Good morning!

Yesterday evening I published the H1 review of my 2025 watchlist, so feel free to check that out!

Today's Agenda is complete.

Spreadsheet accompanying this report: link.

We're finished for today, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Severn Trent (LON:SVT) (£8.0bn) | Expects to perform in line with guidance, including £25m in “ODI reward” in FY26. | ||

DCC (LON:DCC) (£4.69bn) | Q1 op profit in line, modestly behind last year. Outlook: good op profit growth, strategic progress. | ||

Pennon (LON:PNN) (£2.23bn) | Ofwat accepts SW Water’s enforcement package. No financial penalty but £24m of undertakings. | ||

Vistry (LON:VTY) (£2.04bn) | H1 profits in line (adj. PBT £ 80m), underpins confidence in outlook. Net debt £295m better than exps. | ||

Grafton (LON:GFTU) (£1.93bn) | H1 in line. Revenue +10%. Includes benefit of acquisitions. Many markets remain challenging. | ||

Pantheon International (LON:PIN) (£1.39bn) | £23.7m of buybacks in May at 40% discount to NAV. Another £20m allocated (on top of £10m). | GREEN (Graham - I hold) [no section below] | |

Pagegroup (LON:PAGE) (£881m) | Q2 gross profit -10.5% (cc). 2025 operating profit to be broadly in line with consensus c. £22m. | ||

Dr Martens (LON:DOCS) (£736m) | Trading since the start of the year is in line with exps, all guidance unchanged. Healthy order books. | ||

Rank (LON:RNK) (£644m) | LfL net gaming revenue +11% to c. £795m. Full year adj. LfL operating profit ≥ £63m, ahead of exps. | ||

Johnson Service (LON:JSG) (£617m) | H1 rev +5.5%. HORECA saw “slower than anticipated start to summer months”. Debt £99m. | ||

Jupiter Fund Management (LON:JUP) (£575m) | £15bn of AUM bought in. Price £100m, funded from existing cash. Targets £16m annual synergies. | AMBER/GREEN (Graham) I give this acquisition two thumbs up as the price paid seems very reasonable and it sounds like it should be a strategic success. Jupiter is a fund manager I've been quite positive on - its shares have staged a tremendous turnaround since April, not far off doubling from their lows. | |

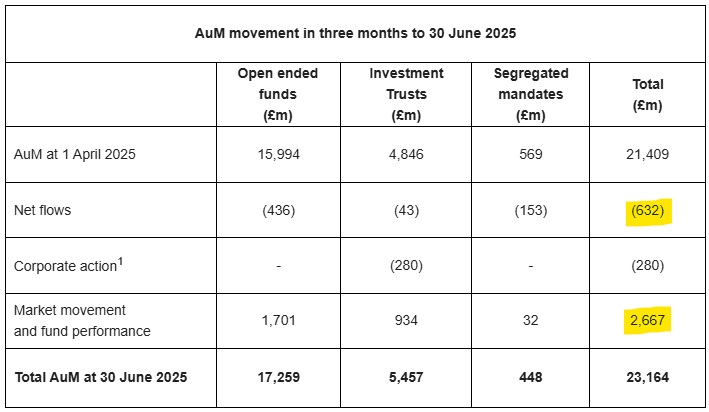

Polar Capital Holdings (LON:POLR) (£495m) | AUM 30 Jun +8.2% in the quarter to £23.2bn. Net Flows -£632m. | AMBER/GREEN (Graham) Leaving my moderately positive stance on this unchanged after some modest outflows in the quarter, which are uncharacteristic of the company. I can't predict the future but I'm hopeful that this is not the start of a new negative trend. Positive market movements have more than made up for the negative quarterly flows. | |

Griffin Mining (LON:GFM) (£356m) | Fully recovered from 2024 suspension of operations. Zinc conc prodn +61% vs prior quarter, Gold conc +157%, Silver conc +174%, Lead conc +82%. | ||

Brooks Macdonald (LON:BRK) (£286m) | Q4 FUM +3.2% to £19.2bn. Q4 net outflows £5m vs £129m outflow in Q3.Anticipates the full year performance to be in line with market expectations. | ||

Pantheon Resources (LON:PANR) (£247m) | Nabors 105AC rig is contracted and is currently mobilising to the Dubhe-1 pad for an well is an appraisal well targeting the Ahpun Topset. | ||

Enquest (LON:ENQ) (£235m) | Completed the acquisition of Harbour Energy's business in Vietnam for $85.1 million. Net of interim period cash flows consideration paid by EnQuest was $25.7 million. Adds net 2P reserves and 2C resources of 7.5 million boe and 4.9 million boe, respectively. | AMBER/GREEN (Mark) [no section below] | |

Liontrust Asset Management (LON:LIO) (£231m) | SP +6% AUM £22.6bn, unchanged over 3mo, £1.2bn net outflows, almost entirely from UK Retail funds. Confident sentiment: “We have now begun to see investors, led by institutional clients, turn more towards actively managed funds and diversify geographically, with Europe and the UK outperforming the US stock market over the first half of 2025”. | AMBER/GREEN (Graham) [no section below] | |

Macfarlane (LON:MACF) (£186m) | SP down 11% | (BLACK) AMBER (Mark - I held) | |

Hostelworld (LON:HSW) (£179m) | SP down 9% Net bookings and revenue flat. H1 Adj. EBITDA down 23% to €7.4m. FY 2025 adjusted EBITDA in line with market consensus | AMBER/GREEN (Graham - I hold) It's a quasi-profit warning as although the company still says it's on track, the market doesn't seem to believe it. The company has a lot to do in H2, with a larger H2 weighting than last year needed to meet full-year adj. EBITDA forecasts. I'm still a fan of the overall story here, but I downgrade our stance by one notch to reflect the heightened risk that the company fails to meet full-year forecasts. | |

DP Poland (LON:DPP) (£97m) | “...marked improvement in sales trends resulted in record monthly system sales for both months, contributing to a 4.9% year-to-date system sales increase.” | ||

Strix (LON:KETL) (£96.2m) | “The Group confirms that a competitive refinancing process will be formally initiated in the coming weeks to provide cost effective and flexible funding to support the Company's medium-term investment-driven growth aspirations.” | AMBER (Mark) [no section below] | |

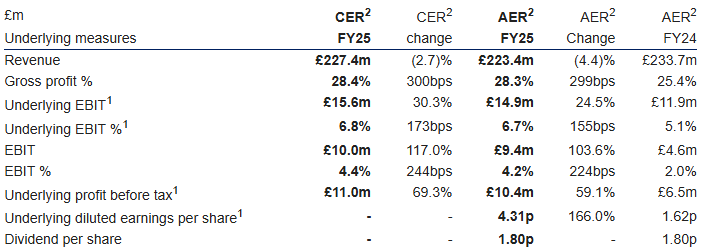

Trifast (LON:TRI) (£92.6m) | Rev -2.7% to £227.4m. U/L EBIT at CCY +31% to £15.6m. U/L PBT £11m. Slightly ahead of consensus. Statutory PBT £4.9m (FY24 £0.8m loss). “Trading headwinds have continued to persist into Q1 FY26 “ | BLACK (AMBER) (Mark) | |

Pebble (LON:PEBB) (£78m) | Revenue and Adj. EBITDA for HY 25 in line with management's expectations despite currency headwinds, slightly behind prior year. | AMBER (Mark) [no section below] | |

Creo Medical (LON:CREO) (£51m) | MicroBlate™ Flex begins lung tumour post-market clinical studyt the Amsterdam University Medical Centre in the Netherlands and at the Royal Brompton Hospital in the UK. | ||

CML Microsystems (LON:CML) (£45m) | 12-year design and supply agreement with leading manufacturer of industrial Global Navigation Satellite System (GNSS) equipment valued at over $30m. | AMBER/RED (Mark) [no section below] | |

Carclo (LON:CAR) (£35.2m) | Will be temporarily suspended from listing and trading from 1 August 2025 until the audit is completed. Highlights previously announced ahead of expectations. | AMBER/RED (Mark) [no section below] |

Graham's Section

Hostelworld (LON:HSW)

Down 9% to 129p/€1.50 (£164m/€190m) - Trading Statement - Graham - AMBER/GREEN

(At the time of publication, Graham has a long position in HSW.)

I pitched this at Mello recently, and also bought a few shares in it myself.

Today’s trading statement has gone down like a lead balloon, even though it reiterates FY25 adjusted EBITDA guidance (the consensus forecast is €19.9m, as compiled by the company).

Key points from this update:

H1 net revenue +0% (€46.7m), net bookings +0% (3.7 million), net average booking value -1% (€13.40).

Direct marketing 51% of revenues (H1 last year: 45%).

H1 adj. EBITDA €7.4m (H1 last year: €9.6m).

The company is still benefiting from some positive cash generation: net cash was €2m as of December 2024, and this has increased to €6m.

And as signalled previously, dividends are back on the agenda with 20-40% of adjusted PBT to be paid, starting in H2 this year.

That’s on top of a £5m share buyback which began recently.

CEO comment:

"Trading over the last six months has been in line with expectations as outlined at our Capital Markets Day in April. Although trading in the first half showed mixed results across regions and channels, we are encouraged by the positive trends observed in June. This included growth in both booking volumes and average booking value (ABV), alongside an improvement in marketing as a percentage of net revenue…

Marketing as a percentage of revenue increased year-on-year, primarily driven by cost inflation in the first few months (which has since moderated) and the growth of paid channels as a proportion of total web channels….

As part of our broader growth strategy, the Group continues to evaluate acquisition opportunities….

Graham’s view

I think I can understand why the market might be underwhelmed with this update.

For a start, 0% growth in top-line indicators (revenue, bookings, etc.) is not exciting.

Customer demand for cheaper Asian destinations has been a long-running reason given for slow top-line growth, and now the company is also talking about bed price deflation in Europe. If the product they are providing is getting cheaper everywhere, that doesn’t bode well for their growth prospects.

Then there is the increase in marketing costs - Hostelworld’s main vulnerability is these costs, which it can’t control (it can control how much it spends, but has no control over their price!).

On a personal note, I am put off by their interest in M&A, which I view as a distraction. I want their core business to prosper, and I don’t see why it can’t! I also don’t want them to drain their cash balance, as they’ve worked so hard to return it to a healthy position. And with buybacks and dividends planned, I don’t see that they are likely to have all that much surplus cash lying around.

Incidentally, I see very little value in the company paying dividends at this stage in its development. It should be an exciting growth story, not a stock that investors are buying into for the yield! But at the same time I understand that LSE investors tend to appreciate some income. Hopefully the dividend will be at the lower end of the 20-40% range.

I’m inclined to keep my positive stance on this share (indeed I’ve slightly increased my exposure to it this morning), but I’m also mindful that today’s update could be interpreted as a profit warning, given the share price reaction.

The company has only generated 37% of its full-year adj. EBITDA forecast in H1, leaving it a lot to do in H2 to meet forecasts.

Last year, the company generated 44% of full-year adj. EBITDA in H1. So the H2 weighting is going to have to be more extreme this year, if forecasts are to be met.

As this is a quasi-profit warning, I’ll downgrade our stance on this by one notch, from GREEN to AMBER/GREEN. Based on existing forecasts, the shares are trading at a PER of about 12x. Given the latent potential of the company, and even if the company will probably miss its forecast, I still think this one is quite interesting.

Polar Capital Holdings (LON:POLR)

Down 4% to 466p (£473m) (includes the effect of 32p ex-dividend) - AuM Update - Graham - AMBER/GREEN

There is a pleasant 8% increase in Polar’s AuM in Q1 (April to June), although this is thanks to market movements rather than flows.

As the table above shows, flows were negative (£0.6bn), while market movements pushed up assets by £2.7bn.

As a rule of thumb, flows are far more important than market movements when it comes to assessing fund manager performance. Flows represent customer demand, while market movements do not!

CEO comment:

"There has been continued demand for a broad range of our funds during the quarter…

During the quarter, the open-ended Technology fund saw net outflows of £162m, an improvement on the £200m of net outflows seen in the previous quarter. Over the calendar year to 30 June 2025, as global indices broadened out, this actively managed fund was 8.5% ahead of its benchmark. Elsewhere, the remaining net outflows this quarter were primarily from the closure of an institutional mandate managed by the Healthcare team and an asset allocation change by a single Emerging Markets Stars client. Despite near-term market volatility, the new business pipeline for the Emerging Markets and Asia team remains strong.

Graham’s view

It’s unfortunate that Polar is now experiencing outflows, as it was one of the very few in the sector that somehow managed to avoid this.

But it is still possible to write off these flows as being rather small and inconsequential.

The Technology fund may have a better time attracting funds in the year ahead, now that it’s outperforming its benchmark.

And the other outflows can be classified as one-off changes that aren’t necessarily indicative of a broader change in client sentiment.

Furthermore, positive market movements can easily overwhelm and offset these outflows, as demonstrated by the overall quarterly AuM movement.

So I’m not panicking here. Bear in mind that I already moderated my stance on this to AMBER/GREEN, as I acknowledge that it’s possible to construct bearish arguments on all active fund managers, including Polar. I do still view this as a manager of the highest quality, and it remains one of the managers where I’m most optimistic about their future. Hopefully these quarterly outflows are just a bump in the road.

Jupiter Fund Management (LON:JUP)

Up 12% to 121.88p (£648m) - Graham - AMBER/GREEN

This is another fund manager where I’ve been quite positive - see my coverage of its Q1 trading update in April, where I thought flow performance was much improved compared to the prior year.

It has also offered exceptional value (much more than Polar),although recent share price gains have erased some of this exceptional value:

For context, in April, Jupiter stock was offering £114 of AuM for every £1 invested in it.

Today’s news is that Jupiter is buying CCLA Investment Management Limited, the asset manager for the non-profit sector, for £100 million.

CCLA has over £15 billion in AuM, so this is a step-change in Jupiter’s overall scale (Jupiter had £44 billion of AuM at the end of Q1).

It’s also a very attractive price being paid in terms of the sheer scale of the assets being bought in. Jupiter is getting £150 of AuM for every £1 it is spending on this deal.

That’s much cheaper than Jupiter itself was trading at, in the April doldrums.

Strategically, Jupiter are very happy with the transaction:

The Acquisition is highly compelling from strategic, cultural and financial perspectives, delivering progress against multiple objectives.

As well as the highly recognised and respected CCLA brand, the investment teams and client engagement model will be preserved, to ensure their clients continue to receive the consistent, high quality client service that they expect.

The Acquisition marks a significant step forward in delivering on Jupiter's key strategic objective of increasing scale, specifically within its home market of the UK. It also opens up a new client channel and provides complementary investment expertise with a high degree of cultural alignment.

Capital allocation framework - in separate news, Jupiter announces that it going to not just pay out 50% of pre-performance fee earnings in an ordinary, but it will also pay out 50% of performance fee earnings in the form of a special dividend or buyback (or both).

Graham’s view

In relation to the CCLA deal, I’m left wondering “what’s the catch”? CCLA is said to have generated “net inflows into long-term funds each of the last 15 calendar years”, which is not what I would have expected, at least for the last few years.

CCLA’s underlying operating earnings were “just under £13m million” in the most recent financial year, which also suggests a reasonable earnings multiple being paid after taxes are accounted for.

Jupiter are targeting “run-rate cost synergies of at least £16 million”, which should further boost profitability and reduce the effective multiple paid (although one-off costs to achieve this will be c. £17m after tax, to be incurred over several years).

I’m tempted to upgrade my stance on this to GREEN but I’ll stay calm for now. There is still a major negative trend facing this sector, and there may be a catch that I’m unaware of. But based on what I know so far, I’m giving this acquisition two thumbs up

Mark's Section

Macfarlane (LON:MACF)

Down 11% to 103p - Trading Update - Mark (I held) - BLACK/AMBER

It is bad news from this straight-talking packaging manufacturer and distributor:

In a year of challenge and economic uncertainty, we currently expect full year 2025 Adjusted Operating Profit to be approximately 10% below 2024.

They don’t make many adjustments (just amortisation and deferred contingent consideration changes) and don’t attempt to sugar-coat it, which is nice to see. However, there is no getting around that this is a miss versus expectations, which were for a strong recovery in EPS:

Their broker, Shore, reveals what this means:

Our revenue line for FY25F reduces by £3m to £307m, EBIT by £4.7m to £24.7 (-16%), with adj. PBT at £21.1m (-18%) and adj. EPS at 9.8p (-19%). We also cautiously reduce our expectations for FY26F, revenues falling by just £1m to £320m, with EBIT reducing by £4.7m to £25.9m (-15%), with adj. PBT at £22.4m (-15%) and adj. EPS at 10.4p (-15%). The balance sheet remains robust with net debt well within facilities. We retain our prior dividend forecasts, and the company confirms the continuation of its share buy-back programme.

As is usual with companies that have net debt, the scale of the miss increases as you go down the income statement, leading to a 19% reduction in FY25 EPS. More worryingly, Shore reduce FY26 expectations by 15% showing they think this is more than a one-off. This is especially disappointing as the company mentions a specific focus on increased cost-cutting which should be feeding through by then. These are the reasons given for the miss:

Distribution is experiencing weaker than expected demand, delays in new business decision making, pressure on gross margin due to the competitive environment, rising input prices and slower than anticipated recovery of labour and property-related cost increases.

Manufacturing Operations is performing robustly with good momentum with our aerospace and defence related customers and the benefit of the Polyformes acquisition, marginally offset by the slowdown in those sectors where customers are being impacted by uncertainty over US tariffs.

Sounds like a perfect storm of delays, margin and cost pressures. As a distributor, there is no escaping the end market conditions in which they operate. At the time of their AGM statement, they said that Q2 had started with strong momentum, and they specifically reference this today:

We highlighted in our AGM statement that market conditions in 2025 were challenging. It is disappointing that the momentum increase we experienced early in Q2 2025 has not been maintained and as a result will impact our full year performance.

I don’t think there was any attempt to mislead investors, and market conditions have simply not been as they expected. This is perhaps a canary in the coal mine for other businesses that rose on what appeared to be a recovery in trading in early Q2.

Macfarlane are keen to point out that they are comfortable enough with debt levels (and presumably so is their bank) for them to continue to buy back shares. This may provide some short-term share price support. However, Shore increase their estimate for net debt at the end of 2025 from £16m to £22.8m on this update. This may well start to limit the company’s ability to make acquisitions, which has historically been the main source fo their growth. And it occurs at a time where they may want to take advantage of weak market conditions to strike good deals.

Mark’s view

I held shares here this morning, so this warning was a bit of a surprise. This was a relatively modestly priced high-quality business that has a history of compounding earnings at a reasonable rate (although mainly through acquisition) and was forecast to return to growth this year. The Stockopedia algorithms liked it too, rating it a Super Stock, and the share price was recovering. However, none of this precludes a profits warning, as today has proven.

It was hard to know how to react this morning. This warning doesn’t change the long-term story of a quality company compounding earnings. However, a multi-year warning means the near-term rating is around 20% higher (assuming no price change), and this didn’t look as good value. These things aren’t exact, though, and if I thought it was sufficiently undervalued on a 2026 P/E of 9, surely it isn’t a sell at a P/E of say 10 (after a drop in share price). There is also the tendency for companies to take longer to turn around than expected, which can lead to further warnings. Even without another warning, forecasts are now for little growth over the next few years, making the investment case weaker - perhaps this will never return to previous levels of EPS growth.

Weighing all this up, I let price be the determining factor in my decision. After all, value investing is about capitalising on perceived differences in value and price. If the price has dropped more than the decline in value, it is a buy. If the price hasn’t dropped enough to provide a margin of safety between price and value, it's a sell. The price has been volatile today (perhaps due to the company continuing to buy back shares), making it difficult to form a personal view, as it changes by the minute. I took the opportunity to sell my shares today when the price hadn’t fallen as much as the drop in 2026 EPS forecasts. It remains on my watchlist and I’d probably be a buyer again if it dropped to 7-8x the now reduced EPS, despite the risk of a further warning. That probably makes it an AMBER for me.

Trifast (LON:TRI)

Up 1% to 70p - Final Results - Mark - BLACK (AMBER)

This fastenings company is undergoing a transformation program in an attempt to return to its previous operating margins. Their “ambition“ is medium-term EBIT margins greater than 10%. They have made some progress against this aim in FY25. However, this isn’t helped by a revenue decline:

The company say this is partly due to a strategic decision to exit some low margin business. Overall, it is a little difficult to work out exactly how these line up versus expectations. On the surface these appear to be a slight miss on revenue, beat on adjusted Net Profit, but a miss on EPS:

Cavendish say these were in line with their expectations. Zeus say:

The operational improvement in margins means operating and pre-tax profit were marginally ahead of Zeus estimates despite revenue being slightly lower.

They appear to gloss over the fact that their previous EPS forecast was for 5.8p of adj. EPS and this figure came in at 4.3p! Dividend being held at 1.8p is below their expectations of a small increase to 1.9p. Perhaps the best that can be said is that these results are mixed.

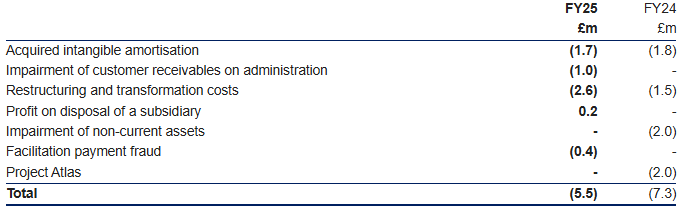

This is also a company that reports a significant gap between adjusted and statutory results. Here’s the breakdown:

Most of these look one-off, but they are not all non-cash. They also don’t appear to have credit insurance in place for all customers, making this an ongoing risk in weak economic conditions. I think we have to conclude that this is the type of business where restructuring costs will be an ongoing recurring cost for the foreseeable future. Excluding these when the current focus of the business is transformation through cost-cutting and operational improvements looks like a bit of having your cake and eating it to me!

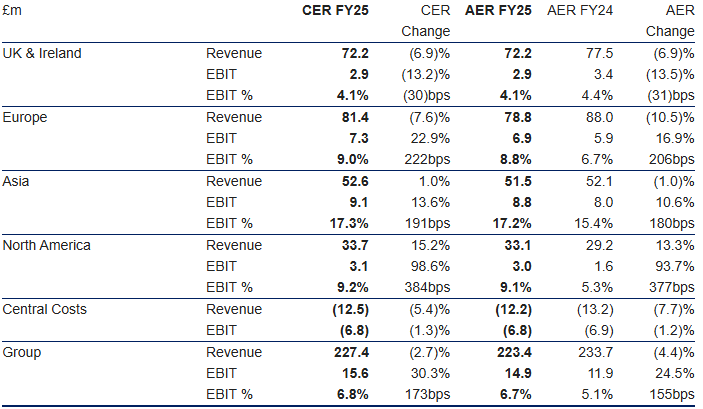

Regional Breakdown:

UK & Ireland remains a weak spot, and EBIT margins here are both lower than the group average and declining:

The company say part of this is due to a warehouse move and consolidation in the UK at the end of the year. However, this can’t be the full story, and on the IMC call, they confirm that the weak UK automotive sector is largely driving this. Other regions appear to be performing well, although there is little revenue growth anywhere.

Balance Sheet:

The company have done well reducing their inventories, although this is no doubt helped by reduced revenue:

Net debt reduced and is now below 1x EBITDA:

This gives them the possibility of considering bolt-on acquisitions again. Although the static gross debt and lack of dividend growth suggests they don’t feel as comfortable with the debt level as they may first appear. This could be due to working capital swings during the year.

Net assets have declined slightly:

Mainly due to a drop in intangible assets:

Meaning net tangible assets have only declined by £0.2m to £87.7m.

Outlook:

This is quite a weak sounding outlook statement:

Trading headwinds have continued to persist into Q1 FY26 due to:

· Macroeconomic headwinds impacting a number of industrial markets, with particular Automotive sector softness

· US tariffs on steel and aluminium, disrupting sourcing and costs

· The weakening USD.

While there was some doubt as to how the FY25 results stacked up with expectations, there is no doubt here that this outlook is disappointing. Cavendish say:

Forecasts: We are reducing our FY26E forecasts, with a 4.3% YoY cut in revenues to £214m, down 13.4%. Lower volume drop-though and further operational performance initiatives result in an adj EBIT of £16.1m, a YoY increase of £1.2m, with margins progressing to 7.5%. This gives adj PBT of £11.7m, with adj EPS at 6.5p, down 22.0%. We reduce our dividend due to the FY25 held dividend, and lower FY26E expectations, with a YoY uplift to 1.9p. Cash generation reflects the profit downgrade, albeit still with a YoY improvement, but also good working capital management, with net debt of £8.8m

Zeus:

…weaker volumes lead Zeus to reduce FY26 revenue by 11% to £214.0m, which, when accounting for unchanged EBIT margin expectations of 7.4% (+70bps yoy), mean adj. EBIT falls 11% to £15.8m (prior: £17.7m). Adj. PBT falls 13% to £11.5m but is still 15% higher yoy.

Zeus’ EPS estimates drop by a similar amount to Adj. PBT.

Valuation:

Making my own updated consensus I get 6.55p EPS for FY26, with £10.4m net debt ex-IFRS16. Zeus expect EPS to grow to 8.7p in FY27 and then 10.8p in FY28, with net debt further declining. Cavendish don’t appear willing to make forecasts beyond FY26 so future years should probably be viewed with a pinch of salt at this time. At the current 71p to buy this makes the forward multiple 10.8x, or around 12x if you debt adjust it.

This isn’t unreasonable if you assume that the transformation program will deliver the results the company say they will. However, that delivery has taken a step backwards with today’s results, and in particular the FY26 outlook, making a dent in confidence.

This trades on a P/TBV of 1.14, which shows that this is modestly rated if they can make those assets productive again, but that this isn’t necessarily a buy on assets alone. This could provide some downside protection, though.

Mark’s view

The cuts to FY26 revenue and EPS with a static share price mean that the forward valuation multiple has increased here today. While the long-term recovery story looks intact, market conditions mean that this moves further into the future. This effect doesn’t look severe enough to change my previous AMBER stance here, though.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.