Good morning!

After the strikes in Iran over the weekend, markets are currently set to open as follows:

- S&P 500 down 1.5%

- FTSE down 0.8%

- VIX Volatility Index has moved from 21 to 22

- Gold up 2% at $5,400

- US crude oil up $5 at $72

Update at 11am: In Friday’s Week Ahead article, I rather optimistically hoped for a week in which we could ignore politics and focus purely on interesting investment opportunities.

That hope didn’t last long as we now have conflict in the Middle East with Iranian strikes today after the US carried out “Operation Epic Fury” in conjunction with Israel over the weekend.

While the FTSE is down by less than 1%, I thought it would be worth mentioning some of the bigger movers.

The fallers:

Informa (LON:INF) down 7% due to its Middle Eastern exposure

Croda International (LON:CRDA) and Smith & Nephew (LON:SN.) Both down 5-6% (SN has results today)

International Consolidated Airlines SA (LON:IAG) down 5%

Banks Barclays (LON:BARC) and Standard Chartered (LON:STAN) down 5%

And the risers:

Defence stock BAE Systems (LON:BA.) up 6%

Oil/commodities stocks BP (LON:BP.), Shell (LON:SHEL), Endeavour Mining (LON:EDV) up 2-3%

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

SSE (LON:SSE) (£33bn | SR64) | SSEN Transmission accepts Ofgem’s RIIO: T3 Final Determination | The transmission business has accepted the RIIO-T3 final determination as “an investable and deliverable settlement overall”. This price control period runs from April 2026 to March 2031. | |

Smith & Nephew (LON:SN.) (£11.7bn | SR53) | Revenue up 6.1% to $6,164m, Trading profit up 15.5% to $1,211m. Met or exceeded 2025 targets for revenue growth, profitability and cash flow. 2026 outlook: targeting further progress, expect Trading profit of c.$1.3bn with free cash flow “around $800 million”. | ||

Sage (LON:SGE) (£7.8bn | SR35) | Beginning share buyback programme of £300m, to be completed by 5 June 2026. | ||

Phoenix Group (LON:PHNF^K16) / Standard Life (LON:SDLF) (£7.7bn | SR57) | Phoenix Group will change its name to Standard Life from 8am today. New ticker is SDLF. Name change reflects organic growth strategy of Pension, Savings and Retirement Solutions business which already trades under the Standard Life brand. | ||

St Jamess Place (LON:STJ) (£7.1bn | SR86) | Re. 25 Feb announcement, beginning share buyback programme of up to £122.6m to be completed by 31 August 2026. | ||

Bunzl (LON:BNZL) (£7.1bn | SR76) | Revenue +0.6% to £11,845m, adj pre-tax profit down 9.8% to £787.1m. Op margin down 0.6% to 7.7%. 2026 outlook reiterated: “moderate revenue growth at constant exchange rates, operating margin slightly down”. | ||

Big Yellow (LON:BYG) (£2.1bn | SR46) | CEO and co-founder Jim Gibson will retire from 20 July 2026. He will be replaced by COO John Hunter. | ||

Energean (LON:ENOG) (£1.65bn | SR42) | Has received notice from the Ministry of Energy and Infrastructure to suspend production and activities at the Energean Power FPSO following the geopolitical escalation in the region. | ||

Oxford Nanopore Technologies (LON:ONT) (£1.29bn | SR37) | Revenue up 22.2% to £223.9m, gross profit up 24.6% to £131.3m. Net loss broadly flat at £145.2m (FY24 loss: £146.2m). 2026 guidance: revenue expected to growth by 21-25% at constant rates. Goss margin to be c.62, expect operating costs to rise by 0-5%. Expect to reach EBITDA breakeven in FY27. | ||

Senior (LON:SNR) (£1.29bn | SR63) | Revenue up 4% to £728.2m, adj pre-tax profit up 21% to £51.2m. Completed sale of Aerostructures division on 31 Dec 25. 2026 trading in line with expectations, outlook unchanged. | PINK (discussions with potential offerors) | |

PPHE Hotel (LON:PPH) (£837m | SR51) | Purchasing freehold of this 494-room hotel for £147.9m, of which £136.5m will be funded by a new debt facility. PPHE previously sold its interest in this hotel in 2017 for £161.5m and leased it back. | ||

GlobalData (LON:DATA) (£639m | SR29) | Revenue up 13% to £322.1m, underlying revenue growth of 1%. Pre-tax profit up 26% to £69.2m, including £20.5m credit on share-based payments. Adj EPS in line at 7.3p. Outlook: Contracted forward revenue up 5% to £179.7m. | ||

Craneware (LON:CRW) (£538m | SR42) | Revenue up 6% to $105.7m, ARR +4% to $184.2m. Adj pre-tax profit up 14% to $23.5m. Adj EPS +16% to 58.7 cents. $25m share buyback. 2026 outlook: in line with expectations. | AMBER/GREEN = (Roland) I leave our previous view unchanged today, but my feeling is the proprietary data and deep sector knowledge should provide some protection for Craneware from would-be AI competitors. The sharp contrast between high free cash flow and low reported profitability suggests to me that past acquisitions may have been fully priced – but I think this is a situation where further research could be valuable to help understand the long-term opportunity. I can’t do that today, so will retain my broadly positive view following the stock’s de-rating over the last six months. | |

ME International (LON:MEGP) (£516m | SR68) | Appointed COO Christophe Dantcikian with immediate effect. He has over 20 years experience in retail, convenience and vending businesses. | ||

Gulf Keystone Petroleum (LON:GKP) (£455m | SR74) | GKP has temporarily shut-in production in Kurdistan “in light of the developing regional security environment”. The company’s assets have not been impacted. | ||

Helical (LON:HLCL) (£254m | SR48) | Exchanged contracts to lease 19,628 sq ft of fitted space at The Bower in London. Letting is “in line with current ERVs” and increases total occupancy at The Bower to 87%. Negotiations are progressing on remaining vacant space. | ||

Tristel (LON:TSTL) (£192m | SR86) | H1 revenue up 14% to £25.65m, UK sales up 13%, overseas sales up 14%. “Sixfold growth in the USA”. H1 adj pre-tax profit up 11% to £5.47m. Outlook: firmly on track to meet FY expectations. | AMBER/GREEN = (Roland) Today’s results show decent H1 growth with continued progress in the all-important US healthcare market. However, US revenue remains relatively insignificant, at £262k, and the company has left full-year guidance unchanged. This suggests that the double-digit sales and profit growth seen in H1 is expected to slow in H2, with forecasts suggesting a reduction in margins and earnings for the second half of the year. It’s also worth remembering the impending departure of the CEO in June – a replacement has not yet been appointed. I can see some attractions here, but the current valuation suggests to me that new buyers may need a longer timeframe, Tristel shares don’t have the combination of value and momentum I’d need to be fully positive, so I’m leaving our previous view unchanged. | |

Focusrite (LON:TUNE) (£136m | SR85) | Founder Phil Dudderidge will step down as chair to become a NED. New chair designate Ian Barkshire will assume the role following July’s AGM. Barkshire was previously CEO of Oxford Instruments. | ||

Arrow Exploration (LON:AXL) (£57m | SR68) | The Mateguafa 10 well was spud on February 11, 2026, and reached target depth on February 18, 2026. It encountered multiple hydrocarbon-bearing intervals. Updates on various other wells provided. Total corporate production is approximately 4,900 boe/d. Cash balance US$7.2 million. | ||

Water Intelligence (LON:WATR) (£50m | SR88) | Strategic partnership between American Leak Detection and Lookout Labs, Inc, a US-based provider of smart water management systems doing business “Bluebot”. ALD will resell Bluebot productions. ALD will be Bluebot’s exclusive services partner with respect to installation, leak detection and repair for Bluebot products purchased over the internet. | ||

Hercules (LON:HERC) (£44m | SR90) | Advantage NRG, has secured new works with a combined contract value of c.£6.7m across the National Grid network in England. The new works run from March to October 2026. | ||

Gelion (LON:GELN) (£41m | SR5) | Total income £0.5m, adjusted EBITDA loss £2.4m, cash £10.5m. “Gelion is now recognised as an emerging global innovator in Sulfur battery technology, with the potential to achieve Tier‑1 status and corresponding value recognition through the remainder of FY26 and into FY27.” | ||

Gana Media (LON:GANA) (£41m | SR6) | “On track in our transition to delivering operational profitability and growth.” H1 revenue £1.05m, operating loss £1.5m. | ||

Kavango Resources (LON:KAV) (£33m | SR5) | Exercised option to acquire 100% of Nara Gold Project, Zimbabwe, consisted of 45 claims. The Seller “has now defaulted on the agreed terms of the Call Option Agreement.” Kavanago will “pursue all avenues to protect the interests of its shareholders”. | ||

FIH (LON:FIH) (£31m | SR64) | Has completed on a contract with TC Gosport Bidco Limited for the sale of PHFC, including its subsidiaries, for £11.62 million. | ||

Haydale (LON:HAYD) (£31m | SR9) | Launching an integrated subscription model across its SaveMoneyCutCarbon operations and JustHeat product deployments. | ||

Novacyt SA (LON:NCYT) (£25m | SR38) | Right issue: Shareholders can elect to acquire New Shares at €0.40 per Share, on the basis of 1 New Share for every 36 Existing Shares. Max raised €784,736. | ||

Skinbiotherapeutics (LON:SBTX) (£21m | SR7) | An interim CEO is appointed for six months, with immediate effect. | ||

Power Metal Resources (LON:POW) (£17m | SR56) | Strategic investment of US$1.5 million for an initial 4.6% shareholding in Greyridge Exploration Corp, the Canadian-based mineral exploration company focused on the discovery of copper and gold deposits in the Kingdom of Saudi Arabia. Has signed an MoU to explore joint ventures with Greyridge. | ||

Fulcrum Metals (LON:FMET) (£13m | SR13) | Average grades from surface across 26 new sample sites of 0.66g/t gold, 0.71g/t silver, 11.72g/t tellurium and 17.1g/t gallium, targeting previously unsampled and infill areas. | ||

Empresaria (LON:EMR) (£12m | SR55) | CEO and CFO appointed. CEO was previously CEO of Medacs Healthcare and Strategic Head of nGAGE Healthcare. | ||

Litigation Capital Management (LON:LIT) (£10m | SR21) | The debt covenant waiver from Northleaf that was due to expire at the end of February 2026 has been extended to 15 April 2026. Strategic Review continues while LIT works towards a long-term resolution of their capital position. | ||

Safestay (LON:SSTY) (£10m | SR54) | FY December 2025: revenue declined to c. £20.6 million (2024: £23.0 million). Adjusted EBITDA decreased to approximately £3.9 million (2024: £6.5 million) reflecting the revenue performance as well as inflationary pressures. The Board continues to consider various strategic options, including further disposals and/or the sale and leasebacks of properties. | ||

Genflow Biosciences (LON:GENF) (£10m | SR10) | Confirms receipt of the first instalment of €336,467 of the previously announced €4 million non-dilutive grant awarded by the Wallonia Region of Belgium. |

Roland's Section

Tristel (LON:TSTL)

Down 2.5% at 390p (£187m) - Half-year Financial Report - Roland - AMBER/GREEN =

Today’s results from infection prevention specialist Tristel are in line with the H1 guidance provided in January and show the infection prevention specialist enjoying rapid sales growth in the US – albeit from very low levels.

Share price progress has been limited over the last few years…

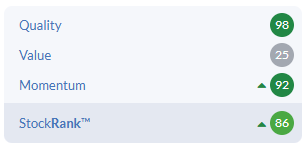

… but this is a bigger and more profitable business than it was in 2023. Today’s figures confirm that quality metrics remain strong and reiterate FY26 expectations. The rising StockRank also suggests momentum may be improving:

However, full-year expectations, reiterated today, suggest full-year earnings growth will be modest. Tristel also has yet to recruit a replacement for departing CEO Matt Sassone.

Let’s take a look.

H1 results summary

Performance has been driven by sustained momentum across our core markets, underpinned by volume growth, pricing discipline, and consistent commercial execution.

These results cover the six months to 31 December 2025 and showcase double-digit sales and profit growth:

Revenue up 14% to £25.65m

Gross margin “steady” at 81% (H1 25: 82%)

Adjusted pre-tax profit up 11% to £5.47m

Reported pre-tax profit up 36% to £4.96m

Adj EPS up 14.6% to 9.36p

Interim dividend unchanged at 5.68p

Net cash of 13.3m (H1 25: £11.7m)

The majority of revenue growth appears to have been driven by volume.

£2.5m of £3.1m sales growth was volume-related;

£0.6m was due to price increases.

Assuming price rises were applied equally to all sales, this suggests prices may have risen by 2% to 2.5%, perhaps slightly below inflation.

However, it’s worth remembering that for the NHS at least, pricing is set by multi-year agreements. In FY24, Tristel secured a new NHS contract that included significant price rises, but also fixed pricing.

My conclusion from this is that price rises may have been greater than 2.5% in some other markets.

Overall, I’m encouraged by the split between price and volume growth in H1.

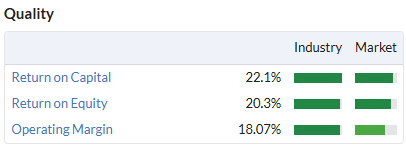

Profitability certainly remained robust and improved at a statutory level:

Rreported operating margin for H1 was 19.1% (H1 25: 16.2%)

My sums suggest a trailing 12-month return on capital employed (ROCE) of 24.7% (FY25: 22.1%).

These figures are consistent with last year’s results, highlighting Tristel’s strong quality credentials:

Cash conversion is also strong. H1 net profit of £4.0m was converted to £4.2m of free cash flow, by my calculations – an excellent result.

The dividend should be covered by free cash flow this year, in my view, providing solid support for the near-4% yield.

Results by location

At the core of Tristel’s business are its sales to the NHS, where it is a dominant supplier of disinfectant products for certain purposes.

UK sales rose by 13% to £9.88m

However, the UK business is relatively mature and it’s overseas – specifically the US – where the market is hoping to see significant growth. Overall overseas growth was strong, with notable increase in a number of markets:

Overseas growth up 14% to £15.77m

Germany up 13.2% to £3.4m

Western Europe up 13.4% to £5.3m

Australia down 0.7% to £1.8m

Other ROW up 88% to £3.9m

US growth: I assume that results for the Americas are reported within the Other ROW category.

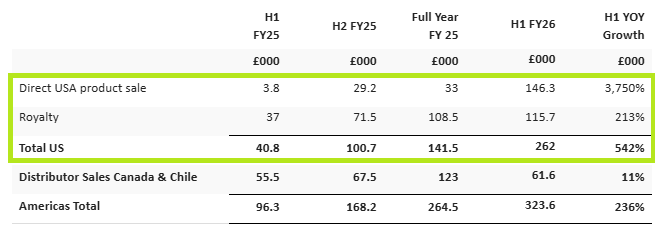

While Tristel does sell within Latin America and Canada, it’s the US specifically where hopes are high for growth. The company has helpfully provided a detailed breakdown of revenue from this region today:

In the top part of the table we can see that Tristel is selling products both directly and through a partnership with Parker Laboratories, which generates royalties for the company.

Total US revenue in H1 this year was 160% higher than H2 25. Given the high growth rate and lack of seasonality to this business, I think this sequential comparison is more useful than the conventional approach of comparing with the same period last year.

Commentary from management suggests continued progress with “leading US healthcare institutions” such as the Mayo Clinic and John Hopkins. The advantage of these is that they provide “important clinical validation and [are] expected to support broader market adoption over time”.

Operational indicators of market activity continued to improve, including increased product volumes, growth in recorded traceability cycles, and expanding training engagement, supporting evidence of deepening utilisation within customer accounts.

The Company also made progress in device manufacturer engagement, with compatibility confirmations and early IFU inclusions for Tristel OPH™ reducing barriers to adoption across ophthalmic applications.

Gaining a foothold in the US market was never going to be easy or quick. But while revenue of £262k was just 1% of total H1 revenue – fairly insignificant – the rapid growth in this market does seem encouraging to me.

Outlook & Estimates - H2 slowdown?

We are pleased with the results reported today and confirm that the business remains firmly on track to meet market expectations, for the year, with international expansion continuing to be a significant driver of growth.

Broker Cavendish has helpfully published an updated note today and has made this available on Research Tree. Many thanks.

Forecasts for the year are broadly unchanged, which Cavendish describes as reflecting “a conservative stance and noting the imminent departure of current CEO Matt Sassone”:

FY25A adj EPS: 17.1p

FY26E adj EPS: 17.7p (prev. 17.5p)

FY27E adj EPS: 19.4p (unch)

Two points are worth highlighting here. The first is that adjusted EPS growth is expected to be just 6% this year.

The second is that it looks likely that FY26 profits will have a modest H1 weighting.

Stripping out today’s H1 adj EPS of 9.36p suggests H2 earnings will be c. 8.34p per share, around 11% lower than H1.

According to the Cavendish forecasts, revenue growth is expected to be c.7% in H2 26. If this is the case, then it looks like margins are expected to be a little lower than in H1, reducing earnings.

Roland’s view

I don’t see too much to dislike in today’s results.

While it’s still too soon to know if Tristel can gain meaningful market share in the US, things do seem to be moving in the right direction with operational, regulatory and commercial progress.

The financial quality of the business and balance sheet remain strong, providing potential headroom for investment if needed and a stable base for future returns.

The main risk is that the valuation continues to price in a healthy measure of future growth:

As a result, investors hoping for truly impressive returns may need to take a long-term view on the likely success of US growth.

There’s also the uncertainty associated with a CEO replacement after a relatively short period in role – Sassone has decided to move back to the US with his family for personal reasons and will leave at the end of June, after less than two years in the role.

On balance I don’t see any reason to change our previous view of AMBER/GREEN today. I can see attractions here, but value and momentum do not seem strong enough to persuade me to take a fully positive view.

Craneware (LON:CRW)

Up 2% at 1,550p (£550m) - FY26 Interim Results - Roland - AMBER/GREEN =

We last covered Craneware in September 2025 (FY25 results) and November 2025 (AGM update), taking an AMBER/GREEN view on both occasions.

Since then, this specialist provider of US healthcare billing software has fallen victim to the wider AI-driven sell off that’s hit the software sector.

Craneware shares have fallen by more than 25% in six months, but my instinctive view is that this seems too harsh for such a company whose hospital customers are generally quite sticky and depend on the company’s products to help maximise their billing revenue.

Let’s see if today’s results support this view.

H1 results summary

Today’s headline numbers look positive to me and full-year expectations remain unchanged:

Revenue up 6% to $105.7m

Annual Recurring Revenue up 4% to $184.2m

Adjusted pre-tax profit up 14% to $23.5m

Reported pre-tax profit up 29% to $13.0m

Adjusted EPS up 16% to 58.7 cents

Interim dividend up 11% to 15.0p per share

Net cash up 18% to $47.8m

$25m share buyback

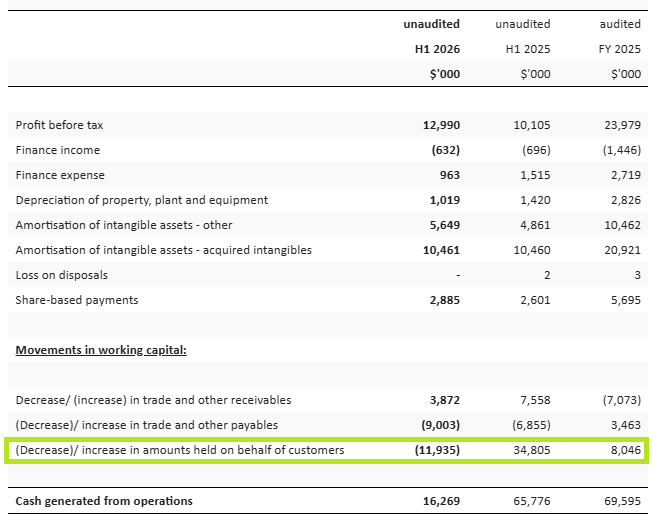

While net cash is positive, it’s worth noting Craneware’s reported cash balances include amounts held “on behalf of 340B customers”. This is a US Federal programme providing discounted access to certain outpatient drugs for eligible patients, although its future appears somewhat uncertain according to today’s management commentary.

As things stand today, Craneware holds a significant amount of funds relating to 340B. The amount held appears to be highly variable, presumably reflecting working capital cycles.

The H1 accounts show a $12m reduction in the amount held on behalf of customers, contributing to a large adverse movement in working capital:

Cash generation: stripping out working capital movements from H1 26 and H1 25 suggests to me that underlying operating cash flow generated by the business rose by 10% to $33.3m in H1. That seems a decent result that is consistent with the group’s adjusted EBITDA for both periods.

On the same underlying basis, my sums suggest Craneware generated free cash flow of $23.6m in H1, providing an exact match for adjusted pre-tax profit of $23.5m. As I’ve explained previously, this is why I’m (mostly) happy to accept the adjusted profit figures here – they are backed by cash generation.

Profitability: the one caveat to my comments above is that Craneware’s profitability appears to remain fairly low, when we fully reflect goodwill from past acquisitions ($235m). This accounts for 70% of balance sheet equity and reflects past spending decisions. I always think it’s informative to consider the returns now being generated from these acquisitions.

Craneware’s statutory operating profit for the half year was just £13.3m, giving a margin of 12.6% and a trailing 12-month ROCE of c.7%. These figures do not seem that impressive to me, for a software business that seems to have a reasonable moat and sticky customers.

In general, I see this mismatch between low ROCE and high free cash flow as an indicator that management has made good acquisitions in the past, but paid a full price for them.

Trading commentary: the company says it’s winning more new business while maintaining strong customer retention rates:

Sales to new customers rose to 12% of sales (H1 25: 2%), providing “significant future expansion opportunity”;

Net Revenue Retention of 103% (H1 25: 103%);

Customer retention rate “above 90% on all measures” (FY25: “over 90%”).

Craneware has deep sector knowledge and data for its niche, which I think should provide some protection from would-be AI challengers. However, the company is also leveraging AI technology itself to help develop new functionality:

Prior investments in data and access to advanced AI via partnership with Microsoft delivering accelerated innovation, with major new Trisus® functionality across multiple products set to launch in H2, supporting medium-term growth ambitions, further underpinned by high levels of ARR and strong customer retention

Outlook

High levels of expansion sales, healthy NRR and an increasing 340B Shelter opportunity underpin our confidence in a positive second half performance and delivery of results for the year ending 30 June 2026 in line with market expectations.

Consensus forecasts suggest adjusted earnings will rise by around 5% to $1.21 per share this year, based on last year’s adjusted earnings of $1.14, before picking up pace a little in FY27. This gives the stock a valuation that’s at the lower end of its historic range:

Roland’s view

I feel like this is a business I need to understand in more depth to take a view on its long-term growth potential. On the face of it, I can see considerable attraction here.

The financial side of US healthcare is notoriously complex and Craneware appears to be a respected specialist, providing tools that help hospitals ensure they are collecting all the revenue they are entitled to.

Cash generation is also extremely strong, suggesting to me that the quality of this business is higher than its reported quality metrics might suggest.

The downside is that growth expectations appear quite modest this year, when comparing consensus forecasts to last year’s adjusted earnings.

I’d also like to understand the group’s working capital movements and debt position a little more closely.

I am also intrigued to see the StockRanks currently view Craneware as a Falling Star, although it’s possible this will change when today’s interims are digested by the algorithm.

On balance I am going to leave our previous AMBER/GREEN view unchanged today, with the caveat that in-depth research might justify an upgrade (or downgrade) to this view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.