Good morning! I have a backlog section on STEM to get us started.

Update: SRC is also from the backlog, in case anyone was wondering.

Today's Report is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BHP (LON:BHP) (£135bn | SR85) | Craig has been at BHP for over 25 years and is currently President Americas. During his tenure in this role the group has become the world’s largest copper producer. | ||

Compass (LON:CPG) (£38.6bn | SR53) | As announced in February’s trading statement, Compass will change the trading currency of its LSE-listed shares to USD from 1 April 2026. This aligns with the group’s reporting currency, “reducing FX volatility” and “simplifying the investment case for global investors”. Dividends will continue to be paid in GBP unless shareholders elect to receive them in USD. | ||

Prudential (LON:PRU) (£27.7bn | SR48) | Adjusted operating profit up 6% to $3,306m, adj EPS up 13% to 101.4c. New business profit rose by 13% to $2,782m and return on equity was stable at 14%. “Structural demand for our products in Asia and Africa continued to rise”. 2026 Outlook: expect double-digit growth in new business profit and adjusted earnings. “Firmly on track” to achieve 2027 objectives. | AMBER/GREEN = (Graham) I’m moderately positive on a stock that looks moderately attractive to me. The StockRank is 48, also very much middle-of-the road, with a Neutral style. | |

Diploma (LON:DPLM) (£6.8bn | SR68) | “Great performance continues through H1. Confident in H2 momentum”. H1 growth was driven by "outstanding" performance in aerospace, with a more typical growth rate expected in H2. Upgraded FY26 guidance: organic revenue growth 9% (prev. 6%) with operating margin c.25% (prev. c.22.5%). Represents a c.13% upgrade to consensus operating profit. | AMBER/GREEN = (Roland) [no section below] Diploma’s share price has risen by nearly 700% over the last decade, highlighting the quality and strong management of this business. The shares always look quite expensive for what is essentially an industrial parts distribution company, but today’s update highlights why Diploma has maintained a commanding valuation. EPS growth has compounded at 15% over the last decade. Even before today, FY26 earnings forecasts had risen by 13% over the last year. Today’s upgrade suggests a further material increase to EPS estimates. With the stock trading on a forward P/E of c.25, I can’t be fully positive but am happy to retain my previous AMBER/GREEN view. | |

Ithaca Energy (LON:ITH) (£4.5bn | SR97) | Total production up 49% to 119 kboe/d, with exit rate of 148 kboe/d. Adj EBITDAX up 45% to $2,030.8m, net cash flow from operating activities up 105% to $1,745m. 2026 outlook: production guidance of 120-130 kboe/d, with net operating costs of $820-860m. Shareholder returns: 2026 dividend commitment of 30% of post-tax CFFO, with a target range of $470-520m (2025: $500m). | AMBER/GREEN = (Roland) [no section below] A slightly mixed update from this large oil producer, whose shares are down slightly today. One possible reason for this cautious reception is that full-year production guidance for 2026 is below the 2025 exit rate of 148kboe/d, suggesting no further production growth is expected this year. It’s also worth noting that while the change in shareholder dividend payout to 20-35% of CFFO is framed as an increase from 15-30% previously, the actual amount expected to be paid looks like it could be pretty similar. As with production, the impression this gives me is that cash flow from operations could fall slightly this year, perhaps due to expected higher operating costs. I estimate a c.9% dividend yield based on today’s guidance, which is obviously still attractive. The shares have spiked higher since the start of the Iran War and perhaps might fall back again if the conflict comes to a prompt end. Making predictions about this kind of macro situation is beyond my paygrade, but on balance I think Ithaca should continue to do what it’s intended to do, generating attractive cash flows from mature fields and existing discoveries. The latter include the large Rosebank project, which is expected to start production in 2026/27. | |

Softcat (LON:SCT) (£2.26bn | SR49) | Revenue up 53.5% to £837.5m, operating profit up 15.6% to £85.2m. Adj EPS up 25.8% to 36.1p. “AI is reshaping customer priorities at pace”. Full-year guidance upgraded: “high single-digit growth in underlying operating profit” (previously low single-digit). | AMBER/GREEN = (Roland) Today’s results show the expected strong growth in hardware needed to support the rollout of AI capacity in data centres. This was supported by growth in security software and “partner-delivered services", many of which I guess may also relate to AI. Customer growth was relatively modest during the period but the company’s existing customers are all spending much more as they adopt AI. At this stage it’s impossible to say how long this spending splurge will last, but today’s upgraded guidance suggests to me that visibility for the remainder of the year is good. Based on the strength of these figures I am going to leave our broadly positive view unchanged today. | |

Moonpig (LON:MOON) (£654m | SR67) | Expect FY26 adj EBITDA to be in line with guidance for mid-single-digit percentage growth. Adj EPS to be at the top end of guidance for 8%-12% growth, aided by buybacks. Announced further £65m buyback for FY27. | ||

Target Healthcare Reit (LON:THRL) (£634m | SR83) | Total accounting return of 6.8%, EPRA NTAV per share up 4% to 119.4p. EPRA adj EPS up 8.5% to 3.4p, covering H1 dividends of 3.016p. LTV now reduced to 15.2% with interest rate hedged on 98% of borrowings until Sept 2030. Sold 10 properties in H1 at a weighted premium of 11.7% to book value. Invested £45m to acquire three “modern operational care homes” in Central Scotland. | ||

Advanced Medical Solutions (LON:AMS) (£432m | SR46) | Revenue up 29% to £228.9m, adj pre-tax profit up 15% to £33.9m. Strong growth in Surgical Business Unit, with sales up 36%. Some recovery in Woundcare business (sales +9%). 2026 outlook: confident in delivering revenue and EBITDA in line with expectations. | AMBER (Roland) In our first look at this stock since 2024 I reach mixed conclusions. While cash generation was good last year, revenue growth was boosted by acquisitions and was just 10% on an organic basis. In addition, sales in the Peters Surgical business acquired in late 2024 were flat year-on-year – a situation blamed on distributor destocking. I can see plenty of scope for growth here, but I’m also aware that revenue growth in recent years has not translated into profit growth. The return on capital generated by the business is also pretty average, suggesting to me that past acquisitions may have been quite expensive. On balance I’m going to take a neutral view on this initial review. But if the company can deliver on guidance for a return to more profitable growth, I’d hope to be able to take a more positive view later in the year. | |

Intuitive Investments (LON:IIG) (£366m | SR58) | Hui10 (IIG’s primary investment) has made “significant progress” with its rollout in China over the last year, in line with management expectations. This includes an increase in lottery transaction value to RMB 306m (2024: RMB 0.8m) and a key regulatory agreement allowing a “paperless play” pilot in 2026. | ||

Sovereign Metals (LON:SVML) (£267m | SR20) | Measured & Indicated Resource increases to 1,652Mt (previously 1,200Mt). Measured & Indicated Contained Rutile increases to 16.1Mt (previously 12.2Mt). | ||

B.P. Marsh & Partners (LON:BPM) (£231m | SR86) | New Investment: Nine Edge Wealth Limited & New Investment: Ventura Risk Partners Holdings | Nine Edge Wealth: acquired 30% equity interest and provided £5m loan in this early stage IFA business with £70m of AUM. BPM has a previous relationship with Nine Edge’s founder, Derek Miles. Ventura Risk Partners: a newly formed insurance broker focused on energy risks. BPM has acquired a 25% equity interest and provided a £2m loan facility. | GREEN = (Graham - I hold) I’m a holder and a buyer of this one, having faith that their investment process will continue to work now that Brian Marsh has taken a non-Executive role. It will be no easy task, as they have grown BPM into a rather large investment vehicle - but if they stick to their knitting, they should have a chance. Both of today’s investments are sized comfortably and still leave them with plenty of cash (the cash balance was £49.5m in January). In each case, they gain a significant equity stake by providing a loan. Nine Edge Wealth is a little unusual as it’s an IFA investment, not an insurance investment, but it was established by someone BPM has done business with before (Derek Miles). I’ll sleep soundly at night, considering the sums involved. |

Pulsar Helium (LON:PLSR) (£173m | SR32) | Successful completion of drilling at the Jetstream #7 appraisal well at the Company's flagship Topaz Helium Project in Minnesota, USA, having reached a total depth (TD) of 2,979 feet (908 meters) on March 10, 2026. As previously reported, gas was encountered during drilling. | ||

Genel Energy (LON:GENL) (£153m | SR29) | Production 17,520 bopd (2024: 19,650). Operating loss $10.3m (2024: $52.4m). “Since regional hostilities began two weeks ago, production has been temporarily halted from Tawke. A state of readiness has been maintained to allow a production restart as soon as it is safe to do so. At this moment, our guidance for 2026 remains unchanged from our January trading statement.” | ||

FDM (Holdings) (LON:FDM) (£135m | SR88) | Revenue down 31%, adjusted operating profit down 59% (£13.6m). A resilient performance in 2025 against a backdrop of continued challenging market conditions. Outlook: ”We continue to see encouraging signs in some of the markets we serve, albeit levels of confidence and activity vary across our geographies. Recent events in the Middle East clearly add to the levels of economic, political and market uncertainty, but the Board is optimistic that areas of the Group less impacted will continue to experience the modest uptick in activity seen over recent months.” | ||

Trufin (LON:TRU) (£119m | SR63) | Revenue +20%, adjusted PBT £8.4m (previous year: £0.9m). Playstack revenue up 24%. Group revenue for the two months ended 28 February 2026 are tracking in line with the Board's expectations at not less than £9.3m. | ||

Ramsdens Holdings (LON:RFX) (£118m | SR96) | Ahead of expectations: Taking into account the strong trading for the first five months of the year, and the Board's updated expectations on the outlook for the gold price, the Group now expects its profit before tax for FY26 to be at least £24m and, if the favourable gold price and trading conditions continue, potentially up to £28m. Previous expectations: £21.1m. | GREEN = (Graham) This update has triggered some large upgrades to FY26 expectations, and FY27 estimates haven't caught up to the current gold price yet. | |

Fevara (LON:FVA) (£67m | SR60) (formerly Carr’s Group) | Completes the acquisition of a high-specification production facility, strategically located in São Paulo State, Brazil. Initial consideration £4.3m: £4m for freehold property, and the remainder for the existing mineral distribution business. Defcon due in March 2027 will be self-funding. | ||

Ilika (LON:IKA) (£50m | SR11) | IKA has received positive feedback from a UK defence agency on safety tests of its batteries under battlefield conditions, highlighting the potential of the technology for use in high-risk, mission-critical environments where safety is paramount. | ||

Nexteq (LON:NXQ) (£43m | SR81) | Revenue +4%, adjusted PBT down 25% (to $3.6m). Net cash $25m. Outlook: “The acquisition of the Group's historically largest customer has led to a reduced revenue expectation in the Quixant brand but we are generating significant interest in Launchpad and IQON-3”. Component shortages and cost increases creating customer uncertainty. Estimates: Cavendish reiterate FY26 and FY27 forecasts for revenues and earnings per share. | ||

Aptamer (LON:APTA) (£22m | SR23) | New programme to develop targeted radiopharmaceuticals, in collaboration with Radiopharmium Ltd. Aptamer has identified three strategic therapeutic targets, representing high‑value clinical conditions, for which Optimer® radioconjugates will be developed. | ||

Goldplat (LON:GDP) (£21m | SR90) | Revenue +53%. Operating profit of £4,802,000 (H1 2024: £2,635,000). Net cash £4.8m. CEO comment: “I am encouraged by the continued strong results achieved by the group (supported by good volumes and high gold price) and Group being in a position to start paying regular dividends.” | ||

Northern Bear (LON:NTBR) (£14m | SR98) | NED has stepped down with immediate effect, and is thanked. A process has also commenced to recruit a permanent Finance Director. | ||

ITIM (LON:ITIM) (£11m | SR38) | Revenues down 2% to £17.5m (“broadly flat”!). Pre-tax loss £464k (2024: profit £175k), impacted by a bad debt. Results are below current market expectations. It was “a robust performance set against a challenging economic backdrop particularly in the retail sector.” | BLACK |

Graham's Section

SThree (LON:STEM)

Down 1% yesterday to 165.4p (£210m) - FY26 Q1 Trading Update & CFO Departure Graham - AMBER =

It was a double header from SThree yesterday, with the Q1 trading update accompanied by news of the CFO departing in a separate RNS.

1-year chart:

Let’s check the Q1 update first:

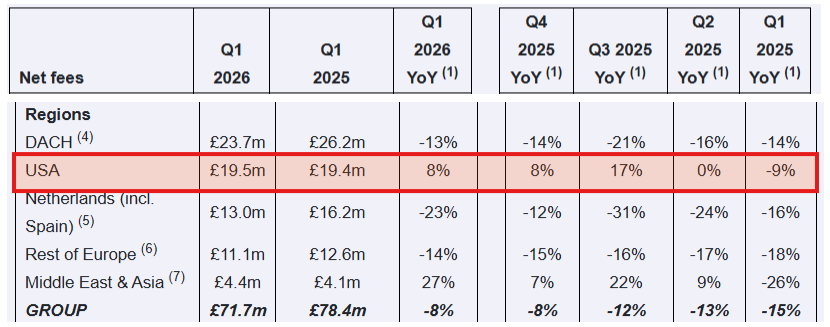

Net fees down 8% year-on-year, “reflecting continued stabilisation, supported by ongoing growth in the USA and Japan, and a significant improvement on the prior-year rate of decline.”

“Key contract renewal period concluded and new business activity broadly consistent year-on-year, with both performing in line with expectations.”

Contract fees down 10% year-on-year, while Permanent fees were flat year-on-year.

I do find it interesting that Permanent recruiting has just outperformed Contract.

STEM has spent years allowing its activities in Permanent recruiting to shrink. Permanent recruiting is seen as a volatile source of income that is more geared to the health of the economy - but in the very short-term at least, it is steadier than Contract.

Net cash of £51m. I interviewed SThree’s management in January and was informed that they can have £30-35m swings in cash on a monthly basis. So while the net cash balance always seems very impressive, it’s important to bear in mind that they are using most of it from time to time - it’s not just sitting idle.

That said, they do have some surplus, especially as there is no cash needed to assist with growth right now (due to the lack of growth). A £20m share buyback is ongoing.

Outlook: in line with previous guidance.

CEO comment:

Trading in the first quarter of FY26 has started in line with expectations, with continued stability across our business and encouraging momentum in select markets, notably the USA and Japan. New business activity was consistent with the prior year, which is particularly encouraging given a lower sales headcount, demonstrating improved productivity and operational efficiency. This performance was achieved against a backdrop of ongoing macroeconomic volatility, including geopolitical uncertainty and rapid technological change, which continues to influence business priorities and investment decisions.

CFO departure: after five years with the company, Andrew Beach is stepping down. He will assist with the transition to a new CFO until July.

He says:

With stable performance being delivered, FY26 expectations reiterated and the TIP (GN note: Technology Improvement Programme) now successfully deployed, it feels like the right time for me to consider the next phase of my career.

I had the chance to speak with Mr. Beach once or twice, and he was very helpful.

Graham’s view

Turning back to today’s trading update and the broader prospects for SThree, I think a neutral stance continues to make sense after an “in line” update.

The bigger picture question for me remains whether or not recruitment is in some way structurally broken. I can’t help noticing the trend that nearly all recruiters are doing poorly, and have been for some time.

While I don’t doubt their explanation that economic trends aren’t helping them, the downturn has been going on for too long, in my view, for that to explain it fully.

In the case of SThree for example, which I think is one of the most strategically sophisticated recruiters, net fees have been falling since at least 2023. And other recruiters have seen even sharper declines than SThree in recent years.

The best counter-argument I can come up with against this point of view is the United States, which is the second-largest regional contributor to SThree’s revenue..

Today’s update shows an 8% increase in net fees in the United States, stated before a currency headwind (after the currency headwind, net fees were flat).

Perhaps this proves that if you have a truly booming economy, net fees can still be strong?

The US has consistently outperformed SThree’s other major regions:

SThree says: “Among the Group's three largest markets, which accounted for 73% of net fees, growth in the USA was underpinned by strong demand for skills in Technology and Energy.”

I should also mention that I’ve been particularly concerned about the ever-growing impact of AI, LinkedIn and other possible sources of technological disintermediation.

While technological disruption might still be a factor, I should acknowledge that if it was happening anywhere, it would probably be expected to happen in the United States first.

So in summary: I still don’t feel like I totally understand why recruitment fees are so weak these days.

I do know that I would be extremely selective when it comes to investing in recruitment stocks, and would probably not invest in any of them - not even in SThree, which remains my pick of the bunch. I’m therefore staying neutral.

Stockopedia’s calculations are far more positive: they love what they see here, calling it a Super Stock:

Ramsdens Holdings (LON:RFX)

Up 10% to 400.5p (£130m) - Trading Update - Graham - GREEN =

Ramsdens Holdings PLC, the growing, diversified financial services provider and retailer, is pleased to provide a further update on FY26 (year to 30 September 2026) trading to date (the "year to date").

I took us back up to fully positive on this one last month and so I am gratified to see that expectations continue to rise:

As I said last time, the surging gold price is central to the story - not something that the company could have predicted, but something that it is well-placed to profit from.

With emphasis added by me:

Further to the Group's announcement on 10 February 2026, the Company has continued to perform well across its core income streams and has seen further benefit from the sustained, very high gold price compared to historic levels in its purchase of precious metals division. Based on the current geopolitical and economic climate, the Board believes that the gold price could remain elevated throughout the second half of FY26. This assumption means that profits within the precious metals division would be ahead of the Board's previous expectations for HY2, reflecting both the high gold price and increased purchase volumes.

The average gold price is up by 50% year-on-year. This has triggered increased gold sales from customers, which are also up by 50%.

Jewellery retail revenue is also quite remarkably up by 25% year-on-year. Perhaps a few customers have sold their old gold, and recycled it into something new?

Even pawnbroking is trading very well, with the loan book up by 18% year-on-year. Logically this does make sense - if consumers are as challenged as so many companies say, this should feed through to increased demand for more pawnbroking loans.

The only weak point is currency exchange, where commissions are down 5% due to customer migration online, where margins are lower.

CEO comment from Peter Kenyon:

"Ramsdens continues to perform well across its diversified business model reflecting the strength of our trusted brand, value for money proposition and outstanding team. In addition to underlying progress across the business, we continue to benefit from the high gold price, which is significantly boosting both customer demand and profits within our purchase of precious metals segment.

Estimates

New PBT guidance is “at least £24m” and “potentially up to £28m”, vs. the prior consensus forecast of £21.1m.

The new note from Cavendish upgrades the FY26 EPS estimate by 14% to 53.2p (previously 46.6p).

Looking ahead to FY27, they have only increased the EPS estimate by 2% to 37.6. However, they acknowledge that this estimate is based on a gold price 30% lower than current levels.

Graham’s view

As I’ve said many times, this stock has become a call on the sustainability of the gold price.

Personally, I’ve always been quite bullish on gold. And I like pawnbrokers as a way for investors to get positive exposure to the yellow metal.

So while I can’t predict the future, I’m fine with the assumption that the current gold price is sustainable (£3,700 per ounce).

This means I’m happy to accept the new PBT guidance of £24-28m for FY September, and I’m inclined to think that FY27 forecasts will have to be upgraded accordingly.

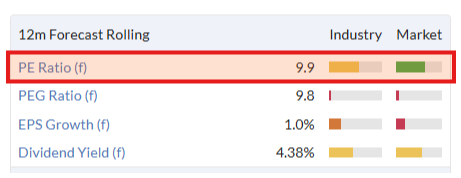

Note that at 53p of EPS, the P/E multiple is more like 7.5x.

The forecast rolling PE is based on estimates at the lower gold price:

Therefore I’d argue that the ValueRank is understated:

Though it hardly matters, as RFX is already classified a Super Stock.

It shouldn’t come as a surprise that I’m going to leave this on GREEN.

Prudential (LON:PRU)

Down 3% to £10.65 / $14.22 (£26.8bn / $35.8bn) - FY25 Results - Graham - AMBER/GREEN

We’ve had a reader request for this and I’m happy to give it a quick overview. Unfortunately the business is too large and complicated for me to be able to do more than that.

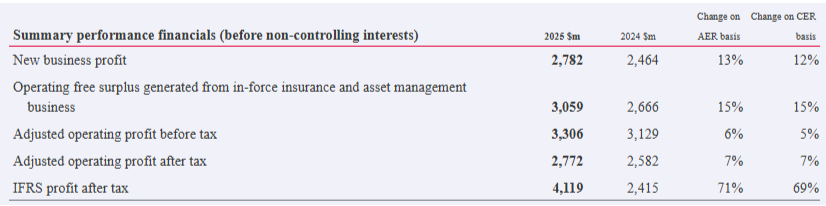

Headline: double-digit growth across key financial metrics in line with the Group's 2025 guidance.

New business up 12% to $2,782m (embedded value basis = present value of future profits).

Adjusted operating profit up 5% to $3,306m

Earnings per share up 12% to 101.4 cents.

Here are some of these numbers in table format, also showing a nice jump in statutory profits (“IFRS profit after tax”):

There’s a 15% increase in the dividend, but the dividend yield is weak (only about 2% at current share prices).

Most returns to shareholders are in the form of buybacks rather than dividends: there’s a $1.2 billion buyback underway in 2026, vs dividends of about $600m

Book value, including anticipated profits (“TEV”):

Group TEV equity of $37.8 billion, equivalent to 1,483 cents per share, up 15 per cent (on an actual exchange rate basis).

I note that the current share price and market cap are only at a modest discount to this (4-5%).

CEO comment:

"2025 was a strong year of consistent delivery for Prudential, with double-digit growth reflecting sustained momentum throughout the year. Structural demand for our products in Asia and Africa continued to rise, driven by the increasing protection, retirement and wealth needs of our customers. We continued to digitise our customer acquisition and servicing capabilities…

We carry the momentum of 2025 into 2026 and are confident in our double-digit growth trajectory across our key metrics, putting us firmly on track to achieve our 2027 financial objectives."

Graham’s view

I think this is one of those instances where it makes sense to write a deliberately short analysis: I do not have a strong view on The Pru but I’m happy to give it an AMBER/GREEN on the basis of its reputation, results that look solid, and a market cap a slight discount to the company’s “TEV equity”.

I should emphasise that TEV equity is forward-looking and is not the same as traditional accounting book value.

The accounting book value of PRU, without any adjustments, is only $20.1 billion (vs. TEV equity of $37.8bn).

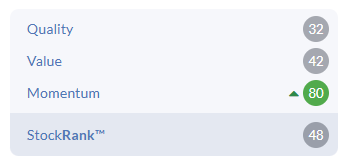

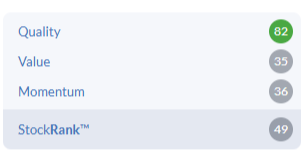

But I do think AMBER/GREEN makes sense: I’m moderately positive on a stock that looks moderately attractive to me. The StockRank is 48, also very much middle-of-the road, with a Neutral style.

Sigmaroc (LON:SRC)

Down 6% on Monday to 115.2p (£1.3 billion) - Full Year Results and Notice of AGM - Graham - AMBER =

SigmaRoc, a leading European lime and minerals group, is pleased to announce its audited results for the year ended 31 December 2025.

Let’s catch up on this story from Monday.

Sigmaroc processes and supplies lime and limestone materials from its quarries across Europe. It mostly sells into the construction industry (45% of revenues) with the main product category being “high-grade minerals (71% of revenues).

2025 saw “Strong delivery ahead of original consensus” (but probably not against existing consensus, seeing as the share price retreated on Monday.)

Some highlights:

Revenue +3.8% even though volumes were down 3%, “reflecting softer construction and steel markets”.

Adjusted EBITDA +16.7% (£262m)

Adjusted PBT +31% (£154m)

Actual PBT +116% (£99m)

Sigmaroc acquired various assets from CRH - previously Cement Roadstone Holdings - in 2024, and says that it has now delivered on its minimum target of €40m of recurring synergies, two years ahead of schedule.

There’s also a reduction in net debt, from £509.5m to £472m. To me, that still looks pretty large against pre-tax profits.

But measured against EBITDA, the leverage ratio is 1.8x (which is not extremely high).

Sigmaroc separately provides “pro forma” or like-for-like numbers, which look only at the performance of continuing operations throughout all of 2025 and 2024. These numbers show a slight reduction in revenues “due to overall volume reduction”, but also an increase in margins “reflecting self-help initiatives and cost control.”

So I think the pro forma numbers reflect pretty well on the company.

Outlook:

The Group expects 2026 to benefit from a number of structural trends, underpinning its strong position in the European lime and limestone markets;

Extreme winter conditions slowed the start of the construction season in certain regions like Poland and Belgium, but sector activity has since recovered

Cost management remains a core focus generally...

CEO comment:

These results demonstrate the quality of our business, the agility of our business model and the resourcefulness of our teams. They show the company is now well set up for its next chapter, to scale and take advantage of the many cyclical and structural tailwinds which are starting to emerge in Europe.

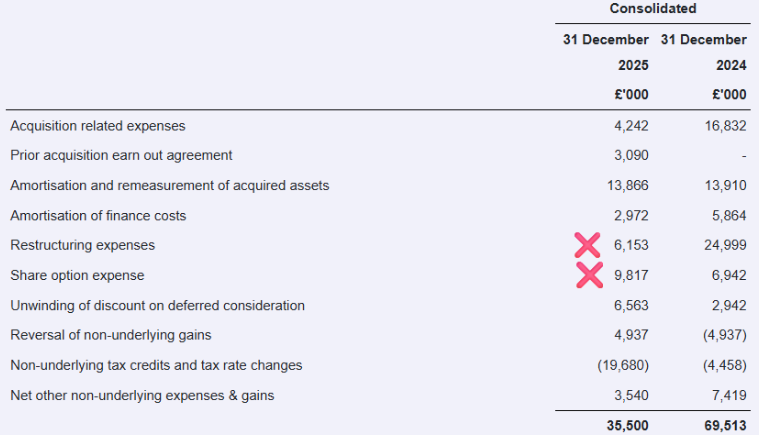

How clean are these results?

There’s a pretty large gap between adjusted PBT (£154m) and actual PBT (£99m).

The company explains the difference with £35m of non-underlying items (after tax) along with £20m of non-underlying tax movements. It’s not how I’m used to seeing non-underlying items presented, but fair enough.

It’s a long list of adjustments, and it doesn’t fill me with confidence. At least the adjustments are lighter than the previous year:

I’ve put an X beside “restructuring expenses” and “share option expense”, as they are two categories I generally don’t allow to be adjusted out.

Most of the others are directly to do with acquisition activity, and are more of a judgement call.

I’m going to rate these results as not clean and I’m inclined to use a number closer to the unadjusted £99m figure than the adjusted PBT of £154m.

Balance sheet has net assets of £857m, or £376m excluding intangibles.

This is a very heavy business with £1.3 billion of PPE. I’m sure the company’s bankers must have good security over these assets.

Graham’s view

Checking my comments in September 2025, I see that I was saying many of the same things back then. I had concerns around debt, adjustments to the accounts, and declining underlying revenue.

The market cap hasn’t changed in the past six months, and I think a neutral stance continues to make good sense.

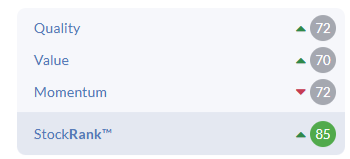

The StockRanks are much more enthusiastic, calling it a Super Stock.

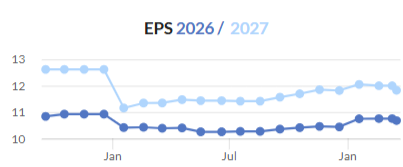

I’ll say one more thing in its favour: EPS estimates have been reassuringly stable or rising over the past year:

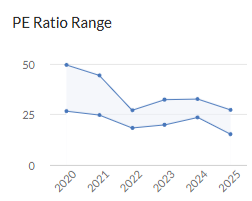

But at an earnings multiple of >10x, considering the heavy and cyclical nature of the business, the adjustments used, and the debt load, I consider it fairly valued here.

Roland's Section

Softcat (LON:SCT)

Up 8% at 1.248p (£2.45bn) - Half-Year Report - Roland - AMBER/GREEN =

Outlook: We now expect high single-digit growth in underlying operating profit in FY2026, up from low single-digit previously.

Investors have progressively shunned this IT reseller and solution provider since last summer, despite a stable earnings outlook and positive trading commentary:

The resulting de-rating of the shares has left Softcat looking cheaper than it’s been for some years:

Today’s half-year results include an upgrade to full-year guidance. Given the stock’s more modest valuation, I’m interested to see if I can justify ignoring Softcat’s Falling Star styling and taking a positive view.

H1 results summary

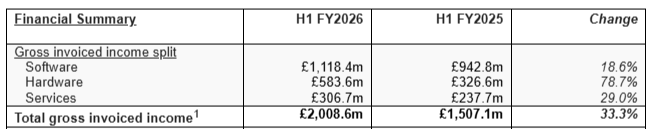

Today’s results cover the six months to 31 January – Softcat has an unusual 31 July year end. Today’s figures show strong growth in sales and profits, which the company says “reflects strong, broad-based performance and the contribution from larger solutions projects, together with a pull forward of some customer orders due to memory shortages.”

Gross invoiced income up 33.3% to £2,008.6m.

Revenue up 53.5% to £837.5m.

Gross profit up 22.6% to £269.9m.

Underlying operating profit up 27.3% to £93.8m.

Underlying earnings per share up 25.8% to 36.1p.

Net cash of £206m (H1 25: £141m).

Interim dividend up 11.2% to 9.9p per share.

Softcat (and others in this sector) report Gross Invoiced Income in addition to revenue, usually with a large gap between the two. Briefly, this reflects IFRS accounting rules relating to revenue recognition, which varies depending on whether the company is the principal or agent in the transaction.

Agent transactions are mainly software, which of course is no longer physically shipped anymore – companies such as Softcat simply act as licenced partners, selling solutions on behalf of giants such as Microsoft.

The nature of the business means that the mix of principal and agent transactions constantly evolves. Gross Invoiced Income is used to provide a consistent measure of total business value transacted and correlates closely with cash received.

The logical pairing with this measure is Gross Profit, which provides a consistent measure of total income received after pass-through product/service costs.

In this case we can see that Softcat’s gross margin fell by 1.2% to 13.4% during the half year, while its underlying operating fell by 0.2% to 4.7%.

The most likely reason for this decline in margins is the 79% growth in hardware sales. This was “driven by datacentre and networking infrastructure, server and compute sales” – in other words, much of this was demand for AI capacity.

Hardware is high value but typically lower margin than software and services, where growth was lower and focused on security and partner-delivered services (such as AI):

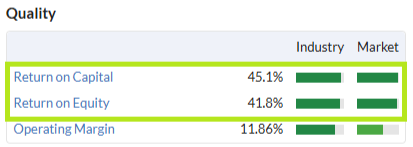

Super profitability: while margins are low in this business, the group’s ability to operate with minimal capital means it generates very high returns on capital and equity:

Today’s results are consistent with these FY25 figures. Softcat achieves this primarily by benefiting from long payment terms from suppliers – effectively free debt – and running a rather large balance sheet.

For example, today’s results show capital employed of only £334m and net assets (equity) of £286m.

These relatively small numbers are dwarfed by trade payables of £582m and cost of sales of £567m. While payment terms will vary, these figures suggest that on average Softcat may take more than six months to pay its suppliers.

In contrast, receivables of £781m are much lower than gross invoiced income of £2,008.6m, suggesting customers pay Softcat far more quickly.

This approach is a core part of the business model and explains why Softcat (and others) maintain strong net cash balances for liquidity.

While this approach isn’t without risk, when it’s well managed, it can be hugely profitable and cash generative.

Operational performance: new customer acquisition rose to 3.5% during the year, compared to 1.6% for FY25. However, the amount of profit generated by each customer rose quite sharply:

Customer base expanded by 3.5% to 10.4k

Gross Profit per customer up 19% to £52.2k

Commentary from CEO Graham Charlton makes it clear that this increased spending reflects customers splurging on AI infrastructure:

AI is reshaping customer priorities at pace, and organisations of all sizes are now prioritising the building of the data, infrastructure and security foundations needed to deploy it effectively and at scale.

Higher spending also pushed more customers into Softcat’s higher loyalty category of those who contribute over £1k of gross profit per year. This group rose by 5.7% to 8.5k, with average gross profit rising by 16.5% to £64k.

The low value of these average gross profit figures highlights the group’s continued strength at the smaller end of the market:

Growth opportunity: the company estimates that it serves approximately 20% of the customers in its target market in the UK, with an average share of wallet of 20% to 25%. On this basis, management believes the business still has a considerable growth opportunity.

Outlook & Updated Guidance

Underlying operating profit growth in the first six months of the financial year is ahead of the Board's expectations, reflecting strong underlying business performance augmented by pull forward of some customer orders due to memory shortages.

Momentum is said to be strong heading into H2, but the company does warn that it faces tougher comparatives due to a strong H2 in FY25. The impact of memory shortages also remains uncertain.

Despite these potential headwinds, profit guidance for the full year is upgraded today:

Softcat now expects “high single-digit growth in underlying operating profit in FY2026, up from low single-digit previously”.

I don’t have access to updated broker forecasts today, but checking back to last year’s results I can see that FY25 underlying operating profit was £180.1m.

Applying perhaps 7.5% growth to this figure suggests this year’s result could be c.£194m.

Ignoring any adjustments (usually quite modest) and applying similar finance costs and tax rate to last year suggests to me this could drop out to earnings per share of 72-73p, versus consensus of 71.3p currently.

Given that H1 underlying EPS was 36.1p, then this seems to suggest that H2 could be flat or marginally ahead of H1, sequentially.

If my guesstimate is correct, then Softcat shares could be trading on around 17x FY26 earnings after this morning’s gains.

Roland’s view

The picture here is similar to that reported recently by Softcat’s larger peer, Computacenter (disc: I hold CCC). Although Computacenter serves much larger customers, the pattern is the same – a huge increase in hardware spending paired with more modest growth in software and services.

Although this is putting pressure on margins at both companies, the sheer volume and value of the hardware being sold is offsetting this, supporting overall profit growth.

Of course, it remains to be seen how long this momentum will last. Softcat doesn’t disclose an order book figure but today’s upgraded guidance suggests to me management are confident about revenue visibility for the rest of the year.

While the risk of an AI-crash or broader recession is worth considering, my feeling is that the near-term outlook remains fairly positive.

I’ve grown wary about ignoring stocks with Falling Star styling. But the strength of these results does not give me any reason to downgrade Softcat and I don’t think the valuation is unreasonable. I’m going to leave my previous AMBER/GREEN view unchanged today.

Advanced Medical Solutions (LON:AMS)

Up 2% at 201p (£444m) - Unaudited Preliminary Results - Roland - AMBER

We haven’t covered this “world-leading specialist in tissue healing technologies” since September 2024. But after a significant de-rating, I think it’s probably a good time to catch up with progress at one of the AIM market’s larger and higher-quality businesses.

2025 results summary

Today’s headline numbers show strong revenue growth and improved margins for 2025 – a nice combination:

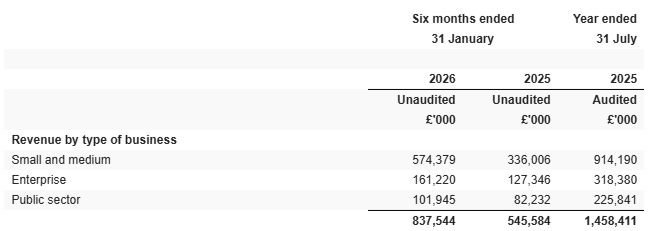

Revenue up 29% to £228.9m

Adjusted pre-tax profit up 15% to £33.9m

Reported pre-tax profit up 81% to £17.8m

Adjusted EPS up 12% to 11.74p

Full-year dividend up 10% to 2.86p per share

Net debt down 10% to £50.5m

Before digging into the accounts in a little more depth, I think it’s worth looking at the trading commentary for last year:

Surgical Business Unit (revenue up 36% to £183.5m, op margin: 14.5%): there was good growth from the company’s LiquiBand products (+10% to £47.8m) and Biosurgical devices (+23% to £23.8m). The Sutures, Clips and VTO business saw revenue rise by 64% to £82.7m, but this was entirely driven by the addition of a full-year contribution from 2024 acquisition Peters Surgical. On a pro forma basis, performance was flat – a situation blamed on normalising distributor inventories post-acquisition.

Woundcare (revenue up 9% to £45.4m, op margin: 6.4%): this division appears to sell bulk materials and own-branded products to customers. It’s a lower value operation but adds volume to the business and has now been restructured to improve profitability.

AMS already sells some products in the US (the world’s largest healthcare market) and is preparing to enter the market with others. I haven’t researched this in any detail but it looks to me like this could create some interesting growth opportunities, perhaps.

Returning to the accounts, I think there are a few points worth noting.

Revenue: organic revenue rose by 10% to £154.8, excluding the £74m contribution from Peters Surgical, which was acquired in mid-2024.

Profit adjustments: adjusted pre-tax profit of £33.9m is almost double the statutory figure of £17.8m. Closer inspection reveals two culprits:

Amortisation of acquired intangibles: £10.3m

Exceptional items: £5.8m

The amortisation charge is non-cash and commonly adjusted out, although it’s worth remembering that it relates to previous cash expenditure on acquisitions.

Exceptionals include £5.2m of integration costs relating to acquisitions plus £660k of restructuring charges (also acquisition related?). In the prior year, the company booked £10.9m of exceptional items, also mostly relating to acquisitions.

Given the company’s apparent practice of making regular acquisitions, I am not inclined to ignore these items, especially as they are mostly likely to be cash costs.

In situations like this I like to compare free cash flow with profit, to see which measure of profit most closely relates to cash generation.

In this case my sums show last year’s free cash flow of £11.3m is a near-perfect match with AMS’s reported net profit of £10.1m for the year.

Inventory increase: I should note that free cash flow would have been significantly higher except for a whopping £13m outflow on inventories during the year. Management says this was necessary to increase inventory cover from 6 months to 7.4 months, “driven by supply chain planning”.

I would guess this increase in inventory should be a one-off outflow. Adjusting for working capital movements gives me a free cash flow estimate of £21m for last year, so on that basis perhaps I can accept the company’s adjusted profits as being representative of underlying performance.

There’s often an element of subjectivity to this kind of analysis – as investors we have to take a view on what we’re looking for and how it should be measured.

Profitability: I like to focus on return on capital rather than solely on margins. AMS does not score very well in this regard.

Using reported operating profit gives me a ROCE estimate of 6.6% for 2025. Even using adjusted operating profit only improves this metric to 8.2%.

Operating margins are respectable at c.10%, so these low returns suggest to me that AMS may have paid quite generous prices for some of its past acquisitions; there’s £113m of goodwill on the balance sheet, nearly half the company’s £260m net asset value.

Debt: net debt excluding lease liabilities was £50.5m at the end of the year. At 5x net profit, this is a little higher than I’d like at first glance.

However, given the group’s overall cash generation and last year’s one-off cash outflows, I think this level of borrowing looks sustainable enough. I would expect to see further deleveraging in 2026, barring any major acquisitions.

Outlook

The Board is confident of delivering full year 2026 revenue and EBITDA in line with current market expectations and believes that AMS is well positioned to drive sustained growth and long-term value creation.

Current market expectations are given as:

Revenue: £245.3m

Adjusted EBITDA: £55.2m

These imply revenue growth of 7% and adj EBITDA growth of 10.6% in 2026, perhaps implying a further improvement in operating margins.

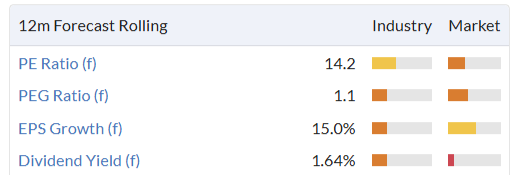

From what I can see these figures are consistent with the consensus estimates in the StockReport, giving us a FY26E adj EPS figure of 13.9p. That’s an 18% increase on today’s equivalent figure of 11.7p.

On that basis, the valuation looks reasonable to me, although not obviously cheap:

Roland’s view

I can potentially see quite a lot to like in this business. I think it’s possible to argue that AMS may now be at the start of a new period of growth and stability, following recent acquisitions and restructuring.

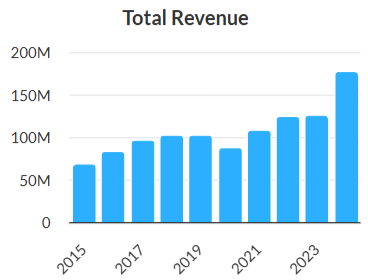

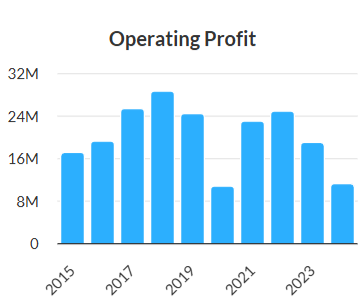

Some improvement is certainly needed, because long-term revenue growth has failed to translate into consistent profit growth. Last year’s operating profit of £22.7m was lower than that reported in 2019:

Another niggle for me is the relatively low profitability of the business, but I think this could improve and am reassured by the strong underlying cash generation.

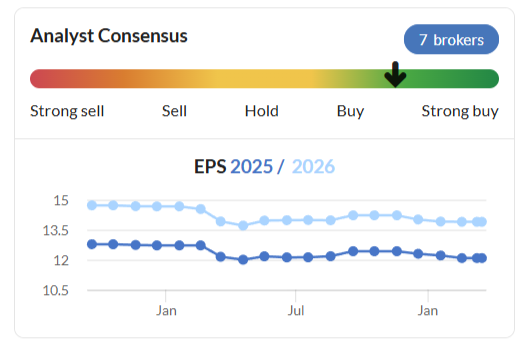

Today’s in-line guidance is reassuring, but the broker forecast trend is indifferent and has edged lower over the last year:

To reflect this initial review and my mixed feelings on the business, I’m going to adopt a neutral view today. If the company does continue to deliver to guidance this year, then I think a more positive stance may be justified over time. I plan to keep an eye on progress here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.