Good morning!

Prime Minister Starmer is still in Number 10 despite the resignation of four ministers yesterday. He has said he won’t stand down unless someone launches a formal leadership challenge. The yield on 10-year UK gilts has now topped 5%, while 30-year gilts are at almost 5.8% – the highest level since 1998.

Across the Atlantic, US inflation rose to 3.8% in April, from just 2.4% in February, prior to the start of the Iran conflict. The increase has been driven by a c.25% increase in petrol prices. This squeeze on consumer spending will add to pressure on President Trump ahead of this year’s mid-term elections. Inflation is expected to spill over into higher prices for food and other goods and services in the coming months.

Trump will shortly arrive in China where he’s expected to discuss China’s support for Iran, in addition to a range of trade issues. More controversially, US arms sales to Taiwan are said to be on the agenda; China would like these to cease. He will be joined by Nvidia boss Jensen Huang in China, suggesting AI will also be on the agenda.

Also on AI, Claude maker Anthropic is reported to be in discussions to raise $30bn at a valuation of $900bn, according to Bloomberg.

Here in the UK we don’t have any $900bn companies, but we do have some more affordable ways to play the AI theme, as Gareth discussed in his latest article on Friday.

FTSE 100 expected to open up 0.6%

S&P 500 expected to open up 0.2%

Brent Crude is trading at $104 a barrel

Gold at $4,703/oz

Update 10:18: added Intertek's response to the latest offer from EQT to the table.

Today's report is now complete. See you in the morning!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| Intertek (LON:ITRK) (£8.2bn | SR59) | Statement re final proposal from EQT | “… the Board of Intertek considers that the financial terms of the Final Proposal [£60 per share + dividend] deliver value in cash to Intertek shareholders at a level which it would be minded to recommend to Intertek shareholders” | PINK (Roland - I hold) [no section below] It looks like Intertek is now likely to accept private equity group EQT’s offer, assuming it is made firm. As a shareholder I’m not unhappy. While I think the long-term value of the business could be greater, £60 seems fair to me and offers certainty versus the execution risk of the company’s own plan to spin-off or sell its lower-margin energy-focused business. |

Spirax (LON:SPX) (£5.29bn | SR73) | Delivering organic growth ahead of industrial production, with margin progression. Full-year guidance unchanged for mid-single digit organic revenue growth. | ||

Babcock International (LON:BAB) (£4.94bn | SR34) | FY26 revenue up 9%, with underlying earnings down 21% to 39.6p due to a £140m charge relating to rework costs for the Type 31 frigate contract. FY27 expectations are unchanged. | AMBER ↓ (Roland) Today’s update reveals a surprise £140m cost overrun on a large project to build five Type 31 frigates for the Royal Navy. Babcock has booked the accounting charge in FY26 but expects cash outflows over the remainder of the contract. While this doesn’t necessarily detract from the positive macro environment for defence businesses, it is a useful reminder of the kind of pitfalls large contractors like Babcock can face. While FY27 guidance is unchanged today, Babcock’s order book fell last year and consensus figures suggest earnings growth will slow this year. The valuation looks up with events to me and I note the StockRank has been falling steadily for months. I’m downgrading our view by one notch to neutral. | |

TP Icap (LON:TCAP) (£2.3bn | SR96) | Record Q1, with revenue up 13% led by Global Broking (+15%) and Energy & Commodities (+13%). Remains comfortable with the outlook for the remainder of the year. | GREEN = (Roland - I hold) It’s no surprise to see that this broking group had a strong Q1 – by design, it’s built to benefit from volatility and heightened market activity. Full-year guidance is unchanged today which is perhaps slightly disappointing, but current forecasts look undemanding to me and I think the risk is probably to the upside. One possible joker in the pack is the group’s high cost base, which I discuss below. However, with a single-digit P/E and near-6% dividend yield, I think the valuation and outlook are attractive and am happy to maintain our positive view. | |

Resolute Mining (LON:RSG) (£1.57bn | SR67) | Study confirms ABC’s “strong economic potential” and “pathway” to become Resolute’s second gold mine in Côte d'Ivoire, with expected gold production of c.141 koz/yr over a 12-year mine life at an AISC of $1,614/oz. NPV (5%) of $1.2bn, capital cost estimate of $648m. | ||

| Savills (LON:SVS) (£1.22bn | SR89) | AGM Statement | Trading for the year to date has been “marginally ahead of the Board’s expectations”, despite the impact of geopolitical volatility. 2026 expectations remain unchanged. | |

Vistry (LON:VTY) (£1.04bn | SR78) | Year-to-date sales rate is 32% higher than last year as Vistry takes action to generate cash, but increased use of discounting and incentives means H1 profit will now be lower than expected and “significantly lower” than last year. H2 profit is expected to be in line with the prior year. Vistry remains committed to the Partnerships model. The new CEO is leading a review of the business and will report by 24 Sept 26. | BLACK/AMBER/RED ↓ (Mark- I hold) While the company says that Adj. PBT will be in line with the middle of the range of analysts expectations, there is a huge variation in these. It is clear that "significantly lower” in H1 and similar H2 performance to last year add up to lower figures overall. There are some signs that the company is being put under financial strain by delays in completions, and the need to offer increased incentives. Average net debt is higher in H1, but expected to be significantly lower in H2. I have reduced our view today to reflect these near-term risks. However, this is a rather unique situation, where a significant proportion of the equity has been sold short into this update. If the company doesn’t report any further bad news in the next few months, and net debt does start to reduce, then there may be significant buying pressure from those shorts closing. After all, the discount to TBV would remain even with a large haircut to land values. | |

Gamma Communications (LON:GAMA) (£810m | SR55) | Good start to FY26, with full-year expectations unchanged. Strategic review: Gamma says it is in discussions with various parties and confirms press speculation that it is in talks with Providence Equity Partners about a possible offer. | PINK (AMBER/GREEN ↑) (Roland) Gamma’s trading faces various near-term headwinds, but these have previously been flagged and guidance for this year is unchanged. Management reports positive progress in the core UK and German markets and confirms that preliminary talks with possible bidders are ongoing. With a trailing free cash flow yield of 7% and single-digit P/E, I think Gamma is likely to offer medium-term value, so I’m upgrading my view by one notch today. | |

Conduit Holdings (LON:CRE) (£693m | SR87) | “Solid start to 2026”, with gross written premiums +4.9% and reinsurance revenue +12.8%. However, overall portfolio risk-adjusted rate change was -5% in Q1, net of claims inflation. Approved new $50m buyback. | ||

Thor Explorations (LON:THX) (£500m | SR100) | First set of drilling results from Douta following completion of PFS earlier this year “confirm expanding gold footprint” at Douta. | ||

Avon Technologies (LON:AVON) (£486m | SR30) | Revenue up 6.8%, but closing order book down 11.4% due to a 31.6% fall in order intake. This is said to be due to timing of US DoW orders and weakness in US commercial helmet demand. H1 adj pre-tax profit up 47% to $21.8m. Firmly on track to meet or exceed FY26 guidance. | AMBER/RED ↓ (Mark) | |

Guardian Metal Resources (LON:GMET) (£393m | SR26) | Guardian Metal is evaluating the potential of recovering tungsten and other metals from the historic tailings at Tempiute, with a view to provide an opportunity for near-term, domestically sourced tungsten in the U.S. These tailings cover c.550 acres and GMET has expanded its mineral rights position to cover the full tailings footprint. Drilling planned for June 2026. | ||

Marshalls (LON:MSLH) (£318m | SR75) | Trading was in line for the four months to 30 April, with revenue down 1% at £205m. Full-year expectations are unchanged. | ||

Public Policy Holding (LON:PPHC) (£286m | SR22) | Revenue up 27.5%, with +5.1% organic growth. Adj net income up 100% to $7.4m, with adj EPS up 74.5% to $0.25. Net debt reduced to $1.8m following January capital raise and US IPO. 2026 guidance: revenue $205-209m, adj EBITDA $46-48m. | ||

Vertu Motors (LON:VTU) (£205m | SR92) | Revenue -1.5% to £4.83bn, Adj. PBT -16% to £24.5m, Adj. EPS -13% to 5.71p, Net debt £61.3m (FY25: £66.6m), FY dividend flat at 2.05p. Outlook: Strong start to FY27, trading profit for March and April 2026 was ahead of the prior year. | AMBER ↓ (Mark) There is nothing wrong with these results, indeed they are slightly higher than forecast (if you accept the ongoing adjustments). However, the share price is now higher than when we reviewed this last, meaning that a forward P/E of 11 doesn’t look particularly great value for a company exposed to worrying consumer confidence trends. Hence I am moderating our view. There is still a discount to TBV, which is mainly supported by freehold property. However, with little sign that these assets can be made productive any time soon, and alternative uses such as property land sales looking shaky, this type of play is only for the very patient. | |

| Afentra (LON:AET) (£170m | SR97) | FY25 Annual Results and Corporate Update | Strategic review: continuing as an independent company. Results: 2025 WI production 6,324 bopd, Revenue -37% to $114.4m, EBITDAX -43% to $51.7m, LBT $3.2m (2024: PBT £52.4m). Refinancing: secured a refinancing of its debt facilities through the entry into a $125 million Pre-Payment Facility at SOFR +6%. | |

Inspecs (LON:SPEC) (£84.9m | SR79) | Revenue -1% to £191.7m, Adj. EBITDA -9% to £17.7m, Op. Profit -3% to £5.7m, Net debt excl. Leases £32.3m (FY24: £22.9m). “….the Group is on track to deliver Board expectations for 2026.” | PINK | |

Orosur Mining (LON:OMI) (£79m | SR12) | Ongoing drilling at Pepas West continues to show positive results, including 23m at 2.98 g/t. | ||

Arrow Exploration (LON:AXL) (£62.5m | SR62) | The Icaco 1 exploration well reached target depth on May 9, and encountered multiple hydrocarbon-bearing intervals. Plans to production test over the coming weeks. | ||

Enwell Energy (LON:ENW) (£44.1m | SR86) | Aggregate average daily production of 1,865 boepd (2024: 2,288 boepd) when in production. Aggregate production volumes of 49 kboe (2024: 722 kboe). Revenue -92% to $3.3m due to license suspensions. Net Loss $4.5m (2024: $23.7m profit). Cash $97.1m (2024: $99.4m). “...continuing to pursue legal proceedings to challenge the suspension orders and protect its business and assets…” | ||

Getbusy (LON:GETB) (£35.7m | SR27) | April ARR +11% to £23.4m. “...the Board reconfirms its expectations for 2026 with a high degree of confidence.” | ||

KRM22 (LON:KRM) (£18.7m | SR8) | ARR +15% to £7.6m. Revenue +10% to £7.4m. Adj. EBITDA -20% to £0.8m. LBT £2.1m (FY24: £1.4m LBT). Net Cash £5.2m (FY24: Net debt £3.5m) following £9.2m fundraise in period. | BLACK | |

Kelso group (LON:KLSO) (£13.7m | SR38) | Intention to raise new funds equal to 5% of its issued share capital at a placing price of 3.0 pence per share, equivalent to c.£650,000. 3% discount to last night’s close. | ||

Panther Metals (LON:PALM) (£10.7m | SR21) | Sixth and final batch of Vibracore sample assay results for the Winston Tailings Project continue to show good grade consistency across the vertical depth-profile and laterally between Vibracore hole collar locations, and support or exceed the previous batches. |

Roland's Section

TP Icap (LON:TCAP)

Up 0.5% at 316p (£2.3bn) - Trading Statement - Roland - GREEN =

(At the time of writing, Roland has a long position in TCAP.)

This interdealer broker group sits as the middle man between buyers and sellers in many key markets globally, notably interest rates, FX and energy commodities. As Gareth highlighted in this recent article, this business gets paid based on activity rather than the outcome of the underlying investments – so it’s designed to benefit from volatility and heightened market activity.

TP ICAP’s management provides evidence of this in this morning’s AGM Update:

Q1 revenue rose by 13% to £689m, a new record

Global Broking revenue: +15%

Energy & Commodities revenue: +13%

Liquidnet (an off-exchange trading venue) revenue: +9%

The company also provides an update on its proprietary OTC data analytics business, Parameta Solutions:

At Parameta Solutions, recently added sales reps are beginning to contribute and the business remains focused on buy-side engagement, new logos, upsell and retention, with Q1 revenue +4 per cent.

Parameta is a high margin (c.40%), recurring revenue business that’s seen as undervalued within TP ICAP’s portfolio. It was previously being prepared for a US IPO, but that seems to be on hold currently. The company says this delay is due to market conditions, but I can’t help wondering if sluggish revenue growth (+5% in 2025) may have contributed to this decision – perhaps investors were deterred by the apparent lack of momentum.

I’m pleased to see TP ICAP is now taking Parameta’s growth more seriously and investing in the business.

Outlook

Management is confident:

As market leaders we are well-positioned to continue to support our clients with highly trusted, reliable execution, and insight as they manage their risk during the continuing macroeconomic and geopolitical uncertainty.

But there’s no change to guidance at this relatively early point in the year:

The Board remains comfortable with the outlook for the remainder of the year at current FX rates.

Forecasts from Cavendish are unchanged today, but the broker says it will review its forecasts on the back of this morning’s announcement.

The StockReport shows a slightly negative trend to consensus estimates in recent weeks, but I would not expect any further downgrade following today’s update:

Roland’s view

Broker consensus prior to today was for revenue growth of just 2.3% in 2026. While there’s still more than half the year remaining, it seems hard to imagine that TP ICAP will underperform this target after such a strong start to the year. After all, I would imagine that strong trading has continued into Q2, which is now 50% complete.

Likewise, consensus earnings forecasts for 33.6p per share would represent a flat performance on last year’s adjusted EPS of 33.5p. Against the macro backdrop, I’d consider this a disappointing result for 2026.

The joker in the pack of course is that costs could rise, both in terms of remuneration and broader overheads. This is, by its nature, a high remuneration business.

Brokers are paid a profit share and broker compensation rose by 6% to £1,068m in 2025. This contributed to total employee compensation and benefit costs of £1,485m last year – 63% of revenue.

Today’s update mentions “strict cost discipline”, but the company has also previously reported recruitment challenges in Energy & Commodities. I imagine that overcoming these challenges to implement “a successful hiring programme” in H2 2025 may have involved providing improved compensation packages.

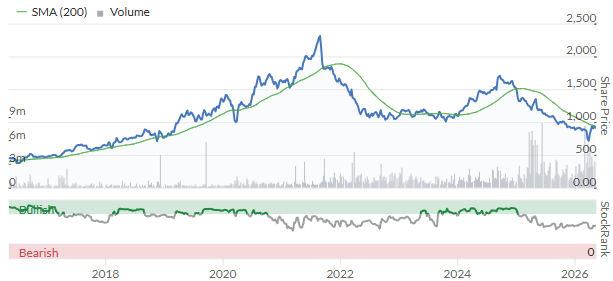

TP ICAP has not been a great long-term compounder, but the stock has performed very well since the start of the war in Ukraine:

Profitability has also started to improve, with (unadjusted) operating margins returning to double digits. Return on equity remains underwhelming, though:

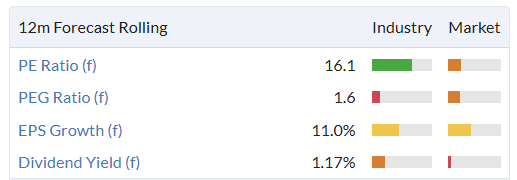

The good news is that – in my view – all of this is already in the price. The shares trade on a single-digit P/E with a 5.7% dividend yield:

The StockRanks view this as a Super Stock and I agree that the valuation and investment case look appealing at current levels.

TP ICAP is currently a member of my SIF portfolio. Personally, I’m happy to hold the shares, which I see as a hedge against volatility and the uncertain macro outlook.

I’m going to leave Graham’s previous positive view unchanged today.

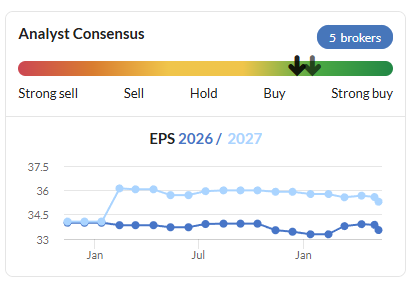

Gamma Communications (LON:GAMA)

Up 5.5% at 943p (£853m) - AGM Trading Update & Response to Speculation - Roland - PINK (AMBER/GREEN ↑)

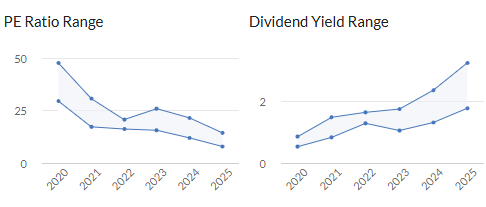

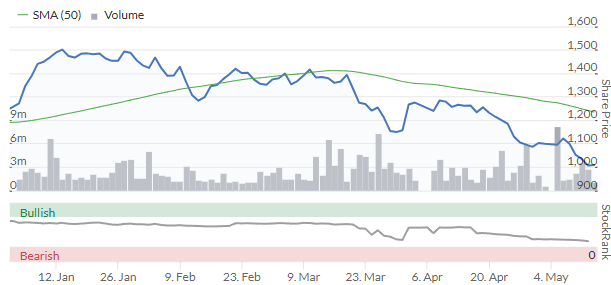

This business communications technology provider has de-rated sharply over the last five years:

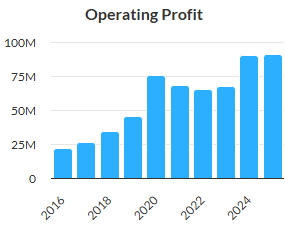

The shares are now trading at seven-year lows, even though operating profit has doubled over the same period:

As far as I can see, this stock is now trading more cheaply (on a P/E basis) than at any time since Gamma’s 2014 IPO.

While the valuation may have overheated at times in the past, I’m not convinced the current single-digit P/E is a fair reflection of the value of this business, despite ongoing headwinds in the UK due to the switch from copper telephone lines to (lower margin) digital services.

Management appears to agree and has perhaps run out of patience for convincing public markets of the group’s value. In March, Gamma confirmed reports that it was in preliminary sale discussions with “a number of interested counterparties”.

Sales talks ongoing: Today, the company has confirmed that preliminary discussions are ongoing and identified one possible bidder as Providence Equity Partners, a US private equity firm with a specialist focus on media and communications.

AGM Trading Update

We also get a trading update to mark today’s AGM, confirming that full-year guidance is unchanged.

Here are the main points:

“The Group has made a good start to FY 2026, with trading in line with expectations.”

Germany: continued strong adoption of cloud solutions, with ongoing momentum from new customer wins and upselling to existing customers.

UK SME: ongoing headwinds from the switch-off in early 2027 of the UK’s legacy phone network (PSTN), as previously guided. However, cloud volumes continue to grow, driven by sustained uptake of Webex for Gamma and PhoneLine+. “Customer engagement and the partner pipeline remain healthy with opportunities for larger migration deals.”

Service Provider: early traction of international strategy in Europe and APAC, has signed first contracts with customers in Germany, Australia and Singapore.

Enterprise: continued momentum from contract renewals and new business wins, including “an AI-led Customer Experience deployment at JD Sports” and further public sector wins.

Balance sheet: net debt was £1.6m at 30 April following expected cash outflows on buybacks (£12.1m) and deferred consideration for past acquisitions (£3.8m).

While I’m not always a fan of share buybacks, following the approach used by Next suggests buying back Gamma shares could create value for shareholders at current levels. Based on last year’s statutory profits, I estimate a pre-tax return on capital of 10.3% at today’s share price. That’s comfortably above the 8% minimum required by Next, whose use of buybacks is generally considered best-in-class.

Outlook

The Board expects financial performance for FY 2026 to be in line with market expectations, with Adjusted EBITDA and Adjusted EPS (fully diluted) in line with the consensus range (FY 2026 Adjusted EBITDA £138.1m - £142.8m and Adjusted EPS (fully diluted) 90.9p - 94.4p respectively, as at 12 May 2026).

Checking the March note from paid research house Progressive shows forecasts that are bang in the middle of the ranges cited above, so I don’t think there’s any change to expectations today.

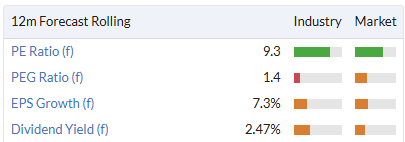

That leaves Gamma still trading on a single-digit P/E, despite hopes of a bid:

Roland’s view

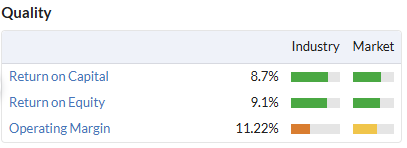

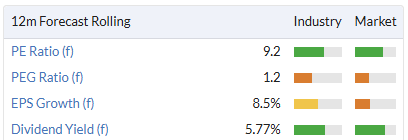

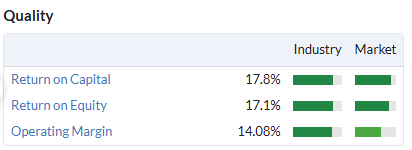

Gamma’s Quality metrics remain strong, as does the balance sheet:

The valuation also looks very tempting to me. By my sums, last year’s results give the stock a free cash flow yield of 7% and trailing EBIT/EV yield of 10.7%.

These are both levels I’d associate with value unless a business is in decline.

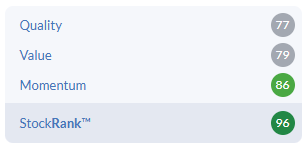

The missing element is momentum. This is highlighted by the StockRank and Contrarian styling:

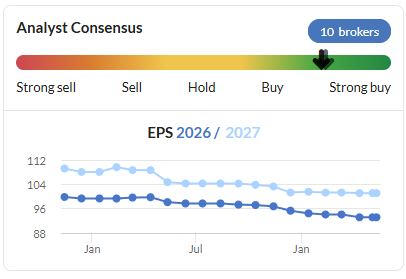

Earnings forecasts have also drifted lower over the last year, although estimates for 2027 still show a useful return to growth:

When I reviewed Gamma’s trading update in January I took a neutral view, commenting that “it feels to me like management may be digging in for a difficult period”. I noted the decision to freeze the dividend and direct up to £85m of cash into buybacks instead.

The share price is largely unmoved since then despite the emergence of possible bidders.

The only explanation I can see for this is that investors are pricing in structural weakness in margins (following the UK PSTN switch off) or slower growth due to subdued economies in Gamma’s core UK and German markets.

There’s evidently some risk of near-term weakness, but I’m reassured by today’s in line statement and my view is that the sell off has probably gone too far.

Although consensus forecasts do indicate flat earnings this year, I think technology and demand will continue to evolve and should support the medium-term growth of this business. I share the StockRanks view that this could be a contrarian opportunity and am moving my view back up one notch to AMBER/GREEN today.

Babcock International (LON:BAB)

Unch at 1,009p (£5.0bn) - FY26 post close Trading Update - Roland - AMBER ↓

Engineering contractor Babcock is one of the main outsourcing partners for the UK defence sector. This is a hot place to be at the moment, as Graham commented in January.

Despite this, Babcock’s share price has fallen by 30% since our last view on 23 Jan:

One reason for this may simply be that Babcock’s share price had run ahead of events. After all, the stock was trading on a P/E of 24 in January with a dividend yield of under 1%.

However, today’s update has revealed another reason why investors may want to be cautious about overpaying for companies such as Babcock – cost overruns on big projects.. While this particular news has only been released today, as far as I know, it’s a type of risk we’ve seen many times before with outsourcing groups, including Babcock (my emphasis):

The Group's strong underlying financial results were partly offset by a non-recurring charge on the Type 31 contract, estimated to be £140 million, fully recognised in FY26.

The Type 31 contract is a deal to build five frigates for the Royal Navy that was awarded to Babcock in 2019. Two ships were floated off last year and are now being outfitted, while a further two are now under construction. Unfortunately, problems have emerged:

During the outfitting stage we have experienced higher than expected levels of rework as a result of changes to the design and the long-term impacts of out-of-sequence build activity earlier in the programme. Whilst the number of such rework events is not entirely unexpected, the work is being performed in the later stages of completion and therefore is more complex and more costly.

Following an engineering review, Babcock has concluded that the cost of completing the contract is now expected to be £140m higher than previously expected. This will be a cost the company has to absorb:

This is reflected in an expected charge on the contract (subject to audit) of £140 million for the revised costs to complete delivery of the Type 31 design and build contract, which is fully recognised in FY26, but the cash costs of which will be incurred over the remainder of the programme.

The market appears to have shrugged off this news today, perhaps because Babcock has left its FY27 guidance unchanged (the group’s year end is 31 March).

However, The Type 31 problems will have a significant impact on the group’s FY26 results:

Contract backlog down 7.7% to £9.6bn

Revenue up 9.1% to £5,273m

Underlying operating profit down 19.3% to £293m

Underlying operating profit excluding Type 31 charge up 19.3% to £433m

Depending on whether you’re willing to exclude the costs of Babcock’s engineering miscalculations, FY26 underlying earnings per share are either slightly ahead of consensus at 60.5p, or significantly below expectations at 39.6p (Stockpedia consensus: 56.3p).

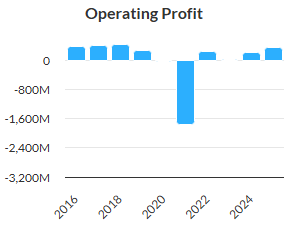

Personally, I am not inclined to ignore these costs. Building ships is a core part of Babcock’s business. If the company miscalculates the likely cost to do so, then ultimately shareholder returns will suffer. This has happened in the past – when departing CEO David Lockwood joined in 2020, the company was struggling with another such mishap (albeit larger):

In this case, the impact appears to be both limited and manageable. Even so, the impact on free cash flow could be material – the company has reported FY26 underlying free cash flow of £262m today. Assuming the cash costs of the Type 31 problems will be similar to the £140m accounting charge reported today, then cash outflows over the next few years could erode the group’s cash generation.

FY27 outlook: incoming CEO Harry Holt (previously in charge of Babcock’s nuclear business) will have to hope that there are no further problems with the Type 31 build.

The company has left its FY27 guidance unchanged today and says it has secured around 70% of revenue for the current year, “a similar percentage to the prior year”.

The consensus page on Babcock’s website gives me the following figures, suggesting sales and (underlying) profit growth are expected to slow this year:

FY27 Revenue: £5,376m (+2% vs FY26)

FY27 Underlying operating profit: £449.3m (+3.8% vs FY26, excluding Type 31)

FY27 Underlying EPS: 63.1p (+4.3% vs FY26, excluding Type 31)

These figures are broadly in line with the consensus estimates on the StockReport. To me, the valuation looks up with events:

Roland’s view

Graham was AMBER/GREEN on Babcock in January, but I am not sure I see sufficient evidence of value or momentum to maintain that view today.

In addition, I’m a little disappointed at the scale of the cost overruns on the Type 31 contract and the decline in Babcock’s order book last year.

As Mark pointed out with Avon, it’s difficult for us to guess how much the intention to increase Western defence spending will translate into additional revenue and profit for individual companies. While Babcock’s position as a key partner for the UK Ministry of Defence looks very secure, that won’t necessarily translate into automatic growth.

The StockRanks have been taking an increasingly cautious view on Babcock and I am inclined to mirror this:

I’m going to downgrade our view by one notch to neutral (AMBER) today.

Mark's Section

Vistry (LON:VTY)

Down 10% at 292p (£1.04bn) - AGM Trading update - Mark - BLACK/AMBER/RED ↓

(At the time of writing, Mark has a long position in VTY.)

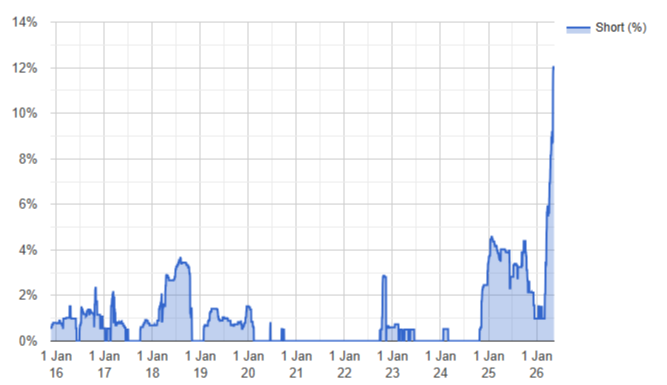

This is a fascinating situation. There is no doubt that today’s warning was expected. Here is the short position going into this update:

[Source: shortracker.co.uk]

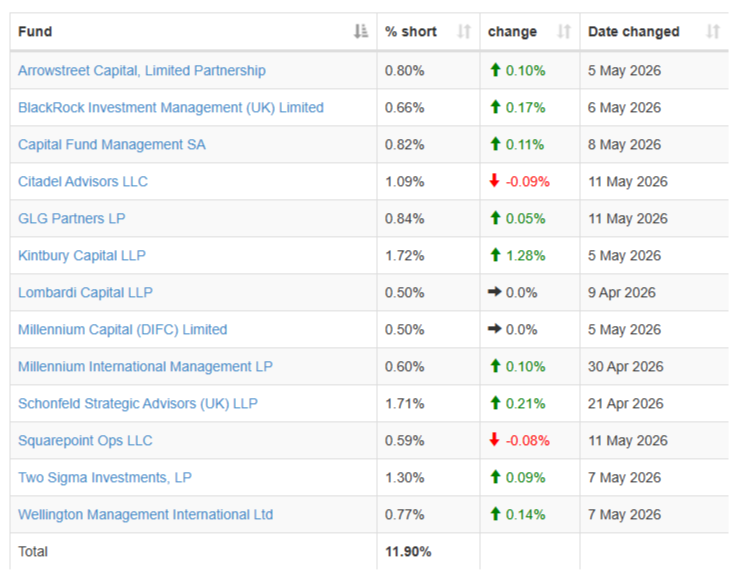

These aren’t just quant funds, either, but look like largely discretionary positions, who have all been increasing their short positions into this update:

[Source: shortracker.co.uk]

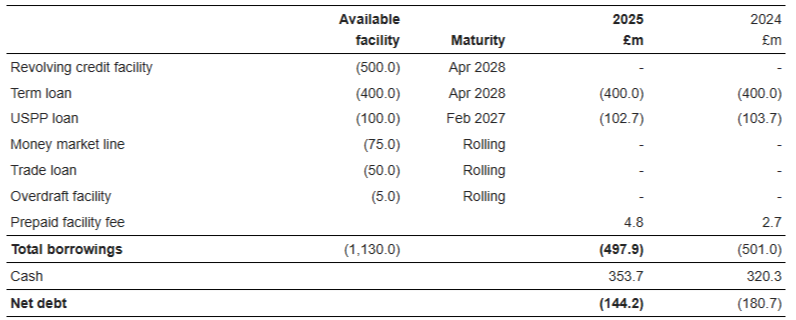

However, looking at the annual report, it was hard to see what exactly is wrong with the company. It was clear from their comments on average daily net debt versus year end position that the financial situation is not as strong as some simple year end metrics may suggest:

Net debt reduced to £144.2m as at 31 December 2025 (31 December 2024: £180.7m) with average daily debt of £733.7m.

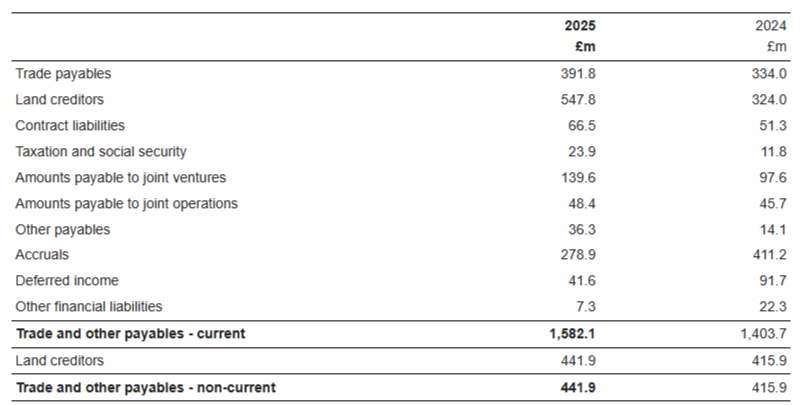

However, the obvious signs of financial distress were not there. Trade payables looked a little elevated, but not necessarily out of the ordinary:

The current land creditors being so large is perhaps the only thing that looks out of the ordinary. It seems the company has viewed the weak market for building land as an opportunity, and been buying. This perhaps looks a little unwise as companies such as Crest Nicholson have had to pause their planned land sales due to lack of demand.

And it is undoubtedly cheap on many metrics, not least that P/TBV:

Given what is happening in the sector, the land on the balance sheet may be overvalued, but it would take a huge haircut to wipe out that discount to book value. Perhaps the most damning critique is that it goes against their stated strategy of moving to an asset-light, partnership model.

Both Roland & I kept our neutral view, when we reviewed it at a significantly higher price. The big question is does today’s update change these dynamics?

First up, it may not be an explicit profits warning, but it is a sort of pre-warning:

Primarily due to the up-front profit impact of the actions to accelerate cash generation, as described above, we expect H1 profit to be significantly lower than the prior year. However, with the benefits of an improved margin mix on active sites and a step up in demand from our affordable housing partners we expect H2 2026 profit to be in line with H2 2025 profit. The Board expects adjusted profit before tax for FY 2026 to be towards the middle of the range of analysts' forecasts.

H1 significantly below, H2 in line with last year, clearly makes the FY below the previous year. There’s a huge range of analysts forecasts:

The range of analysts' forecasts (excluding those who have not updated forecasts since the start of March) for 2026 APBT is £168m to £283m.

Mid-point is £226m, but we rarely see such variation in analysts' views. Adjusted PBT for FY25 was £269m, so realistically, FY26 is likely to be below FY25 on earnings. I suspect the numbers in the Stock Report from Refinitiv include stale forecasts, something the company say they have filtered out for their numbers manually:

There are modest signs that the company may be having some liquidity challenges. They talk about their cash generation focus. They are prioritising sites where they can make near-term sale or require lower capex, and being stricter with the economics of land purchases. There are signs that the sales strategy is delivering:

The year-to-date Open Market sales rate remains around 30% higher than the prior year, despite some moderation in recent weeks reflecting uncertainty arising from the Middle East conflict. The use of increased incentives and discounts has been more significant on low margin sites and developments that are nearing completion, resulting in an earlier recognition of profit impacts and a higher weighting of the overall profit impact in the first half than previously anticipated. We expect the level of discounting and its effect on profit to reduce in the second half of the year.

So homes are selling but they’ve been having to offer much bigger incentives, and this is impacting margins.

Perhaps the most disappointing part is that they are pausing their share buyback. This suggests that their liquidity headroom isn’t entirely comfortable. However, there is no mention of issues with banking covenants (unlike at Crest Nicholson, for example). And their facilities will not need renewing for some time:

There are no signs of the usual language indicating that an equity raise is on its way. So while I don’t think they are entirely comfortable, I also don’t see an immediate liquidity crisis, which looks like what the short positions may be pricing:

….the combined effect of the above actions is expected to deliver significantly lower average net debt levels in the second half and we are now expecting a net cash position in excess of £100m at 31 December 2026.

Mark’s view

It would be a push to describe today’s update as good news, but it isn’t truly terrible news, which is what a 12% short position (of only declared positions that we know about) suggested was about to arrive. The financial situation clearly isn’t comfortable, and hence I’m downgrading our view to AMBER/RED to reflect the risks as an investment. However, the eagle-eyed will spot that I have a position here and this updated view looks incongruous with that. For clarity, this is a small controlled-risk position initiated today, on the basis that a significant proportion of the equity is sold short, presumably expecting a liquidity squeeze soon. However, given that today’s update didn't bring things to a head, this now looks like a crowded trade. If further bad news doesn’t arrive in the next few months, and the company does see significantly lower debt levels in H2, then the squeeze is likely to be the other way. I accept that this position is high risk and I’m trading against market actors that are usually smarter than me!

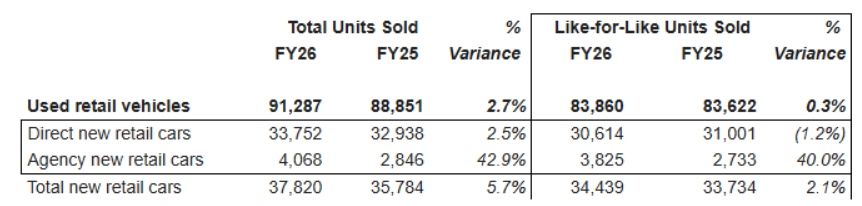

Vertu Motors (LON:VTU)

Flat at 65p (£205m) - Final results - Mark - AMBER ↓

Vertu don’t calculate percentages for us, but it is clear that these results aren’t anything to write home about:

Revenue is flat and adjusted EPS is down 13%. However, these are slightly above consensus which was for Adj. PBT of £24.0m. Forecasts had been declining for some time, though, so I wouldn’t place much emphasis on this:

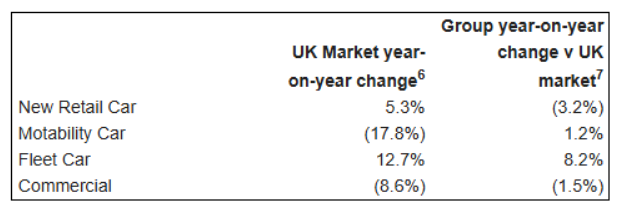

Much of the challenges have been market driven, with motability criteria tightening, and commercial sales weak:

The big underperformance has been in New Car Retail, where historically Vertu have been under-represented in Agency sales. This has been the fastest growing part of the market with Chinese electric car brands, which are much cheaper for an equivalent vehicle. Despite seeing almost 40% LFL growth in Agency volumes, this still lags the market:

Vertu are under-represented here, but are looking to fix that imbalance:

Programme to enhance portfolio with new Chinese entrant brands implemented and set to continue: Jaecoo, Omoda, Lepas, Chery and Leapmotor to be added to portfolio.

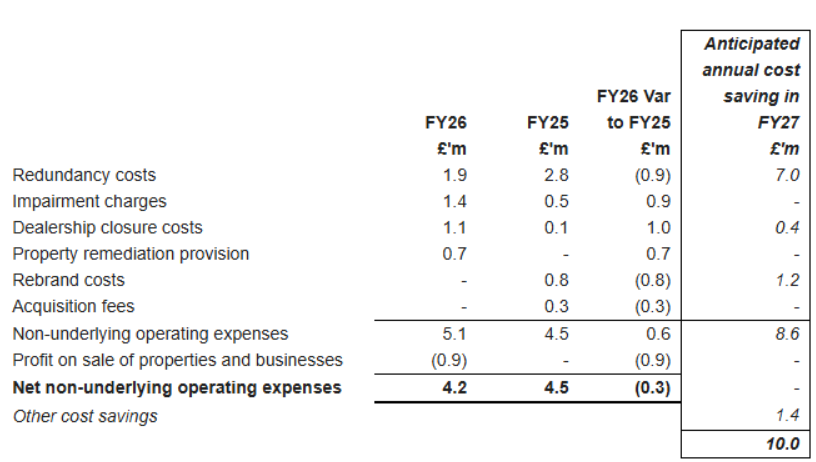

Adjustments:

These are pretty standard. However, it is worth noting that few of these appear to be one-offs:

The group is likely to continue to optimise its workforce and dealership network, and future bolt-on acquisitions aren’t out of the question. So while these make sense from a business perspective, we can be sure they won’t be adjusting out the gains from these programs in FY27!

Balance sheet:

Net debt is roughly flat at around £61m, which is relatively modest. They do have negative working capital, with payables exceeding inventories and receivables. This is normal for this sort of business, but is worth bearing in mind that they could see cash outflows from working capital if trading dipped.

They are backed by significant freehold property, though:

The Group has a balance sheet with shareholders' funds of £357.5m (2025: £357.6m) underpinned by a freehold and long leasehold portfolio of £327.1m (2025: £330.9m) and net debt (excluding lease liabilities) of £61.3m as at 28 February 2026. The Group's conservative financing and capital structure resulted in a strong tangible net assets position of £235.1m as at 28 February 2026, representing 75.9p per share.

It is worth noting that if they had to pay rent instead of owning most of their sites they would probably be loss-making. The reality is that these assets are currently producing a sub-optimal return on capital.

Outlook:

Current trading looks good, with them saying “strong start to FY27, trading profit for March and April 2026 was ahead of the prior year.” However, there is a possible sting in the tail. While they have yet to see any impact from events in the Middle East, they flag the very weak consumer confidence in the UK.

Forecasts:

Shore doesn't appear to make any significant changes to forecasts, and usually provides estimates out to FY29. However, they aren’t particularly inspiring. A forward P/E of 11, falling to 10 for FY28, and 9x for FY29.

These still suggest that the assets are not particularly productive, and it may require a step change in consumer conditions or industry dynamics for these forecasts to be beaten and the stock to look good value on earnings rather than just assets.

Mark’s view

Although these results come in slightly ahead of expectations, these have been gradually reduced over the last year or so, meaning we should read little into this. There is a positive outlook, with no impact from the Middle East so far. However, it may be hard for the company to escape the impact of weakening consumer confidence in the UK. Assuming they hit forecasts, a P/E of 11 doesn’t look particularly inspiring, so the investment thesis here is largely a very long-term one assuming that their freehold assets can be made proactive, or sold off to someone who can make them productive. We’ve tended to be moderately positive here in the recent past. However, the price is now higher than when we first gave that rating, and with the risks perhaps now to the downside rather than the upside, I think a more neutral view of AMBER probably makes sense. There is still a reasonable discount to TBV, but with no sign that these assets will be particularly productive, even out to 2029, this sort of play is only for the very patient.

Avon Technologies (LON:AVON)

Down 6% at 1500p - Interim Results - Mark - AMBER/RED ↓

Some impressive numbers for H1:

Adjustments:

Excluding amortisation of intangibles is fairly standard. However, this is another company that wants to us give them all the credit for making cost-savings in the business, but exclude all the costs of doing so:

These costs are about 20% of operating profit so are not negligible. However, they are reducing and don’t change the fundamental picture of a company becoming significantly more profitable.

Outlook:

This confirms that they expect these trends to continue in the near term:

Firmly on track to meet or exceed FY26 guidance with exciting long-term growth prospects

· Increasingly confident in H2 delivery with strong commercial and international pipelines

· Still see significant operational improvement opportunities in both businesses

· Clear pipeline of opportunities to outperform core markets and deliver sustainable growth

However, there is some scary looking moves in the future order intake:

The issue is at Team Wendy where there are government procurement delays in the US:

Team Wendy's order book declined by 30% vs HY25. This reflects strong delivery on our DoW NG IHPS and ACH Gen II programs and improved commercial lead times which reduced the backlog of orders. Commercial orders have also been held back due to delays in government funding although there are signs that this is starting to ease.

Valuation:

The multiples here already price in some significant future growth:

With no asset backing to fall back on, the investment case here lives or dies on them delivering that earnings growth. The defence backdrop should be supportive of this in the near-term, but as recent issues with governmental budgets in the US show, a desire to invest in defence doesn’t always lead to actual spending.

Mark’s view

Given the rating and drop in order book, I can see why the market has taken fright today. Significant future growth is already priced in, and while today’s results and outlook back that up, there is little room for error at the current earnings multiple.

I’m not sure I’m smart enough to judge how much of the current desire for increased defence spending by governments around the world will lead to actual increased spending. Nor judge whether that money will be spent on Avon’s products, or, for example, used to replace missile stockpiles that were expended defending against Iranian drones. So in the absence of any great defence industry insight, I am going to rely on the Stock Ranks:

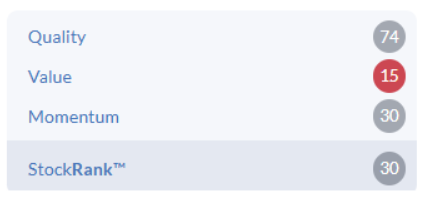

With the Momentum Rank of 30, and likely to drop further once the reaction to today’s results is processed by the algos, this is rated as a Falling Star. Since the shares peaked in the middle of last year, the Stock Rank has been declining:

With a long way down before that Value Rank of 15 starts to provide share price support, I feel we should be broadly negative here. AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.