Good morning! It's a fairly quiet day for results today, as usual for Friday.

Today's agenda is now complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Berkeley group (LON:BKG) (£3.5bn | SR75) | Reiterates guidance for FY26 pre-tax profit of £450m “and a similar level for FY27”, together with target net cash of c.£300m. Trading has been constrained by consumer confidence. The situation in the Middle East “is weighing heavily on risk sentiment” and “we await to see the impact of this on the market”. | AMBER = (Roland) London brownfield specialist housebuilder Berkeley says profits for the year to 30 April 2026 should be in line with expectations, but warns of a hat-trick of headwinds: planning delays, cost inflation and the impact of the Middle East conflict on interest rates are all cited as current issues. With the stock now trading at around book value, Berkeley is cheaper than I can remember seeing this stock. I can imagine that value could emerge at this level. However, profit guidance reiterated today suggests the business is only likely to generate a return on equity of c.9% in FY26 and FY27. With no sign of improving momentum, the price looks fair to me against the current backdrop. I am going to leave my neutral view unchanged today. | |

Glenveagh Properties (LON:GLV) (£959m | SR72) | Revenue up 7%, with partnerships growth (+61%) offsetting a 14% fall in homebuilding revenue. Home completions up 11% to 2,568. Pre-tax profit up 10% to €125m, EPS up 18% to 20 cents. Forward order book up 41% to 1,252 homes (+15% to €1.3bn). Outlook: “strong momentum”, guiding for EPS of up to 21 cents. Expect completions of c.2,750 units. | ||

VAALCO Energy (LON:EGY) (£441m | SR82) | Production of 21,160 working interest boepd (16,556 net revenue interest). Full-year net loss of $41.4m, positive EBITDAX of $173.4m. Declared quarterly dividend of $0.0625 per share. | ||

CLS Holdings (LON:CLI) (£233m | SR54) | EPRA earnings down 17% to £30.2m, EPRA EPS -17.4% to 7.6p. Dividend of 4.0p per share. EPRA NTAV per share down 6.7% to 200.7p due to falling property values. Vacancy rate increased to 14.5% (2024: 12.7%) due to lease expiries in London and Paris plus two insolvencies in Germany. LTV was 50% at year end (2024: 50.7%). | ||

Stelrad (LON:SRAD) (£170m | SR79) | Revenue down 3.8%, adj operating profit up 3% to £32.5m. Adj EPS up 0.2% to 13.08p with total dividend up 3.9% to 8.09p. Outlook: “Trading in the early months of the financial year has been in line with management expectations”. End markets are stable but demand remains subdued. | AMBER = (Roland) Last year was difficult and saw a 4% decline in volumes due to soft conditions in the UK and Europe. However, Stelrad has now completed various restructuring activities and appears to be able to support margins if sales don’t worsen further. Cash generation was also impressive last year, in my view. With the stock trading on a forward P/E of 9 and offering a 6% yield, I am tempted to upgrade to AMBER/GREEN today. I’ve added the stock to my watch list, but Stelrad’s relatively high debt levels and the uncertain timing of any market recovery mean I’ve opted to leave my neutral view unchanged today. | |

Atlantic Lithium (LON:ALL) (£122m | SR18) | Awaiting ratification of mining lease for Ewoyaa Lithium Project in Ghana. Continued exploration in Côte d'Ivoire with “new spodumene pegmatite occurrences discovered”. Company has entered into a £28m financing arrangement to support the Ewoyaa project, plus an £8m share placement agreement (£4m raised so far) and a “committed equity facility” for up to £20m. Company has ceased discussions relating to a potential corporate transaction. | ||

EnSilica (LON:ENSI) (£47m | SR49) | Proposed equity funding to raise up to £10m (12/3 4.35pm) & Result of oversubscribed Placing and Subscription | Raised gross proceeds of £9.7m at 47p per share in an oversubscribed placing that was announced after markets closed on Thursday. Funds will be used to “progress user-terminal Application Specific Standard Product (“ASSP”) chips to accelerate potential supply revenues and unlock approximately £2.0m in matched funding from the previously announced £10.38 million non-dilutive UK Space Agency Award.” Also running a £0.3m retail offer at 47p that is expected to be open until 4pm on 17 March 2026. | Roland: 47p represents a fairly modest 4% discount to yesterday’s closing price of 49p, suggesting decent demand from investors. |

Digital 9 Infrastructure (LON:DGI9) (£44m | SR n/a) | Funds managed by IFM Investors (a minority shareholder in Arqiva) have agreed to sell their 14.84% interest to Polus Capital Management for £8.9m. This implies a valuation of c.£60m for Arqiva. “D9 and Polus are aligned in their commitment to work actively with Arqiva’s management”. D9’s 51.8% economic interest in Arqiva is unchanged. | ||

Zenith Energy (LON:ZEN) (£30m | SR43) | Acquired two agrivoltaic development projects in Piedmont, Italy, with an expected installed capacity of 23 MWp and 5MWp. Has also secured sufficient land to install a 5MW BESS. Total consideration for acquisitions is €2,016,000. | ||

Atome (LON:ATOM) (£25m | SR5) | Signed debt financing documents with lenders for the $420m total debt package that forms part of the $650m fertiliser plant project at Villeta, Paraguay. Equity documents are in the final stage of negotiations and will set out details of the project's $244m equity funding. | ||

Jangada Mines (LON:JAN) (£17m | SR27) | 1,100m 10-hole programme completed targeting TP2, a 1km anomaly that is one of six potential targets identified. Gold mineralisation intersected in all holes, with a minimum of 0.5g/t AU. | ||

Transense Technologies (LON:TRT) (£10m | SR43) | Secured new contract as part of “DriveSense” project supported by the APC R&D programme being led by Cummins to develop next-generation smart electric drive systems for heavy-duty vehicles. The project is expected to complete in December 2026. Transense’s element of the project is valued at c.£0.6m. | ||

Reabold Resources (LON:RBD) (£10m | SR60) | An investor group has agreed to subscribe for £1.9m of new shares at 0.1p per share, conditional on Reabold raising a further £1.1m by 12 May 26. This funding is expected to be used to progress the West Newton project, including the company’s share of the recompletion of the A-2 well. |

Roland's Section

Berkeley group (LON:BKG)

Down 3.5% at 3,608p (£3.4bn) - Trading Statement - Roland - AMBER =

In my recent piece on housebuilders I highlighted high-end developer Berkeley as the most profitable UK-listed housebuilder (over the last 12 months) and one of my picks from this sector, in terms of quality.

Berkeley has deep expertise in redeveloping large brownfield (former industrial) sites and is mainly focused on London. It has an impressive track record, but today’s update makes clear that the business isn’t immune to the pressures facing housebuilders generally and London developers in particular.

Here are the key points from today’s trading update, which covers the period from 1 November to 28 February and comes ahead of the group’s April year end:

Reiterated guidance for FY26 pre-tax profit of £450m, with “a similar level for FY27”.

Expected net cash of around £300m, following settlement of £250m of land creditors and £190m of shareholder returns.

Trading has been “constrained by the impact on consumer confidence of geopolitical events and macroeconomic uncertainty”. However, “sales enquiries remain good and the value of underlying reservations has been recovering towards the levels seen over the summer (2025) prior to the pre-Budget hiatus”.

While this year’s financial results are expected to be in line with forecasts, these comments suggest that sales have not yet recovered to the level seen prior to last November’s Budget.

Margins are still under pressure. Most of Berkeley’s developments are high-end flats, but average sale prices for flats fell by 6% last year according to Land Registry data. While Berkeley may have fared better than this (although we don’t yet know), cost inflation is an issue that appears to be threatening the viability of some developments:

We are working hard to counter the challenges we face and we are reviewing our planning consents to enhance and restore margins to the appropriate level to enable moving them into production.

Delays to planning are a further issue, particularly the “very complex” process required by the Building Safety Regulator for building control approval:

The poor initial implementation of the BSR has severely impacted the supply of new homes in London and other urban areas and we fully support Government's aspiration that the BSR becomes an enabling regulator as soon as possible.

Berkeley says it’s working with the BSR and that “good progress” has been made over the last six months, but approvals within the expected timeframe are still the exception to the norm.

Outlook

The impact of planning delays and cost inflation may now be compounded by the possibility that the conflict in the Middle East will result in higher inflation and mortgage rates, creating further affordability issues for buyers:

The emerging situation in the Middle East is weighing heavily on risk sentiment and we await to see the impact of this on the market. While reaffirming guidance, we are aware of the risk of a further deterioration in macro conditions with the potential for higher inflation in the near term and for interest rates to remain higher for longer.

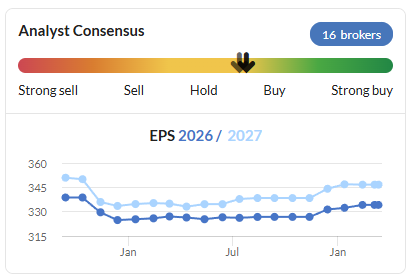

Broker forecasts have actually trended higher over the last year, but my impression from today’s update is that there’s a risk FY27 expectations could be moderated if the Middle East conflict continues to escalate:

Roland’s view

Berkeley is relatively unusual among UK volume housebuilders for its focus on complex, long-term projects. To take just one example, the group is currently working on a project to redevelop 24 former National Grid gasholder and industrial sites in London and the South East.

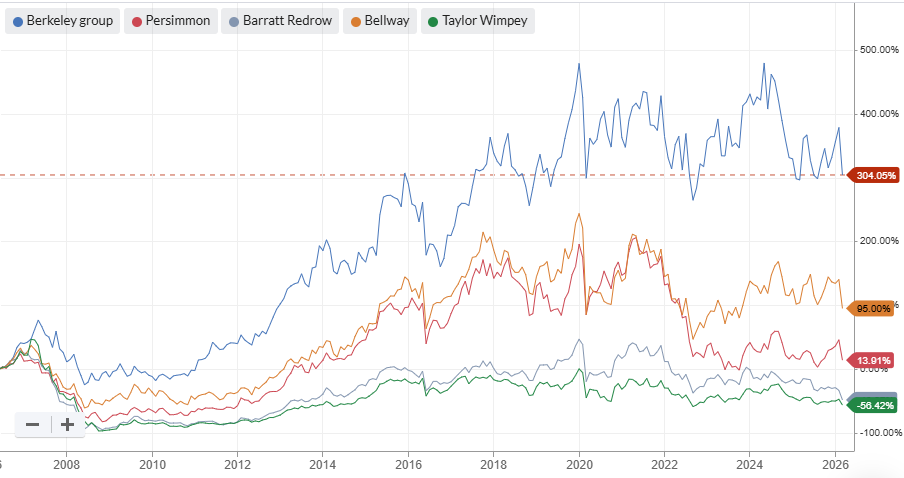

This brownfield strategy has generated terrific value for shareholders over the last 20 years:

However, executive chair Rob Perrins recently commented in an interview with the FT (paywall) that current obstacles to London homebuilding mean that “my biggest competitor for land is Big Yellow” (the self-storage group). Discussing the company’s Regent’s View gasholder development with the FT journalist, he said that if the site went on the market today, “a residential developer would not buy it”.

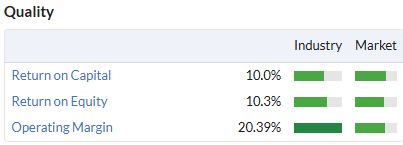

Admittedly, Berkeley’s trailing 12-month operating margin of 20% doesn’t immediately suggest the business is struggling to maintain the viability of its developments. But I think it’s notable that Berkeley – unlike many rivals – has maintained its profitability at a level where it’s able to support shareholder returns and cover its cost of capital:

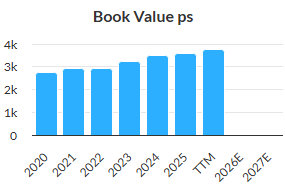

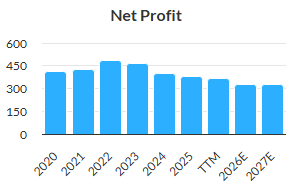

In evidence of this, the company’s book value per share has grown by an average 5% per year since 2020:

This has been achieved despite regular dividends and declining profits, highlighting the quality of the group’s capital allocation decisions:

I’ve always seen Berkeley as a classy operator and this view is unchanged today. Broadly, I also share the company’s view that the long-term outlook for London (and London residential property) is positive.

The question for me is whether the current valuation reflects the near-term risks, which appear to be growing.

One point in the company’s favour is that Berkeley shares are currently trading in line with or slightly below book value. That’s very unusual for this business, which has historically traded at a premium to book value:

However, at current levels, forecasts suggest the business will only generate a c.9% return on equity in FY26 and FY27. For that level of profitability, I’d argue that 1x book value is probably a fair valuation.

I think value could emerge at current levels, but hope is not an investment strategy.

With no sign of any improvement to momentum (and perhaps the risk of a downgrade) I am going to remain consistent with our system and leave my previous neutral view unchanged.

Stelrad (LON:SRAD)

Down 2% at 131p (£167m) - Preliminary Results - Roland - AMBER =

Central heating radiator specialist Stelrad warned on profits in November, but today’s full-year results appear to be in line with revised guidance.

I can see some things to like about this specialist manufacturer, which could be strongly geared to any recovery in demand. I’m interested to see whether today’s results and outlook justify an upgrade to my previous neutral view.

2025 results summary

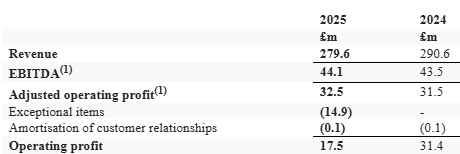

Stelrad’s headline figures for 2025 do not look too terrible if you’re willing to overlook some large adjustments – more on this shortly:

Revenue down 3.8% to £279.6m.

Adjusted operating profit up 3% to £32.5m.

Adjusted operating margin 11.6% (2024: 10.8%).

Adjusted earnings per share up 0.2% to 13.08p.

Reported earnings per share down 95% to 0.66p.

Net debt reduced by 14.3% to £51.2m.

Dividend up 3.9% to 8.09p.

I’ll come back to the company’s profits in a moment, but first I think it makes sense to review the trading environment Stelrad has faced over the last year.

Trading commentary: sales volumes fell by 4% last year, reflecting “well-documented market conditions” in the UK and Europe. Subdued conditions in housing and construction more generally are indeed well recognised. See my earlier comments on Berkeley Group.

Softer demand was reflected by the 3.8% drop in revenue, which breaks down as follows:

UK & Ireland: revenue down 4.4% against a volume decline of 6.9%, increase in average size of radiators sold.

Europe: revenue down 3.9%, primarily due to softer conditions in France.

Turkey & International: revenue rose by 3.9%, with improved market conditions.

The increase in adjusted profits was driven by cost-cutting and a continued shift towards a higher-margin sales mix, with the average profit contribution achieved from each radiator rising by 2% to £20.50 per unit.

The company says its On Time In Full (OTIF) delivery in the UK remained at 98% last year. Following a range of restructuring activities, including the exit of a loss-making contract in its Italian subsidiary, management believes the business is well positioned for a return to growth.

Profits - big adjustments: today’s results highlight a large gap between adjusted and reported profits:

Exceptional items of £14.9m need explanation, but I’m reassured to see that none are listed for last year – perhaps these really are one-offs.

Checking the accounts reveals that the bulk of last year’s exceptionals relate to impairment charges on the Radiators SpA business in Italy, where Stelrad exited a loss-making contract to produce steel panel radiators, having failed to renegotiate an acceptable new deal.

Unfortunately, this has resulted in a laundry list of impairment charges totalling £12.2m:

The main elements of the non-cash exceptional items relate to impairment of goodwill of £2.7 million, impairment of customer relationships of £1.4 million, impairment of property, plant and equipment of £5.8 million and a provision against inventories of £2.3 million, all within the Radiators SpA business.

These are described as non-cash, but some, if not all, of them relate to past cash expenditure.

According to AI, Stelrad acquired Radiators SpA in 2022 for around £24m. Today’s impairments suggest that a sizeable proportion of that original expenditure is now being written off.

The decision to exit the problem contract is expected to lead to a shortfall in revenue and volume in the near term. But the company plans to use this as an opportunity to focus on “the electrical and designer product ranges which are unique to this division and were the key strategic rationale for acquiring the business”.

Cash flow

Today’s cash flow statement is one of the highlights of these accounts for me.

Stelrad reports free cash flow of £20.5m today. My calculations produce an estimate of £19.8m, so I’m happy to use the company’s methodology in this case.

Free cash flow of c.£20m would give Stelrad shares a free cash flow yield of around 12% at current levels – potentially good value.

One caveat to this is that working capital movements were moderately favourable last year, mainly due to shrinking inventories. Forecasts from broker Singer Capital suggest this situation could reverse in 2026, reducing free cash generation. However my hope would be that if this happens, it signifies an improvement in trading (demand), so could be positive for medium-term returns.

On balance I’m quite impressed by Stelrad’s cash generation and don’t have any concerns here.

Balance sheet

I would be remiss not to comment on Stelrad’s balance sheet, which carries quite a lot of debt.

Today’s results show year-end net debt of £51.2m. The company says this equates to leverage of 1.16x EBITDA, which looks quite comfortable.

Personally, I prefer to look at leverage based on an estimate of how long it might take a business to repay its debt, rather than just service it.

Based on last year’s adjusted net profit of £16.7m (which was supported by free cash flow), I would look at Stelrad as having leverage of around 3x. That’s below my preferred limit of 4x, but I would ideally like to see this multiple fall further.

While I think Stelrad can probably afford this level of borrowing, it’s not without risk and is relatively expensive. Debt costs accounted for around a quarter of adjusted operating profit last year.

As far as I can see, the main reason why Stelrad’s debt levels don’t fall more quickly is the group’s generous dividend – last year’s payout will cost around £10m.

At current levels, the dividend provides a tempting 6% yield. While this is covered by free cash flow, it’s hampering debt reduction.

We might speculate that one reason the payout hasn’t been cut may be that CEO Trevor Harvey has a c.9% shareholding in the company. This means he’s in line to receive a dividend income of c.£900k this year in addition to his contractual remuneration.

Quality - return on capital employed

I am all in favour of companies focusing on return on capital employed as a key performance metric. But I always like to look closely at how this is calculated. In some cases, it’s calculated using non-standard measures that provide a more favourable view than the standard ROCE calculation used in the StockReport (which I also prefer).

Stelrad appears to be a case in point.

The company reports a very impressive adjusted return on capital employed of 30.1% for 2025 (2024: 27.1%).

My calculation of 2025 return on capital employed is 24% (using adjusted operating profit) or 13% using reported operating profit.

While Stelrad’s strong free cash flow means that I could be persuaded to use adjusted operating profit in this instance, I’m not entirely comfortable with the company’s definition of capital employed, which it terms Business Capital Employed.

If I’ve understood it correctly, this measure excludes cash held on the balance sheet, lease liabilities due within 12 months, and a deferred tax asset.

In a strictly narrow sense, I agree that this definition more closely reflects the actual capital directly employed in the manufacture and supply of its radiators.

From an equity perspective, I think the company’s definition is overly narrow.

In my opinion, it’s not realistic to suggest that a manufacturer with £76m of debt does not need to have any cash on hand to operate, for example. Nor does it seem realistic to exclude lease payments due within the current year from a view of the capital required to operate the business.

Despite this quibble, I think Stelrad does generate attractive returns on capital employed and could be a reasonably good quality business.

Outlook

Trading in the early months of the financial year has been in line with management expectations. The Group's end markets are stable, but market demand remains subdued, and we expect this to continue for at least the first half of 2026. In the meantime, the Group continues to leverage operational opportunities to optimise future growth and profitability.

Stelrad says it’s well positioned for a market recovery, but highlights that the timing of any improvement in conditions remains uncertain.

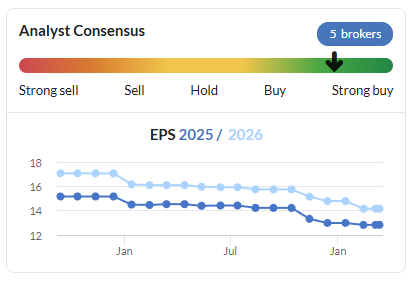

I don’t have access to any updated broker forecasts today, but I would guess that most broker estimates will remain largely unchanged following today’s results.

Consensus forecasts have moved significantly lower over the last year, but have stabilised since November’s profit warning:

FY26 forecasts suggest adjusted earnings of 14.2p per share. That would put Stelrad on a P/E of 9.2x at current levels, with a 6% dividend yield.

Roland’s view

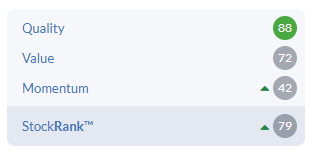

Stockopedia’s algorithms were styling Stelrad as a Contrarian pick ahead of today’s results, and I am inclined to agree. The StockRanks highlight strong quality and value metrics and momentum has been improving recently:

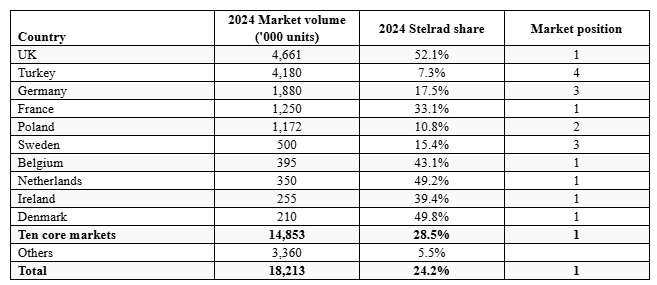

While I have some reservations about the level of debt in this business, I’m quite impressed in some other ways. Stelrad claims to be the market leader in six of its 10 core markets and has shared some quite impressive market share figures today (note that these relate to 2024):

The main risk I can see is that demand could continue to fall this year. If that happens, it could lead to further downgrades and pressure on the group’s profitability. In that kind of scenario, the debt could become more of an issue.

However, if I adopt the view that last year was likely to be a low point for earnings, then I think there’s a strong case to be made that Stelrad shares could offer good value at current levels.

I’m tempted to turn positive today, as I was for similar reasons with Berkeley Group.

However, given the uncertainty over the outlook and the recency of Stelrad’s last profit warning, I think it might be more consistent with our methodology to leave my neutral view unchanged for a little longer. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.