Good morning!

In overnight news, President Trump has paused US plans (announced on Sunday) to provide a safe escort for ships through the Strait of Hormuz. The decision has come after reported clashes between US and Iranian forces.

Stocks surged to all-time highs following the news, with the S&P 500 closing up by 0.8% at 7,259 and South Korea’s Kospi index gaining 6% to a new record as investors redoubled bets on AI. Correction: the tech-heavy Nasdaq index also closed at new highs last night:

Oil prices fell, with Brent Crude down by around 1.5% to $108. However, UK Natural Gas rose by 2.6% as fears of shortages continued. Elsewhere, Norway has announced that it will reopen three gas fields that were closed in the late 1980s.

Markets are expected to open higher this morning, while oil has continued to fall:

FTSE 100 to open up by 1% at c.10,325

German Dax to open up 0.7% at c.24,555

S&P 500 to open up by 0.3% at c.7,280

Brent Crude down 1% at $107.5

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

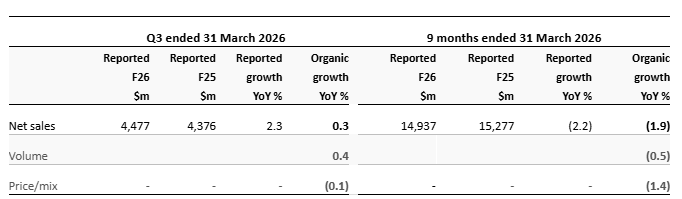

Diageo (LON:DGE) (£32.9bn SR62) | Q3 sales up 2.3% (0.3% organic), with YTD sales down by 2.2%. Weakness in North America, where net sales fell by a “high-single-digit” amount. FY26 guidance unchanged. | AMBER ↑ (Roland) Today’s quarterly update shows sales ahead of expectations, with a return to modest growth. Full-year guidance remains unchanged though, suggesting Q4 is not expected to erase the group’s difficult H1. The main drag on results remains North America, where Diageo’s sales slowdown deepened in Q3. I am confident of a turnaround but would like to see some progress with debt reduction before turning positive. To reflect this, I’m moving our view up to neutral today. | |

Next (LON:NXT) (£15.2bn SR61) | Full price sales up 6.2% in Q1, versus a forecast of 4.0%. Sales forecast for the remainder of the year is unchanged. FY27 pre-tax profit guidance is increased by £8m to £1,218m (EPS guidance +5.6p to 792.9p). Guidance is based on the assumption the impact of events in the Middle East neither worsens nor improves. | GREEN = (Roland) [no section below] This is another exemplary update from Next, which beat sales forecasts in Q1 and has upgraded profit expectations accordingly. With the group’s usual prudence and clarity, assumptions for the impact of the Middle East conflict are made explicit and have been extended to include a continuation of the current situation. Sales guidance for the remainder of the year is unchanged, but I don’t think it’s unreasonable to speculate that further upgrades may be possible. Graham was GREEN on Next in March. There’s been no significant change in valuation since then, so I’m happy to remain fully positive today. | |

Smith & Nephew (LON:SN.) (£9.9bn | SR54) | Q1 underlying revenue up 3.1%, with group growth in line with management’s expectations. New $500m share buyback announced. FY26 guidance unchanged, with trading profit expected to rise by c.8%. | ||

Kingfisher (LON:KGF) (£4.8bn | SR99) | CEO Thierry Garnier has resigned to take up a senior leadership role at a company outside of Kingfisher’s markets. He has a 12-month notice period and will remain in role while the search for a successor is undertaken. | ||

Renishaw (LON:RSW) (£3.5bn | SR74) | Revenue for the nine months to 31 March rose by 9.5%. Q3 was “a record quarter” with revenue up 14%. Substantial expansion of order books for semiconductor & electronics manufacturing and aerospace & defence. Full-year expectations in line with recent guidance for adj pre-tax profit of £145m to £165m. | ||

TBC Bank (LON:TBCG) (£2.6bn | SR82) | Net profit up 14.5% to GEL365m, with net asset value up 2.6% to GEL6.5bn. Q1 return on equity of 23.4%, +0.2% YoY. Remain confident of strong economic growth in Georgia and Uzbekistan in 2026. | GREEN = (James - I hold) Despite conflict impacting the broader region, it was more of the same from TBC Group. The Georgian business delivered first-quarter numbers that are hard to fault – 15% profit growth, a 23.4% return on equity, and loan book expansion of 12%. The Uzbek business continues to drag with loan book recalibration following regulatory changes negatively impacting profitability. Investors will also be concerned by rising NPLs across the business. Despite this, the headline numbers remain strong and the valuation metrics are incredibly compelling. | |

Trainline (LON:TRN) (£892m | SR72) | Net ticket sales up 7% to £6.3bn, with revenue up 2% to £453m. Adj EPS up 23% to 23.6p per share. FY27 outlook: greater competition and fare freeze to weigh on growth. Net ticket sales of £6.2bn to £6.45bn, w/ revenue of £440m to £455m. | ||

Biopharma Credit (LON:BPCP) (£785m | SR97) | Confirms that it has received a payment of $37.1m from Alphatec, consisting of $35m in principal and $2.1m of prepayment fees and accrued interest. The company earned a 11.93% net IRR on its ATEC investment. | ||

Target Healthcare Reit (LON:THRL) (£648m | SR95) | EPRA NTAV per share up by 1% to 120.6p, mainly due to a LFL valuation uplift of 0.8% driven by rent reviews. Total accounting return of 2.3% for the quarter, with adj EPRA EPS of 1.6p and fully covered quarterly dividend of 1.508p per share. | ||

J D Wetherspoon (LON:JDW) (£637m | SR28) | LFL sales up 3.4% in the 13 weeks to 26 April, with YTD LFL sales up 4.3%. Outlook: higher costs may result in “profits slightly below market expectations”. | BLACK (AMBER/RED =) (Roland) [no section below] Wetherspoon’s share price has risen slightly this morning despite today’s profit warning. This might reflect the broader market jump at the prospect of an end to the Middle East conflict or it may signify that investors have already priced in the downside here following earlier downgrades. Year-to-date sales growth of around 4% suggests to me that volumes may have been broadly flat, although this information isn’t disclosed. However, I’m struck by today’s report that the company has spent £26m on share buybacks so far this year at an average price 15% above the current share price. I would argue this cash might have been better used to help reduce net debt, which is expected to end the year between £740 and £760m, incurring £47m of interest costs. If today’s update was in line I would have upgraded to AMBER, but given the further downgrade to profit guidance I am going to leave our moderately negative view unchanged, reflecting the StockRanks' Value Trap styling. | |

| Intuitive Investments (LON:IIG) (£531m | SR55) | Extension of PUSU Deadline | Preparations for a possible offer are continuing. The deadline for Acceler8 Ventures to make a firm offer has been extended to 5pm on 3 June 2026. | TAKEOVER |

Guardian Metal Resources (LON:GMET) (£418m | SR26) | Strong progress across all PFS workstreams, with all required drilling now completed. The PFS is being supported by a US Department of War Defense Production Act Title III investment of $6.2m in a GMET subsidiary. | ||

Foresight Solar Fund (LON:FSFL) (£351m | SR48) | NAV per share unchanged at 99.2p on 31 March. Lower irradiation in Jan/Feb led to below-budget generation, but performance improved in March. Power prices increased during the period. Recent government policy changes are not expected to affect Foresight’s dividend for 2026. | ||

Vanquis Banking (LON:VANQ) (£304m | SR71) | Net receivables up 29% to £2,802m, with net interest margin down 2.2% to 15.6%. CET1 was down by 0.6% to 15.9%, reflecting deployment of capital to support lending growth. £3m provision for FCA Motor Finance redress is unchanged. Outlook: all financial guidance remains unchanged for 2026 and 2027 | ||

Animalcare (LON:ANCR) (£230m | SR51) | Revenue up 20%, with adj pre-tax profit up 62.7% to £10.9m. No dividend proposed following the announcement of a recommended acquisition on 16 April 2026. | TAKEOVER | |

Capricorn Energy (LON:CNE) (£224m | SR98) | Potential bidder Alamadiyaf al-Masiyyah continues to report progress regarding its funding arrangements. Deadline for a firm offer has been extended to 5pm on 3 June 2026. | TAKEOVER | |

Seeing Machines (LON:SEE) (£204m | SR18) | Reported production of 1.28m units in Q3 FY26, representing 122% quarter on quarter growth with over six million vehicles on the road now using Seeing Machines technology. Business guided to positive EBITDA for Q3 and H2, with production volumes rising again in Q4. | AMBER ↑ (James) Today’s update offers the inflection points that bulls had been hoping for. The increase in production volume is very impressive, and with the European General Safety Regulation mandating DMS fitment across new vehicles from July, the catalyst is really coming into view. That doesn’t counteract all of our concerns - debt refinancing remains an issue - but there’s definitely cause to look at this stock with greater optimism. At 36.2x forward earnings, it’s not cheap, but multiples can compress quickly beyond an inflection point. | |

Reach (LON:RCH) (£180m | SR68) | Q1 revenues fell 6.9% year on year as digital revenues dropped 8.1% due to lower search and referral traffic. Print revenues also declined 6.6%. Reach said it was on track to meet full-year market expectations despite this difficult first quarter. | AMBER = (Roland) While the decline in print revenue appears to be largely as expected, changes to Google algorithms have created new challenges for online publishers in recent months. As a result, the slump in digital revenue seen during the final quarter of last year continued into Q1. I am inclined to be cautious about the opportunity here, but with the stock trading on a P/E of <3 and offering a potential 12% dividend yield with cash flow support from 2027, I am not sure I can justify a negative view. To reflect this situation and today’s in line guidance, I am leaving our neutral view unchanged. | |

Smiths News (LON:SNWS) (£161m | SR98) | Revenues of £515.7m and adjusted operating profit of £18.3m for the first half of FY26 – both below FY25. Results on track to meet market expectations of £37.2m adjusted operating profit. Growth supported by strength in newer verticals, including recycling. Secured 96% of publisher contracts through to 2029 following renewal with the Guardian group. | ||

Hostelworld (LON:HSW) (£128m | SR21) | Reiterated full-year guidance ahead of AGM at noon, 6 May, with new chair Marieke Bax noting that intra-European travel demand was holding up and offsetting softness in long-haul bookings from Asia, which are impacted by the Middle East conflict. | ||

Ramsdens Holdings (LON:RFX) (£124m | SR96) | Upgraded profit before tax guidance for FY26 to a range of £28.5m to £31.5m, well ahead of the prior consensus of £24.1m, driven by a gold price running around 40% ahead of last year and a 50% increase in the weight of gold purchased. Record pawnbroking lending also contributed to the changed guidance. Cavendish upgraded forecasts: - FY26E adj EPS: 63.2p (53.2p prev.) - FY27E adj EPS: 44.7p (37.6p prev.) | GREEN = (Roland) The price of gold has remained strong, despite falling from the record high levels seen earlier in the year. Ramsdens’ gold purchase business is booming and pawnbroking demand has also risen. On the downside, the company flags up the risk that currency demand could fall if summer holiday travel is disrupted and warns of growing volatility in gold. Broker forecasts also suggest profits will peak this year. I’m conscious of these risks, but at this stage I think it’s fair to remain positive given the chain of earnings upgrades, Ramsdens’ underlying business growth and the reasonable valuation. | |

Jubilee Metals (LON:JLP) (£89m | SR36) | Jubilee Metals reported a 28.7% increase in saleable copper production to 2,177 tonnes for the nine months to March 2026. Full-year copper production is under review pending confirmation of progress at the Molefe Mine expansion. | ||

Brave Bison (LON:BBSN) (£83m | SR42) | MiniBMA, the marketing training business acquired by Brave Bison in August 2025, has signed a deal to put more than 1,000 Omnicom Oceania employees through its programme. | ||

Zanaga Iron Ore (LON:ZIOC) (£42m | SR25) | Zanaga Iron Ore Company announces completion of development programme for its Republic of Congo iron ore project, confirming improved economics including a Stage One NPV of $2.54bn. | ||

Energypathways (LON:EPP) (£18m | SR11) | EnergyPathways Irish Sea to be awarded a Gas Storage Licence by the North Sea Transition Authority (NSTA) as part of its MESH project – expected to be Britain’s largest integrated energy storage facility. | ||

Chesterfield Special Cylinders Holdings (LON:CSC) (£18m | SR73) | Chesterfield Special Cylinders announces lease of three acres of land adjacent to existing freeholding site in Sheffield – the lease is extended from less than 20 years to 125 years. | ||

Portmeirion (LON:PMP) (£13m | SR62) | In 2025, Portmeirion Group generated £91.1m in revenue – down £0.1m on 2024. The company reported a basic earnings per share loss of 25.3p, following a 8.04p profit the prior year. The group also announced the appointment of Michael Scheepers as CEO. |

Roland's Section

Ramsdens Holdings (LON:RFX)

Up 8.5% at 418p (£135m) - Trading Update - Roland - GREEN =

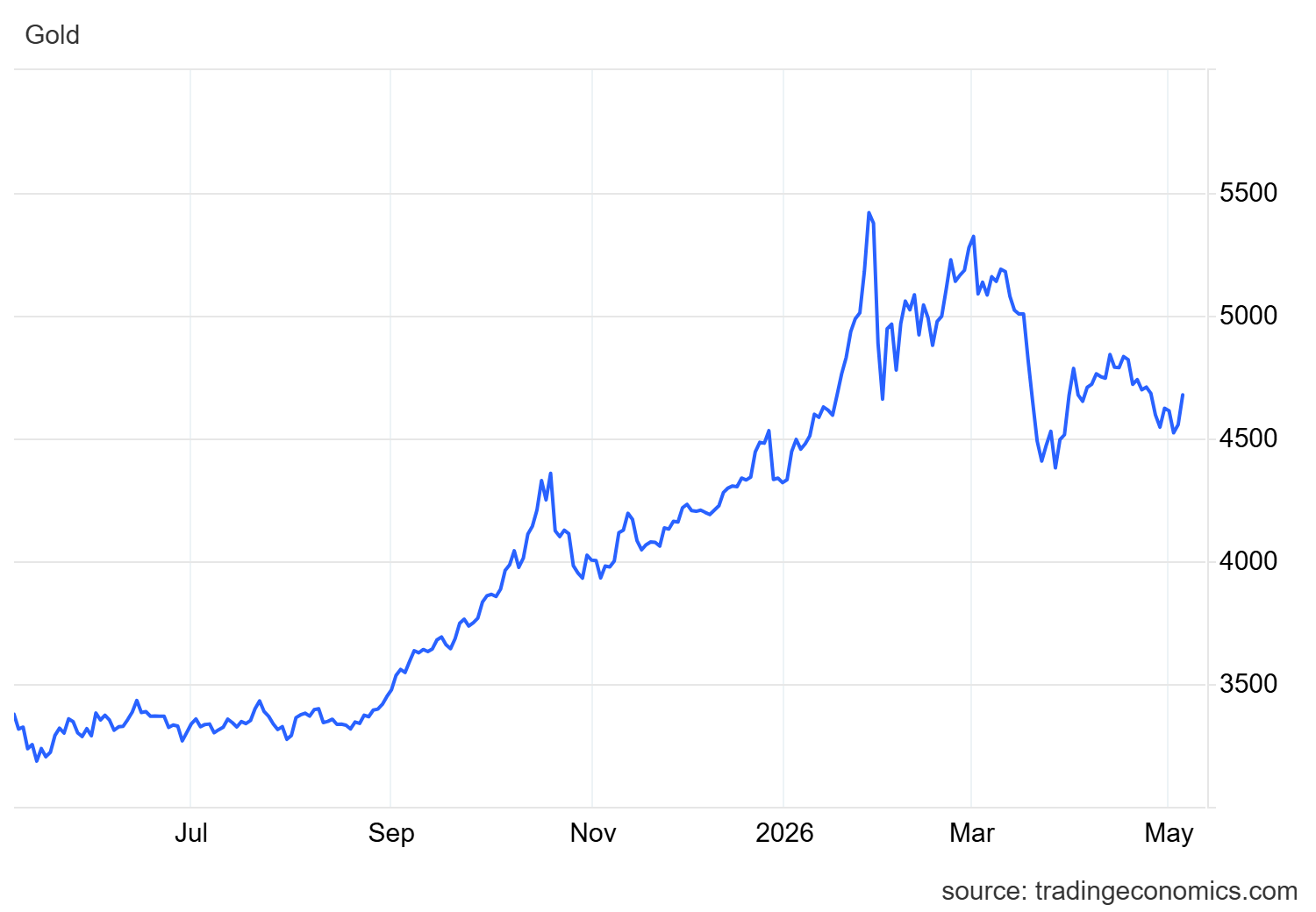

The UK’s remaining listed pawnbroker has proved to be an excellent way to play the gold price over the last couple of years:

Today we have another upgrade from this well-regarded small cap. This continues a long-running trend that’s seen FY26 earnings estimates double over the last 18 months:

Here are the main points from this morning’s update, which covers the period since 1 October 2025.

Unsurprisingly, the gold price is the main factor behind today’s upgrade:

While gold is below the highs seen earlier this year, Ramsdens says the price of the yellow metal remains 40% above the same period last year.

The combination of continued high prices, Ramsdens’ marketing efforts and UK macroeconomic conditions has driven strong growth in gold purchase volumes and pawnbroking:

The weight of gold purchased during the year to date is 50% above the same period last year.

Jewellery retail revenue is 25% ahead, year-on-year, with “slightly improved” gross margins.

Strong demand has seen the pawnbroking loan book rise by 24% to £14.1m since the end of September 2025.

Currency slowdown? The main risk flagged up today is that demand for foreign exchange could slump if jet fuel shortages reduce international travel over the peak summer period.

Ramsdens says total currency exchanged so far this year is “marginally back on last year”, but the commission earned has fallen by 9% as customers increasingly migrate online and towards lower margin currency cards.

New stores: Five new stores have opened recently and are said to be trading well. The company expects two further stores to open in May and expects to open between 10 and 12 stores in total during FY26.

Outlook

Ramsdens warns that the gold price has become volatile and the geopolitical environment remains uncertain. However, as things stand the Board believes pre-tax profit is now likely to be significantly ahead of previous guidance:

FY26 pre-tax profit to be “at least £28.5m” (previously “at least £24m”).

If the favourable gold price continues and summer currency volumes are in line with last year, FY26 pre-tax profit could be up to £31.5m (previously £28m).

With thanks to house broker Cavendish on Research Tree, we have updated earnings forecasts today. Interestingly, Cavendish has now chosen to upgrade its FY27 forecasts, in addition to FY26:

FY26E adj EPS: 63.2p (+18.8% versus 53.2p previously)

FY27E adj EPS: 44.7p (+18.8% versus 37.6p previously)

I think it’s worth emphasising that these forecasts show a drop in profits next year. This reflects an expected decline in profits from precious metal purchases, with continued growth in the remainder of the business.

Roland’s view

I see Ramsdens as a well-run business with attractive economics; returns on capital are notably high:

The valuation also remains reasonable, in my view, with the possible caveat that if FY26 does mark a peak in earnings from gold, the shares could look more expensive as we roll into FY27:

The potential for earnings to fall next year may explain why Ramsdens’ share price has only risen by <10% this morning, despite a 19% increase to FY26 and FY27 earnings estimates.

In effect, the stock is now slightly cheaper than it was yesterday!

Of course, predictions for the gold price in 2027 are subject to a very high level of uncertainty. I would expect further changes – up or down – to Ramsdens’ FY27 earnings estimates in the coming months.

Graham took a positive view on Ramsdens’ following March’s upgrade. Given the size of today’s upgrades and the stock’s current valuation, I don’t see any reason to change our view today. It looks like earnings expectations are still catching up with the strong gold price.

I’d also note that the algorithms continue to have a favourable view of this business, with Super Stock styling and a high StockRank:

Diageo (LON:DGE)

Up 4.9% at 1,548p (£34.6bn) - Q3 FY26 Trading Statement - Roland - AMBER ↑

I have been looking for an opportunity to turn more positive on this FTSE 100 drinks group. Is today’s quarterly update – which highlights an unexpected return to quarterly sales growth – the excuse I need?

Q3 & YTD trading highlights

The main takeaway from this morning’s update is that third-quarter sales rose by 2.3%, or by 0.3% on an organic basis. Volumes also rose by 0.4% during the quarter.

This result appears to be ahead of company-compiled consensus forecasts available on Diageo’s website, which suggested organic sales would fall by 2.3% in Q3.

Year-to-date sales performance is still negative, but a return to top-line growth is a key target for the business. It’s also the kind of early result from turnaround boss Sir Dave Lewis that could help to improve market sentiment towards this unloved stock.

I’ve pasted in the financial summary from today’s update to save retyping:

Source: Diageo Q3 26 statement

Geographic split: US slowdown

Diageo isn’t out of the woods yet, though. Today’s update was achieved despite a deepened sales slump in the group’s largest market, North America, which accounts for nearly 40% of group sales.

Source: Diageo Q3 26 presentation

Today’s commentary reflects a mixed performance across the world, especially in spirits. Ready-to-Drink (RTD) and Guinness are more consistent positive themes, with sales up nearly everywhere:

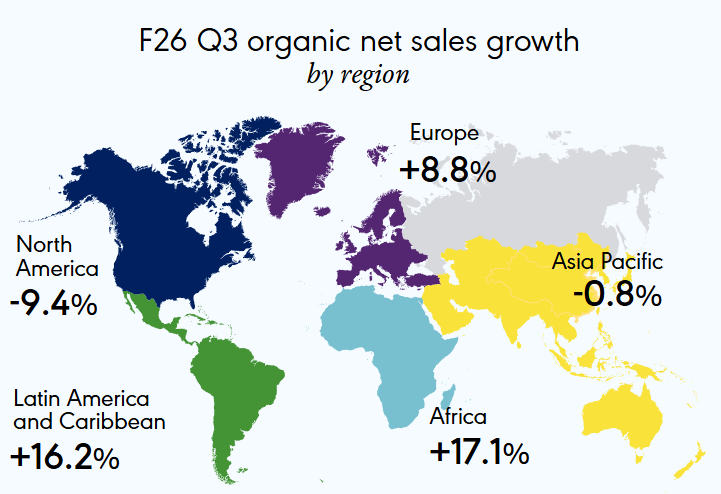

North America (Q3 -9.4% / YTD -7.6%): volumes fell by 9.9%, with price/mix growth limited to 0.5% by “the need for a more competitive offer” – i.e. price cuts. Spirit sales fell by 15.4%, driven by tough comparatives and a double-digit decline in tequila. Diageo Beer Company USA sales rose by 9.1%, led by Smirnoff RTD and Guinness.

Europe (Q3 +8.8% / YTD +4.3%): sales growth was driven by Guinness in the UK and Ireland and by spirits in the Middle East, Central and Eastern Europe. Price rises contributed 2.6% in Q3, with volumes up 6.3%.

Asia Pacific (Q3 -0.7% / YTD -8.2%): sales remained negative, with volumes down by 4.6%. However, performance improved significantly relative to H1. The main drag remained sales of white spirits in China, which “declined double-digit”. This offset low-single-digit gains in sales of international premium spirits. Price/mix rose by 3.8%, reflecting a more favourable product mix. Once again, Guinness contributed to the recovery, with organic sales up by a “double-digit” amount.

Latin America and Caribbean (Q3 +16.2% / YTD +7.7%): volumes rose by 10.5% in Q3, with price/mix contributing 5.6%. It looks like there may be some element of restocking here, with “buy-in ahead of the FIFA World Cup and Easter timing”. Brazil delivered double-digit volume growth, offsetting a high-single-digit sales decline in Mexico. Spirits were a winner in this region, with “double-digit scotch growth”. RTDs also performed well, led by Smirnoff Ice in Brazil.

Africa (Q3 +17.1% / YTD +12.7%): this region only accounted for 8% of net sales, but saw significant growth with volumes up 20% in Q3, offsetting some weakness in pricing due to a change in product mix. South Africa, Tanzania and Uganda are flagged up, with growth in both spirits (Kenya Cane) and beer (Serengeti). There was also strong growth in RTDs.

Outlook

Although there’s the obligatory caveat about the Middle East, Diageo’s FY26 guidance is unchanged today. That’s reassuring, given that we are less than two months from the year end on 30 June.

While we are mindful of continued geopolitical uncertainty, including the impact of the ongoing conflict in the Middle East on energy, supply and distribution; we are reiterating our fiscal 26 guidance.

After cutting expectations with his maiden update in February, CEO Lewis has given investors the stability they hope for by remaining in line today:

As a reminder, full-year guidance is for a 2.3% decline in organic sales, paired with modest growth in operating profit, aided by $300m of cost savings.

Consensus forecasts prior to today suggest FY26E adj EPS of 161 cents per share, putting Diageo on a P/E of around 12x.

Roland’s view

Diageo is clearly still having problems in North America. Dave Lewis acknowledges this today, promising action:

North America remains our biggest challenge, where market conditions are soft and our offer needs to be more competitive. Actions are already underway to address this.

Despite this, I am struggling to see any reason to be negative on Diageo when it’s trading on 12x earnings and offering a 3%+ dividend yield.

This is a world-leading business with a large portfolio of some of the world’s most valuable and recognised brands.

While patterns of alcohol consumption may be changing, this is ultimately a consumer goods group – Diageo’s brands cover the spectrum from premium to value and include a good number of ‘nolo’ options, including the spectacularly successful Guinness 0.0%.

My feeling is that Diageo may have lost touch with this reality and become complacent during the boom years for spirits premiumisation. I believe it should be possible for the business to reshape its product range to meet current demand more successfully. In my view, the shake-up promised by Lewis is likely to reprioritise marketing and should lead to a gradual recovery in performance.

I was AMBER/RED in February following Diageo’s profit warning and dividend cut.

I don’t think there’s any reason to maintain this negative view following today’s update. Indeed, I think there’s a good chance an AMBER/GREEN view could be justified.

The main reason I’m not turning positive today is that I’d like to see some progress on debt reduction before relaxing too much; Diageo’s net debt to EBITDA multiple was 3.4x at the end of December 2025. That’s a little above my comfort level, even for a business of this type.

To reflect this mix of views, I’m moving up to neutral (AMBER) today, with the hope that I’ll be able to turn more positive later this year. Diageo is on my watch list.

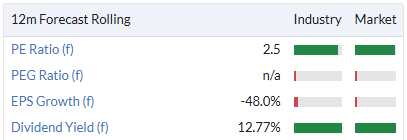

Reach (LON:RCH)

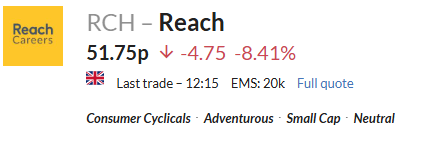

Down 7.4% at 52p (£165m) - Trading Update - Roland - AMBER =

Today’s trading update from this media group has met with a downbeat reception despite being billed as an inline update.

What seems to have happened is that online traffic has been hit by another Google update that’s resulted in a loss of volumes. This continues a trend first reported in July 2025 – my understanding is that there has been more than one such update to Google’s algorithms, putting some pressure on sites that rely on Google traffic.

The increased prominence of AI snippets (culled from other publishers' websites) at the top of Google Search results is unlikely to help either – increasingly, people are finding they don’t need to click through.

The impact of these trends is reflected in the company’s share price, which has fallen by 34% since the company’s half-year results were published on 24 July 2025:

Q1 trading - weak: while Reach doesn’t report user volumes, today’s revenue update makes it clear that both digital and print revenues suffered in Q1:

Digital revenue down 8.1%;

Print revenue down 6.6%;

Group revenue down 6.9%.

Print: Of course, it’s important to remember that print revenues are expected to be falling – print revenue fell by 4.6% last year and Reach’s strategy is to manage the print decline by growing the digital user base to offset the loss of print revenue.

My impression is that print performance in Q1 was largely as expected.

Cost savings are also underway to help support results – the company has previously guided for a 5-6% reduction in adjusted operating costs this year.

Digital: the main concern for me is that digital revenue isn’t rising. The 8.1% decline in digital revenue extends the 7.8% decline reported during the final quarter of last year.

Clearly, the company’s online efforts are not (yet) delivering tangible results. It’s not clear to me how much of this decline is due to Google changes and how much reflects wider factors (including the relative appeal of Reach content versus alternatives such as YouTube).

Outlook

CEO Piers North has left full-year guidance unchanged today, but I would argue that the weak start to the year could mean a greater H2 weighting to profits than previously expected.

Arguably, that increases the risk of a profit warning later this year. Consensus forecasts have been stable for some time though, so it’s possible that the current expectations may be supportable:

Pension cash windfall? One other factor to consider is the company’s pension scheme recently purchased a buy-in for its remaining uninsured members. According to March’s results, this has reduced Reach’s total expected scheduled pension contributions by £8.6m.

In an updated note today, house broker Panmure Liberum suggests that this could lead to a significant improvement in free cash flow in 2027 and 2028, potentially providing full cash support for the current dividend.

Roland’s view

The market already knows that Reach is ex-growth and has priced the shares accordingly. If forecasts are maintained – or even if they decline slightly – it’s possible to argue the stock is already too cheap:

The forecast dividend of 7.3p is covered by forecast earnings of c.21p, but is not expected to be covered by free cash flow this year. This suggests a further rise in net debt for 2026; net debt (excluding leases) rose from £14.2m to £34.9m last year.

However, this situation is expected to reverse from 2027. Today’s update from PanLib suggests free cash flow could support the dividend from 2027 onwards, potentially underpinning a very attractive 10%+ yield.

It’s also possible that digital performance will strengthen as Google changed bed in and publishers adapt (as they usually do, over time).

I am inclined to be cautious about the opportunity here, but given the low valuation and in line nature of today’s update, I am going to leave Graham’s previous neutral view unchanged today.

James's Section

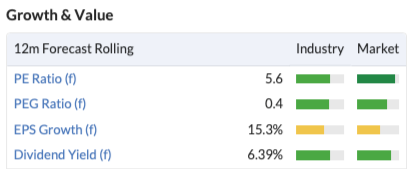

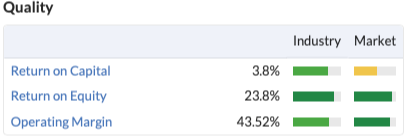

TBC Bank (LON:TBCG)

Down 1% at 4,654p (£2.62bn) – Q1 Results – James – GREEN =

(At the time of writing, James has a long position in TBCG.)

When I started writing, the stock was up 5%, then down 4%, and now it’s closing in on parity. Clearly, the market hasn’t made its mind up yet, but I have, and I’m reassured.

Personally, TBC Bank is a top-10 holding, sitting between Credo Technologies and Alphabet, and representing one of my largest UK-listed investments:

Headline numbers hold up

The company has been caught in the crossfire of two concerns, both outside of its control - Georgian political risk following the post-election protests of 2024/2025, and the US-Iran conflict.

However, today’s numbers confirm that neither is hurting the underlying business. Group net profit came in at GEL 365m, up 15% year on year with ROE at 23.4%. The Georgian business remains the core driver, with 24.1% ROE on 14% earnings growth and 24% growth in net interest income.

As always, banks thrive when the local economy is performing, and the Georgian economy continues to be exceptional. The country’s actual GDP growth in Q1 came in at 9.1%, well above TBC Capital’s own 7.4% full-year forecast.

Countries in which we operate, Georgia and Uzbekistan, are not immune to the fallout from this conflict. However, so far, the economic impact has been relatively muted, and, for now, we still expect to see strong economic growth in both countries in 2026, with a 7.4% real GDP growth forecast for Georgia and 7.9% for Uzbekistan.

Some signs of trouble

Investors should also have their eyes on the figures lurking beneath the headline numbers. Operating expenses rose 20% year on year. Staff costs were up 27% and the cost-to-income ratio climbed from 37.2% to 40.2%. NPLs also rose 36% year on year, with CIB Georgia NPLs more than doubling - that’s something to watch carefully.

What’s more, the Uzbek business continues to drag. Management guided for the Uzbekistan reset at the FY25 results and framed it as a deliberate recalibration following regulatory changes in the country. Net income fell 4% there year on year, ROE slumped to 10.9%, and the loan book is down nearly 10% quarter on quarter.

However, management suggests the pipeline is more encouraging than the numbers suggest. Auto loans and collateralised MSME lending are set to be launched around mid-year.

The former should tie in with the company’s majority investment in OLX Uzbekistan (no longer part of the OLX Group), a classifieds marketplace operating across a wide variety of sectors, including autos, with strong reach across the country.

James’ View

I bought shares in TBC and peer Lion Finance (which reports tomorrow) shortly after Russia invaded Ukraine four years ago. Both performed incredibly well, and I cashed out before the 2024 election - assuming the disruption would be worse for business than it has proven to be. Stayed invested and I’d be up 500% and 1,000% respectively.

As alluded to, I’m back in TBC, and unsurprisingly, it’s the metrics that garnered my interest. Away from the operational challenges, the numbers still look great. The stock trades at 5.6x forward earnings, with a price-to-earnings-to-growth (PEG) ratio in the region of 0.4. These figures point to a vast discount to the sector average globally.

Profitability metrics are also unmatched. The ROE figure (23.4%) sits far ahead of anything we’d see in the UK, albeit significantly below Lion Finance at 28.1%. Total returns are notably lifted by a dividend yield of 6.4% on a forward basis, with coverage in the region of 2.8x.

These figures, coupled with 15% net profit growth in the first quarter, continue to support my bull case. The company also boasts a strong StockRanks at 82. I’m staying GREEN.

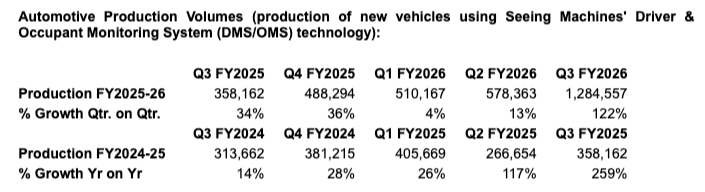

Seeing Machines (LON:SEE)

Up 8.2% at 4.48p (£203m) - Q3 FY2026 KPI Update - James - Amber ↑

Roland left this at RED in January, concerned that a loss-making growth story was trading expensively and that a looming debt refinancing made the risk-reward unattractive. The business had also announced that a customer had made an accelerated lump sum royalty payment of $14.1m, having previously been expected over the next four years. Roland wondered if this was a bailout in disguise.

Today’s update doesn’t resolve all of those concerns, but it does guide towards the inflection point that bulls had been waiting for. Seeing Machines, which makes the driver and occupant monitoring systems (DMS/OMS) that are fitted into cars by manufacturers, earns a royalty every time a device is deployed.

Production volumes soar

As such, the latest production volumes are clearly encouraging. The business said that production volumes hit 1.28m units in the third quarter, up 122% on the previous quarter and up 259% year on year.

Source: Seeing Machines Q3 KPI Update

Of course, production figures don’t always mean sales. But Seeing Machines said that Q3 royalty revenue would be higher than royalty revenue for the entire first half of the financial year. The company expects to deliver positive adjusted EBITDA in Q3 and H2 FY2026.

This appears to reflect Seeing Machines’ main catalyst: the European General Safety Regulation, which mandates DMS fitment across new vehicles from July 2026. That deadline is coming quickly into view.

Q3 delivered a clear inflection point for Seeing Machines. Importantly, Q3 Royalty Revenue was higher than Royalty Revenue for the entire first half of the financial year, demonstrating the operating leverage in our Automotive model as production programs scale. The Company expects to deliver positive Adjusted EBITDA in Q3 and H2 FY2026.

Management reported that there are now more than 6.1m vehicles on the road with Seeing Machines driver and occupant monitoring systems, marking an increase of 88% from 12 months ago. While we don’t have the full picture, this points to a truly impressive uptake from its client base.

The aftermarket Guardian business is a slight concern. Unit sales fell to 1,610 in Q3 from 3,764 in Q2, though management says some expected sales have shifted into Q4 and early performance there is encouraging. ARR grew 5% to $14.7m. It is a smaller and slower-moving piece of the business but worth monitoring.

The step-change in quarterly volumes is significant and we believe this marks the beginning of a new phase of higher, more consistent production volumes as we move through the end of FY2026 and into FY2027.

James’ View

The debt refinancing - approx $62m convertible note with Magna International maturing in October - and valuation concerns that Roland raised in January haven’t gone away.

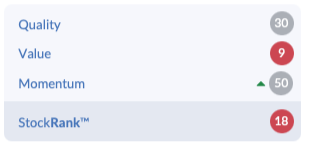

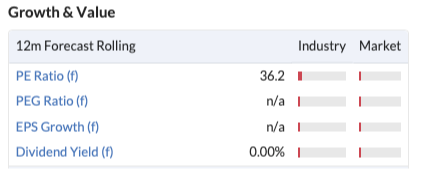

And some of those concerns are reflected in the company’s poor StockRanks - just 18. The business trades around 36.2x forward earnings and with a price-to-sales ratio of 4.6 on a trailing basis.

However, I think there’s some cause to look at Seeing Machines a little differently now. It’s currently trading around 2x forward sales, and that doesn’t look overly stretched for a business that’s apparently approaching inflection point. Those of us familiar with companies near inflection point will also be acutely aware of how quickly a 36.2x multiple can compress.

I'm not ready to go GREEN - the refinancing and Guardian softness keep me cautious - but the inflection promise is real enough to move off RED. AMBER feels right here. Watch Q4 closely.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.