Good morning!

The Nasdaq 100 closed at a record high yesterday and Keir Starmer is still Prime Minister. However, Health Secretary Wes Streeting is said to be preparing to launch a leadership challenge as soon as today. Former Deputy PM Angela Rayner has also been cleared of any tax-related wrongdoing by HMRC, opening the door for her to launch a leadership bid as well.

The situation in the Middle East appears to remain unchanged and nothing concrete has yet emerged from President Trump’s visit to China.

In the US, Kevin Warsh has been (narrowly) confirmed as the new chair of the Federal Reserve in a Senate vote. He will inherit some thorny issues from outgoing chair Jerome Powell, including rising inflation and Presidential pressure to cut interest rates.

Finally, today’s house price report from the Royal Institution of Chartered Surveyors showed a net balance of -34% in new buyer enquiries last month while the net balance of agreed sales was -36%. Both measures were broadly similar to March and show a reduction in housing sales activity.

House price expectations were also negative according to RICS, with a net balance of -38% indicating that estate agents are seeing more price cuts than price increases.

FTSE 100 expected to open up 0.4%

S&P 500 expected to open up 0.2%

Brent Crude is trading at $104 a barrel

Gold at $4,705/oz

Today's report is now complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£214bn | SR79) | Perioperative Imfinzi plus neoadjuvant EV showed statistically significant and clinically meaningful improvements in event-free survival and overall survival in muscle-invasive bladder cancer in the Phase III VOLGA trial. | ||

National Grid (LON:NG.) (£63.5bn | SR68) | Underlying operating profit up 6% to £5,680m with underlying earnings up 6% to 78.0p, in line with expectations. FY27 outlook: expect underlying EPS growth of 13% to 15% – in line with current forecasts. | ||

3i (LON:III) (£24.8bn | SR59) | FY26 total return of 22% (£5,304m) on opening shareholders’ funds, with NAV up 19.2% to 3,030p per share. Action LFL sales growth is 2.4% YTD, versus 6.8% during the same period last year. | AMBER = (Roland) The market is now pricing this private equity group’s shares at a c.30% discount to 3i’s latest book value. I think this reflects the risk that the premium valuation multiple applied to retailer Action (c.75% of the portfolio) may need to be moderated. While I’m fairly sure Action remains a good business with solid growth prospects, the situation isn’t without risk. Sluggish European economies and the group’s decision to launch in the US could put pressure on LFL growth and future profitability. On balance, I think Graham’s previous neutral view remains fair, albeit for slightly different reasons to those he gave one year ago. | |

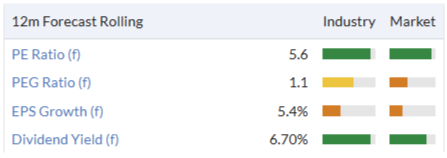

Aviva (LON:AV.) (£18.6bn | SR46) | On course for 2026 guidance. General insurance premiums up 19% to £3.4bn, with wealth net inflows of £3.3bn and AUM up 18% to £233bn. Aviva’s combined operating ratio improved to 94.1% (Q1 25: 96.6%) while its Solvency II Cover Ratio fell 9% to 171%. | AMBER/GREEN = (Roland) [no section below] I’ve been moderately positive on Aviva for sometime and don’t see any reason to change this view today. Growth in general insurance and wealth management remains strong. Although performance in Health and Retirement (annuities) was weaker than last year, overall guidance for performance through 2028 remains unchanged. Viewing this business primarily as an income stock, current forecasts suggest a 6.7% dividend yield with expected dividend growth in excess of 5%. That implies an expected return of >10% over the coming 12 months – potentially an attractive valuation, in my view. | |

Land Securities (LON:LAND) (£4.25bn | SR25) | EPRA earnings up 2.1% to £382m with EPRA EPS up 2.2% to 51.4p, at the top end of guidance. Total accounting return of 5.6% with EPRA NTA per share up 1% to 882p. Dividend 2% to 41.2p per share. FY27 outlook: expect LFL rent to grow 3-5%, FY27 EPRA EPS expected to be stable vs FY26, in line with previous guidance. | ||

Burberry (LON:BRBY) (£4.2bn | SR43) | Revenue -2% to £2,420m with adj operating profit +£160m (FY25: £26m). Returned to LFL sales growth from Q2 with FY26 LFL sales +2%. Outlook: expect revenue growth and margin expansion, but mindful of uncertain macro environment. | AMBER = (Roland) [no section below] Today’s results show a return to meaningful profitability and positive like-for-like store sales growth (albeit only 2%). While overall revenue fell last year, I see this as a respectable set of results, supporting the strategy set out by CEO Joshua Schulman after he took charge. However, the near-term outlook may be uncertain. The company warns that the macro environment could affect sales and does not provide any explicit comment on FY27 expectations today, instead merely guiding for “further progress”. This might leave the door open for a modest broker downgrade at some point. More broadly, I think the £4bn market cap already reflects significant improvements in growth and profitability. Today’s adjusted operating margin of 6.6% is a far cry from the 20%+ achieved in the past, but Burberry shares are still trading on a FY27E P/E of 27 and a FY28E P/E of 18. Even if the company delivers on these forecasts, I think the current valuation is probably up with events. I’m leaving our neutral view unchanged today. | |

ITV (LON:ITV) (£2.95bn | SR94) | "ITV maintained good momentum in the first quarter of 2026, delivering results in line with market expectations.” External revenue rose by 1%, with Studios +4% and M&E -2%. Remains in active discussions with Sky about a possible sale of the M&E business. FY26 outlook unchanged. | ||

Shaftesbury Capital (LON:SHC) (£2.52bn | SR39) | “... a positive start to 2026”. 151 leasing transactions completed representing £13.7m of new rent, 5% ahead of December ERV and 18% ahead of previous passing rents. Vacant space represents just 2.5% of ERV. | ||

Premier Foods (LON:PFD) (£1.71bn | SR82) | Revenue +2.5%, adj pre-tax profit +8.5% to £183.6m. Net debt down £48.4m to £95.2m. Branded revenue +3.4%, with market share gains in Grocery and Sweet Treats. Outlook: Trading profit expectations for FY27 remain unchanged. | ||

Shawbrook (LON:SHAW) (£1.61bn | SR50) | Loan book +2.6% to £19.7bn, customer deposits +1.8% to £18.7bn. CET1 ratio +0.2% to 12.6%, with 3-month-plus arrears +0.1% to 1.7%. Outlook: FY26 guidance initiated for a loan book of c.£21bn and underlying RoTE of c.17%. Maiden dividend with respect to FY26 will be payable in FY27. | ||

Watches of Switzerland (LON:WOSG) (£1.24bn | SR91) | SP +14% FY26 revenue +13% to £1,828m, or +11% excluding 53rd week. The US now accounts for over half group sales. Adj EBIT expected to be £152-155m, ahead of previous guidance. FY27 outlook: revenue +5% to 10%, with adj EBIT margin +0.4% to +0.8% vs FY26. | AMBER/GREEN = (Mark) The midpoint of the range here is only 3.5% ahead of consensus, making the share price rise today look aggressive. However, the forward guidance suggests that EPS should grow by 15% at the midpoint of guidance ranges into FY27, and assuming that can be maintained over the medium-term, the shares don’t look that expensive compared to this growth rate. There are a couple of things to be cautious about: the company is increasingly exposed to a stretched US consumer, and we have yet to see the scale of the adjustments made. Overall though, momentum is behind the business, especially in the US, and it makes sense to keep our broadly positive view. | |

Great Portland Estates (LON:GPE) (£1.22bn | SR28) | All floors now under offer within six months of completion. Pace of leasing “underlines the continued demand for high-quality, well-located workspace”. | ||

Grainger (LON:GRI) (£1.15bn | SR65) | Net rental income +7.8%, with EPRA earnings +4% to £31.4m and EPRA EPS +4% to 4.2p. EPRA NTA per share -3% to 290p with LTV increasing to 40.2% (FY25: 38.4%). | ||

Princes (LON:PRN) (£927m | SR82) | Revenue +6% to £506.6m, with adj EBITDA +17% to £38.2m. Net cash of £344m. Outlook: “trading in the early part of FY 2026 has remained in line with Management expectations”. Expects further profitability improvement in FY26, while noting broader macro uncertainty and inflationary pressures. | ||

Spire Healthcare (LON:SPI) (£606m | SR37) | SP +48% “Trading in the first four months of the year to April 2026 has been in line with our expectations.” …continues to target FY26 adjusted EBITDA broadly in line with FY25. Non-binding proposal received from funds advised by Toscafund, the Company's second largest shareholder, regarding a possible cash offer of 250 pence per share. Would be a 67% premium. | PINK (Roland) Today’s offer looks more generous on some measures than others. It’s also interesting to remember that Toscafund helped to block a 250p offer from a rival health firm back in 2021! While I’d like to think Spire could be worth more as a standalone business, the company’s track record and balance sheet suggest to me that 250p probably is a reasonably fair offer for shareholders. In addition, Toscafund’s long involvement with this business and the previous withdrawal of rival named bidders suggests to me this takeover is likely to go ahead. | |

Costain (LON:COST) (£527m | SR95) | Trading for the period remains in line with the Board's expectations. Expects revenue growth and further growth in adjusted operating profit in FY26. Expects FY26 net cash position to be approximately £175m. | ||

Auction Technology (LON:ATG) (£429m | SR43) | Proforma CCY Revenue +7.9% to $126.1m, Adj. EBITDA +9.9% to $42.7m, Adj. EPS +4.7% to 19.9c, Net Debt +43% to $152m. For FY26 we have modestly upgraded our full year guidance ahead of current market expectations. | AMBER = (Roland) The modest upgrade to guidance only appears to amount to a 1% increase in revenue expectations. Today’s updated broker note from Cavendish suggests this isn’t expected to have any impact on earnings per share for the year. My view remains that this business has been underperforming its potential, so I’m keen to hear from the new CEO when he’s had a chance to formulate some plans (he only started on 5 May). For now, the valuation looks about right for a slow-growing and not-very-profitable business. I’m staying neutral until a clearer picture emerges. | |

Tharisa (LON:THS) (£360m | SR99) | Headline earnings per share ('HEPS') for the six months ended 31 March 2026 are expected to be between US 16.1 cents and US 16.6 cents per share | ||

Malibu Life Holdings (LON:MLHL) (£309m | SR28) | Appointment of Todd D. Shriber as Chief Executive Officer, effective Monday, July 20, 2026. | ||

Future (LON:FUTR) (£267m | SR64) | Revenue -8% to £349m, Adj. EBITDA -24% to £83.3m, Adj. EPS - 22% to 46.4p, Adj. FCF -18% to £91.1m. Net Debt £314.1m (FY25: £276.4m) 1.6x leverage. Outlook is unchanged and in line with current consensus. Board believes that the Group is fundamentally undervalued. | AMBER = (Mark - I Hold) Weak results underline why expectations were downgraded a few months ago. However, the cash flow remains prodigious and the board gives an in line outlook. This leaves a fair amount to do in H2 to hit those forecasts, but it will be aided by a “transformation” programme. They continue to buyback shares and if a stabilisation and recovery do arrive this will juice the upside. However, given the H1 trends it would seem foolish to rule out a further short-term warning. With this, and a Momentum Rank of 1, making the investment case finely balanced, I’m sticking with our previously neutral view. | |

Secure Trust Bank (LON:STB) (£239m | SR92) | Net lending +6% YoY to £3.345bn, Deposits -6.6% YoY to £3.149bn, reflecting the reduced funding requirement following sale of the Consumer Vehicle Finance business in Feb 2026. Remain on track for the full year and confident of medium-term prospects. | ||

Eurocell (LON:ECEL) (£103m | SR62) | Trading conditions have remained subdued in 2026. Outcome difficult to assess. Paused branch opening programme. | AMBER/GREEN = (Mark) | |

4Basebio (LON:4BB) (£67.6m | SR1) | Richard Bungay appointed as Chief Financial Officer, with effect from July 2026. 2 non-execs step down. | ||

Microlise (LON:SAAS) (£67.2m | SR47) | Adj Revenue +4% to £84.0m, Adj. EBITDA -27% to £8.3m, Adj. EPS - 59% to 1.72p. Statutory LBT £2.5m. Expects revenue from OEM customers below FY25 level. | BLACK/AMBER/RED = (Mark) While FY25 is said to be in line on adj. EBITDA, it is a 15% miss on EPS. Their broker takes an axe to future forecasts too, with FY26 estimates 39% lower and a whopping 61% taken out of FY27. Net cash forecast for FY27 went from £20.4m down to just £6.2m, knocking out another one of the valuation legs. This means that the shares still don’t look cheap even on FY27 estimates, and given recent trends it would be hard to have much faith in these. Despite the share price halving since we last took a broadly negative stance the company, I am in no rush to change this view. | |

Panther Securities (LON:PNS) (£50.2m | SR82) | PAT -36% £4.25m, NAV flat at 672p after special dividend paid. | ||

Gattaca (LON:GATC) (£34.2m | SR93) | Contract recruitment has continued to perform strongly …trading ahead of market expectations. Continuing underlying profit before tax for FY26 to be not less than £6.0 million (previous guidance: £4.5 million). | GREEN = (Mark - I hold) | |

Touchstone Exploration (LON:TXP) (£28.9m | SR75) | Q1 Prodn. +8% to 4,657 boepd, Revenue +14% to $12.5m, Funds flow from operations $1.85m, net loss $2.38m. Net debt $76.1m. | ||

| Cordel (LON:CRDL) (£25.0m | SR47) | Recommended Cash Acquisition of Cordel Group plc (4pm Wed 13/5) | Agreed cash offer of 12.4p per share with Vossloh AG (a German railway technology company) | PINK |

essensys (LON:ESYS) (£10.6m | SR30) | Has received valid acceptances of the Offer representing 97.01%. Compulsory acquisition of the rest. | ||

Nexus Infrastructure (LON:NEXS) (£10.0m | SR49) | Revenue +5.6% to £32.3m, u/l op. Loss £0.8m (HY25: £1.1m loss), Cash £8.5m (HY25: £9.6m), net assets £26.2m (HY25: £28.1m). “While cognisant of the continued challenging UK macroeconomic backdrop, the Board remains confident in the Group's ability to deliver full-year results in line with market expectations.” |

Roland's Section

Spire Healthcare (LON:SPI)

Up 48% at 222p (£894m) - AGM Trading Update & FY26 Outlook + Statement regarding possible offer - Roland - PINK

I have been critical of management here for repeatedly complaining that Spire’s share price is too low, while not necessarily delivering the returns on capital needed to justify a re-rating.

The business has effectively been up for sale for a while now, although talks with other named bidders were terminated in March.

Today we have the first indication of what both the company’s board and an informed, well-funded buyer believe to be a fair price for Spire’s property estate and private healthcare business:

Toscafund Asset Management has made a possible cash offer of 250p per share, valuing the equity at £645m. Including last-reported net debt, the total value of the offer is c.£1bn plus lease liabilities.

The offer would include an option for shareholders to opt for an unlisted equity alternative to cash.

Toscafund is already Spire’s second-largest shareholder, with c.24% according to our data.

After a number of earlier proposals, Spire’s board has said it would be prepared to recommend Toscafund’s latest offer.

250p represents a 66% premium to yesterday’s close, but it’s only marginally above the level at which the shares traded for most of the last five years:

Looked at differently, here are a few other measures of valuation for the Toscafund offer:

250p is a 36% premium to Spire’s FY25 book value of 184p per share;

250p gives a FY26E P/E of 31, falling to a FY27E P/E of 18.5;

250p represents c3.7x FY25 adj EBITDA. This is below the 5.5x multiple at which Spire made two acquisitions last year.

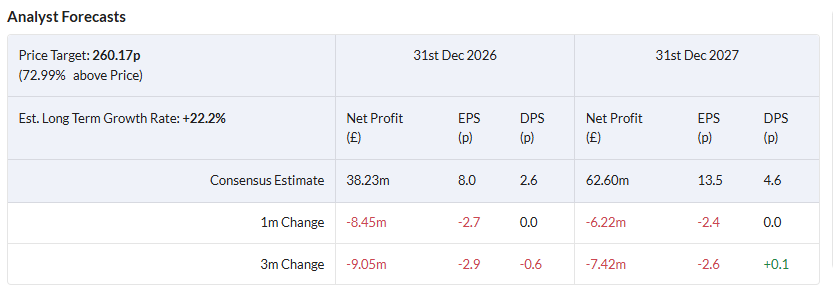

250p is broadly in line with analysts’ average target price for Spire of 260p.

Finally, it’s also worth remembering that Spire received an offer at 250p from Australia’s Ramsay Healthcare in 2021. The Board recommended the offer to shareholders, but major shareholders voted against the deal.

One of the shareholders who blocked the deal at the time was … Toscafund.

In fairness, the macro context was more helpful then – demand for NHS-funded services was booming and interest rates were still at rock bottom. Neither of those things are true today. In March’s results, Spire confirmed that it expected “NHS budgetary constraints to continue” and didn’t expect year-on-year growth in NHS revenue in 2026.

Even so, I can’t help feeling that Toscafund’s new offer at 250p (following previous lower offers) carries a certain chutzpah.

AGM Trading Update: helpfully, Spire has also issued a trading update today confirming that performance so far this year has been in line with expectations and reconfirming its FY26 outlook:

Accordingly, we confirm the Group continues to target FY26 Group adjusted EBITDA broadly in line with FY25.

Checking back to last year’s results shows FY25 EBITDA of £268.6m (FY24: £260.0m).

Assuming a flat result this year means that the forward adj EBITDA multiple for this proposed acquisition would also be c.3.7x. Broadly often means slightly below, though, and we can see that earnings forecasts have been steadily trending lower:

Roland’s view

Spire’s profitability has been woeful in recent years:

One reason for the low returns on book value is the £400m+ of goodwill from past acquisitions on Spire’s balance sheet. Ignore this – as makes sense for a buyer of the whole business – and I estimate return on equity rises to 5.2%.

That would still be too low to persuade me to pay 1.4x equity value for a share.

However, I can see a couple of reasons why a private bidder might be happy to pay a premium to Spire's book value:

Toscafund will most likely find ways to improve profitability. In addition to any operational improvements, it may be able to refinance at lower cost and perhaps increase leverage.

Spire’s operating cash flow has remained very strong in recent years:

Does today’s offer represent good value for shareholders?

In an ideal world, I’d like to think this business could command a higher valuation. But Spire’s track record, balance sheet and exposure to NHS budgets suggest to me that in today’s markets, 250p probably is a reasonably fair offer.

Toscafund has been invested for a long time and can be assumed to know Spire’s business very well. Other potential bidders have withdrawn, so I would guess that this deal is now likely to go ahead.

I’m going to withdraw our view on the basis of today’s share price rise and the likelihood (as I see it) of the takeover proceeding.

3i (LON:III)

Down 11% at 2,150p (£22.1bn) - Results for the year to 31 March 2026 - Roland - AMBER =

We don’t look at investment trusts very often, but 3i is both a FTSE 100 member and down by 14% today.

This private equity trust is also particularly interesting because it’s largely a proxy for the performance of its largest holding, European value retail Action (similar to B&M). Action now accounts for almost 75% of 3i’s portfolio value, based on today’s results.

The group’s investment in Action (which started in 2011) has been a terrific success. But 3i’s share price has now fallen by more than 50% since November:

The main trigger for today’s sell off and that in November appears to have been the company’s reports of slowing like-for-like sales growth at Action. Let’s take a look at this holding.

Doubling down on Action?

3i increased its equity stake in Action from 57.9% to 65.4% last year through various cash and share transactions. Other Action investors appear to be taking profits, while 3i is effectively doubling down by buying more at a higher valuation.

This may yet prove to be a prescient move by CEO Simon Burrows. Action believes it has significant “whitespace” to expand into in Europe:

Current store count: 3,335 stores in 15 countries;

Estimate of “additional white space potential … in Europe”: c.4,650 stores

If this is correct, Action could double in size again while remaining inside Europe, a market it undertstands well.

However, the company is also aiming higher than this and is planning to launch in the US at the end of 2027 or beginning of 2028.

I’m pretty sure the number of European retailers who have tried and failed to succeed in the US market is greater than the number who have succeeded. The US is a vast market, but therein lies complexity as well as opportunity. It’s also hugely competitive with a large base of retailers who will compete intensely with Action.

Sales slowdown?

Action’s sales performance last year was strong but showed clear evidence of slowing like-for-like store growth:

Source: 3i FY26 presentation

Today’s results confirm that LFL sales growth has continued to slow in FY26:

In the year to 10 May, Action’s LFL sales growth was 2.4% (vs 6.8% comparable LFL last year)

In France and Germany, YTD LFL sales have been flat due to consumer confidence and lower footfall since the start of the Middle East conflict.

FMCG categories are said to be trading well, but seasonal categories have underperformed

It’s not a surprising picture, in my view, and total revenue and sales growth is still being boosted by ongoing store openings. But LFL growth is a key requirement for a successful retailer, as margins tend to come under pressure otherwise (taking into account inflation).

If this situation persists for any time, I think the risk is that the premium valuation 3i applies to Action (which underpins the value of its portfolio) could come under pressure.

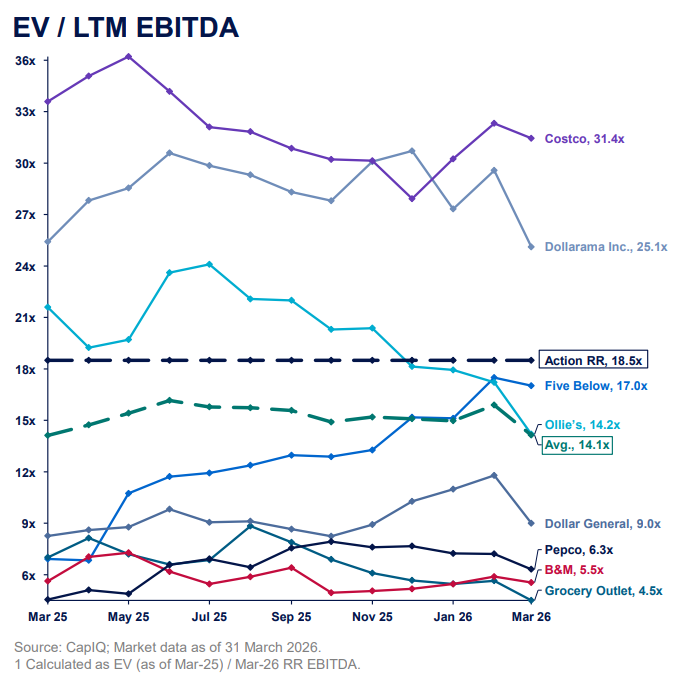

Action valuation: 3i’s approach to valuing Action assigns a far higher EBITDA multiple than normal to the business. Broadly speaking, this reflects management’s belief that Actions growth characteristics and business economics are also superior to most rivals (my bold):

At 31 March 2026, we valued our 65.4% stake in Action at £23,743 million. Our approach to the valuation of Action remains consistent. The valuation reflects the continued strong growth in Action's LTM run-rate EBITDA, its low leverage and an unchanged LTM run-rate EBITDA valuation multiple of 18.5x, net of the liquidity discount.

The company says this the valuation is benchmarked against “a broad peer group of discounters, with a higher weighting towards the top-quartile subset of North American value-for-money retailers”. This chart from today’s slide back provides some more context:

Source: 3i FY26 presentation

Action’s valuation is far above that of some well-known UK retailers with overlapping market segments:

B&M: 5.2x

Tesco: 8.3x

Kingfisher (B&Q owner): 5.7x

Dunelm (disc: I hold): 5.8x

Even at its peak, in 2021-2023, B&M was only valued on an EV/EBITDA ratio of c.9x.

Of course, Action is much larger and faster growing than most of these retailers. If the current growth slowdown proves to be a temporary blip, then Action’s premium valuation could remain supportable.

However, I think it’s worth noting what the market is saying about 3i’s portfolio and – effectively – about Action.

A growing discount to book value

3i has reported a total return on shareholders’ funds of £5,304m for the year ending 31 March 2026 today. This is based on a mix of realised proceeds from disposals (£1,517m) and unrealised investment returns.

As a result, 3i’s reported net asset value per share rose by 19.2% to 3,030p last year.

However, the shares are trading at around 2,150p at the time of writing. That’s a 29% discount to net asset value.

Applying this same discount to 3i’s Action holding suggests the market is valuing Action at around 13x EBITDA.

Outlook

No specific forward guidance is provided today but 3i does emphasise its commitment to continuing to allocate capital efficiently and generate attractive returns – the company has a target return of 15% per year:

… the Board is conscious that the second half of the year has been challenging for shareholders, as the share price has adjusted from the significant premium to NAV that had built up, particularly over the preceding two years. Our focus is, as it has been since 2012, on building sustainable value in the portfolio as measured by growth in NAV and dividends per share, where the benefits of compounding returns accrue to shareholders over the long term.

Broker forecasts have been edging lower since November and seem unlikely to rise following today’s report:

Roland’s view

When Graham looked at 3i’s results in May 2025, he took a neutral view and noted:

… given the lack of diversification it offers and the high premium to NAV at which its shares trade, I don’t see a particularly compelling opportunity.

3i’s premium to NAV has now been erased and the shares trade at a 30% discount to book value. Given the apparent quality of the group’s core holding in Action, does this make the stock a compelling buy today?

If 3i can continue to deliver returns in line with its target of 15% per annum, then I would argue the current discount to book value is likely to represent an attractive entry point.

The risk is that this largely depends on the progress and growth prospects for Action.

I don’t feel qualified to judge the potential for Action’s continued growth, but I would note that my experience of following other retail rollouts is that they often end up being priced for perfection before problems start to emerge.

I’d be more relaxed about this situation if 3i didn’t apply such a demanding valuation multiple to Action.

As things stand, I can’t help feeling that the market’s discount could be closer to a fair value for 3i’s portfolio. There’s the potential for a bounce if trading recovers quickly, but if macroeconomic conditions in big European markets remains sluggish I can also see some downside risk.

The decision to expand into the US isn't without risk either.

On balance, I think Graham’s previous neutral view remains apt, albeit for slightly different reasons to those he gave.

Auction Technology (LON:ATG)

Up 8.5% at 384p (£467m) - Interim Results - Roland - AMBER =

I’ve commented more than once that I believe this online auction group is underperforming its potential, so I’m pleased to see tentative evidence of a return to growth in today’s half-year results, albeit with a fall in profit margins:

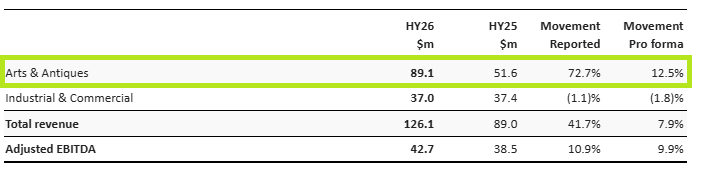

Revenue up 7.9% to $126.1m (pro forma constant currency)

Adj operating profit up 8.9% to $36.9m (pro forma constant currency)

Adj earnings up 4.7% to 19.9 cents

Adjusted free cash flow up 86.6% to $26.5m

Adjusted net debt up 42.7% to $152.0m

The main negative here is the reduction in profitability. Today’s figures indicate an adjusted EBITDA margin of 33.9%, well below the 43.3% achieved last year. It seems pricing power may be under pressure – something management refers to in divisional trading commentary below.

The company also debuts some modified performance metrics:

Items sold up 2% to 3.6m (flat in Art & Antiques and up 4% in Industrial & Commercial)

Group Gross Merchandise Value flat at $1.8bn, with A&A GMV +5% to $0.5bn and I&C down 2% to $1.3bn)

Take rate increased to 7.1% from 6.6% pro forma, based on continued success with value-added services, especially shipping for art and antiques.

Segmental results: underlying divisional performance for A&A seems slightly better than these headline figures suggest and suggests turnaround efforts are bearing fruit:

Source: ATG FY27 interim results

Arts & Antiques (A&A): Our actions are delivering with pro forma revenue growth of 12.5%. Investments in improving the buyer and seller experience are starting to drive financial results in A&A, specifically LiveAuctioneers. The A&A market remains healthy.

However, in I&C the company says that agricultural markets are “challenging” and flags up “competitive dynamics” in the sector, driven by auction house consolidation and the adoption of (rival) third-party white label solutions by some sellers.

I wonder if this may account for the fall in margins?

Current trading and outlook

For FY26 we have modestly upgraded our full year guidance ahead of current market expectations.

The company now expects pro forma revenue growth of 5-6% (previously 4-5%). Guidance for an adjusted EBITDA margin of 34.5% to 35.5% (FY25: 40.4%) is unchanged.

This guidance implies a slight improvement in H2 margins versus H1 (33.9%) but still remains well below the level of profitability achieved in the past.

Broker forecasts: Cavendish has issued a new note today that’s available on Research Tree. Its analysts do not expect the 1% increase in revenue to drop down to profit; FY26 earnings forecasts have been left unchanged at 38.75 cents per share.

Roland’s view

ATG was a(nother) disastrous 2021 IPO, but I continue to think there could be a decent business here if new CEO Duncan Painter can address some of the group’s performance issues (and avoid overpriced acquisitions).

Painter only started work on 5 May so was not involved in these results, which cover the six months to 31 March 2026. I think it’s too soon to draw judgement here and would like to hear from him later in the year, when he has had a chance to review the business in detail and formulate some plans.

For now, I would argue that both profitability and growth are insufficient to justify a premium valuation, so the forward P/E of 11 looks about right to me:

I’m going to mirror the StockRanks and leave my previous neutral view unchanged today.

Mark's Section

Gattaca (LON:GATC)

Up 17% at 127p (£34.2m) - Trading Update - Mark - GREEN =

[At the time of writing, I have a long position in the company.]

It’s a short but sweet unscheduled trading update from one of Ed’s 2026 NAPS:

Further to the Group's interim results announcement on 24 March 2026, contract recruitment has continued to perform strongly leading to the Group trading ahead of market expectations.

As a result, the Board expects Group continuing underlying profit before tax for FY26 to be not less than £6.0 million (previous guidance: £4.5 million).

Recently, I have been critical of companies over-egging their language, saying they were “materially” or "significantly" ahead when they are only upgrading by single-digit percentages. No such issues here, in fact the opposite. They don’t seem to consider a 33% upgrade to PBT as material!

You could say the signs were there for this beat, as when they reported interim results in March they did 6.9p EPS in H1 of their FY forecast (at the time) of 9.3p EPS. However, the market appears to have forgotten that in the meantime as the shares drifted on no news.

Forecasts:

Their broker Panmure Liberum translates this into a whopping 43% rise in FY26 EPS to 13.3p. However, the impact on outer years is less, They say:

At this stage, we keep our FY27E and FY28E forecasts very cautiously set with no material change to NFI and a £0.5m increase in PBT in both years. The macro remains tough and the slower than expected rate of hiring in H2 26 may mean a slightly longer lead time on the associate growth.

So it seems that part of the near-term beat is simply the lower costs associated with not being able to add the sales headcount as rapidly as expected.

Still, PL increases FY27 EPS by 16% to 14.4p and FY28 by 14% to 16.5p. They also increase the dividend payment in line with the percentage increase in EPS, so we now have a 6p forecast for this year.

Valuation:

Given the share price has moved this morning, I need to do my own multiple calculations. Assuming 130p to buy, I get the following metrics:

Cash-adj. P/E is not ideal, as it double counts the impact of interest earned on the cash. However, it does take account of the modelled reduced cash pile as working capital increases as they grow.

Overall, these figures look too cheap for a business that is out-performing and the broker describes their future forecasts as “very cautiously set”.

Mark’s view

This shows that a surprisingly conservative management for the sector continues to deliver where it matters - in the financial results. While the signs that they were on for a beat may have been there in the HY results, the market appears to have forgotten this dynamic in the intervening period, meaning that today’s rise just takes us back to where we were a few months ago.

This means that the company continues to look good value, and great value if you assume they can use that cash balance to grow further either organically or via acquisition. I am in no rush to change our previously positive view. GREEN

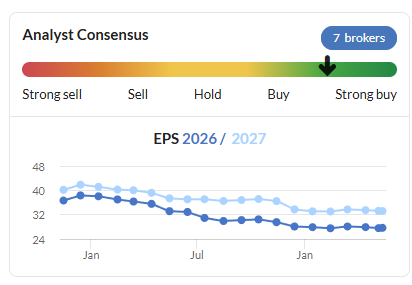

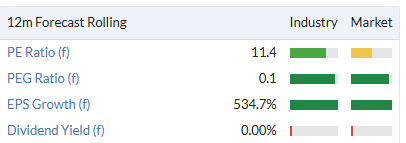

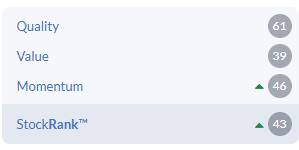

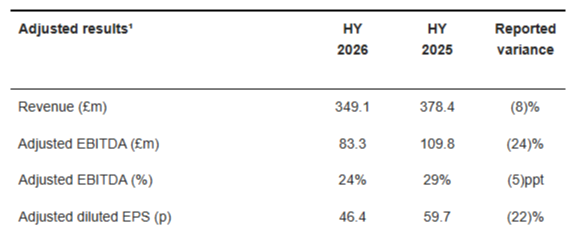

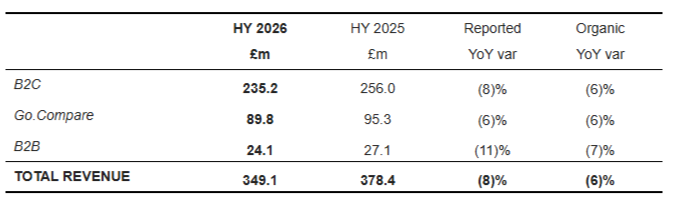

Future (LON:FUTR)

Up 7% at 310p (£267m) - 2026 Half Year Results - Mark - AMBER

[At the time of writing, I have a long position in the company.]

It seems the market was rather worried about these results. Poor revenue trends from Reach recently didn’t help, nor the March profits warning:

There has been a significant de-rating of the shares over the past year. Whereas FY26 earnings consensus has dropped from 136p to 103p, a drop of 24% over the last year, the share price has lost more than 2/3rds of its value.

This is despite a buyback that has reduced the share count from 106.7m shares down to 92.8m, and an increase in the annual dividend from 3.4p to 17p. It seems that many market participants don’t want to own this at any price. Looking at today’s interims, you can see why they may be wary:

An 8% drop in revenue leads to a 22% drop in EPS and leaves a lot to do in H2 to hit the FY forecasts.

Segmental reporting:

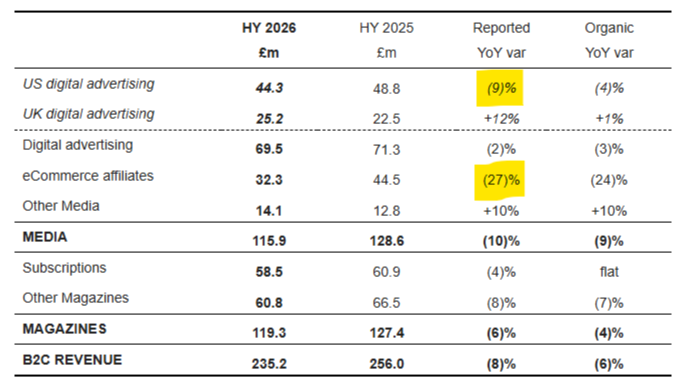

All their segments are down, but as the largest group Business-to-Consumer down 8% is the big contributor:

In this division, a couple of numbers stand out. While UK digital advertising has actually made a comeback, the US continues to decline. Affiliate marketing, which is perhaps the part of the business most likely to be disrupted by AI search is down 27%:

AI:

As Roland has already commented on previously, the company is pursuing a Google-zero strategy with the aim of driving traffic organically, rather than via search. Their acquisition of Sheerluxe is part of this, and explains why they were willing to pay a multiple higher than their own shares were trading on for this business. However, the jury is out on how successful they will be with this. In the meantime they can expect weaker revenue.

However, they are not wholly an AI loser, and are increasing their revenue from new initiatives:

Future Optic is our AI visibility ad package, presented in December, which leverages our high AI visibility in LLMs. This initiative is gaining traction with £2m sold to date and £10m booked for the full year. The reason this initiative is successful is:

1. It solves a problem for advertisers (i.e. how they achieve visibility for their products in LLMs); and

2. Future has scale and expertise in AI visibility which is externally recognised (e.g. by SimilarWeb, Peec, Ahrefs and Promptwatch)

These figures are still relatively small, but the growth rate suggests that this could become a larger part of the business and offset some of the natural decline.

Adjustments:

As usual, there is a big gap between adjusted and statutory figures. Amortisation of acquired intangibles is the biggie, and it is normal these days to exclude this charge. The scale of Share–Based-Payments suggest at the very least we should take the fully diluted share count, but again, it is normal to exclude these. The exceptional costs have jumped, though:

Exceptional items for the period totalled £3.2m. This primarily reflects £2.9m in restructuring costs associated with our ongoing Group-wide efficiency programme, which remains on track to deliver targeted annualised savings of £20.0m by FY 2028. A further £0.1m related to legacy onerous property obligations, consistent with prior-year treatment.

These look more one-off than many companies, and if they really can deliver £20m of annual savings from a relatively small one off cost, this will have been a price worth paying. However, it is worth watching for how ongoing these “transformation” costs will be.

Cash flow:

With the majority of the adjustment being non-cash, the cash conversion is excellent:

The Group remains highly cash generative, a consistent feature of the Group, with cash inflow from operations of £96.2m (HY 2025: £115.9m) reflecting continued strong cash generation. Adjusted operating cash was £101.5m (HY 2025: £119.3m).

I never like to see the word “adjusted” before the word “cash”. However, even on a statutory basis, this is strong.

Balance sheet:

Despite the strong operating cash flow, net debt has risen:

After expenditure on property, plant and equipment and website development costs and returning £52.9m (HY 2025: £43.2m) to shareholders in the period through share buyback programmes and annual dividend, leverage has increased to 1.6x (FY 2025: 1.3x) and net debt excluding lease liability has increased to £314.1m (FY 2025: £276.4m).

This is partly because they paid a £16m dividend and bought back £36.9m worth of their own shares, but also because they made a £39.9m acquisition in the period. Cash interest and taxes are also not insignificant.

I’ve never really considered the balance sheet here strong, given the lack of asset backing, negative working capital and size of the debt. However, facilities are both long-dated and largely fixed interest:

At 31 March 2026, 39.3% (£236.0m) of the Group's facilities remained undrawn (31 March 2025: 53.8% (£350.0m) undrawn). The Group's £300m revolving credit facility, maturing May 2029, and £300m senior unsecured bond, maturing July 2030, provide the Group with long-dated maturity profiles on its committed debt facilities. As at 31 March 2026, 82.4% (31 March 2025: 100%) of the Group's drawn debt was fixed at an average rate of 6.75% (HY 2025: 6.39%)

The current leverage ratio at 1.6x Net Debt/EBITDA is a little higher than their target of 1x, but not excessive. They suggest that they will “...focus on reducing net debt in the second half, with a view to managing leverage down to 1x over time“ in the future, but are continuing with their ongoing buyback. On 1st April, they had £20m of the most recent £30m left to deploy, which would reduce the sharecount by a further 7% or so at the current price.

Outlook:

Despite what looks like a difficult H1, the core guidance remains the same at the (reduced) level from March:

Outlook is unchanged and in line with current consensus

● The Group is expecting mid to low single-digit organic revenue decline for FY 2026.

● The Group continues to expect to deliver an adjusted EBITDA margin in the range of 25-27%.

● The Group continued to expect cash conversion to adjusted EBITDA to ~90%.

Company compiled consensus for FY 2026 includes 7 analysts: Revenue £710m, EBITDA £183m

Valuation:

If they really are trading in line, the valuation is incredibly low for a business with this level of cash generation:

If this level of cash generation continues, they could probably buy back all of their shares outstanding over the next few years, while also returning their net debt levels to target.

The problem is that given the disruption in their end markets from AI, and recent profits warning, very few investors have the confidence that they will actually be able to deliver in line with these forecasts.

Mark’s view

I can see this going one of two ways. It is either a cigar butt whose core business has been undermined by AI search taking over, and the current strong cash flow is the last puff of that. Or it is a business which will adapt to mitigate and eventually take advantage of these trends. With the prodigious cash flow enabling them to continue to significantly reduce their share count over time, the returns of the latter would be phenomenal if it happens. The downside of the former case is, of course, that they keep going down to zero, while buying back shares that with hindsight proved overvalued. I’m not sure which will be reality. However, it is the mismatch between the limited downside and possibly significant upside that keeps me interested here.

However, I have been proved wrong by the price action so far and with a recent profits warning and a Momentum rank of 1, significant caution is required. For the moment Roland’s previous AMBER view feels about right.

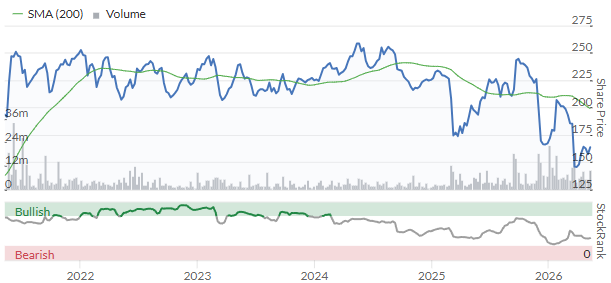

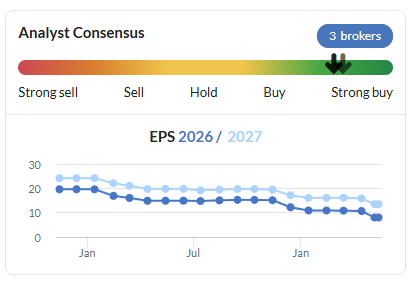

Watches of Switzerland (LON:WOSG)

Up 14% at 606p (£1.24bn) - FY26 Trading Update - Mark - AMBER/GREEN =

The market has liked this update for the year just ended which has shown double-digit revenue growth:

Full year Group revenue of £1,828 million, +13% vs prior year in constant currency (+11% reported)

o Excluding the FY26 53rd week, Group revenue was +11% in constant currency (+8% reported)

And most importantly:

FY26 Adjusted EBIT expected to be £152 - £155 million, ahead of previous guidance reflecting the improved sales performance

I can’t see them quoting the consensus in the RNS, but helpfully, they have it on their website:

That works out to be around 3.5% ahead, so perhaps not as material as the rise in the share price today suggests.

We can’t access any of the broker coverage here, so we need to go off the direct guidance for FY27:

- Revenue: 5 - 10% at constant currency

- Adjusted EBIT margin: 40 - 80bps expansion from FY26

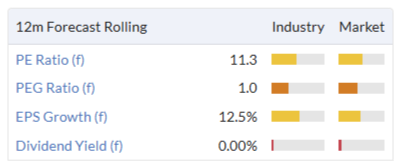

Taking the middle of this range would give £1,965m sales and £177m EBIT, up 15% from FY26. Despite a sea of orange on the valuation front, the PEG makes this look reasonable value if those sort of growth rates can be maintained over the medium term:

However, there are a couple of things to be cautious about:

Adjustments: all of these figures are on an adjusted basis, and we have been critical of the scale of adjustments in the past. We have yet to see what assumptions go into these adjusted figures.

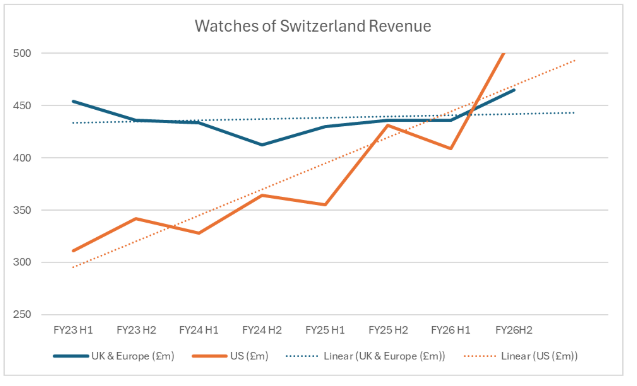

The US has been the stand out growth engine again and has exceeded UK & Europe revenue for the first time. The company is increasingly exposed to the US consumer, and as the issues last year showed, the vagaries of US tariff policy:

Whenever I cover this company, I can’t quite get this satirical article out of my head: https://www.thedailymash.co.uk/news/society/mans-luxury-watch-successfully-impresses-fellow-twats-20161024115895

It is funny because there is an element of truth about it. The luxury watch market is highly dependent on the view of luxury watches as a display and store of wealth. Much of the success of WOSG is based on the relationships they have built with key brands, and the perception that luxury watches hold their value. Part of this allure is restricting access to the most desirable watches and brands. Anyone investing here, should keep a very close eye on second hand watch trends, especially in the US.

While today’s rise in share price looks aggressive compared to the size of the upgrade, it also reflects the ongoing trend for the US market to grow rapidly. With the US an increasingly important part of the business, if this growth can be maintained over the medium-term the shares still don't look expensive. While the company continues to perform in the US ahead of expectations (even modestly), I am happy to keep our broadly positive view of AMBER/GREEN.

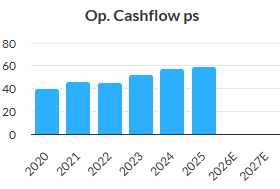

Microlise (LON:SAAS)

Down 16% at 49p (£67m) - Results for the year ended 31 December 2025 - Mark - BLACK/AMBER/RED =

Microlise must have thought it a great choice when they went for SAAS as a ticker when they listed in 2021. Things have perhaps not turned out how they imagined:

Although they've perhaps done no worse than any other late-2021 float. And it would have been hard for them to foresee that SaaS would become code for “disruptable” in 2026.

What management probably should bear some responsibility for is the following trend:

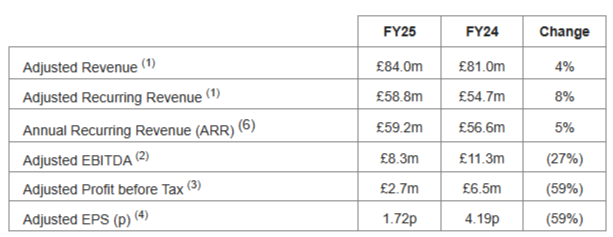

FY25 comes in at consensus, at least on an adjusted EBITDA basis:

EPS is a 15% miss against Canaccord Genuity’s previous forecast.

Statutory measures show a loss, and a quick look at the cash flow statement shows £2.5m spent on PP&E in the year, plus the same £2.8m capitalised intangibles, making adj. EBITDA a poor valuation measure to use for a business such as this.

Forecasts:

The real damage comes to future years, though. Despite an in-line Q1, they say:

As a result of the above investment and a challenging market environment we expect FY26 revenues to be slightly below current market expectations and adjusted EBITDA to be at the lower end of current market expectations.

In response, Canaccord reduces FY26E Adj. EPS by 39% to 2.1p and FY27E by a whopping 61% to 3.2p. This is much more than the flesh wound that the share price response today suggests.

Perhaps even more worryingly, Canaccord reduces their FY27 net cash estimate from £20.4m to £6.2m. This is driven by working capital unwind, and a material increase in capex expectations. Again this shows why we shouldn’t use EBITDA to value this business. At the former level, it would be around 30% of the market cap and make a difference to the valuation, now it is around 10% which is not as material.

Valuation:

At 48p the forward P/E is around 23, and while it falls to 15 for FY27, it would seem foolhardy to put too much faith in that figure. It is tempting to think that a share price that has more than halved over the last year means the company looks cheap. However, not in this case, it seems.

Mark’s view

Despite the share price halving since Graham reviewed their last profits warning, the scale of today’s broker downgrades to future years means the shares still don’t look good value. The net cash that may have provided some kind of valuation support in the past looks committed to capex with highly uncertain payback. Perhaps the time to buy will be when the market becomes so disgusted with the word SaaS that Microlise feels forced to change their ticker! In the meantime, our broadly negative view remains. AMBER/RED.

Eurocell (LON:ECEL)

Flat at 104p (£103m) - Trading Update - Mark - AMBER/GREEN =

An unsurprisingly downbeat AGM statement on the market conditions:

Trading conditions have remained subdued in 2026. Ongoing challenging macroeconomic conditions and weak consumer confidence have been compounded by uncertainty over the impact of conflict in the Middle East on demand and supply chains. This has continued to affect activity levels in both the repair, maintenance and improvement (RMI) market and new build housing.

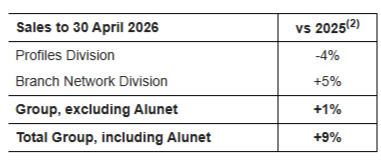

I am actually surprised that branch network sales have done as well as they have:

They may view this as a bit of an anomaly, though, as they also say:

New branches create a short-term drag on profitability but enable longer-term profit improvement. Whilst we have identified further potential new sites, we have temporarily paused the opening programme until there is better visibility over the general economic outlook.

Buybacks are flagged as continuing, although with a get out clause if things should deteriorate:

As previously announced, our intention remains to continue share buybacks in due course, assuming no prolonged impact from the situation in the Middle East and subject to maintaining a strong financial position.

They also flag the Alunet earnout needing to be paid, and some IT investment. Overall, they seem comfortable with the headroom on their facilities that were renewed recently, so I see the buybacks as likely to continue.

They are quite vague on forecasts, though, commenting that:

However, the effect of this backdrop on consumer confidence and new build housing market activity over the near term remains difficult to assess, which is reflected in the range of analysts' forecasts for the year.

Company compiled range of analysts' forecast adjusted profit before tax for the year of £21 million to £23 million.

It seems notable to me that they highlight the range of forecasts (that doesn’t actually look that wide to me), but don’t explicitly say they are trading in line with these.

They have two brokers, neither of which we can access. This seems far from ideal for a £100m market cap company. So I wouldn’t be surprised to see the consensus here tweaked downwards over time.

Mark’s view

The lack of explicit in-line statements is a little worrying. Given the market backdrop I wouldn’t be surprised to see some modest downgrades over time. However, this is undoubtedly a cyclical industry and the current valuation multiples have quite a lot of wriggle room while still being able to be described as cheap:

They continue their buyback, and while they may be pausing their branch roll-out they still have long-term growth potential. So I struggle to be too negative at current levels and keep our broadly positive view of AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.