Good morning!

Well done to Roland and the entire team for their coverage over the last two weeks, while I had a break in northern Spain.

I managed to remove myself from following the daily news cycle most days - but not on the day of Volvere's full-year results! (I hold.) One of the costs of running a highly concentrated portfolio is that you never get to fully switch off.

In macro news, the growing importance of UK politics has been a key theme, with the potential for instability and/or a more free-spending PM motivating traders to bet heavily against the pound. There has also been a further rise in the 10-year bond yield:

1-year chart from Trading Economics.

The other major macro issue is of course the US-Iran conflict, which remains in an impasse.

It's not wonderful mood music for investing, but macro news rarely is all that uplifting. Let's move on and look at today's company news!

Key overnight indicators:

- The FTSE is set to open down 0.5% at 10,140

- The S&P is trading down 0.6% at 7,360

- Brent Crude futures are up 1.7% at around $111

- UK natural gas futures are up nearly 3% at 128.6p per therm.

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£211bn | SR78) | Baxfendy approved in the US for hypertension & Enhertu approved in two HER2+ early BC settings | Baxfendy approval based on BaxHTN Phase III results showing statistically significant and clinically meaningful reduction in systolic blood pressure in patients with uncontrolled or resistant hypertension. Enhertu approved in the US for two new indications for patients with HER2-positive early breast cancer | |

GSK (LON:GSK) (£75bn | SR92) | First RSV vaccine approved for adults aged 18-59 years at increased risk and for all adults 60 years and older in Japan. | ||

Anglo American (LON:AAL) (£45bn | SR56) | Agreement re sale of steelmaking coal business & Update re Collahuasi environmental permit in Chile | Agreed sale of steelmaking coal mines in Australia to Dhilmar for cash consideration of up to US$3.875bn, proceeds to reduce debt. Collahuasi: the environment authorisation for an ongoing upgrade project has been withdrawn by the Chilean authorities. Anglo doesn’t expect any immediate impact on production. | |

Standard Chartered (LON:STAN) (£42bn | SR89) | Appoints Manus Costello as Group Chief Financial Officer. He was previously Global Head of IR. | ||

Molten Ventures (LON:GROW) (£1.02bn | SR90) | Generated proceeds of c.£63m from a further partial sale of Molten’s Revolut holding, taking Revolut realisations to date to c.£120m (20x invested capital). Remaining Revolut holding valued at c.£110m. | ||

Kainos (LON:KNOS) (£953m | SR46) | Revenue +17%, adj pre-tax profit up 2% to £67.1m. With adj EPS +7% to 41.1p, slightly ahead of expectations. Year-end contracted backlog +18% to £433.9m. Outlook: expect “another positive year”. Sees AI as the biggest opportunity since cloud computing. | AMBER ↓(Roland) I think this is a decent set of results and remain broadly positive on the medium-term prospects for Kainos, but I think some caution may be prudent while we see if last year’s momentum can be maintained while repairing the damage to profit margins caused by a ramp-up of contractor staff. I’ve moved down to neutral today to reflect my view that the valuation is probably about right and my niggling concern that the company did not see fit to mention its view on FY27 market expectations in today’s outlook statement. | |

| Advanced Medical Solutions (LON:AMS) (£544m | SR60) | TA Associates - No Intention To Make An Offer for AMS (15/5 pm) & Response to TA Associates Announcement | SP -20% Late on Friday evening, would-be bidder TA Associates announced that they would not be making an offer for AMS (see here, previously). This morning, AMS’s Board has issued a statement reiterating its confidence in the company’s standalone prospects. | |

Hays (LON:HAS) (£480m | SR34) | Appointed Mark Dearnley as CEO with immediate effect; he has been interim CEO since 27 Feb 26. | ||

Harworth (LON:HWG) (£419m | SR18) | “To date, we have completed, conditionally exchanged, and are in legals on 63% of our 2026 sales pipeline, with sales completion being back-ended in the year.” Seeing some cost inflation and persistent longer transaction timelines. | ||

Capita (LON:CPI) (£381m | SR27) | SP +6% Year-to-date revenue +2.9%, in line with expectations. Making good progress with sale of private sector contact centre business. Capita’s main Public Service division has grown revenues by 5.8% in the first four months of the year. Contracts won year-to-date were worth £750m, up 20% year-on-year. Reiterates plans for c.£40m of cost savings across 2026 and 2027, with a cash cost to achieve these savings of £20m. Expecting positive free cash flow, before the impact of business exits, in 2026. | AMBER/RED = (Graham) [no section below] I analysed the sale of Capita’s contact centre business in March: the buyer is taking very little risk but if it works out, the defcon to Capita could be material (£61.5m). For me, the main attraction of the disposal long-term is the simplification of the group, including the removal of Contact Centre’s empty revenues. This deal is planned to complete by August. Meanwhile, Capita’s remaining businesses are working hard to increase automation and increased productivity via AI tools. I’d like to upgrade our stance here back to neutral, and the “contracts won” figure is encouraging. However, the most recent £143m net debt figure (Dec 2025) prevents me from upgrading. I don’t consider Capita to be distressed, but neither do I think the company’s balance sheet makes for an appetising investment, given its struggles. There are very large leases on top of that financial net debt figure. No dividends or material buybacks here since 2017/2018. | |

Franchise Brands (LON:FRAN) (£293m | SR62) | Appoints Neil Miller as chief financial officer from 26 May, he was previously CFO at Praesidiad, a PE-backed security solutions group. Current CFO will step down from Board on 26 May and become Group Delivery Director. | ||

Winvia Entertainment (LON:WVIA) (£237m | SR43) | Acquired Rev Comps, a digital prize draw platform for £11.8m + potential earnouts. Rev Comps generated revenue of >£80 million and pre-tax profit of c.£2.1m during the year to 31 May 25. | ||

Alternative Income REIT (LON:AIRE) (£58m | SR55) | 24% shareholder Clenstone has made a possible offer, without “any offer price or range of prices”. Glenstone previously made a 66.5p possible offer in Nov 25, which the AIRE Board rejected. | PINK | |

Cora Gold (LON:CORA) (£73m | SR28) | 1m oz MRE announced for Sanankoro in Jan 25 totalling 31.4 Mt at 1.04 g/t Au for 1,044 koz – a 13% increase in contained metal from the 2022 MRE. | ||

Ariana Resources (LON:AAU) (£49m | SR44) | 13.6% interest in Zenit sold to Özaltin for gross cash proceeds of $19.2m, or c.$17.2m after local taxes. Ariana retains a 9.9% interest in Zenit and now has pro forma cash and investments of £29m with no debt. | ||

Staffline (LON:STAF) (£43m | SR84) | “The Board remains confident that, notwithstanding the ongoing challenging macro-economic backdrop, FY 2026 results will be in line with management expectations.” | GREEN ↑ (Graham) On balance, I think it’s reasonable for me to stick my neck out and go GREEN on this. It would be very easy for me to stay AMBER/GREEN, but this looks like a reputable company at 6x earnings, trading well, growing, and with an OK balance sheet. | |

Blencowe Resources (LON:BRES) (£39m | SR8) | Graphite estimates: The maiden Beehive JORC Mineral Resource adds 21.3 Mt (Inferred) and increases total Orom-Cross JORC Mineral Resources to 64.3 Mt (Measured + Indicated + Inferred) across Northern Syncline, Camp Lode, Iyan and Beehive. | ||

Synectics (LON:SNX) (£36m | SR84) | Trading in the first five months of FY November 2026 broadly in line with management expectations. Expecting an H2 weighting, as before. Subject to energy sector activity normalising through the second half, the Board currently expects trading for FY 2026 to be in line with market expectations. | AMBER/RED = (Roland) Today’s update stops short of cutting full-year guidance, but in my view it does suggest a heightened risk that earnings could fall short of forecasts this year. The market seems to have taken a similar view, marking the stock down sharply this morning. While I am generally positive on this business, last year’s strong profits appear to have been highly exceptional. This factor plus the ongoing restructuring leaves me feeling cautious. When combined with the uncertain outlook for Energy-related projects, I think it’s logical to maintain my moderately negative view today. | |

Manx Financial (LON:MFX) (£34m | SR46) | Net assets rise from £37.3m to £43.6m. Normalised PBT £8.6m (2024: £8.3m). Basic EPS 5.33p (2024: 6.87p). Outlook: The economic backdrop in the Isle of Man and the UK remains uncertain… At the same time, these conditions are creating opportunities for the Group to support customers through both our existing and new short-term financing products. | ||

Celebrus Technologies (LON:CLBS) (£33m | SR50) | Buyback programme of up to 1 million shares. The Company intends to hold all Ordinary Shares so purchased in treasury for the purpose of satisfying future obligations in relation to its employees' or other share schemes. | (Graham note - this buyback is for the benefit of employees, not shareholders.) | |

Eenergy (LON:EAAS) (£22m | SR60) | CEO steps down by mutual agreement and with immediate effect. Will leave the company at the end of May “to pursue other opportunities”. He is very briefly thanked. The CFO becomes interim CEO. | ||

Europa Oil & Gas (Holdings) (LON:EOG) (£19m | SR18) | North Yorkshire Council: Local Planning Authority has issued its decision to refuse planning permission for the Cloughton gas appraisal well. Europe is assessing its options “with a view to appealing the decision and is confident that on appeal the planning permission will be approved”. | ||

88 Energy (LON:88E) (£14m | SR26) | South Prudhoe total gross unrisked 2U Prospective Resources increased ~35% to 768.9 MMbbls, of which 640.7 MMbbls net to 88E. | ||

Cellbxhealth (LON:CLBX) (£13m | SR5) | Collaboration with AdventHealth, one of the largest faith-based health systems in the United States, for the use of CelLBxHealth's Parsortix® platform in two clinical studies. | ||

Kazera Global (LON:KZG) (£12m | SR2) | Kazera owns an interest in a tantalum and lithium project in southern Namibia, “Aftan”. There are “continued and growing expressions of interest received in relation to the development of Aftan”. “Evaluation ongoing regarding potential strategic pathways available to Kazera in relation to its interest in Aftan.” | ||

Empresaria (LON:EMR) (£11m | SR54) | SP +7% Revenue -3% (+2% LfL). Loss before tax £4.4m (2024: £5.2m). Strategic focus: “stabilising the business and eliminating loss-making activities”.Outlook: “The challenging economic environment… has continued into 2026… trading outlook remains uncertain at the macroeconomic and global political levels.” | AMBER/RED = (Graham) [no section below] It’s a poor set of results here as would be expected at an £11m market cap, although on an adjusted basis there is some cause for optimism with an 82% increase in adjusted PBT to £4m. Adjustments include a £5m impairment and £2m of “exceptional items”. The previous Board and management teams are blamed for getting strategy wrong, with Empresaria now returning to a decentralised model. Unfortunately with the company having £17m of net debt I must maintain our cautious and moderately negative stance here - it’s nearly always a red flag when net debt exceeds the market cap, and Empresaria doesn’t have the track record to suggest that this debt load is comfortable. Hopefully the new management team can stop the bleeding, although headroom of c. £5m doesn’t sound like much to me considering the volatile cash flows typically experienced in the recruitment sector. I suppose this could be an interesting high-risk, high-reward type of bet at current levels for those who have conviction in the new Board. |

Graham's Section

Staffline (LON:STAF)

Up 7% at 39.65p (£46m) - AGM Trading Update - Graham - GREEN ↑

It’s a concise AGM update from this provider of blue-collar/industrial recruitment services.

Key points:

Gross profit up 14.6% in the first four months of 2026

Recruitment GB: 9.1% increase in temporary worker hours.

Recruitment Ireland: “strong start to 2026”.

Trading sounds very healthy:

This excellent operational performance is underpinned by a healthy new business pipeline, driven by organic growth and market share gains across Staffline's blue-chip customer base.

Buyback: £3.18m has been spent buying back 7 million shares at an average price of 45.36p (current share price 39.65p).

Outlook: in line with management expectations.

Estimates: Zeus and Panmure Liberum have both left profit forecasts unchanged, although they increase EPS estimates due to the falling share count.

Panmure Estimates for 2026:

Revenue up 17% to £1,298m

PBT up 24% to £9.2m

Fully diluted EPS up 36% to 6p

Diluted EPS is seen continuing to improve, to 6.8p in 2027 and 7.6p in 2028.

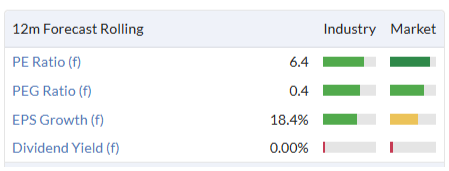

If we are happy to value the company on 2027 earnings, that gives a P/E multiple of less than 6x.

The more conservative “12m forecast rolling” calculation by Stockopedia gives a P/E of 6.4x:

Net cash was £1.5m in December 2025. Panmure suggest that this will fall in the current year before rising in 2027.

It’s worth noting that there is a high degree of seasonality and that cash flows can be volatile in the short-term: Panmure say that net debt at the end of H1 could be £9m as the company sees a temporary outflow arising from its huge contract with food and drink logistics provider Culina. This Culina contract already contributed to a hefty £8m cash outflow in 2025.

Graham’s view

Growth-oriented, temporary cash drain is something that I always try to embrace, but the £9m H1 net debt estimate does stand out to me. It’s a reminder that recruitment companies need a high cash balance at some points in the year, in order to balance out the negative cash flow they experience at other times.

Hopefully Culina doesn’t ever run into any financial difficulties of its own, as that could become very awkward for Staffline.

As for the overall merits of Staffline as an investment, I already upgraded our view on this stock to AMBER/GREEN in January.

Within the recruitment sector, this one is different, due to its blue-collar focus. I imagine that it’s somewhat less prone to technological disruption than white-collar recruiters (who have to be masters of LinkedIn and various other tools). And recent Stafflin updates have been very strong - beating expectations for 2025, producing very clean profits without adjustments, and currently on track for another good result in 2026.

Another positive is that recent growth has also been organic: the last major M&A deal by Staffline was a £12m disposal last year.

On balance, I think it’s reasonable for me to stick my neck out and go GREEN on this. It would be very easy for me to stay AMBER/GREEN, but this looks like a reputable company at 6x earnings, trading well, growing, and with an OK balance sheet.

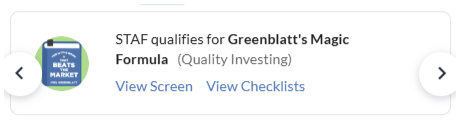

It passes my favourite stock screen, The Magic Formula, along with Jim Slater’s ZULU Principle and Tiny Tiny Titans.

And while Momentum has been weakening, it is still a Super Stock:

A few risks in closing:

Economic exposure to various industries: security, driving, logistics.

Possible customer concentration risk with Culina.

The year-end net cash balance can be deceiving; watch out for temporary cash drain.

There has been no dividend since 2018 but at 6x earnings, I appreciate their preference for buybacks - although I hope this doesn’t kick off another marathon buyback debate in the comments!

Roland's Section

Synectics (LON:SNX)

Down 12% at 180p (£31m) - AGM Trading Update - Roland - AMBER/RED =

I am relieved to see I downgraded this security and surveillance system group to AMBER/RED when I last looked at the company’s full-year results in March.

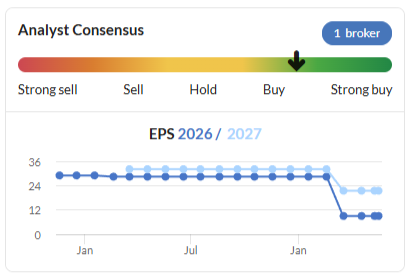

My decision was prompted by a weak forecast for FY26 suggesting a 10% drop in revenue this year as the contribution from a large one-off contract dropped out of the numbers. It seems that the company’s failure to maintain FY25 profitability had not previously been priced into broker forecasts, which were cut by more than 50% following March’s results:

The announcement of a “Strategic Update” in March also led me to think a measure of caution might be appropriate.

Today’s AGM update is in line, but only just, in my view. Let’s take a look.

Trading commentary

Positive activity has continued across a number of the Group's core markets with trading in the first five months of the year ending 30 November 2026 ("FY 2026") broadly in line with management expectations.

Leisure and hospitality: strong order intake in the North American gaming market, secured contracts with new customers.

Includes largest contract win to date in Canada, providing a surveillance solution for a large-scale casino and integrated resort in Ontario.

Critical Infrastructure, Public Space & Transportation: secured additional contracts with new and existing customers, including a recent win totalling over £1.4m with a UK regional authority, covering approximately 220 buses.

Energy: geopolitical uncertainty has led some customers to delay project and infrastructure investment decisions, “although the scale and quality of these opportunities remain unchanged”. As a result, “the timing of certain contract awards and project activity” is unclear at this stage.

Outlook

Revenue and profitability for the full year will be weighted towards the second half of the year, consistent with the historical profile of the business.

Leaving aside the exceptional result from last year, profits do indeed seem to have been H2-weighted in recent years.

However, achieving full-year guidance is dependent on conditions in the Energy sector returning to normal:

Subject to energy sector activity normalising through the second half, the Board currently expects trading for FY 2026 to be in line with market expectations.

Synectics helpfully specifies market expectations as being FY26 revenue of £62m and adj EBITDA of £4.1m. The equivalent figures for FY25 were £68.1m and £8.5m.

This means that even if the company meets expectations, EBITDA is expected to halve this year.

March’s forecasts from house broker Singer Capital suggest the reduction to earnings per share could be even greater – with FY27 profits also expected to remain below FY25 levels:

FY25 actual adj EPS: 27.8p

FY26E adj EPS: 9.0p

FY27E adj EPS: 21.5p

One bright point is that the company has plenty of cash to support its turnaround and manage any temporary weakness in trading – net cash was £14m at the end of November 2025.

Roland’s view

While CEO Amanda Larnder says the company is making “good progress with its strategic transition”, I would probably reserve judgement until there’s some evidence of renewed growth or improved profitability.

The market reaction to today’s update suggests investors are pricing in a profit warning later this year. I think it’s fair to suggest the odds of this have increased.

Although today’s update is in line, achieving current guidance depends on energy market conditions normalising quickly enough to rescue an H2-weighted forecast. I am not sure how likely this is.

While earnings are expected to rebound from FY27, Synectics’ valuation looks up with events to me given the uncertainty around the outlook and some rather average quality metrics:

It’s probably worth noting that while the StockRanks style this as a Contrarian opportunity with high value and quality scores, this is based on last year’s exceptional results and doesn’t reflect the drop in profit expected this year:

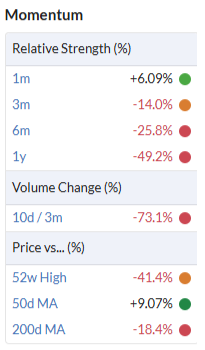

In my view, the low MomentumRank is probably more relevant to this situation. In addition to the prior cut to earnings guidance I flagged above, technical momentum has also been weak recently:

I am going to leave my previous AMBER/RED view unchanged today.

Kainos (LON:KNOS)

Down 1% at 808p (£945m) - Full Year Results - Roland - AMBER/GREEN =

This UK-based IT services provider provides outsourced digital services and has a specialism in Workday (NSQ:WDAY), providing a range of product development and consulting services for this enterprise software platform.

Kainos has a particularly strong presence in the UK public sector and healthcare markets, although around one-third of revenue now comes from North America.

Today’s results cover the year to 31 March and show strong growth, with earnings slightly ahead of expectations. There’s also a matching increase in the order backlog, but markets seem strangely unexcited.

Let’s take a look.

FY26 results highlights

Here are the headline figures from today’s results:

Revenue up 17% to £431.1m

Adjusted pre-tax profit up 2% to £67.1m

Reported pre-tax profit up 19% to £58.1m

Adjusted earnings per share up 7% to 41.1p (Stockopedia consensus: 39.4p)

Net cash down 33% to £89.1m

Revenue growth was strong last year, but the group’s adjusted pre-tax profit margin fell from 17.9% to 15.6%. This was flagged in April and was due to the increased use of contractors and third-party suppliers to support growth following a series of contract awards.

In today’s commentary, management says this should unwind this year, improving margins:

As we replace temporary contractors with full-time employees over the course of the year, we anticipate clear margin improvement.

I don’t see last year’s dip as a big concern, given that the group’s operational metrics suggest that last year’s growth is being sustained into the coming year:

Bookings up 32% to £505.3m

Contracted Backlog up 18% to £433.9m

Product Annual Recurring Revenue (ARR) up 23% to £89m

The increase in the contracted backlog mirrors last year’s increase in revenue, giving me confidence that last year’s growth should be sustained in FY27.

The quality of Kainos’s profits also remains high, according to my sums:

Return on Capital Employed: 49.8%

Underlying free cash flow conversion from net profit: 92%

Divisional commentary

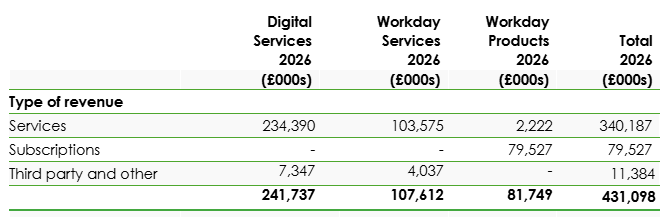

More than half the company’s revenue comes from its Digital Services business, with the remainder split across Workday Services (consulting/implementation) and Workday Products (add-on products for Workday). This latter unit is also the source of all of Kainos’s recurring revenue:

Source: Kainos FY26 results

Workday Products: revenue rose by 15% last year, with a 23% growth in ARR. “Almost 700 customers” now use Kainos’s Workday Products, with 41% using more than one.

The year-end backlog rose by 20% to £178.7m. These products generate a high gross margin, supporting investment in developing and marketing new products, which rose by 16% to £37.4m last year. I like to see companies maintaining investment in new products, especially in a rapidly-evolving market such as IT, where AI is disrupting many existing tools:

AI: the company notes that while it currently charges by user, it has options available to switch to usage or consumption-based pricing. This is expected to be a common theme as AI agents replace human users. Kainos says it does not expect any change to the overall level of our pricing [as a result of AI].

Digital Services: revenue rose by 23% last year, with bookings up 29% supporting a contracted year-end backlog of £180m.

The company says that in both the public and healthcare sectors, customers are increasingly awarding larger and longer contracts. The company is focusing on these high-value opportunities, “which deliver greater returns relative to the effort required to win them”.

Equally, Kainos continues to pursue smaller contracts selectively, where they provide an opportunity to build relationships with new customers.

The revenue base is heavily skewed to UK government departments and agencies:

Public Sector +11% to £136m;

Healthcare (NHS) +55% to £74.9m;

Commercial +4% to £10.7m;

North America +127% to £20.2m.

Some example contract wins provide a flavour of the type of work undertaken:

Home Office: support the digital infrastructure for managing people and goods at the UK border;

Department for Transport: run, maintain and improve its bus data services;

Driver and Vehicle Standards Agency: deliver a platform making it easier to schedule driving tests;

NHS: “won significant contracts with NHSE”, including a Digital Health Checks project to improve access to vaccinations and screenings. The company sees “greater use of technology in the health service” and has not experienced any disruption to contract awards due to the government’s plan to bring NHS England back under direct control.

Workday Services: Kainos is a “leading” Workday partner in Europe and a full services partner in the US. At the end of the year the company had 944 accredited Workday consultants (FY25: 809).

Workday services revenue rose by 9% to £107.6m last year, but rose by 12% in North America. EMEA was 1% lower.

Sales bookings increased by 44% to £121.8 million (2025: £84.6 million) and the contracted backlog at the year end was £74.9 million (31 March 2025: £59.3 million). The strong sales performance in the year reflected our focus on our core strengths in complex deployments, which helped us to win more large consulting contracts.

Outlook

Slightly disappointingly, Kainos does not explicitly mention FY27 expectations in today’s outlook commentary. Arguably, this leaves the door open for a subtle broker downgrade without an explicit profit warning.

Guidance for the year ahead is more general, noting “long-term structural drivers” in its markets and providing a non-specific comment on "near term" expectations:

Our near-term performance is supported by a healthy pipeline, a significant contracted backlog and a strong balance sheet.

For FY27 specifically, the company anticipates:

Continued momentum in Workday Products, achieving ARR of £100m by the end of 2026;

Further growth in Digital Services;

Another “positive year” for Workday Services, with a continued focus on “complex deployments” and consulting opportunities linked to the company’s own products.

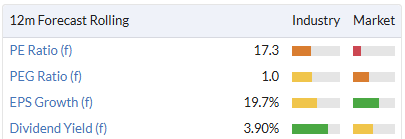

I don’t have access to any updated broker notes today, but consensus estimates on Stockopedia suggest double-digit earnings growth this year:

FY26 actual adj EPS: 41.1p

FY27E adj EPS: +15% to 47.2p

If unchanged, these estimates price the shares on a 17x multiple for the year ahead, with a 3.9% yield:

Roland’s view

At face value, I think today’s results are pretty decent. The only caveat to this is the loss of profitability last year due to the increased use of contractors.

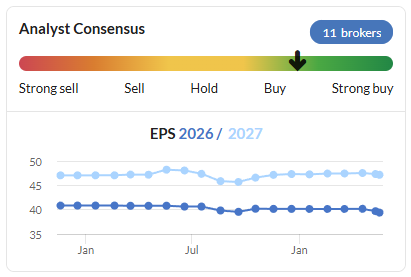

Assuming this trend reverses in FY27 as guided by management, I don’t see any reason to doubt current market forecasts for continued growth. Broker consensus has been largely stable over the last year and the lack of share price movement today suggests to me there have been no major revisions to analysts’ estimates:

At the same time, I can’t help noting the falling StockRank and weak share price action over the last six months:

My concern is increased by the company’s rather vague guidance today, with no mention of FY27 expectations.

The StockRanks may take a more positive view when Kainos’s FY26 results are digested. But the algorithms currently style this business as a Falling Star, a style I have learned it is often best to avoid.

There’s also a risk the market has spotted some looming weakness that’s not yet obvious from management commentary. On the other hand, I think it’s possible that Kainos has also just been the victim of the ‘SaaSpocalypse’ – the fear that AI will erode such companies’ business.

Personally, I don’t think that’s likely. I am increasingly of the view that companies such as Kainos may be net beneficiaries of AI, as long as they are able to demonstrate the value it can provide for clients.

Despite this, I’d argue that a forward P/E of 17 is probably about right for a business of this kind, especially given the concerns I’ve flagged above. For this reason I’ve decided to cut my view by one notch to neutral today, while we wait to see if Kainos can maintain last year’s momentum while repairing its margins.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.