Good morning!

We have one major profit warning to look at today, from Accesso.

In personal news, I've started spread betting again, for the first time in several years.

The point of this will not be to get rich (!), but merely to open a range of small positions where I don't have the funds or the conviction yet to create full-size positions.

While I don't recommend spread betting, as it's highly risky and most people lose money doing it, I do have a suggestion for those who already engage in it: make sure you compare the standard daily funded bets vs. forwards on the same instrument.

The daily funded bets have an overnight financing charge which I think adds up to c. 7-8% annualised, depending on interest rates at the time and the provider you're using. On the other hand, forwards have a wider initial spread but no ongoing financing charges. For positions being held for several months or up to a year, I think they are far superior!

2pm: all finished there, have a good weekend everyone!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.) (£61.7bn) | Upstream production in Q2 now expected to be higher vs. prior quarter. | ||

Flutter Entertainment (LON:FLTR) (£37.6bn) | Flutter pays $1.755bn for 5% of Fanduel. Flutter now owns 100%. Extension of US partnership. | ||

| Smarter Web (OFEX:SWC) (£948m based on latest share count) | Bitcoin Purchase | Total bitcoin holdings increase to 1,275 (value £110m), and has £31m in cash. | RED (Graham) [no section below]

Net worth is £141m plus the value of a small web design agency, and yet the market cap is £948m. The way I see it, the only way this can avoid crashing back to earth is if a) the bitcoin price bails them out, or b) they raise vast amounts of cash and invest it very cleverly. So it is theoretically possible that they could bridge the gap between their current net worth and their vastly larger market cap. But I wouldn't bet on it. |

Warehouse Reit (LON:WHR) (£490m) | Warehouse Directors switch their recommendation from BBOX to Blackstone’s new 113.4p offer. | PINK (Graham) [no section below] | |

accesso Technology (LON:ACSO) (£191m) | SP down 26% Revenue expected at lower end of range. Major customer does not intend to renew an agreement, $6m of gross profit impact. 2026 outlook to be updated when conditions are clearer. | BLACK (RED) (Graham) This still has quite some distance to fall before I think it would be in deep value territory. As it has now published profit warnings for two summers in a row, I think a RED stance is appropriate. | |

Premier Miton (LON:PMI) (£117m) | SP down 6% Net outflows £173m (prior quarter: net outflows £221m). £10.5bn AuM. | AMBER/GREEN (Graham) These days, I tend to be AMBER/GREEN on fund manager stocks. They offer great value against historic metrics, but the relentless trend of outflows does concern me. Still, they are intriguing! PMI is classified by Stockopedia as a Super Stock. | |

Sundae Bar (LON:SBAR) (£42m) | Raised £95k recently, has allocated surplus proceeds to Bitcoin acquisition. | RED (Graham) [no section below] Everything with a bitcoin treasury policy gets a RED from me. This one is interesting because as far as I can tell, they only managed to raise £95k from their recent retail offer. And these funds are the initial basis of their bitcoin treasury policy - I'll be impressed if they even have enough funds left over to buy one bitcoin, after costs. Interim results to March 2025 showed zero revenues and very little cash. | |

Westminster (LON:WSG) (£12m) | Interest-free credit from a major shareholder. Conversion price on CLN moves from 3p to 2p. | RED (Graham) [no section below) This has been around for a very long time but never seems to do very much for its shareholders. Recent interim results were again loss-making and the company has been raising fresh equity to fill the gap. Today's news is another form of equity raise with the lender agreeing to get more shares in exchange for an interest-free loan. |

Graham's Section

accesso Technology (LON:ACSO)

Down 23% to 367p (£148m/$200m) - Trading and Commercial Update - Graham - RED

accesso Technology Group plc (AIM: ACSO), the premier technology solutions provider for leisure, entertainment, and cultural markets, today provides the following update on its ongoing commercial performance.

We haven’t looked at this one in about a year. The last time we covered it was another profit warning, last summer, when Paul said he was “unenthusiastically AMBER”.

That profit warning, caused by delays to new park openings, also saw an over 20% drop in the share price.

There have been more downs than ups for shareholders in recent years:

Here is today’s warning:

For the six months ended 30 June 2025, Group revenue reflected softer than expected attendance across our customer portfolio. Our own performance held up well, but customer dynamics at key venues limited volumes and therefore reduced the transaction pool from which we drive a large share of our revenue.

This exposure - to the number of people who attend venues using Accesso’s technology - doesn’t sound like something that Accesso has any control over.

They say that they “remain laser-focused on delivery” for the rest of the key summer period. But I don’t see how their own performance can help to boost attendance numbers in the short-term.

Full year revenue will be “at the lower end of our anticipated guidance range”, and unfortunately the company does not provide this range in the RNS.

Checking the most recent full-year results, published in April, the company said that revenue growth in 2025 “is unlikely to exceed the effective 5.3% reported in 2024”. It seems that consensus was for growth of about 2%.

EBITDA margin guidance of 15% is unchanged.

Loss of business: a major customer does not intend to renew one of their agreements with Accesso, resulting in a gross profit impact of $6m from 2026.

They say that the revenue lost is “meaningfully offset by significantly improved commercial terms in the remaining agreements with the customer” and that “this underlines the strength of our ongoing relationship and the customer's continued belief in our ticketing platform as a mission-critical revenue solution”.

This wording makes me uneasy, as it sounds like they are trying to spin a defeat as some sort of a positive. The loss of $6m of gross profit is pretty significant for a company of Accesso’s size. Total gross profit was $119m last year.

Sales pipeline and recent wins: they say “we have been encouraged by the strength of our sales pipeline and a notable improvement in our commercial win rate”, and “it is clear that our revised commercial strategy is proving successful”.

2026 outlook is cloudy:

The Group will update the market on guidance for 2026 once trading conditions become clearer, further progress is made on our current commercial momentum, and the contract discussions with the major customer are concluded.

When the company published its profit warning in August last year, it did not include 2025 guidance in the RNS. Same thing today, with no 2026 guidance.

But brokers have published 2026 forecasts that are visible on the StockReport: revenue $164m, net profit $18.6m. In light of the statement above, I think we should treat these forecasts as being out of date.

Graham’s view

I like the fact that the company recorded net cash of $28.7m at its last full-year results. But apart from that, I’m finding a whole bunch of negatives:

Major profit warnings both this year and last year, during the key summer periods.

High dependence on attendance numbers at its customers’ sites, a variable beyond the company’s control.

No concrete guidance figures given in the RNS and no research or forecasts made easily available.

No significant growth. Perhaps revenue is about to fall in 2025 vs. 2024. Then the loss of $6m of gross profit in 2026 will need to be offset by new business.

Some of the narrative in today’s RNS has been too heavily massaged for my liking.

Sometimes I go for AMBER/RED when there is a profit warning but where I feel that the stock still has many redeeming features.

In this case, the net cash (and arguably the £8m buyback) are redeeming features, but the list of negatives is too long.

I’m therefore going to go fully RED on this for the time being.

In valuation terms, the market cap is equivalent to $200m (enterprise value: $171m).

The company was forecast to generate c. $16m of adjusted net income this year, prior to today’s profit warning.

If we adjust that down to $12m for the sake of argument, that gives a cash-adjusted P/E multiple of 14x.

In my book, it therefore still has quite a distance to fall before it would be in deep value territory. So I think a RED stance is appropriate for now.

Premier Miton (LON:PMI)

Down 6% to 67.1p (£120m) - Q3 AuM Update - Graham - AMBER/GREEN

The market doesn’t love this AuM update.

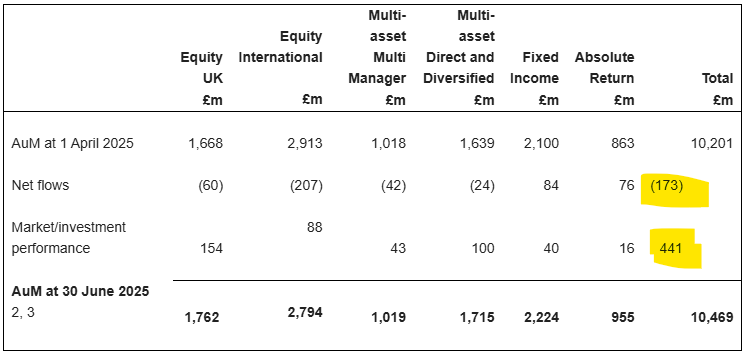

Premier Miton had £10.2 billion as of March 2025 (see our coverage of their half year results in May).

This has now increased slightly to £10.5bn.

However once again, the increase is due to market movements, with the company again experiencing outflows:

They point out that the outflows (£173m) were smaller than the prior quarter (£221m).

CEO comment:

"There were encouraging signs of progress during the Quarter despite reporting a net outflow overall. Demand for our absolute return and fixed income funds remained good, supported by consistent investment performance. Notably, net outflows from our UK equity funds reduced by over 50% compared to the average of the previous four quarters, reflecting improving investor sentiment and solid fund performance.

"While our European equity strategy recorded further net outflows of £132 million, this occurred alongside a strong period of performance, with the fund ranking second out of 130 in its sector over the Period. We believe that this positive performance will begin to translate into improved flow dynamics over the coming quarters.

Graham’s view

I note that at the Q2 update, they said their European Opportunities fund was experiencing outflows “driver by shorter term relative underperformance”.

Today they are pointing to a positive quarterly performance for their European strategy, but this is surely too short-term to be of any significance?

I’ve looked up their European Opportunities fund on Morningstar and I can see that it’s had a poor 2025 (7.5% return vs. benchmark 19.9%), and ranks very low against other funds for the year so far. But its long-term performance seems fine to me.

The scale of the outflows from their “International Equity” category is worth mentioning: 7% of starting AuM was withdrawn during the quarter.

Over the last six months, 11% of starting AuM has been withdrawn.

At least their other categories seem to be doing much better.

On balance, I’m inclined to leave our AMBER/GREEN unchanged here, as today’s update doesn’t seem to change all that much, even if it has disappointed some investors.

Like Polar Capital Holdings (LON:POLR) and Jupiter Fund Management (LON:JUP) (but not Liontrust Asset Management (LON:LIO)), this is categorised as a Super Stock. So it offers a bit of everything: quality, value and momentum - perhaps less momentum after today's move.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.