are launching this product in the aftermath of the recent legal controversy around UK motor finance, so they are unencumbered by any potential legal issues faced by others in the sector re: historic practices.

CEO comment:

The launch of our asset finance product marks an important milestone for the Group and delivers on our long-held ambition to be a multi-product lender. Given these products tap into markets which are significantly larger than our core inventory finance product, it supports our medium-term goal of hitting a loan book of £1.3bn by the end of FY28 and deliver mid-teens return on equity. This, in addition to the Group's performance year to date, leaves the Board confident of achieving market expectations for the full year.

The company’s ROE most recently (per the StockReport) was 13%. I’m optimistic that we’ll see ROE rising as promised, as the company scales up.

Estimates: with thanks to Panmure Liberum I can see the following estimates.

2025 PBT £14.5m, earnings per share 4.9p.

2026 PBT £18m, earnings per share 7.6p.

Graham’s view: the financial sector has offered us plenty of bargains in recent years but this is currently one of my favourites.

Not only is it pretty cheap against earnings about (5x or 6x, depending on how you measure it), it’s also cheap against its balance sheet - net assets were £115m at the last full-year results.

And for this cheap valuation, the market is offering what I think is a genuine growth story, hopefully with rising quality as it grows.

Reflecting their own belief that they are undervalued, they have been buying back their own shares.

I have no reason to change my GREEN stance on this. With growing small-cap financials, you can never be 100% sure, but I continue to think the risk:reward looks very attractive here.

Roland's Section

Synectics (LON:SNX)

Up 1% to 330p (£59m) - Half Year Report - Roland - AMBER/GREEN

At the time of publication, Roland has a long position in SNX.

Synectics plc (AIM: SNX), a leader in advanced security and surveillance solutions, announces its unaudited interim results for the six months ended 31 May 2025 ("H1 2025" or the "Period").

CCTV specialist Synectics is a member of my rules-based SIF portfolio and a personal holding, so the firm’s progress is of particular interest to me.

After a strong run in 2024 the shares have flatlined this year, perhaps reflecting a lack of recent earnings upgrades. As I’ve discussed previously, I also have some niggling concerns about the company’s rather average profitability.

Let’s see if today’s figures suggest any changes to these trends.

Half-year results summary: today’s numbers have been met with a shrug by the market but seem broadly positive to me, reflecting a solid H1 boosted by a one-off big win:

Revenue up 35% to £35.5m

Underlying operating profit up 38% to £3.0m

Adjusted earnings up 59% to 16.4p per share

Interim dividend up 10% to 2.2p

Net cash of £12.1m (H1 24: £6.4m)

Order book: £35.1m (H1 24: £30.2m, FY24: £38.5m)

Management flags up several decent-sized contract wins from the first half, including a £2m deal with West Midlands police and a £1.1m pilot programme with bus and coach operator Stagecoach. There was also a significant Asian casino win that was initially valued at $2.2m, but later enhanced by a $4.8m contract extension.

Order intake seems to have remained fairly resilient, with the order book standing at £35m at the end of May. That’s 16% ahead of the same time one year ago, but below November’s year-end figure of £38.5m. In today’s results, CEO Amanda Lander says that this is because the big casino win was included in the year-end order book but has largely been delivered this year.

My reading of her comments is that this large deal boosted H1 results but may not be within the company’s ongoing run-rate of revenue. This seems to be reflected in current consensus forecasts for FY25 revenue of £65m. This implies H2 revenue of c.£30m, £5m (16%) below the H1 figure reported today.

Profits also seem likely to be weaker in H2, in my view, given the company’s guidance for higher operating costs to support increased investment in product development and commercial capabilities. Full-year forecasts for earnings of 24.9p per share imply that 65% of this year’s profit may have been generated in H1.

Profitability & Adjustments: today’s results are commendably free of non-underlying items, so the underlying operating profit of £3.0m translates into a statutory operating margin of 8.4% for the half year.

My sums suggest a trailing 12-month return on capital employed of 12.8%.

Both metrics are an improvement on FY24 figures:

However, given the apparent H1 weighting to profitability in FY25, I wonder if profitability will revert to last year’s level over the full year.

Synectics has two reporting divisions and its profitability is easier to understand when viewed through this lens:

Systems: sells Synectics own solutions globally through distributors and systems integrators. End users include the casino and oil and gas sectors;

Ocular: sells Synectics and third-party products directly to customers, mainly UK public sector and infrastructure customers.

Growth was split across both segments in H1, but the main drag on profitability seems to be the Ocular division:

Systems: revenue +6.2% to £23.6m, op profit +35% to £3.9m (16.7% margin)

Ocular: revenue +2.9% to £12.6m, op profit +14% to £0.8m (6.1% margin)

I appreciate that supplying direct to customers is likely to carry significantly greater overheads than selling through a distributor. But I’d have thought that this would partly be reflecting in pricing differentials to end users and wholesale partners.

Thinking about it, I wonder if Ocular’s low profitability could be due to other reasons. For example:

Selling third-party products – Synectics may only receive a distributor’s (very low) margin on these items;

Lower pricing power on solutions sold to UK infrastructure/public sector (versus private sector end users). The company hints at this, mentioning tighter margins due to “the nature of competitive procurement frameworks”.

However, one advantage of the split between these two segments is the diversification it provides across a wide range of uncorrelated sectors that this small company probably couldn’t otherwise address.

Balance sheet & cash flow: Synectics has no debt and the group’s net cash position rose to £12.1m during the half year, nearly double the £6.4m reported at the same point one year ago.

This accounts for a fifth of the group’s market cap and implies a cash-adjusted FY25E P/E of just 9.5 – not expensive at all, in my view.

Synectics’ balance sheet and cash generation look excellent to me, but as a small company I suspect the market is more focused on growth than value.

While the cash position should provide some downside protection, I suspect it wouldn’t be enough to prevent a sell off if Synectics’ growth disappoints over the next 12-18 months.

Outlook: on that note, today’s outlook statement sounds positive but is only in line – not the upgrade investors were probably hoping for:

Trading remains comfortably in line with market expectations for FY 2025, and we expect revenue to be broadly balanced between the first and second halves.

I view use of the word comfortably as being the opposite of broadly – i.e. while broadly often means slightly below, comfortably seems to suggest scope for improvement.

In this case, I’m slightly unsure how to read this statement. As I mentioned earlier, today’s unchanged forecasts from house broker Shore Capital suggest revenue could fall by 14% to £30m in H2. I wouldn’t describe that as “broadly balanced”.

At the same time, “comfortably in line” doesn’t seem to suggest any imminent danger to hitting FY25 profit forecasts.

I wonder if the key to understanding this mixed messaging is the risk of a slowdown in the higher-margin but cyclical oil and gas sector:

We are seeing some slippage in expected order timing, as project approvals in the oil and gas sector are taking longer than anticipated. More frequently, projects are being re-evaluated or re-engineered following the design work, primarily due to higher-than-expected cost estimates. Despite this, the overall outlook remains positive, and we anticipate increased activity in the second half of FY 2025.

Roland’s view

A business of this kind – with many end markets and a range of products – will always face some cyclical and timing risks. Investment in product development is also a factor that’s likely to vary over time due to product and technology update cycles.

I don’t have any serious concerns about today’s update, given unchanged forecasts and expectations for FY26 growth:

The group’s improved cash position and cash-adjusted P/E of <10 looks decent value to me. Net cash provides optionality to invest in growth or acquisitions and is an interest-earning asset in its own right in the current market.

I’m comfortable maintaining our view at AMBER/GREEN today.

Celebrus Technologies (LON:CLBS)

Up 12% to 166p (£66m) - Full Year Results - Roland - AMBER

Celebrus Technologies plc (AIM: CLBS, "the Group", "Celebrus"), the data solutions provider, announces its final results for the year ended 31 March 2025.

This data firm specialises in providing insights for marketing and fraud detection purposes. I last wrote about Celebrus in April, when its shares had fallen sharply due to a warning that revenue for the year would be below expectations.

To add to the uncertainty, the company chose that moment to unveil a new revenue recognition policy and redefine its measure of recurring revenue. Management also slipped in a warning that FY26 results would be affected by the restructuring of the group’s agreement with a large customer.

At the time, I speculated that the combination of changes being announced might imply a sharp fall in revenue for FY26. Today’s results confirm that this will be the case, as the company moves away from selling third-party hardware and software to focus on its software-only in-house solutions.

This strategy shift means I’m not sure how relevant today’s full-year results really are. However, they do provide a starting point for understanding the valuation and outlook, so are worth a look.

FY25 results summary

Today’s results appear to be in line with the revised guidance provided in April.

Total revenue down 5.4% to $38.7m

Software revenue (exc 3rd party) up 9.4% to $30.3m

Annualised recurring revenue (ARR) up 13.9% to $18.8m

Gross margin of 61.9% (FY24: 52.9%)

Adjusted pre-tax profit up 14.5% to $8.7m

Adjusted EPS up 36% to 18.24 cents per share

Net cash down 18% to $31.5m, reflecting working capital movements

(Note that Celebrus also switched to reporting in USD for the 24/25 financial year. Comparative figures have been translated by the company, but it’s worth remembering the currency discrepancy if you are reviewing past years’ results.)

These results don’t seem terrible, seemingly showcasing improved profitability as the company transitions away from third-party hardware revenue.

However, there’s a sting in the tail – today’s reinstated broker forecasts suggest a significant reduction in profitability over the next couple of years as third-party revenue drops off and the shift to monthly revenue recognition works through the accounts.

A look at the segmental breakdown of last year’s results shows that the drop-off in third-party revenue was already well underway last year. Third party revenue fell by 37% to $8.3m:

These numbers suggest that a further $8m of revenue is likely to disappear as the company completes its shift away from this sector.

Interestingly, the accounts show that over 90% of third-party revenue last year was generated by one or more major customers, defined as generating over 10% of group revenue.

What we don’t know is what proportion of profit was generated by these customers – or if they are transitioning to software-only Celebrus solutions.

Outlook & reinstated forecasts

Brokers Cavendish and Canaccord Genuity withdrew their FY26 and FY27 forecasts following April’s update but have reinstated them today.

These estimates confirm what CG describes as “a painful forecast reset”. This is due to the expected loss in FY26 of c.$8m of third-party revenue and $6m in software licence revenue due to the change in revenue recognition from annual to monthly.

Given that operating costs are expected to continue rising as Celebrus invests in product spend and marketing, this outlook means that the company is expected to drop to a loss in FY26 before reporting a minimal profit in FY27.

Here’s a summary of today’s updated forecasts from Cavendish:

Revenue | Adj PBT | Adj EPS (p) | |

FY25A | $38.7m | $8.7m | 13.5 |

FY26E | $23.5m | -0.7m | -0.7 |

FY27E | $27.0m | 0.8m | 2.0 |

FY28E | $37.0m | 5.1m | 10.0 |

I’m not sure how much faith I’d place in forecasts for FY28 at this stage, but even then, profitability is expected to be lower than it was last year.

After this morning’s share price gain, these forecasts price Celebrus on a FY28F P/E of 22.

Even if I strip out today’s net cash of $31m, that’s still equivalent to a P/E of 14 – in three years’ time.

In fairness, it’s worth pointing out that the change in revenue recognition is an accounting change only. It won’t change the (annual) timing of cash receipts from clients on their licence renewal dates.

However, the loss of third-party revenue will have a real impact on cash flow, so I think it would be premature to suggest Celebrus could be trading on bargain free cash flow multiples due to the continuing growth in ARR.

Outlook: today’s results were paired with a second RNS this morning trumpeting two new contract wins.

The company says that contracts with “a European bank” and “an American fintech in the trading and brokerage sector” have a combined value of just under $4.0m and will add $1.1mm to ARR in their forest year.

This brings group ARR to almost $20m, based on the year-ending figure of $18.8m.

Management says that “a good proportion of revenue” for the current year is also committed, perhaps providing some confidence in today’s broker forecasts.

Roland’s view

Markets have welcomed today’s results from Celebrus, although its share price remains a long way below the level seen at the start of the year.

Personally, I’m a little surprised at the level of optimism investors seem to be showing today.

Today’s forecasts imply that it will take three years for the group’s revenue to return to last year’s level. Even then, profits are still expected to be lower than in FY25.

I remain unsure whether this change in strategy was prompted by changing customer requirements or Celebrus’s own desire to become a pure-play software provider.

Long term, I think it’s possible this new model will deliver superior profitability and cash flow. But we appear to be some distance from that point at the moment.

In the meantime, I’d argue that the current valuation adequately reflects near-term earnings prospects, even allowing for the large cash position.

I’m going to upgrade our view to neutral today, but I’d want to see some evidence of accelerating growth to take a more positive position.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.