Good morning!

There are few major overnight moves to report.

Brent crude is a little lower at $113.50.

UK natural gas futures are up 7% to 119p (the pre-war price was 75p).

The FTSE is set to open at c. 10,270.

In company news, I enjoyed watching interviews with Warren Buffett and Greg Abel over the weekend (disclosure: I'm long Berkshire Hathaway (NYQ:BRK.B)). Berkshire Hathaway's Annual Shareholder Meeting was on Saturday.

Buffett is still sharp at 95, and Greg Abel seems to inspire a lot of confidence. But they always say that you should watch what an investor does, more than you listen to what they say. Berkshire Hathaway, with a market cap of $1 trillion, holds record cash reserves of $380 billion. If, like me, you think the US is still overheated, this should help to confirm your prior belief! Others will view this as an unacceptable degree of cash drag. I would point out that there are plenty of other funds and vehicles to choose from if you don't want any cash drag!

That's all for today, see you tomorrow! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| HSBC Holdings (LON:HSBA) (£234bn | SR70) | Earnings Release 1Q26 | Pre-tax profit down $0.1bn to $9.4bn due to higher expected credit losses (notably a $400m loss on a UK fraud case) and higher operating expenses. RoTE was 17.3%, versus 17.9% in 1Q25. Outlook: all financial targets are unchanged. | AMBER (Roland) These quarterly earnings have missed expectations slightly, but I don’t see anything seriously amiss here and am confident this global bank will remain able to navigate the difficult current market conditions. Taking a high-level look at valuation, my feeling is that the current share price is probably within the ballpark of fair value, so I’ve adopted a neutral view. |

Vodafone (LON:VOD) (£27bn | SR93) | Vodafone will pay £4.3bn to buyout CK Hutchison’s 49% share of VodafoneThree to become the sole owner of “the UK’s largest mobile operator and one of the fastest growing broadband providers”. Deal values VodafoneThree at 7.6x FY27E EBITDAaL. | ||

| Intertek (LON:ITRK) (£7.4bn | SR53) | Response to possible offer announcement by EQT | Intertek confirms that on 5 May 26 it received a further cash offer of £58.00 per share from bidder EQT – a 54% premium to the undisturbed closing price of £37.70 on 9/4. This offer is being reviewed by the Board and follows previous offers of £51.50 and £54.00, which were rejected. | |

Plus500 (LON:PLUS) (£3.2bn | SR87) | SP +2% Entered FY26 with “strong momentum”. Q1 ahead of expectations, the Board remains confident in the outlook for FY26. Cavendish forecasts (issued in April): 2026 revenue $823.9m, adj. EPS 401.4 cents. 2027 revenue $802.4m, adj. EPS 419.4 cents. Cavendish has a “Hold” rating on the stock. | GREEN = (Graham) [no section below] It’s a brief update from this international trading platform that has generated an 8,000% return for shareholders since IPO. It raised expectations last month at the Q1 update, and today’s AGM statement effectively reiterates the outlook given then. I have no reason to change my stance, which is based on the company’s legendary cash generation and its vastly improved geographical/product diversification. The quality of its customer base has also improved significantly over time. I’ve learned not to fight the tape with this High Flyer. | |

Kosmos Energy (LON:KOS) (£1.43bn | SR33) | Net production c.74.8k boepd, +25% vs Q1 2025. Revenue of $371m or $55.81 per boe. Q1 adjusted net loss of $36m or $0.07 per share. | ||

AEP Plantations (LON:AEP) (£684m | SR99) | Paying c.$162m to acquire 98.3% shareholding of Pinago, which has 15,400 hectares of palm oil plantation and 3,500 hectares of planted rubber. In 2025, Pinago harvested 161kt of FFB and produced 105,000t of CPO. Pinago generated a net profit of c.$18m in 2025, giving a 9x P/E multiple for the acquisition. Cavendish updated broker estimates: - FY26E adj EPS: 293c (prev. 217.8c) - FY27E adj EPS: 271.5c (prev. 182.9c) | GREEN = (Roland) [no section below] This acquisition looks sensible and reasonably valued to me, with the caveat that there is a high dependency on commodity prices to drive AEP’s profitability. My (limited) understanding is that an average tree age of 12 years means the plantation should now enjoy a period of highly productive maturity, before any major replanting requirements arise. This morning’s upgrade from broker Cavendish leave AEP shares on a forward P/E of 9 with substantial net cash and support the view that this deal should be value accretive for shareholders. Given that this is the second upgrade to FY26 forecasts in two months, I am going to leave Graham’s previous positive view unchanged today. | |

Auction Technology (LON:ATG) (£421m | SR40) | Duncan Painter is appointed CEO with immediate effect. Previous CEO experience includes Omnicom Commerce and Ascential plc. | ||

Air Astana AO (LON:AIRA) (£380m | SR48) | Revenue up 13%, EBITDAR down 20% to $48.2m. After-tax loss of $(21)m. Confident in medium-term guidance. | ||

RWS Holdings (LON:RWS) (£342m | SR93) | In “advanced and exclusive discussions” to acquire Obviously, which is an IP protection and brand integrity platform. Acquisition is expected to comprise cash of £16.5m and an earn-out of up to £23.5m. Obviously generated £2.5m of revenue and a loss of £1.5m in the year to 28 Feb 26. | GREEN = (Roland - I hold) The price being paid for this loss-making startup (founded 2024) makes me a little nervous, but the impression I get is that Obviously could complete a suite of IP services that will allow RWS to upsell to its existing client base and generate material revenue growth. I’m going to remain positive because I think RWS remains a good, cheap business with improving prospects, but I think shareholders may need to wait some time until it’s clear whether the company has overpaid for Obviously. | |

Empire Metals (LON:EEE) (£227m | SR3) | Results from the first 88 holes at Thomas, out of a 712- hole program, continue to substantiate and delineate multiple thick, near-surface intercepts above 7% TiO₂, individual intervals exceeding 10% TiO₂, and a peak grade of 17.83% TiO₂. | ||

Gulf Marine Services (LON:GMS) (£224m | SR72) | 2 new contracts mark entry into Africa and Latin America. One contract is a charter for up to 170 days of the company’s recently-acquired vessel, while the other (in Africa) is a third-party vessel management contract, a new line of business for GMS. Current backlog now stands at $666m. | AMBER ↑ (Roland) [no section below] The most material piece of news in today’s announcement is that GMS’s backlog has risen by 10% to $666m since the end of 2025 ($606m) and remained stable during April (1 Apr 26: $660m). Full-year guidance has also been left unchanged today, having previously been placed under review in mid-April. This seems encouraging to me, given fears the company might be losing business due to events in the Middle East where a major client has declared force majeure and broker Zeus reports four vessels are “offline”. In this context, expanding into new regions also seems sensible – although we do not know how much today’s contracts have contributed to the improved backlog. I don’t think we can ignore the geopolitical and cyclical risks here, but I’m reverting to a neutral view to reflect the reiteration of previous earnings guidance and the reasonable valuation. | |

ASA International (LON:ASAI) (£212m | SR74) | Charles Harman appointed as Chairman. Current chair and deputy chair will step down. Harman was previously Vice Chairman at JP Morgan Cazenove. | GREEN = (Graham - I hold) [no section below] The outgoing Chair had two stints with ASA International, with his first involvement going all the way back to 2013, several years prior to the company’s IPO. A great deal of experience will therefore be leaving the Board with him, but his chosen successor is a heavy-hitting investment banker who will not be intimidated by a company of ASA’s size. We also have the departure of the company’s founder from the Board. Dirk Brouwer, still owning 32% of the company, will become Founder and Chair Emeritus (non-Board), and will remain “associated with ASA International in an advisory capacity.” With two departures and only one new joiner, the size of the Board will shrink to seven for now. With the shares continuing to trade at 4x earnings, my positive view here is unchanged. | |

Galantas Gold (LON:GAL) (£195m | SR25) | The current pit-constrained Mineral Resource Estimate update comprises an Indicated Mineral Resource of 102.4 million tonnes (Mt) at 0.45 grams/tonne (g/t) gold (Au) containing 1.47 million ounces (Moz) Au. Shareholders are reminded that Galantas does not yet own Andacollo. | ||

Rainbow Rare Earths (LON:RBW) (£196m | SR28) | Reviewing the potential benefits of US Listing. Company remains focused on core strategic priorities of feasibility studies at the Phalaborwa project in South Africa in 2026 and the Uberaba project in Brazil. | ||

Camellia (LON:CAM) (£154m | SR79) | FY25 revenue from continuing activities of £268m, with a trading Profit of £1.0m. Disposal proceeds of £20m, with year-end net cash of £134m. Post year-end disposal proceeds of £14.7m from Linton Park and UK Artwork. | ||

Invinity Energy Systems (LON:IES) (£100m | SR7) | Remains focused on reducing the cost of the Endurium product to expand addressable market. Targeting 66% reduction in cost per kWh compared to VS3 by “late 2026”. | ||

Andrada Mining (LON:ATM) (£95m | SR26) | High-grade lithium mineralisation confirmed across multiple drill holes with associated credits in tin (Sn) and tantalum (Ta) mineralisation confirmed in all reported holes. Expanded Stage 1 drill programme. | ||

Kodal Minerals (LON:KOD) (£63m | SR30) | Final payment for the second shipment of spodumene concentrate to Hainan received. “The operation has now received revenue of over approximately US$89 million from its first three shipments, and we expect shipments to continue at regular intervals targeting cargoes of up to 20,000 DMT." | ||

Cobra Resources (LON:COBR) (£49m | SR15) | Resource definition drilling has been completed across COBR’s Wudinna rare earth prospects, Boland and Head. All samples have been submitted for analysis. Initial results from Boland provide encouraging observations. Further results are anticipated through the coming months. | ||

Amigo Resources (LON:AMGO) (£33m | SR81) | JV between Amigo Resources (51%) and AK Corporation FZCO / Anil Group (49%) over a 17.73 km² contiguous REE licence package in south-west Tanzania. As operator and majority partner, Amigo's Group will lead and fund exploration programmes. AK Corporation is the local partner and asset originator. | ||

Cadence Minerals (LON:KDNC) (£22m | SR54) | DEV Mineração S.A., owner and operator of the Amapá Iron Ore Project in Brazil, has received the Installation Licence from the State of Amapá Environmental Authority. | ||

Robinson (LON:RBN) (£21m | SR83) | Sale of the Hipper House surplus property: net proceeds of £730k to be used to reduce bank debt. | AMBER ↑ (Graham) [no section below] We’ve been AMBER/RED on this one. Net debt was £5.4m at FY December 2025, with more disposals planned to reduce that figure further. A £600k disposal was announced in March (at a surplus to £540k book value). Today’s £730k sale (after costs) is at an even more impressive premium vs £320k book value, and RBN shares have bounced by a few percentage points in response. The full-year results noted that contracts had been exchanged on a total £3.6m of disposals, and that they were sale agreed on a further £2.9m of properties. As this is a profitable company (12.3p EPS forecast this year) and as the sale of surplus properties looks set to eliminate net debt, I don’t see the need for us to remain negative on this packaging company. I upgrade our stance by one notch to neutral. A word of warning: Robinson issued its most recent profit warning in December, and this year’s energy price movements may prove to be another serious challenge. | |

Fusion Antibodies (LON:FAB) (£18m | SR6) | Revenue +9% (£2.1m). Underlying gross margin 43% (2025: 22%). Cash £1.04m. “The Board remains cautiously optimistic for FY2027.” | ||

Genedrive (LON:GDR) (£15m | SR7) | University Hospitals Sussex NHS Foundation Trust hospitals transitioned to Business as Usual routine clinical service of the Genedrive® MT-RNR1 ID kit for the prevention of Antibiotic Induced Hearing Loss in newborns. This is “a key milestone in driving wider scale adoption of our MT-RNR1 genetic test in the UK”. | ||

Light Science Technologies Holdings (LON:LST) (£15m | SR3) | Contract confirmation from one of LST’s approved Injectaclad installers requiring c.£0.41m of Injectaclad material. | ||

Celsius Resources (LON:CLA) (£14m | SR13) | Update on complex conflict involving expiry of payment deadline for purchase of various shares from Celsius. The Board has terminated the executive consulting agreement with one of the company’s Executive Directors with immediate effect. | ||

Fulcrum Metals (LON:FMET) (£13m | SR13) | £6m funding package: £1m equity and up to £5m convertible debt. £2.5m at-the-market facility. | ||

Frontier IP (LON:FIPP) (£12m | SR10) | The new CFO was most recently the CFO of Actimed Therapeutics, and before that Destiny Pharma. |

Roland's Section

RWS Holdings (LON:RWS)

Up 5.5% at 97p (£360m) - Agreement in principle to acquire Obviously Group - Roland - GREEN =

(At the time of writing, Roland has a long position in RWS.)

Mark maintained our fully positive GREEN view on this content solutions company in his review on 23 April.

I am also positive, but I suspect it could be some time until we see whether the acquisition of Obviously Group will create genuine value for shareholders; Obviously is just two years old and generated only £2.5m of revenue last year:

Launched in 2024, Obviously is a UK-based technology company that has started to disrupt the IP management and protection solutions market, displacing existing solutions for multiple enterprises. Headquartered in London, Obviously employs approximately 30 people, 50% of whom are engineers and developers.

Note: today’s RNS is reporting an agreement in principle and not yet a firm acquisition.

Terms: A quick look at the main terms suggest that RWS is paying a lot of money for a loss-making startup:

Acquisition consideration is expected to total up to £40m.

This would comprise an initial cash payment of £16.5m plus an earn-out of up to £23.5m, payable based on “stretching EBITDA-related performance hurdles” from 2027 to 2029.

Obviously generated revenue of c.£2.5m in the year to 28 Feb 26, with a loss of £1.5m.

The initial cash payment proposed equals 6.6x last year’s sales, while the full consideration would equate to 16x last year’s sales – for a loss-making company!

Rationale for acquisition: unsurprisingly, today’s RNS leads with the “highlights” or rationale for this deal, not the financial terms.

The main points mentioned suggest to me that RWS believes Obviously will plug a gap in its offering to rapidly unlock significant new revenue opportunities – if so, that might explain the high price being paid.

The acquisition, if completed, will position RWS as a provider of an innovative end-to-end brand lifecycle technology solution, from creation and localisation to protection, strengthening RWS's value proposition as a unified "Global Brand Guardianship" platform for large enterprise clients.

Some of the details provided are:

“The acquisition will, if completed, expand the Group's total addressable market by c£2bn, through expansion into trademark and brand protection solutions, whilst also strengthening Protect's ability to capture a greater share of its existing addressable market.”

“RWS would plan to leverage Obviously's technology to offer the full range of IP services - patents, trademarks and brand - on a single, consolidated AI enabled platform.”

Obviously's client base is mostly made up of enterprise companies, including “well-known media & entertainment, technology, financial, pharmaceutical and sports companies.”

Obviously CEO Lewis Whiting would continue to lead the business post-acquisition.

About Obviously – this business has three core capabilities:

IP Portfolio Management: “a platform for IP case and workflow management with integrated IP services”

Brand Protection: “an AI-enabled brand protection capability”

IP Intelligence: “use of commercial and sales data to connect enforcement activities to real world commercial impact”

Roland’s view

RWS has a longstanding reputation and good market share in a number of IP-related areas, such as patent filings, translation and renewal. If Obviously really does provide good quality functionality in additional adjacent areas, I can see that this could be used to create a one-stop shop solution that can be upsold to RWS’s existing (large) client base.

That could – in a positive scenario – create rapid growth in recurring revenue and profitability.

However, it’s beyond my level of expertise to gauge how successful or quick this process might be. Nor do I have any insight into the quality of Obviously’s services versus various more established peers. My hope is that CEO Ben Faes’ track record – as a senior executive at Google – provides some evidence that he understands how to build profitable, large-scale technology platforms.

I also assume that chairman and 24% shareholder Andrew Brode is supportive of this deal, providing some boardroom skin in the game.

I can see some risks, though. We don’t know anything about the “stretching” EBITDA performance targets that have been agreed, never mind how they might translate to real-world actual shareholder earnings. This makes the true valuation and expectations behind this acquisition hard for outside investors to appraise.

Even if the acquisition is successful, we don’t know about any additional tech costs that might result as RWS seeks to create an integrated IP platform from previously separate services.

RWS has faced significantly higher IT costs in recent years as it upgraded services and addressed the technical debt from previous acquisitions. I was hoping to see a reduction in such costs going forward.

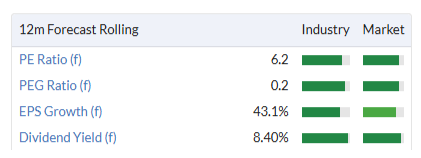

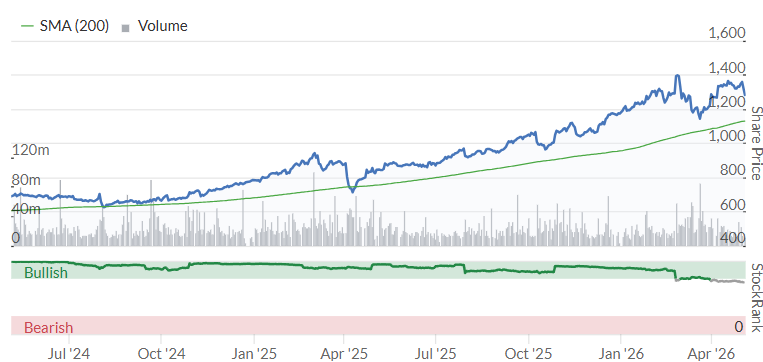

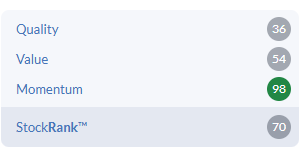

Despite the risk of poor returns from this deal, I’m going to leave our positive view unchanged today because I believe RWS remains a market-leading business in its core localisation and IP markets and I think the shares remain too cheap:

The StockRanks are also supportive, with Super Stock styling and strong factor scores – including improving momentum:

HSBC Holdings (LON:HSBA)

Down 5% at 1.291p (£220bn) - Earnings Release 1Q26 - Roland - AMBER =

Today’s quarterly earnings release has received a downbeat reception from the market after HSBC’s first-quarter results missed consensus estimates, due to higher costs and bad debt charges:

Reported pre-tax profit down $0.1bn to $9.4bn (company-compiled consensus: $9.6bn);

Adjusted pre-tax profit “broadly stable” at $10.1bn;

Annualised Return on Tangible Equity (RoTE): 17.3% (company-compiled consensus: 17.7%);

Common Equity Tier 1 (CET1) ratio down 0.9% to 14.0% vs 4Q25 (in line with consensus).

Bad debt charges: HSBC’s Expected Credit Losses rose by $0.4bn to $1.3bn for the first quarter. As a reminder, banks are required to model expected losses based on a variety of criteria, not simply wait until losses are confirmed before reporting them.

In today’s update, HSBC highlights two (relatively) big numbers:

A $400m “fraud-related” exposure in the UK, which the FT reports is related to collapsed mortgage lender MFS.

A $300m increase in expected credit loss allowances to reflect “heightened uncertainty and a deterioration in the forward economic outlook” due to the Middle East conflict.

These are eminently manageable amounts for this bank, but they have triggered a slight downgrade to the bank’s guidance for 2026. HSBC now anticipates reporting Expected Credit Losses of 45bps (0.45%) of average loan balances this year, from 40bps previously.

Operating costs: guidance for a total underlying increase of 1% in the bank’s cost base in 2026 is unchanged today. But operating cost growth in the first quarter was 3% on this adjusted basis, or 8% on an unadjusted basis.

I’m not sure how much seasonality (e.g. bonus accrual) might be included in these figures, but again the impression seems to be that cost growth might be running slightly ahead of expectations.

Net interest income: higher interest rates remain a boon for banks. Most of the big UK banks employ hedging strategies which mean that they are continuing to enjoy the benefit of higher rates, even though most central bank rates are now below peak levels. HSBC alludes to this in its commentary today (my emphasis):

The increase was mainly driven by deposit balance growth, the benefit of reinvestment of our structural hedge at higher yields and the impact of lower market interest rates on the funding deployed to the trading book, partly offset by higher trading balances.

Net interest income rose by 8% to $8.9bn in Q1. Excluding the funding costs of HSBC’s trading book, Banking NII rose by $0.7bn to $11.3bn, in line with consensus.

Outlook

We retain all of the Group financial targets we announced at our full year 2025 annual results in February 2026, including a RoTE of 17% or better for 2026, 2027 and 2028, excluding notable items.

HSBC’s main financial targets are unchanged today. I’ve already discussed the small increase in credit loss expectations above. There is also a slight increase to net interest income guidance for the year reflecting the slower-than-expected decline in interest rates:

We now expect banking NII of around $46bn in 2026, reflecting an improved interest rate outlook, while recognising the outlook remains volatile and uncertain. We had previously provided banking NII guidance of at least $45bn for 2026.

The bank’s CET1 ratio is expected to remain in its target range of 14% to 15% – well above regulatory requirements.

Roland’s view

HSBC notes heightened macroeconomic uncertainty in today’s commentary, while emphasising its ability to handle such conditions (my emphasis):

The macroeconomic outlook is facing heightened uncertainty, creating volatility in both economic forecasts and financial markets resulting in both tailwinds and headwinds. The Group is well-positioned to manage the impacts of these challenges through our high-quality revenue streams, conservative approach to credit risk and strong deposit franchise. Supporting our clients through this volatile period is a top priority.

I think it’s worth remembering that this 160-year old global bank is also one of the largest in the world. HSBC’s ability to handle difficult geopolitical conditions is a core part of its identity and is not in doubt, in my view.

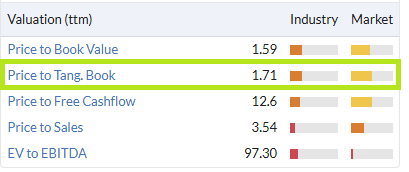

Valuation: HSBC shares have risen by 85% over the last two years:

They now trade at 1.7x tangible book value, according to the StockReport:

For a bank that’s generating a 17% return on tangible equity, this valuation seems within the ballpark of fair value to me. This view is based on the assumption that most equity investors will generally target an annualised return of at least 10% from stock market investments.

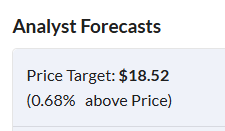

The StockRanks are currently neutral and I note that analysts’ consensus price targets suggest a similar view on fair value is held by the market:

Although earnings estimates have been steadily trending higher over the last 18 months, today’s commentary and market reaction may suggest that further upgrades are less likely, at least in the short term:

The size and complexity of this bank mean that a detailed review is beyond the scope of this report (and my abilities!). But I don’t think there’s any reason to be seriously concerned about HSBC following today’s update. The valuation isn’t unreasonable, either.

At the same time, I would guess that there may be better buying opportunities available at some point in the future.

To reflect this balance, I am going to adopt a neutral view on HSBC today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.