Good morning!

The two big stories of the moment remained in stalemate overnight. President Trump says the Iran ceasefire is “on massive life support”, but the fragile truce remains in place while Pakistan continues to try and broker a deal.

At home, Prime Minister Keir Starmer is still in charge, but seemingly by the slimmest of margins – senior ministers have reportedly suggested he set a departure date.

The UK’s woes are probably more relevant to government bond investors than equity markets. But the Middle East situation continues to have the potential to unleash widespread consequences.

While the accepted wisdom is that markets hate uncertainty, these markets don’t seem too concerned by the current geopolitical situation. The S&P 500 closed up 0.2% at a new record high yesterday, while the FTSE 100 remains within about 6% of the record high seen just before the start of the conflict.

Market futures suggest more of the same today, with oil remaining elevated and markets fairly calm, albeit opening lower:

FTSE 100 expected to open down by 0.6%

S&P 500 expected to open down by 0.2%

Brent Crude at $103.25 a barrel

Gold at $4,715/oz

Update 09:50 - Intertek (LON:ITRK) : latest offer details added to table

All done for today, see in you in the morning.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Vodafone (LON:VOD) (£28bn | SR93) | Total revenue increased 8.0% to €40.5 billion, due to strong service revenue growth and the consolidation of Three UK. Top end of FY26 guidance range achieved. | AMBER/GREEN = (Roland) Today’s results show modest progress on profit and cash generation, but Vodafone CEO Margherita Della Valle still needs to show she can improve the returns on capital generated by this reshaped business. I’m impressed by progress so far and while I don’t think the shares offer the value they once did, the group’s free cash flow performance and forward guidance for c.5% growth suggest to me that the stock could continue to deliver positive returns. | |

Imperial Brands (LON:IMB) (£21bn | SR57) | Tobacco net revenue growth of 1.5% supported by robust tobacco pricing. Adjusted earnings per share up 5.3%. On track to deliver full year results in line with guidance. | ||

| Intertek (LON:ITRK) (£7.7bn | SR57) | Statement re Final Possible Offer & Response to possible offer announcement by EQT | Private equity group EQT has made a final indicative proposal for an offer of £60 per share, plus a final dividend of 107.7p, giving a total of £61.077 per share. This represents a 59% premium to the closing price on 9 April, the last day before EQT’s initial proposal. | TAKEOVER |

IMI (LON:IMI) (£6.7bn | SR80) | First quarter organic revenue was 5% higher year on year. Full year guidance reconfirmed. Continues to expect that full year adjusted basic earnings per share will be between 136p and 142p. | ||

3i Infrastructure (LON:3IN) (£3.4bn | SR85) | Generated a total return of 8.5% for the year ended 31 March 2026, in line with its target. 6.3% increase in the target dividend for FY27 to 14.30 pence per share. | ||

Derwent London (LON:DLN) (£1.9bn | SR57) | Leasing activity this year has been strong with £25.3m completed to date. A further £6.7m is under offer. Making good progress towards its target of £1bn of disposals over three years, with contracts exchanged on £278m of disposals in Q1. | ||

International Workplace (LON:IWG) (£1.8bn | SR26) | Group revenue of $958m, representing growth of 4% year on year. Maintaining FY2026 guidance with adjusted EBITDA range of $585m-$625m, company-owned revenue growth of at least 4%, and recurring managed fee income of $80m. | ||

Greggs (LON:GRG) (£1.6bn | SR72) | Total sales up 7.5% to £800m. 2.5% LFL sales growth in the year to date. 41 gross new shops opened. No change in overall 2026 cost inflation expectations; circa 3% on a LFL basis. Expects good first half profit progress. Board's expectations for the full year outcome remain unchanged. | AMBER = (Ed S) | |

Pantheon International (LON:PIN) (£1.6bn | SR n/a) | Targeted portfolio sale in the secondary market generated net proceeds of £224m at a blended discount to reference date NAV of 8.1%. Majority of the net proceeds to be used for share buybacks to enhance shareholder value and generate liquidity. | ||

Wizz Air Holdings (LON:WIZZ) (£1.1bn | SR59) | Expects to report a breakeven to slightly positive net profit result for the full year ended 31 March 2026. The net income improvement versus previous guidance resulted from stronger underlying revenue and a well-hedged macroeconomic mix. Wizz ended the financial year with a strong liquidity position, reporting a total cash position of €2.1bn. | ||

Bytes Technology (LON:BYIT) (£752m | SR40) | Full-Year Results, Board Change & Share Repurchase Programme | Gross invoiced income (GII) increased 11.5%, with 11.4% growth in software and 24.6% in services. Earnings per share down 6.1%. New £25m share buyback. FY2027 outlook remains consistent with that provided in its FY2026 trading update on 24 March. The company is splitting the CFO and COO roles. | |

Renew Holdings (LON:RNWH) (£725m | SR89) | Group revenue increased 3.5% to £589m. Adjusted operating profit growth of 4.4% to £33.4m. Record Group order book of £945m. Dividend increased 4.9%. | ||

Griffin Mining (LON:GFM) (£553m | SR56) | Revenue in 2025 was $137,496,000, up 1.8%. Generated profit after tax of $22,062,000 (2024: $11,351,000) and basic earnings per share of 12.1 cents (2024: 6.08 cents). | ||

Wickes (LON:WIX) (£467m | SR80) | 1.3% revenue growth for the period. Retail revenues were down 0.4% while Design & Installation revenues were up 6.4%. Remains comfortable with consensus expectations for adjusted PBT for 2026. | ||

Picton Property Income (LON:PCTN) (£376m | SR73) | Schroder Real Estate Investment Trust and LondonMetric have agreed an indicative offer for Picton, where Picton shareholders would receive 0.190 LondonMetric shares and 0.881 SREIT shares per Picton share. This values Picton at 78.2p per share based on yesterday’s closing prices. | TAKEOVER | |

Restore (LON:RST) (£366m | SR57) | Trading remained robust during the period. The Board remains confident that the group will deliver adjusted profit before tax for the full year in line with market expectations. | ||

Marstons (LON:MARS) (£323m | SR89) | Revenue down 1.1% on an underlying basis. Basic EPS up 9.1%. The Board remains confident in delivering full-year market expectations. The World Cup presents a ‘significant opportunity.’ | ||

Norcros (LON:NXR) (£261m | SR95) | Intends to explore options to sell the group’s remaining South African business. This is a separate operating unit which generated revenue of £99.4m and adj op profit of £6.7m for the year ended April 2025. | ||

On Beach group (LON:OTB) (£246m | SR56) | Travelled volumes up 22% to 201.6k, but revenue down 12% and adj pre-tax profit down 72.6% to £2.3m due to “competitive pricing.” Outlook: reinstating guidance, “confident” of delivering adj pre-tax profit of £18-25m. | BLACK (AMBER ↓) (Ed S) | |

Avingtrans (LON:AVG) (£215m | SR77) | The Adaptix Ortho350, a “breakthrough orthopaedic 3D imaging system”, has received CE Certification. This allows commercial sales in the EU and UK. | ||

Andrews Sykes (LON:ASY) (£213m | SR53) | FY25 revenue up 1%, pre-tax profit up 7.7% to £18.1m. “Positive trading momentum experience towards the end of 2025 has continued into the current financial year, with overall performance in the year to date in line with the Board's expectations.” | ||

Seeing Machines (LON:SEE) (£202m | SR19) | Has received a $3.8m order for Guardian Backup-driver Monitoring System from a “leading North American autonomous driving company”. Q4 Guardian revenue to date now exceeds total Q3 Guardian revenue. | ||

Midwich (LON:MIDW) (£173m | SR72) | “... excluding our Middle East business, the Group has performed in line with the Board's expectations in the first quarter” | ||

Strategic Minerals (LON:SML) (£164m | SR39) | CRD042 was completed on 6 May. It intersected a long intersection containing multiple wolframite (tungsten), cassiterite (tin) and chalcopyrite (copper) mineralised structures typical of the SVS deposit (as visually logged and sampled by CRL geologists). | ||

Frontier Developments (LON:FDEV) (£117m | SR95) | Strong sales of JWE3 and other games mean FY26 revenue now expected to be c.£103m with adj op profit of c.£16m, ahead of previous guidance. Over the last month, “delays beyond Frontier’s control have impacted the release of further content for the game [JWE3]”. Management is working to resolve these matters. | GREEN = (Roland) Today’s update includes a c.50% upgrade to FY26 operating profit guidance. Buybacks since February will also provide an 11% boost to future earnings per share. With a net cash balance of £45m, I am confident Frontier still looks cheap. Delays to the release of further JWE3 downloadable content are a concern as they could impact current momentum. I speculate on the possible cause of this below but conclude that this business is still good and cheap enough to allow me to maintain our positive view. | |

Pharos Energy (LON:PHAR) (£111m | SR91) | Production for four months to 30 April was 5,561 boepd, in line with 2026 guidance of 5,200-6,400 boepd. | ||

Macfarlane (LON:MACF) (£103m | SR54) | Full year expectations unchanged. Q1 revenue “marginally ahead” of prior year, with organic growth in both Distribution and Manufacturing. Gross profit in line with expectations but behind prior year. | ||

Kromek (LON:KMK) (£66m | SR97) | The Group expects to report revenues and PBT for FY26 in line with market expectations (consensus: revenue £27.2m, PBT £2.15m). | ||

NWF (LON:NWF) (£64m | SR56) | Stronger performance in fuels due to Middle East conflict means that full-year pre-tax profit is expected to be significantly ahead of market consensus (previously £10.3m). FY27 outlook remains uncertain. | AMBER/GREEN ↑ (Roland) [no section below] Today’s update confirms that fuel trading returned to normal in December after a mild autumn. Profits have since received a further boost thanks to the volatility that’s resulted from the Middle East conflict – such conditions are often profitable for large distributors of fuel. Trading in the Food and Feed divisions is said to be in line, resulting in an overall upgrade to full-year expectations. Unfortunately I don’t have access to any updated forecasts today so I can’t see the scale of this upgrade, but I would guess that use of the word “significantly” suggests an upgrade of perhaps 10%. NWF has been through a difficult patch over the 18 months, with several previous profit warnings. Management warns that the outlook for the year ahead remains uncertain, but with the stock now trading on a P/E of 8 and offering a covered dividend yield of more than 6%, I think it may be fair to move to a moderately positive view. If NWF can return to its historic form, I think this could be an interesting contrarian opportunity. | |

Character (LON:CCT) (£43m | SR67) | Revenue down 8.9%, adj pre-tax profit up 15% to £2.4m & adj EPS up 28.8% to 11.06p. Net assets of £33.4m. Full-year results expected to be significantly ahead of current market expectations. | AMBER = (Roland) Today’s update shows a recovery in profitability at this toy manufacturer, but forecasts remain dependent on sales performance in the key Q4 buying season. With consumer spending under pressure, I think there’s still some risk of disappointment. More broadly, today’s upgraded forecasts do not include any change to revenue guidance, suggesting any return to sales growth next year will be minimal. Given the strength of the balance sheet, it’s possible that I’m being too cautious. But I’m going to leave our neutral view unchanged for a little longer. | |

Corcel (LON:CRCL) (£40m | SR10) | Operational Update, CFO Appointment and Launch of New Corporate Branding | KON-16 exploration well targeted within the next 12 months. Farm-down discussions active “with multiple potential strategic partners”.New seismic confirms key Sirius and Canopus prospects. | |

Angling Direct (LON:ANG) (£36m | SR86) | Revenue up 13.8% with UK LFL sales +11.9%. Adj pre-tax profit up 44% to £2.9m, EPS up 51.9% to 2.81p. Net cash of £10.9m. Outlook: saw a strong start to the year, but trading has softened since the onset of the Middle East conflict and costs have risen. FY27 guidance unchanged at this stage. | ||

XP Factory (LON:XPF) (£28m | SR60) | Revenue up slightly to “more than” £59m, with FY26 adj EBITDA to be “marginally ahead” of market expectations of £5.1m (FY25: £6.6m). FY27 trading has been in line with expectations. | ||

Rua Life Sciences (LON:RUA) (£16m | SR42) | The spinout of subsidiary RUA Structural Heart has been completed, led by Leducq. RSH has raised £7.8m in convertible debt, of which £4.8m came from RUA and £3m from Leducq. RUA retains 100% equity interest but will no longer fund RSH. | ||

Mycelx Technologies (LON:MYX) (£11m | SR27) | A contract for the lease of MYCELX water treatment equipment for offshore operations. The lease has commenced and the contract is expected to contribute c.$850k to FY26 revenue and c.$1.5m on an annual basis. Underpins current FY26 expectations. |

Roland's Section

Frontier Developments (LON:FDEV)

Up 21% at 400p (£142m) - Trading Update - Roland - GREEN =

Today’s update is mostly very positive, with revenue and profit expected to be ahead of expectations following strong sales of Jurassic World Evolution 3, the latest edition of its flagship title:

Revenue of c.£103m (previously “around £100m”)

Adjusted operating profit of c.£16m (previously “around £11m”)

Recent buybacks will also juice upcoming results – c.4m shares have been repurchased since February. This has reduced the share count by 10% and is expected to add 11% to earnings per share.

With a 50% increase to operating profit guidance and the 11% boost from buybacks, I would guess that earnings forecasts could also rise by c.50% after today’s update (with the caveat that the impact of tax credits make this hard for me to accurately model).

Valuation - still too cheap? Frontier’s market cap has risen to c.£140m in early trading this morning, valuing the stock at less than 10x adjusted operating profit.

That looks decent value in itself, in my view – but the group’s £45m net cash position means the stock is potentially much cheaper in cash-adjusted terms.

I think it’s fair to say Frontier shares remain good value after this morning’s update – with the caveat that future earnings visibility is always somewhat uncertain in this sector.

There’s also a second potential issue that has been flagged up today.

Delays with JWE3 new content?

Frontier says that cumulative sales revenue for Jurassic World Evolution 3 is now ahead of Jurassic World Evolution 2 over an equivalent post-launch period. This includes new content released since the launch – an integral part of the video game business model.

That’s obviously good news.

But the company then goes on to report mysterious delays with new JWE3 content over the last month:

In the last month, delays beyond Frontier's control have impacted the release of further content for the game. Frontier is working hard to resolve these matters and return to its planned content roadmap.

This seems a little odd and I think there’s a lack of disclosure here. What factors “beyond Frontier’s control” might prevent it releasing new content? I don’t have time to spend hours trawling Reddit forums and industry websites, so I enlisted AI to help me with this.

With the caveat that the comments below are third-party speculation and may be inaccurate, online comment suggests the delays reported by Frontier today may be related to changes to the scheduling of future Jurassic World films by Universal Studios, which owns the intellectual property.

An announcement about the next film – rumoured to be Jurassic World Liberation – was expected at a major industry convention in April, but this didn’t happen. The suggestion is that Frontier’s next downloadable content may contain material linked to the next film, hence the delay.

Frontier reportedly needs to gain approval from Universal for all content releases, so any rescheduling at Universal would affect Frontier’s release schedule.

It’s also suggested that Frontier’s activity on Steam suggests it does have further downloadable content that’s ready to go when it gets the green light.

Roland’s view

When I reviewed Frontier’s trading update in January, I left our fully positive GREEN view unchanged.

I would do the same today without hesitation, if it wasn’t for the disruption to new content releases mentioned above. I’m finding it hard to gauge how significant this might be.

Given the lack of disclosure, shareholders will have to hope the company can “resolve these matters and return to its planned content roadmap” without losing too much momentum on JWE3.

However, given the reported commercial success of last year’s Jurassic World Rebirth at the box office (which grossed c.$886m worldwide) it seems unlikely to me that Universal will want to hobble this golden goose.

On balance I am going to leave our positive view unchanged today. While I’m a little concerned, I think Frontier is cheap enough to offset the unknown risks posed by current delays to content releases.

The StockRanks also remain highly positive – I’d expect the MomentumRank to benefit from today’s upgrade:

Vodafone (LON:VOD)

Down 4% at 115p (£26.4bn) - FY26 Preliminary Results - Roland - AMBER/GREEN =

I have been a big fan of Vodafone’s turnaround under CEO Margherita Della Valle and I believe last week’s news that the company is taking full ownership of VodafoneThree is positive – it will become the largest mobile provider in the UK, in line with Della Valle’s strategy to focus on markets where Vodafone can be lead.

However, today’s results and guidance suggest to me the shares could be approaching something closer to fair value, after a stonking run that’s seen this former laggard double in 12 months:

Key financial figures from today’s results:

Revenue up 8.0% to €40,461m

Adjusted EBITDAaL up 3.8% to €11,351m

Reported pre-tax profit: €1,864m (FY25: €(1,478)m

Adjusted earnings up 36% to 10.72 euro cents per share

Total dividend up 2.5% to 4.6125 euro cents per share

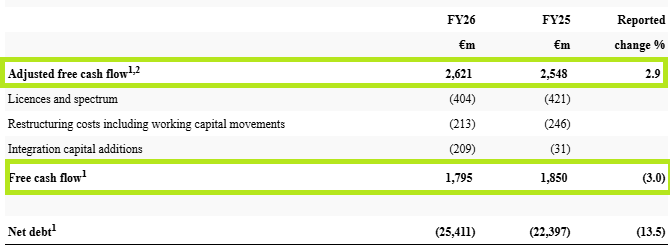

Profits from this business are complicated by all sorts of factors, so I prefer to focus on free cash flow – which to its credit, Vodafone reports quite clearly.

Cash flow: two versions of this figure are provided, adjusted and statutory. For some reason I’ve never understood, adjusted free cash flow excludes spending on licences and spectrum, even though these are absolutely essential to the business:

Source: Vodafone FY26 results

Adjusted FCF is a key guidance metric for the firm and today’s €2.6bn result is at the upper end of guidance for €2.4bn to €2.6bn.

This cash generation gives me the following yields. I see this as more useful than most other valuation metrics for this business:

FY26 adj FCF yield: 8.2%

FY26 reported FCF yield: 5.6%

Profitability: for a mature, capital-intensive business of this type, operating in competitive markets, this level of free cash flow yield seems about right to me. The group’s adjusted EBITDAaL margin fell by 1.1% to 28.1% last year and returns on capital remain stubbornly low:

FY26 return on capital employed: 4.4% (FY25: 4.4%)

I continue to expect this measure to improve as performance continues to recover and the restructured group beds in, but I am not sure how quickly this will happen.

FY27 Outlook: Vodafone has provided FY27 guidance today that suggests steady progress over the coming year:

FY27 adj EBITDAaL: €11.9 to €12.2bn (+5.7% vs FY26 at the midpoint)

FY27 adj free cash flow: €2.6bn to €2.9bn (+4.9% vs FY26 at the midpoint)

As far as I can see, this FY27 EBITDAaL guidance is slightly below previous consensus, while FY27 free cash flow guidance appears to be aligned with consensus.

Assuming earnings estimates for the current year remain largely unchanged suggests to me the shares are trading on a forward P/E of around 13.

Roland’s view

I am pretty certain Vodafone is a better business than it was a few years ago. The group has shed operations in markets where it isn’t the leader and redoubled its efforts in its core markets.

Growth in the group’s Africa division was strong last year, with organic service revenue up 12.9%. As I discussed when reviewing Airtel Africa last week, I think this market continues to offer exciting long-term growth opportunities.

However, performance in the UK (+0.3%) and Germany (-0.2%) highlighted the mature and competitive nature of these markets.

Against this backdrop, I think Ms Della Valle is continuing to do all the right things – notably by taking full control of VodafoneThree. While this will add restructuring costs and additional debt in the short/medium term, I think it opens the door for the company to reap the rewards from the consolidation of the UK market.

At current levels, Vodafone shares offer a 3.5% dividend yield and look fairly priced to me on a near-term view. However, if free cash flow growth can be maintained at c.5%, as guidance suggests, I think the shares could continue to deliver further positive returns, albeit more slowly than over the last year.

I’m going to leave my previous AMBER/GREEN view unchanged today.

Character (LON:CCT)

Up 9% at 269p (£46m) - Half-Year Financial Report - Roland - AMBER =

Graham upgraded our view on this toy manufacturer to neutral in January, highlighting improved profitability despite falling revenues.

Today’s interim results confirm these trends, with half-year earnings equivalent to nearly 100% of previous consensus. This has prompted a big upgrade to FY expectations, with brokers Allenby and Panmure Liberum both issuing upgraded forecasts today.

Let’s take a look.

Results highlights: key figures

Revenue down 9% to £48.3m

Adjusted pre-tax profit up 14.3% to £2.4m

Adjusted earnings up 29% to 11.06p per share

Net cash of £13.7m (FY25: £12.6m)

Interim dividend up 33% to 4p per share

My first port of call with these figures is to understand why profits have risen so much, despite the drop in sales. It turns out there are three elements to this:

Gross margin rose by 2.4% to 31.7%, as the cost of goods sold fell faster than revenue.

However, gross profit still fell slightly, down 1.4% to £15.3m - so we can see that this alone doesn’t explain the rise in pre-tax profit.

Operating costs are the missing element: selling and distribution costs fell by 10% to £3.7m, while administrative expenses were 1.7% lower at £9.4m.

I wonder how much of the reduction in selling and distribution costs reflect a decline in sales volumes. We aren’t told if this is the case.

Improved stock position: it seems that one reason for the improvement in gross margin may be an improved stock position, with less stock needing to be written off or discounted.

However, with the geographical mix, some exciting new additions within our product portfolio, a projected largely clean inventory position at the year-end (reducing the need for significant provisions) and favourable FX rates, we expect to maintain the improved HY26 gross margin for the remainder of this financial year.

Inventories at the end of February stood at £9.7m, down by nearly 25% from £12.7m at the same time in 2025.

Possible £9.8m property sale: Character owns a warehouse property (Infinity House) that was previously empty but has now been leased for five years at a rent of £773,000 per annum.

This arrangement also includes an option for a party connected with the lessee to buy Infinity House for £9.8m in cash. This option will lapse on 30 June 2026, so is perhaps designed to give the lessee time to arrange financing or occupy the property before making a final decision on whether to buy it.

Outlook

The company’s statement is positive but not specific:

Although dependent on achieving forecast trading performance in Q4 (the Group's key trading period in the financial year), the Board currently expects that the Group's profit before tax and highlighted items for the year ending 31 August 2026 will be significantly above current market expectations.

With thanks to brokers Panmure Liberum and Allenby for making updated forecasts available on Research Tree today, we can get a more specific idea of what Character’s management may be expecting:

Previous FY26E adj EPS estimates: 11.3p (PanLib) & 14.0p (Allenby)

New FY26E adj EPS: 22.1p (PanLib) and 22.6p (Allenby)

FY27E adj EPS: 27.6p (PanLib)

These forecasts put Character Group on a FY26E P/E of 12.

Additionally, both brokers consider that if the Infinity House property is sold, the £9.8m would be considered surplus cash and likely returned to shareholders. Based on the current £46m market cap, that could equate to c.20% of the current share price, depending on any tax liabilities.

Roland’s view

Momentum has been very weak here for a long time:

I think it’s too soon to know whether today’s update marks a genuine turning point, but it’s definitely possible.

The improved profitability of the business is certainly important, but there’s not yet much evidence of any return to sales growth – another key element to a sustainable re-rating.

Brokers’ revenue forecasts remain unchanged today, suggesting revenue will fall by c.20% to £100m in FY26, before returning to very modest growth at £103m in FY27.

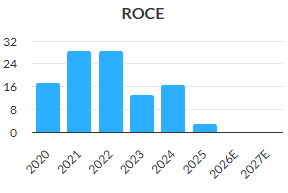

Character Group has delivered attractive returns on capital in the past and my sums suggest we could see ROCE return to c.20% in FY26, at least on an adjusted basis:

Optimistically, today’s upgrade might justify us switching to a more positive view, especially given the potential for a windfall if the property sale goes ahead.

However, I am not entirely convinced. I would argue that a P/E of 12 is probably fair for a low-margin toy manufacturer – especially as we don’t yet know if sales will meet targets during the key Q4 buying period (presumably when retailers order Christmas stock).

Given prevailing macro conditions and pressure on consumer incomes, there is perhaps a risk that retailers will order slightly less than anticipated if the Middle East conflict isn’t resolved soon.

I am going to err on the side of caution and leave our neutral view unchanged today, but I’d certainly be open to upgrading my view on any further positive news.

Ed S's Section

Greggs (LON:GRG)

Up 5% at 1,598p (market cap of £1.65bn) – Trading Update – Ed S – AMBER=

Greggs has posted a trading update for the first 19 weeks of 2026. And the numbers are relatively encouraging:

Total sales up 7.5% to £800 million

2.5% LFL sales growth in the year to date, 3.3% in the most recent 10 weeks

41 gross new shops opened, 20 net openings, 2,759 shops now trading

The company says that partnerships with franchisees and grocery retailers are progressing well and contributing to the growth in overall sales.

Looking ahead:

The Board's expectations for the full year outcome remain unchanged

There is no change in overall 2026 cost inflation expectations; circa 3% on a LFL basis

It expects good first-half profit progress with incremental operating costs from its new Derby site primarily impacting the second half as previously guided

It continues to target around 120 net openings for the full year

LFL sales performance has improved against what remains a challenging market, with good operational cost control supporting encouraging year-on-year profit progress in the year to date.

In terms of the Middle East conflict/oil prices, it says:

Our forward buying of key commodities continues to provide protection against increased inflation in the near term; we have forward purchase agreements in place representing circa five months of cover for our food and packaging needs and 85% of our 2026 energy and fuel requirements are fixed in price. In addition, circa 50% of our 2027 energy and fuel requirements are fixed.

We are monitoring the situation in the Middle East and should the conflict continue and become prolonged we, like all food retailers, will likely see higher overall cost inflation through the end of 2026 and into 2027.

On its expansion:

In the coming weeks we will open our first shop in an airport outside the UK, working in partnership with leading global travel operator Lagardère Travel Retail at Tenerife South Airport. Tenerife South is a destination for millions of UK and international passengers each year and represents an excellent opportunity to test our offering in an international travel hub.

Ed S’s view:

Back in March, Roland gave Greggs an AMBER rating and I’m going to keep the stock at that rating for now because it's a tricky one.

On one hand, we have a well-established company with a strong, trusted brand and a high return on capital employed (ROCE) that is trading on a very reasonable P/E ratio (approx. 13 looking at analysts’ EPS forecasts for 2026), and offering an attractive dividend yield (approx. 4.3% on a trailing basis). We also have a company that is actively enhancing its menu with healthier options to appeal to more consumers, and continuing to expand (and experimenting with international expansion).

On the other hand, we have a business that is vulnerable to both weak levels of consumer spending in the UK, the rise of GLP-1 weight-loss drugs (about 7% of the UK population have used these drugs), and potentially cost inflation if the Middle East conflict continues. We also have a stock that looks weak technically.

On the GLP-1 issue, Jefferies downgraded the stock earlier this year to Hold from Buy (and cut its price target to 1,610p) due to uncertainty here. "We are increasingly of the view that the rapid uptake of GLP-1 weight‑loss drugs is impacting Greggs," wrote analyst Andrew Wade, who noted that Greggs’ higher‑frequency consumers could be affected.

One other issue on the negative side is the high level of short interest here. Looking at FCA data on shorttracker, short interest is 10.7% with 11 funds short the name. To me, that’s a red flag – hedge funds clearly expect performance to deteriorate (potentially due to the GLP-1 issue).

So, while I’m encouraged by the solid LFL sales growth announced in today’s update (especially the 3.3% growth in the most recent 10 weeks), I’m going to keep the stock on AMBER for now. To upgrade it, I’d want to see sustained operational momentum.

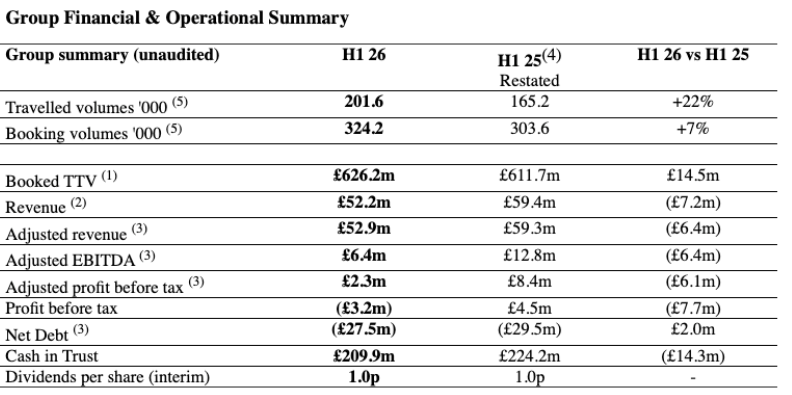

On Beach group (LON:OTB)

Down 16% at 142p (market cap of £205m) – Trading Update – Ed S – BLACK (AMBER ↓)

On the Beach Group has posted its interim results for the six-month period ended 31 March 2026. And investors are clearly unimpressed, with the stock down 16% as I write. Let’s take a look at what’s going on.

Financial summary:

Record H1 booking volumes of 324k, growing by +7% and significantly ahead of the market, with TTV +2% despite significant industry headwinds

Adjusted revenue of £52.9m (down £6.4m) due to widespread demand disruption from the conflict in the Middle East since 1 March

Adjusted EBITDA of £6.4m (H1 25: £12.8m) and adjusted PBT of £2.3m (H1 25: £8.4m)

Strong balance sheet and an asset light, profitable, cash generative operating model, with £88m of headroom and £209.9m in the customer trust account

Net debt decreased by £2.0m, while the company continued to return capital to shareholders – c.£33m capital committed to buying shares and paying dividends in the period

The Board is confident in the group's prospects and is declaring an interim dividend of 1.0p, in line with prior year.

Strategic highlights:

Customer search funnel conversion is +24%

App monthly active users are +29%

App booking mix now represents 38% of all bookings

In year repeat bookings +24%

2 year repeat rates +17%

Booked volumes +7% and travelled volumes +22%, vs total market (ATOL) +3%

Exceptional items:

Exceptional items total £2.6m in H1 26 (H1 25: £0.9m). This comprises £0.7m of booking cancellations arising from the Middle East conflict; and £1.9m of other costs (H1 25: £1.0m), of which £1.5m relates to the restructuring programme, with the balance representing legal and professional fees and share repurchase costs. Exceptional recoveries of £0.1m in H1 25 related to refunds from airlines for cancelled flights from previous periods.

Current trading and outlook:

OTB continues to trade profitably and generate cash.

Although demand remains more subdued as a result of the conflict in the Middle East, booking activity has stabilised to a more consistent trading pattern since the half year.

Bookings over the last 6 weeks since H1 26 are +9% as we approach the key Summer departure months.

Despite the current geopolitical uncertainty and a challenging consumer environment, the Board is reinstating FY guidance and is confident in delivering Adjusted PBT in the range of £18m-£25m.

The significant strategic progress made during the period further underpins OTB's prospects for the medium term.

Management commentary:

Whilst the Group has limited exposure to destinations in the Middle East, the ongoing conflict has impacted consumer demand since 1 March and led the Group to withdraw its guidance, as announced in the AGM Trading Update. H2 booking activity has stabilised to a more consistent trading pattern and bookings over the last 6 weeks are up 9% as we approach the key Summer departure months. As a result, we have today reinstated guidance and the Board is confident in delivering FY26 Adjusted PBT in the range of £18m to £25m."

Ed S’s view:

I think the main driver of today’s share price fall is the full-year guidance.

Back in December, the company said that it was confident in delivering FY26 Adjusted PBT in the range of £39m-£43m. In March, it suspended its guidance due to the Middle East conflict.

Today, it has come back with new guidance of Adjusted PBT in the range of £18m-£25m. So, that is obviously a major drop from the pre-conflict guidance.

I’ll point out that a Reuters article says that a company-compiled poll had analysts' estimates at £38.5m-£42m.

There’s also the fact that H1 profitability is down significantly year on year (-£3.2m versus £4.5m in H1 last year) despite the fact that the Middle East conflict only kicked off in the final month of the period. It notes here:

As well as creating a volume headwind, the change in mix arising from the conflict has also impacted margin as higher value, higher margin, longer lead time summer bookings, particularly to eastbound destinations, have been deferred as customers adopt a 'wait and see' approach.

Is there rebound potential here? Potentially.

There are definitely things to like about this business:

Loyalty towards OTB continues to grow with in-year repeat bookings up 24% and 2-year repeat rates up 17% in the period. Note that on Trustpilot, the company has a 4.1 rating, which is solid.

OTB has an asset-light business model and is independent of airlines and hotels, meaning that it has more flexibility than any standalone tour operator, airline, or hotel chain and can pivot or expand quickly depending on demand and opportunities.

Technology investment has enabled many manual operational processes to be automated. 98% of bookings are now automated (vs 60% in FY22).

AI adoption is scaling across the organisation. Its chatbot is currently resolving booking, flight, and transfer & payment queries, and agentic AI has been deployed across engineering, supply, operations and customer service, improving productivity, quality, reducing time to market and risk exposure. Note that on 24 March, OTB's app was launched on ChatGPT. This has created a new acquisition channel. An integration with Anthropic is currently in progress and it is planning integrations with further LLMs in H2.

The company is seeing strong growth in key strategic expansion areas (City trips and Republic of Ireland bookings). It also says that it’s poised to take share in the large, high growth Cruise market.

Bookings have picked up since the end of the H1 period.

On the downside:

We don’t know how long the Middle East conflict will continue for so there is uncertainty here. If oil prices remain high, they could squeeze consumer spending. High oil prices could also push flight prices up, reducing demand.

While the company is using AI effectively, the technology could also be a risk. If it wipes out a lot of white collar jobs in the years ahead, the travel industry could be badly impacted.

The company’s performance has been patchy in the recent past. In September, the stock tanked after the company posted lower-than-expected guidance.

The chart doesn’t look good. We have a strong downward trend.

Weighing up the bull case versus the bear case, I’m going to give OTB an AMBER rating. I do see potential for a rebound if the backdrop improves but I also see a few risks that can’t be ignored.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.