Good morning!

Yesterday was a remarkable day in the markets. The FTSE was down by 250 points until 11am, when it made a complete reversal in the space of about 10 minutes, as investors reacted to breaking news re: Trump's attitude to the war with Iran. The timing of that news is thought to have been designed to coincide with the open of US markets.

In company-specific news yesterday, there was also the remarkable profit warning, and share price reaction, at Goodwin (down 48%).

The latest overnight action has been more relaxed. The FTSE is set to open up slightly today, at around 9900. There are still fears that the war with Iran could escalate to involve civilian infrastructure, but the short-term risk of that happening is thought to have passed.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Kingfisher (LON:KGF) (£5.0bn | SR100) | Underlying LfL sales +1.4%. Adjusted PBT +6% (£560m). Guidance: Adjusted PBT of £565m-£625m and free cash flow of £450m-£510m. New £300m buyback. | ||

Bellway (LON:BWY) (£2.5bn | SR73) | Underlying operating profit +1.5% to £159m. Volume output in FY26 is now expected to be ahead of previous guidance at between 9,300 and 9,500 homes. Average selling price anticipated to be £325k (previously £320k) due to product mix. On track to deliver FY26 underlying operating profit within the range of £320m - £330m. | ||

Trustpilot (LON:TRST) (£914m | SR74) | Marcus Roy appointed Chief Financial Officer following “a thorough and wide-ranging search”. He has been Group CFO of The Economist Group since 2021. | ||

Fevertree Drinks (LON:FEVR) (£871m | SR63) | Revenue +4% at constant currencies (+2% at actual currencies). Adjusted EBITDA down 16% (£42.4m). Outlook: Notwithstanding the current uncertain geopolitical outlook, our expectations for 2026 remain unchanged and in line with market expectations. | ||

CVS (LON:CVSG) (£797m | SR37) | The CMA's final decision does not introduce any new remedies over and above those announced in its provisional decision. The Board expects the Group to continue to trade in line with market expectations. | ||

Gamma Communications (LON:GAMA) (£759m | SR61) | Revenue +11%, adjusted PBT +7% (£119.4m), actual PBT down 8% (£87.7m). Outlook: The Board expects FY 2026 financial performance to be in line with market expectations, with Adjusted EBITDA and Adjusted EPS (fully diluted) within the consensus range. | ||

M P Evans (LON:MPE) (£758m | SR98) | Average mill-gate price for CPO $866 per tonne (2024: $823). Revenue +5%. EPS 161.3p (2024: 129.6p). “Since the year end, crops have continued to increase in the early part of 2026, and pricing for the Group's output remains strong." | ||

Bytes Technology (LON:BYIT) (£708m | SR49) | FY26 results in line with the outlook provided in October 2025. For FY27, we expect high single-digit to low double-digit percentage growth in gross profit, with operating profit broadly flat as the Group absorbs c.£4.5m of cost normalisation, reflecting higher technology costs following the completion of strategic projects and a return to normal bonus levels, on top of continued headcount investment for growth. | BLACK? (AMBER/RED =)(Roland) We don’t have access to updated forecasts this morning, but this looks like another profit warning to me, this time downgrading profit expectations for the year ahead due to higher costs. This issue aside, I don’t think there is anything terribly wrong here. I estimate the shares may now be trading on a forward P/E of c.12x with a possible 7% yield. I’m going to leave our AMBER/RED view unchanged to reflect today’s apparent downgrade, but if the company can start delivering in line results this year then I think the value on offer could become interesting. | |

Chesnara (LON:CSN) (£689m | SR44) | Adjusted operating profit up 42% (£56m). Assets under administration +10% (£15bn). £140m. “...we continue to see further opportunities to grow, with a positive M&A pipeline and a great track record of disciplined execution.” | AMBER/GREEN = (Graham) Though the market cap is less than £1 billion, I classify this as a complex financial stock, the same as I do with the High Street banks and very large insurers. What this means practically is that I accept I’m never going to have a very strong conviction in it - it’s simply too complicated to analyse for someone like me who is also studying lots of other companies. | |

Everplay (LON:EVPL) (£378m | SR49) | Revenue flat. Gross margin up significantly. Adjusted EBITDA +11%. Adjusted PBT +12% (£48.5m). “The Group has made a good start to FY 2026 and has an exciting pipeline of at least 15 new games and apps expected to launch during the year… expects the Group to achieve FY 2026 results in line with current market expectations.” | ||

Foresight Solar Fund (LON:FSFL) (£332m | SR54) | NAV per share 99.2p (Dec 2024: 112.3p). 8.1p dividend declared. “Foresight Solar has delivered solid operational performance and continued to progress its strategic objectives, despite not being immune to the regulatory challenges and persistent discounts that have impacted the sector.” | ||

PZ Cussons (LON:PZC) (£314m | SR75) | 6.3% LfL revenue growth in Q3. The Group now expects to report adjusted operating profit towards the upper end of the previously updated £53-57 million guidance range. | ||

Octopus Renewables Infrastructure Trust (LON:ORIT) (£305m | SR63) | NAV per share 93.8p (Dec 2024: 102.6p). Dividends declared 61.1p. "The year under review was characterised by disciplined capital allocation and active portfolio management in a challenging operating environment.” | ||

Public Policy Holding (LON:PPHC) (£275m | SR38) | Q4: organic growth 5.4%, total growth 27.8%. FY2025: organic growth 6.2%, total growth 24.7%. GAAP net loss $39m (2024: net loss £24m). Adjusted EBITDA +17.7% ($45.4m). “Our balance sheet flexibility allows us to pursue earnings-accretive acquisitions while our strong cashflow allows us to continue investing in organic growth initiatives. Momentum from Q4 has set us up well for a good start to 2026.” | ||

Henry Boot (LON:BOOT) (£234m | SR87) | BOOT’s share of land and property sales £193m (2024: £224m). Revenues marginally lower. PBT “broadly in line with market expectations” at £29.1m (2024: £30.7m). Assuming the impact from the conflict in the Middle East is not prolonged, the business is well positioned to deliver the recently revised market expectations for FY26 and with a continued belief that we will deliver against our medium term growth and return targets. | ||

Niox (LON:NIOX) (£227m | SR38) | Revenue growth 17% (15% at constant currencies). Adjusted EBITDA +21%. PBT £11.2m (2024: £7.8m). Trading in 2026 financial year has started well. | ||

YouGov (LON:YOU) (£205m | SR66) | Revenue +2%, adjusted operating profit down 20% (£24m). Actual operating profit +14% (£16.8m). Given dislocation between our confidence in YouGov's intrinsic value and the current market valuation, the Board expects to launch a share buyback programme in place of the annual dividend. Expects to deliver adjusted operating profit of £52-56 million for FY26, after investing £6m in Shopper division. | BLACK (AMBER/RED ↓) (Graham) It’s not yet in obvious bargain territory, but if you’re optimistic about adjusted operating profit hitting £70m in a couple of years, then it’s potentially interesting. I’m downgrading this to AMBER/RED in the short-term, to be consistent with our policy on profit warnings. However, in terms of the long-term value on offer, YouGov has never interested me before. I am now interested, and will be keeping a close eye on where it goes from here. | |

Regional REIT (LON:RGL) (£150m | SR68) | LfL valuation down 5% year-on-year. EPRA net tangible assets £315.2m (2024: £340.8m). “...the leasing market remains subdued, with some tenants taking longer to make decisions, and often choosing not to move at all… in this context, the Board feels it is right to act with increased prudence, targeting an 8p dividend per share for 2026.” | ||

S4 Capital (LON:SFOR) (£137m | SR72) | Full year results in line with revised guidance. Net revenue down 8.4% like-for-like. Adjusted operating profit -5.5% (£74m). Operating profit £2.7m. “2026 like-for-like net revenue is expected to be in line with current analyst consensus, slightly below 2025, with operational EBITDA margin targeted to increase by at least 100 basis points, primarily due to the annualised impact of the 2025 cost actions.” | ||

Jubilee Metals (LON:JLP) (£109m | SR25) | The Phase 1 drilling results at the Molefe copper mine, scheduled for 24 March 2026, have been delayed pending formal sign-off from the Competent Person as required under the AIM rules. | ||

EKF Diagnostics Holdings (LON:EKF) (£106m | SR78) | Revenues £51.6m (2024: £50.2m). Adjusted EBITDA +9.3% (£12.4m). PBT £7.1m (2024: £6.3m). The 2025 results establish a strong foundation for the Five-Year Strategic Development plan, providing EKF a positive base from which to push further into new markets with a simplified product offering and greater commercial focus on the areas of strategic importance. | ||

Roadside Real Estate (LON:ROAD) (£103m | SR25) | “While integration of… recent acquisitions is in the early stages, we are working in close partnership with the incumbent teams to optimise fuel sales and drive operational efficiencies. The fragmented UK energy forecourt market presents a compelling opportunity to build a resilient, income-generative portfolio of desirable freehold assets.” | ||

Personal group (LON:PGH) (£95m | SR72) | Revenue +11% and adjusted EBITDA ahead of expectations, up 22% to £12.1m. Entered 2026 with strong momentum. | AMBER/GREEN = (Roland - I hold) Today’s results are strong and comfortably ahead of earnings expectations for 2025. The company’s house broker has not chosen to carry this upgrade through to FY26, but I think the valuation and growth potential here remain broadly attractive. In my review below I cover today’s results in more detail and include some notes from my call with Personal’s management team this morning. | |

Wynnstay (LON:WYN) (£83m | SR96) | Group trading over the first four months of the financial year has been in line with the Board's expectations and is ahead of the same period last year. “While there remains a risk of cost inflation, including fuel and other inputs, arising from ongoing geopolitical uncertainty, the Board does not currently expect a material adverse impact on the Group and maintains its full year expectations.” | ||

Xaar (LON:XAR) (£81m | SR45) | Revenue up 12% at constant currency. Adjusted PBT from continuing operations £0.8m (2024: loss £1m). “Early trading in 2026 is in line with expectations. The order book is healthy for this time of year, and the Board believes the Group is well positioned for further progress - both in 2026 and in the longer term.” | ||

Zephyr Energy (LON:ZPHR) (£71m | SR26) | Significant increase in hydrocarbon production from the Company's non-operated asset portfolio during Q4 (vs. Q2 and Q3). Continued progress towards delivering first commercial production from the Paradox project. Two divestments of non-core, non-producing assets obtained with the Acquisition announced in August 2025. | ||

Journeo (LON:JNEO) (£67m | SR72) | Revenue +11% (£55m). Adjusted PBT +13% (£5.7m). Cash £12m. “Across the operating businesses, we have strong orderbooks and a growing pipeline of sales opportunities which gives the Board confidence that Journeo will continue to deliver growth and increasing value for all stakeholders.” | ||

Michelmersh Brick Holdings (LON:MBH) (£67m | SR59) | Revenue down 1.7%, pre-tax profit down 46.3% to £4.3m. Adj EPS down 8.3% to 7.5p, dividend held at 4.6p. Low single digit increase in UK brick despatch volumes, “challenging markets in Europe”. Outlook: order intake running ahead of manufacturing, but “confidence and predictability [...] have been diluted over the last 12 months”. Confident the company can deliver growth in 2026 “relative to 2025”. | ||

Corero Network Security (LON:CNS) (£59m | SR25) | Revenue up 3.7% to $25.5m, ARR up 23% to $23.9m. Adj EBITDA down 33% to $2.0 due to higher operating expenses. “Strong new business pipeline for FY 2026”. Outlook: Q1 2026 has “started strongly”, confident in prospects of further growth. | ||

Real Estate Investors (LON:RLE) (£52m | SR61) | Revenue down 13%, EPRA EPS down 10.5% to 1.7p. EPRA net tangible assets down 4.3% to 49.1p per share. Completed £8m of disposals at 95.9% of Dec 2024 valuations. LTV reduced to 24.8%. Occupancy currently at 78% with contracted rental income of £8.2m p.a. | ||

TMT Investments (LON:TMT) (£49m | SR66) | NAVps up 8.9% to $7.13, total NAV of $220.8m. Benefited from revaluations of seven investee companies including Bolt and Scale AI. Completed a number of partial sales “at NAV-enhancing valuation levels”. | ||

Staffline (LON:STAF) (£49m | SR97) | Revenue up 11.5%, aided by “a significant new strategic partnership with a leading logistics provider”. Gross profit up 10.6% to £78.3m. Adj pre-tax profit up 48% to £7.4m. Outlook: “healthy new business pipeline underpinned by organic growth and market share gains”. Expects 2026 trading to remain in line with expectations. | ||

Time Finance (LON:TIME) (£41m | SR80) | Own-book lending up 27% to £86.5m. Revenue up 4%, pre-tax profit up 5% to £6.2m. Pre-tax margin improved by 1% to 22%. Outlook: expect full-year results to be in line with market guidance. | ||

Ultimate Products (LON:ULTP) (£39m | SR90) | Revenue down 6%, adj pre-tax profit down 40% to £3.1m. “Subdued consumer demand for general merchandise and a deliberate reduction in third-party clearance sales”. International branded sales up 19%, driven by EU discounters. Outlook: expects H1 trends to continue through the year, with full-year profitability in line with consensus. | ||

Flowtech Fluidpower (LON:FLO) (£37m | SR24) | Revenue up 9%, adj operating profit up 33% to £3.6m. Net debt stable at £15.2m. 2026 outlook: current trading is in line with expectations, with good momentum in order book. | ||

Gattaca (LON:GATC) (£33m | SR99) | Revenue up 10%, adjusted pre-tax profit up 187% to £3.0m. Adj EPS 6.9p, net cash £13m. Outlook: macroeconomic headwinds affecting client demand and candidate sentiment. FY26 guidance for adj pre-tax profit of £4.5m is unchanged. | ||

Getbusy (LON:GETB) (£29m | SR23) | Revenue up 3%, ARR up 5% to £22.6m. Adj EBITDA down 78% to £323k, pre-tax loss of £1.1m. Outlook: SmartVault ARR growth expected to strengthen in 2026 with improved EBITDA margin. | ||

Hardide (LON:HDD) (£25m | SR51) | Expect H1 revenue to be up by 50% at c.£4.5m, with adj EBITDA of £1.3m (H1 26: £0.4m). Outlook: “well positioned to deliver” on recently upgraded full-year expectations. | ||

Prospex Energy (LON:PXEN) (£17m | SR22) | A subsidiary has been offered the San and Dunajec onshore licence areas in Poland. | ||

Mission (LON:TMG) (£16m | SR64) | Revenue from continuing operations down 8%, adjusted pre-tax profit down 39% to £3.0m. Adj EPS down 46% to 2.0p. Leverage increased to 2.8x EBITDA. Targeting £4m of additional cost savings. 2026: trading so far this year has been in line with expectations. | ||

Itaconix (LON:ITX) (£15m | SR27) | Revenue up 61% to $10.5m, gross profit up 61% to $3.6m, adj EBITDA loss reduced to $600k. Cash of $4.4m at year end. Outlook: “strong order momentum and a growing pipeline of projects”. 2026 expectations are unchanged (revenue: $13.3m, adj EBITDA $0.3m). |

Graham's Section

YouGov (LON:YOU)

Down 11% at 154.6p (£181m) - Results for the six months to 31 January 2026 - Graham - AMBER/RED ↓

YouGov, the international research and data analytics group, announces its results for the six months ended on 31 January 2026.

We’ve been cautious about this stock for years, with the most recent example of this being Mark’s comments last month.

Unfortunately, caution has been rewarded with a deeply sinking stock price.

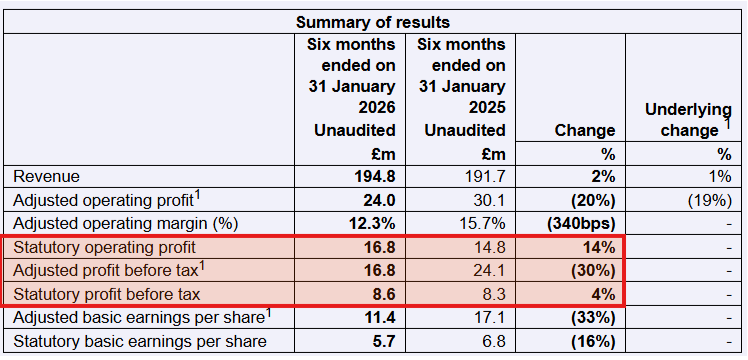

Here is today’s H1 results table:

The headline is “Revenue growth of 2%; statutory operating profit growth of 14%”.

There are many different measures of profitability to choose from.

I tend to favour the simplicity of statutory PBT, as I’ve never been very comfortable with the adjustments used by YouGov.

Let’s note again the big gap between adjusted PBT (£16.8m) vs. actual or statutory PBT (£8.6m)

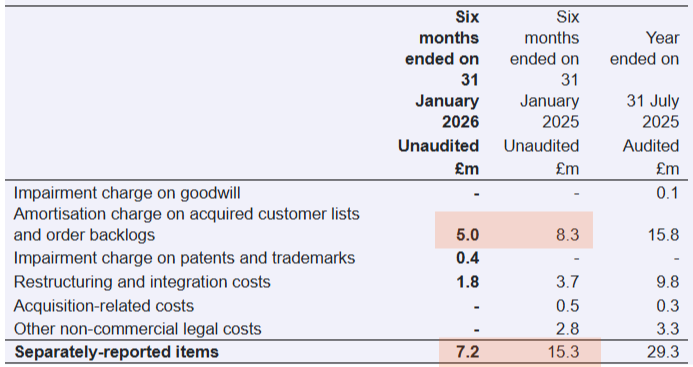

Checking the footnotes, which you have to do with this share, I find that the company capitalised £9.5m of spending on its intangible assets in H1, while writing down - or amortising - £15.4m of them. A chunk of the amortisation now relates to assets it acquired in 2024.

Overall, therefore, the treatment of intangibles has turned into a pretty serious drag on official profitability.

The company attempts to get around this problem by adjusting some of it out.

From footnote 4, here are the adjustments:

You can see that in H1 this year, the adjustments or “separately-reported items” are much lower than they were last year.

That’s a good thing - fewer adjustments means cleaner results. But it doesn’t change the fact that underlying profitability isn’t really going anywhere.

Cash flow can help us understand what’s going on:

H1 this year: £37.1m of cash generated from operations (before tax and before changes in working capital, which were heavily negative for cash flow).

H1 this year: £9.2mm spent on investing activities, and another £3m spent on leases elsewhere in the cash flow statement.

These cash flow numbers might be the best argument for using some of the company’s preferred measures of profitability. Based on the above, I think the pre-tax cash inflow in H1 was in the region of £25m. This lines up well with an adjusted operating profit figure of £24m.

The same calculation for H1 of the prior year gives a cash inflow of nearly £27m, or £30m if we exclude an acquisition. That perfectly matches the adjusted operating profit for the period of £30m.

I’m sorry for getting so technical here, but I thought it was necessary.

The point is that I’m now willing to consider using adjusted operating profit here.

Balance sheet: net assets are £186.5m, but this includes vast amounts of goodwill and other intangibles. Take them out and you’re left with negative equity of c. £230m.

That negative equity is real, not imaginary: there is net debt of £160m, leaving a pretty substantial leverage ratio of 2.1x.

That debt is what remains after YouGov spent €315m buying GfK’s Consumer Panel Business in 2024, now renamed as YouGov Shopper.

This business appears to be causing a few headaches. From today’s commentary:

Shopper revenues increased 3% in reported terms, and was 2% lower on an underlying basis. The decline was due to the early client deliveries towards the end of FY25. Expected to return to growth by year end with order backlog ahead of last year.

The Shopper division's adjusted operating profit of £6.8m (HY25: £13.9m) was impacted by the additional investments to drive future growth and maintain competitiveness. The incremental impact of these investments in FY26 is expected to be £6 million.

Today’s profit warning relates to this issue:

Taking into account the £6 million of incremental investment in Shopper, the Group expects to deliver adjusted operating profit of £52-56 million for FY26.

I think that operating profit for FY26 was supposed to be closer to £60m, so the additional £6m spend on Shopper appears to be coming straight out of that figure.

CEO comment:

We delivered a resilient first half performance, with continued growth in our core US and UK markets and good momentum in our Research division. While the macroeconomic backdrop remains uncertain, clients continue to prioritise high-quality human data and strategic research projects, areas where YouGov continues to be strongly positioned.

During the period we have increased the level of targeted investments in both Shopper and our AI-enabled products, which we believe will reposition our platform as the industry-leading pioneer in the age of AI, enhance the value of our data, improve the client experience and drive operational efficiencies over time. A meaningful proportion of this investment has been directed towards Shopper to enhance its competitive positioning in the market.

Graham’s view

I didn’t expect to say this, but I think that YouGov shares might be starting to offer some value here.

We’ve been talking negatively about this one for a long time, and the market has been agreeing with us:

But let’s suppose, controversially, that the adjusted operating profit figure is not a bad approximation of pre-tax cash flow. That’s at least £52m of cash coming into the business, pre-tax, during a year of heavy investment.

The GfK acquisition doesn’t seem to have worked out as planned, which is not a surprise, but it’s in the past. What matters is what happens next, with the share price at a fraction of its former levels:

Market cap £181m

Net debt £160m

Enterprise value c. £340m

Applying 25% tax to the adjusted operating profit figure leaves, in theory gives at least £39m of after-tax cash flow, vs. £340m enterprise value.

Ok, it’s not yet in obvious bargain territory - but if you’re optimistic about adjusted operating profit hitting £70m in a couple of years, then it’s potentially interesting.

The company itself obviously thinks its undervalued:

Given dislocation between our confidence in YouGov's intrinsic value and the current market valuation, the Board expects to launch a share buyback programme in place of the annual dividend.

I’m downgrading this to AMBER/RED in the short-term, to be consistent with our policy on profit warnings.

However, in terms of the long-term value on offer, YouGov has never interested me before. I am now interested, and will be keeping a close eye on where it goes from here.

Chesnara (LON:CSN)

Down 2% at 292.8p (£675m) - Final Results - Graham - AMBER/GREEN =

This life insurance consolidator is never going to be exciting in the same way as other shares can be, but it’s been a steady performer. The dividend stream has been enormous (about 20p annually), while the share price itself has held up reasonably well:

With the share price increasing last year, it joined the FTSE 250 in August.

Let’s see if I can make sense of the headlines in today’s full year results from the company.

Overview:

Chesnara reports its 2025 full year results, demonstrating a period of transformational strategic delivery with two major acquisitions announced over the past 12 months. Performance was underpinned by disciplined operational delivery alongside the impact of exceptional capital markets activity undertaken during the year, with significant year‑on‑year growth across our key performance indicators.

Selected highlights:

Operating cash generation £94m (2024: £79m)

Adjusted operating profit £56m (up 42%)

Assets under administration £15bn (up 10%)

As we mentioned here last July, Chesnara spent £260m buying HSBC Life (UK), priced at a discount to that business’s “own funds”. That deal completed in January 2026, “marking Chesnara's largest transaction and substantially increasing the scale of the Group.”

£140m of fresh equity was raised, and a £150m deeply subordinated bond was issued.

More recently, Chesnara announced the acquisition of Scottish Widows Europe SA.

Final dividend: raised 6% to 14.8p. Total dividend for 2025 of 22.5p, up from about 21.5p for the prior year.

CEO comment:

"The Group has delivered strong financial results alongside two material deals, the acquisition of HSBC Life (UK) Ltd which completed in January 2026 and the proposed acquisition of Scottish Widows Europe SA. These deals are expected to significantly increase the Group's scale and longer-term Operating Capital Generation potential. And we continue to see further opportunities to grow, with a positive M&A pipeline and a great track record of disciplined execution."

Reading through the commentary, this stands out:

The estimated pro-forma position of the Group post these acquisitions is over £1bn of Own Funds, which represents a near doubling over the last 5 years, post the payment of c£160m of dividends over the same period and includes capital raised of £490m.

Buying Scottish Widows Europe will cost €110m (£95m), but they expect it to generate €100m in the first five years and €250m over its lifetime. It’s expected to complete around the end of 2026.

Outlook:

Looking into 2026 and beyond, we continue to see a very healthy pipeline of acquisition opportunities and remain positive about the outlook for further M&A. Our disciplined approach and strong capital position mean we are well placed to execute value-accretive transactions. 2025 was a transformative one for the Group and a year where our people have done a terrific job delivering across our key strategic initiatives. Going forward, we have increased confidence we can materially grow the group and deliver further value for our investors.

Adjustments

PBT is only £19m, and in fact is negative £7m after making a tax adjustment that sounds quite important to me (removing “Tax attributable to policyholders' returns”).

Here are the costs that get adjusted out, to bring a negative £7m PBT up to a £56m adjusted operating profit:

“Investment variances and economic assumption changes” (£6m)

“Impairment and amortisation and profit or loss on disposal” (£6m)

“Integration and restructuring costs” (£40m)

Financing costs £11m

Graham’s view

Though the market cap is less than £1 billion, I classify this as a complex financial stock, the same as I do with the High Street banks and very large insurers.

What this means practically is that I accept I’m never going to have a very strong conviction in it - it’s simply too complicated to analyse for someone like me who is also studying lots of other companies.

But I do like the story. I admire the track record. The acquisitions are both impressive and promising.

I might even be willing to look past the heavy adjustments to PBT and operating profit, which I don’t often do.

So in conclusion, I’m leaving this on AMBER/GREEN.

The StockRanks are cool on it, calling it a Turnaround. The statutory profit results in the last few years haven’t been good enough for it to do any better than this:

Roland's Section

Bytes Technology (LON:BYIT)

Down 14% at 257p (£607m) - Full Year Trading Update - Roland - BLACK (AMBER/RED =)

Unfortunately today’s full-year update from this IT value-added reseller appears to be the latest in a series of creeping downgrades over the last 18 months:

While FY26 results are expected to be in line with October’s revised (downgraded) guidance, FY27 operating profit is now expected to be “broadly flat” (i.e. probably slightly below) as the business absorbs higher costs. My impression is that operating profit was previously expected to rise in FY27.

FY26 trading update

Today’s update summarises FY26 financial results and provides some additional detail on the headwinds faced during the year and the outlook for the current year (Bytes has a 28 Feb year end).

FY26: “double-digit gross invoiced income growth”.

FY26 gross profit up 2.3% to c.£167m (FY25: £163.3m).

FY26 operating profit down 6.6% to c.£62m (FY25: £66.4m).

FY26 cash conversion “exceeded 100%” with a year-end cash balance “over £98m” (FY25: £113m).

Last year’s results were affected by the impact of changes to the incentives offered to Microsoft’s enterprise sales partners (such as Bytes), which led to softer results from public sector clients. Changes to Bytes sales structure for private sector customers are also said to have resulted in “phasing effects”.

H1 gross profit was flat year-on-year at £82.4m, telling us that H2 gross profit improved to c.£84.6m. Today’s commentary suggests that this improvement came late in the day, with gross profit up by c.6% in January and February versus the prior year.

Higher operating costs were also a headwind – the increase in gross profit last year translated into a fall in operating profit due to the impact of higher costs. I discussed this in more detail when I reviewed October’s half-year results.

Outlook

Unfortunately today’s FY27 guidance suggests the same dynamic will continue to hold back profits this year:

FY27: “expect high single-digit to low double-digit percentage growth in gross profit”

FY27: “operating profit broadly flat”

The company provides a list of factors that are expected to lead to higher operating costs this year, outweighing expected gross profit growth:

“c.£4.5m of cost normalisation” reflecting higher technology costs following completion of strategic projects.

A return to normal bonus levels.

Continued headcount investment for growth.

We don’t have access to any updated broker forecasts today and Bytes does not include details of consensus forecasts on its website or in its RNS releases.

However, consensus forecasts on Stockopedia prior to today suggest a c.4% increase in adjusted earnings for FY27, so I think it’s reasonable to assume that operating profit was also expected to rise this year.

Having said that, even if I’m right and this is a profit warning, it doesn’t seem like a major downgrade to me.

Assuming a c.5% reduction to EPS forecasts, Bytes shares could now be trading on 12x forecast earnings. If the company’s record of special dividends is maintained then this could support an attractive c.7% dividend yield.

Roland’s view

I’m relieved to see I’ve been AMBER/RED on this business for a while due to last year’s profit warnings and the somewhat vague guidance provided in September and October. Bytes shares have continued to drift lower since then and the sell-off has been extended today:

Having said that, I don’t think there is anything fundamentally wrong with this business.

Profitability also remains exceptional:

This is a capital-light business, thanks to the extensive supplier credit enjoyed by large resellers in this sector.

In FY25, Bytes generated a net profit of £55m from balance sheet equity of just £98m – but it also carried year-end payables of £327.5m on its balance sheet.

While this model can work very well for shareholders, any unexpected slowdown in order intake can result in cash outflows as the company has to meet payables without a corresponding inflow of cash from new(er) customer orders. I believe this is why all three UK-listed companies in this sector tend to maintain significant net cash balances.

Bytes’s valuation is now lower than at any time since the company’s 2020 IPO:

I am going to leave my AMBER/RED view unchanged today to reflect our policy towards profit warnings and downgrades.

However, if the company can return to delivering in-line trading results over the coming year, I think the valuation has probably reached a level that could be quite attractive on a medium-term view. I plan to continue watching Bytes with interest.

Personal group (LON:PGH)

Up 10% at 333p (£104m) - Preliminary FY25 Results - Roland - AMBER/GREEN =

(At the time of publication, Roland has a long position in PGH.)

Personal Group Holdings Plc (AIM: PGH), the workforce benefits and insurance provider, is pleased to announce its preliminary results for the year ended 31 December 2025 ("FY25").

This niche insurance provider is a holding in the SIF folio and my personal holdings, so I was pleased to have a chance to chat to CEO Paula Constant and CFO Sarah Mace this morning following the publication of today’s full-year results. My thanks to both for taking the time to talk with me.

In this review I’ll summarise last year’s results and then include some extra detail on the business from my conversation with management.

FY25 results

These are a strong set of figures from Personal Group, with earnings coming in comfortably ahead of expectations:

Revenue up 11% to £48.4m

Annualised recurring revenue (ARR) up 12% to £48.6m – over 90% of 2025 reported revenue was recurring

Adjusted EBITDA up 22% to £12.1m (market consensus: £11.6m)

Pre-tax profit up 23% to £8.4m

Earnings per share up 32% to 23.3p (market consensus: 20.1p)

Total dividend up 41% to 23.3p, in line with 100% new payout policy.

Net cash up 5.8% to £29.0m

Tax boost: the EPS beat seems particularly impressive but appears to have been aided by a £0.4m R&D tax credit, which I estimate added 1.3p per share to earnings. Stripping this out gives an underlying EPS figure of 22p and a growth rate of 24%, which is more in line with the increase in pre-tax profit.

Despite this year’s move to a 100% dividend payout ratio, it’s clear the business remains highly cash generative. Personal Group says its regulatory capital requirement (for insurance) is around £6m. The company’s policy is to maintain a buffer of around twice this amount, so £12m currently.

This left a further £17m at the end of 2025 that was surplus to requirements. There is no debt.

Given this performance I don’t have any near-term concerns about the safety of the dividend, which currently offers a near-7% yield.

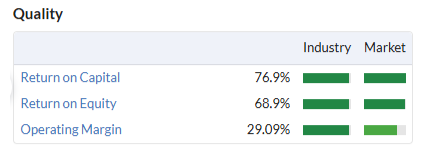

Profitability also remained excellent last year – my sums suggest an operating margin of 17.6% and return on equity of 19.8% – both in line with past performance:

Trading summary: growth was delivered across the business last year.

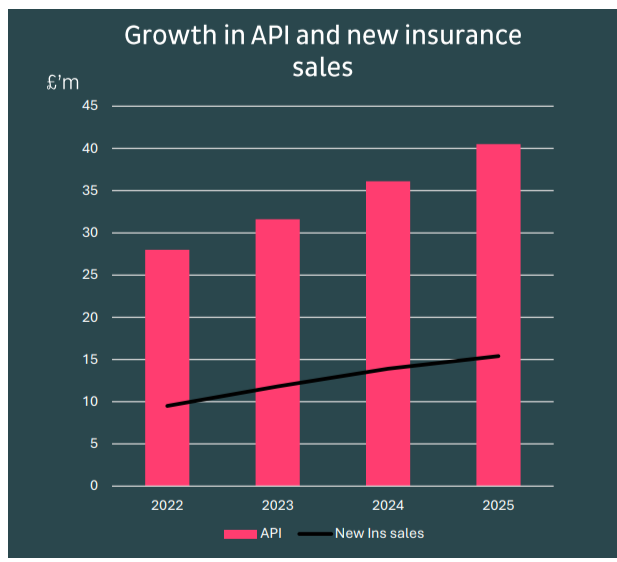

Insurance: this division provides a range of simple products aimed at supplementing sick pay, primarily for blue collar workers in sectors such as transport and logistics. I’ve previously discussed the business model in more detail here.

This insurance is sold by face-to-face teams who typically achieve high levels of conversion. Personal Group is also in the early stages of rolling out a digital insurance product to expand its addressable market.

2025 performance was good, with double-digit sales growth achieved from a 4% increase in field sales days:

Insurance revenue up 12% to £36.2m

Annualised premium income up 12% to £40.5m

Adjusted EBITDA up 18% to £14.6m

This extended a strong run of growth in recent years:

Retention of existing policyholders remained high at over 80%, while improved field team performance helped to increase the overall penetration rate among addressable employees to 14.5% (2024: 13.0%).

New client wins added a further 50,000 employees to the company’s addressable market for insurance last year – I’m told this equates to around 20 new clients, giving an average of c.2.5k employees per client. Some of Personal Group’s longstanding clients are far larger, though – Royal Mail is a longstanding example (<100k employees).

The group’s total addressable market of employees is said to be c.1.25m people.

Profitability is excellent with an EBITDA margin of 40.3% (2024: 38.6%) and a claims ratio of 27.1% (2024: 29.1%). However, this latter figure doesn’t tell the whole story, due to high distribution costs from face-to-face sales. I’ll discuss this further shortly.

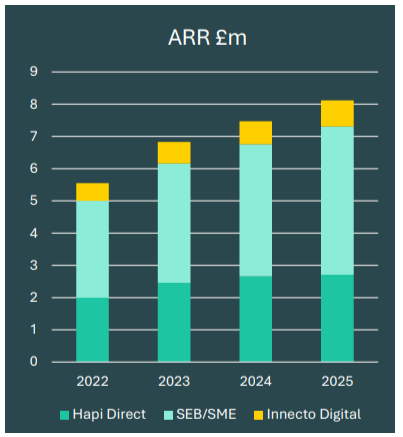

Benefits & Rewards: this business provides the Hapi employee benefits platform and also powers the Sage Employee Benefits service (disc: I hold SGE). This provides benefits for employees such as retail discounts, wellbeing services and Cycle to Work offerings. For example, last year employees gained £2.2m of discount vouchers on £53m of spend.

The group also operates Innecto Digital, a Pay & Reward consulting service aimed at HR departments. Profitability in both of these units improved last year:

Benefits platform revenue up 5% to £8.1m

Benefits adj EBITDA up 19% to £5.1m

Pay & Reward revenue up 10% to £2.8m

Pay & Reward adj EBITDA up 19% to £1.0m

A good track record here, too:

2030 & Growth: the company launched a five-year growth plan last year with some clear targets:

>£100m revenue

£30m EBITDA

Access 300k new insurance employees

Double Benefits & Reward client base and add 10 additional partnerships

Today’s 2025 results appear to be mostly on track to meet these ambitions:

2025 revenue growth: 11% (2025-30 CAGR: 15%)

2025 EBITDA growth: 22% (2025-30 CAGR: 20%)

2025 insurance: access to 50k new employees (2025-30 CAGR: 60k)

Management hopes to see new client wins provide greater access to new employees this year, to bring growth in this key metric back onto track.

The company is also targeting “1-2 significant new partnerships” for the Benefits & Reward business in 2026, with efforts led by a recently recruited Partnerships Director.

Outlook & Updated Estimates

Personal Group’s house broker Canaccord Genuity has published updated forecasts on Research Tree today. Our thanks for making these available more widely.

Slightly to my surprise, Canaccord’s 2026 forecasts have reduced slightly today:

FY26E revenue: £54.4m (unch)

FY26E adj EBITDA: £14.1m (previously £13.9m)

FY26E adj pre-tax profit: £10.2m (previously £10.3m)

FY26E adj EPS: 24.3p (previously 24.9p)

FY26E dividend: 24.3p (previously 25.5p)

These forecasts imply revenue growth of 12.4% and EBITDA growth of 16.5% in 2026.

Stripping out the R&D tax credit from 2025 EPS suggests underlying FY26E EPS growth of 10.5%.

According to the broker, the small reduction to pre-tax profit and EPS forecasts today is due to higher depreciation and amortisation charges after recent software investment.

Canaccord has also introduced FY27 forecasts suggesting growth of 12%/15%/19%/19% across revenue/EBITDA/PBT/EPS.

One takeaway from this is that forecasts for both 2026 and 2027 are slightly below the growth rates implied by the company’s 2030 targets. However, it’s still early in the year – 2025 forecasts were upgraded twice last year – before coming in ahead again today.

Using Canaccord’s latest forecasts as a guide, Personal Group shares trade on a forward P/E of 14 and dividend yield of 7.4%.

Management Q&A

Here is a summary of the main points I discussed with the CEO and CFO on my call this morning. These are taken from my notes so are not verbatim and may contain errors.

Q: Digital insurance offer – can you share any insight on progress to date and the expected scale/profitability of this business?

A: Invested in development of this service last year and is now piloting with a number of clients. The offering includes three digital variants of the company’s core insurance products, offering slightly less cover than would be provided in face-to-face sales.

Very happy with progress, people are buying and sales have probably exceeded early expectations, with some people purchasing multiple products for themselves and family.

Initially nervous about offering digital insurance to clients where face-to-face (F2F) sales also take place, but has now put digital insurance into Royal Mail (a major F2F client) and is able to reach employees (e.g. white collar) that can’t be reached with F2F.

The addressable market is expected to be 1%-2% of the group’s overall addressable market, but this could still make a useful contribution to the group’s ambition of generating 10% of EBITDA from new businesses by 2030.

No clear detail on expected profitability yet versus the core insurance product, but is expected to be profitable in its own right. Very different cost base to F2F sales.

Q: Client concentration risk – the 2024 annual report mentions the risk of losing clients that generate more than 20% of revenue. Do you have any clients who fall into this category?

A: On the Benefits side, around 60% of revenue comes through the Sage partnership, so this carries a certain concentration risk.

Working to diversify concentration risk by winning new clients. 50,000 new addressable employees for insurance sales were added in 2025, equating to around 20 clients (2.5k/client).

The group’s core strength is in transport (e.g. bus depots) and logistics, but healthcare, food production and retail are also important. Sees plenty of opportunity for further client wins within core addressable markets.

Recently added care home operator Avery (10k employees) and is seeing initial signups ahead of the normal run rate. Care homes are said to generate 60%-70% of the value per employee that Personal Group gets from bus depots, so aren’t so profitable but are an important market.

Q: Have the FCA Consumer Duty rules introduced in recent years led you to make any changes to the way you operate?

A: Yes. When Consumer Duty was introduced, we decided to embrace it “like a big company”.

One area of change is the claims ratio – this was historically around 25%, but the company is now pricing deliberately to try and move this into the high 20s/30%. The reason for this is to address potential concerns over FCA Fair Value requirements.

[RH: My understanding of Fair Value is that claims payouts should account for a sufficient share of insurance premium income to demonstrate customers are receiving good value for money.]

Personal Group’s claims ratio is low compared to most insurers, with a far higher component of distribution costs due to the face-to-face sales strategy. However, the company’s view is that its offering is still well-aligned with Consumer Duty rules because it helps to reduce the “protection gap” – offering insurance cover to people who might not otherwise be able to access it.

The CFO made the point that while the company’s claims ratio is low, high distribution costs mean its combined operating ratio (which indicates overall underwriting profitability) is more typical of other insurers.

[RH: I have previously estimated the combined ratio at 75%-80% and I believe this is a fair estimate for the 2025 results]

Distribution expenses totalled around £7m last year, according to my notes. That equates to around 20% of insurance revenue and is below claims payout levels.

Roland’s view

I think there are a few points worth flagging up from today’s results and updated forecasts.

First of all, current and expected growth rates appear slightly below the level needed to hit the group’s 2030 targets. However, my feeling is that some of the growth initiatives that are underway may well deliver back-end loaded performance, so the targets still seem credible to me based on current performance.

The Sage Employee Benefits partnership represents 60% of Benefits revenue, so carries some concentration risk.

However, Personal Group signed a new contract with Sage last year expanding the partnership, which has been running since 2017. Presumably Sage is happy with the service and with Personal Group. It’s also worth remembering the Benefits business only accounts for around one-third of group profits.

Finally, Personal Group appears to have thought carefully about regulatory risks and acted pre-emptively to try and manage these.

While my view is that niche financials will always carry some regulatory risk – and we’ve seen plenty of examples in recent years – my overall view of this business remains positive.

If the company can maintain its current growth rate for the next few years, I think it’s fair to suggest the stock could deserve a significantly higher valuation by 2030.

I’ve been AMBER/GREEN on Personal Group for some time now. I am tempted to upgrade to be fully positive, but to reflect today’s nuanced update to FY26 forecasts I’ve decided to leave my AMBER/GREEN view unchanged for now.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.