Good morning! I’ll be with you for the end of the week.

News organisations this morning are reporting that the US and Iran are close to a deal that would extend the ceasefire for 60 days and launch talks on the future of Iran's nuclear programme. US officials said that the two countries have agreed on a framework of a deal, pending the approval of Trump and Iran's leadership. However, Iran's semi-official Tasnim news agency denied this and JD Vance told reporters that "We're not there yet, but we're very close and we're going to keep on working at it".

As seems to be the case at the moment, financial markets are looking on the bright side of life and pricing in a deal, but not an immediate return to the pre-war level of oil flowing through the Straits of Hormuz.

In economic news, the U.S. Personal Consumption Expenditures (PCE) price index recently registered its highest annual jump in three years, pushing long-term U.S. bond yields higher. Elevated inflation numbers and the potential weakening of the petrodollar system due to the impact of the Iran war are challenging the traditional role of the U.S. Treasuries as a safe haven.

Overnight market movements:

The FTSE is set to open flat at 10,437

S&P 500 is up 0.1% at 7,570

Brent crude (July delivery) is down 1% at $91.80

Gold is up 0.3% at $4,508

Bitcoin is flat at $73,600

Spreadsheet accompanying this report: link

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£213bn | SR71) | AstraZeneca's Imfinzi (durvalumab) in combination with Bacillus Calmette-Guérin (BCG) induction and maintenance therapy has been approved in the US for the treatment of adult patients with BCG-naïve, high-risk non-muscle-invasive bladder cancer (NMIBC). | ||

Drax (LON:DRX) (£2.72bn | SR95) | Commissioning of Hirwaun Power Station, the first of three 299MW Open Cycle Gas Turbine plants which Drax is developing, is now complete and Drax has assumed commercial control from the developer Metlen Energy & Metals. | ||

Ocado (LON:OCDO) (£1.75bn | SR28) | Ocado and Asda have agreed to enter a partnership to develop Asda's online business across the UK. Focus will be to quickly replace and upgrade Asda's existing ecommerce infrastructure, with Ocado's solutions to be rolled out across both stores and dark stores from 2027. No material financial impact on FY26. Expects to turn cash flow positive during the second half of this financial year, with Full Year cash flow positivity expected in FY27 | ||

Great Portland Estates (LON:GPE) (£1.26bn | SR30) | Has pre-let over 13,000 sq ft of Fully Managed offices at Elsley House at an average rent of £260 per sq ft, 4.4% ahead of the new March 2026 ERV. | ||

Avacta (LON:AVCT) (£346m | SR12) | Richard Hughes, one of Avacta's non-executive Directors, will become non-executive Chairman | ||

Serabi Gold (LON:SRB) (£261m | SR99) | Unaudited interim results for the three-month period ended 31 March 2026 | Gold sold 10,323oz. EBITDA +135% to $29.2m, PAT +138% to $21m. AISC $2,293/oz. Net Cash $64.4m (31 Dec: $43.9m) | AMBER/GREEN (Mark - I hold) These are impressive results versus the prior Q1, but not versus Q4 last year. Looking at the details, this was only due to timing of gold sales and if we normalised for these, the quarter would have been even stronger. A big rise on AISC may be concerning but is largely due to how costs are accounted for. Direct costs in the income statement look well-controlled, although I am expecting some cost inflation for the rest of the year. Taking the higher AISC does take the edge off my valuation model. However, FY26 looks set to be a great year, despite recent weakness in the gold price. There appears to be enough upside left at the current price in all but the most extreme downside scenarios. As such, I am happy to maintain our previously mostly positive view (and my shareholding). |

Pulsar Helium (LON:PLSR) (£168m | SR28) | Has acquired approximately 1,360 acres of surface land in Lake County, Minnesota, located within its flagship Topaz Project for $2.5m. | ||

Borders and Southern Petroleum (LON:BOR) (£101m | SR69) | Operating Loss $1.4m (2024: $1.2m), Cash $2.5m (2024: $2.1m) after a $2.8m capital raise in period. Active dialogue re the farm-out of Darwin [corrected from Sea Lion, where they don't have a stake] with multiple interested parties | ||

Clean Power Hydrogen (LON:CPH2) (£68.3m | SR19) | In the final stages of testing the unit experienced an unexpected error, causing it to commence a standard shutdown procedure. During that shutdown procedure, the unit experienced an incident which has caused significant damage to the equipment. Operations suspended. Engaged in discussions with certain existing shareholders and prospective new investors regarding a potential equity capital raise. Ongoing uncertainty regarding the Company's financial position. Shares Suspended. | BLACK/RED = (uncertainty regarding the Company's financial position) Commiseration to any holders here. The best outcome appears to be a very discounted equity raise, the worst outcome is insolvency. I’m pleased to say Graham had already been highly negative on this company when he looked at it a year ago, meaning that he had called the risky nature of this venture correctly. It will be no surprise that today’s events won’t lead to an upgrade in our stance! | |

Blencowe Resources (LON:BRES) (£43.3m | SR10) | Revised commercial model increases NPV10 by 15% to US$1.254 billion over the initial 15-year life of mine. Cost increases reduce IRR . | ||

Time Out (LON:TMO) (£37.9m | SR15) | Time Out Market Vancouver is now open to the public. | ||

Churchill China (LON:CHH) (£37.4m | SR75) | Hospitality sales remain broadly in line with expectations. Ongoing focus on efficiency and productivity will continue to deliver benefits. Awaiting detail of government support for the UK ceramics industry. | BLACK(broadly in line)/AMBER/GREEN = (Mark) This “broadly in line” short update potentially kicks any recovery in the top line into the long grass and it's tempting to take a more negative view today. However, Roland only just upgraded this on a long-term valuation disconnect. This remains despite obvious end-market weakness. So I am adopting a wait-and-see approach today. | |

Kavango Resources (LON:KAV) (£35.2m | SR5) | Peter Wynter Bee, currently Interim Chief Executive Officer and Non-Executive Chairman, to step down on 1 July. Donald McAlister, currently Executive Interim Finance Director, will assume the role of Non-Executive Chairman and Interim Chief Executive Officer | ||

Europa Oil & Gas (Holdings) (LON:EOG) (£19.7m | SR18) | Has received approval from the Ministry for Mining and Hydrocarbons Department of Equatorial Guinea required to complete the Farm-out Agreement with Fuhai. Deal remains subject to Overseas Direct Investment approval from the Shandong Provincial government. | ||

Cellbxhealth (LON:CLBX) (£19.7m | SR8) | Has entered into a Master Services Agreement with AstraZeneca establishing CelLBxHealth as a qualified service provider to AstraZeneca, enabling the Company to support drug discovery and development through CTC powered analytics of clinical trial samples using the Parsortix® platform. | ||

Great Western Mining (LON:GWMO) (£17.7m | SR27) | Loss €1.08m (2024: €1.74m loss). Net assets -10% to €8.6m. Cash €0.07m. £3.5m capital raise post-period-end. | ||

Itaconix (LON:ITX) (£13.8m | SR19) | Has filed a patent application covering paint formulations incorporating BIO*Asterix® ingredients. Signed an agreement with an established specialty paint company to support the completion and evaluation of initial paint products using BIO*Asterix® ingredients. | [This is an RNS-Reach] | |

Medpal AI (LON:MPAL) (£10.1m | SR1) | Revenue £1.6m (25H1 £0m), Loss £3.27m, Net Debt excl. leases £300k, after £3.27m raise in period, £4.0m raised post-period end. “Management forecasts pharmacy-level EBITDA breakeven at a combined run rate of 80,000 items per month, expected to be achieved in Q4 2026.” |

* Market caps at previous trading day’s close

Mark’s Section:

Serabi Gold (LON:SRB)

Up 3% at 352p (£261m) - Unaudited interim results for the three-month period ended 31 March 2026 - Mark (I hold) - AMBER/GREEN =

(At the time of writing, I hold a long position in the stock.)

Production and cash figures were already released in their ops update. However, these are still impressive year-on-year results:

- Cash held at 31 March 2026 of $64.4 million (31 December 2025: $49.2 million).

- Company now debt free; repaid $5.3 million to Banco Santander in Brazil during the quarter. EBITDA for the three-month period of $29.2 million (Q1-2025: $12.4 million).

- Post-tax profit for the three-month period of $21.0 million (Q1-2025: $8.8 million).

- Profit per share of 27.72 cents (Q1-2025: 11.58 cents).

We also get a look at an updated balance sheet, where nothing looks out of place and it remains in a strong financial position given the net cash.

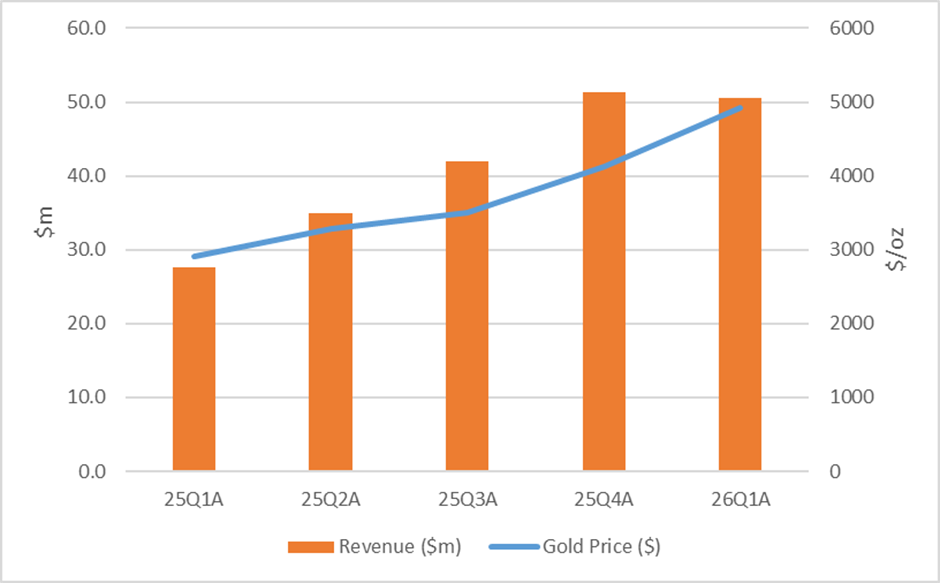

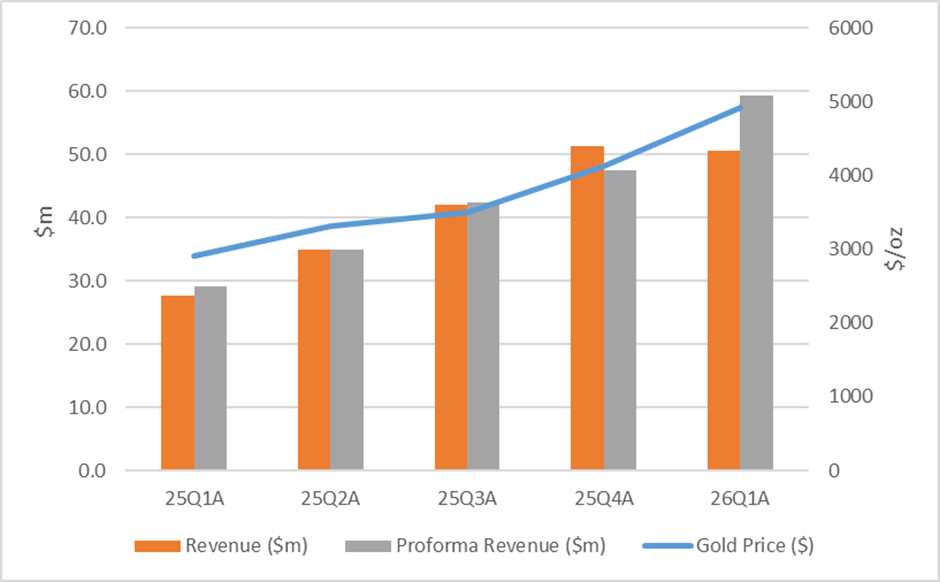

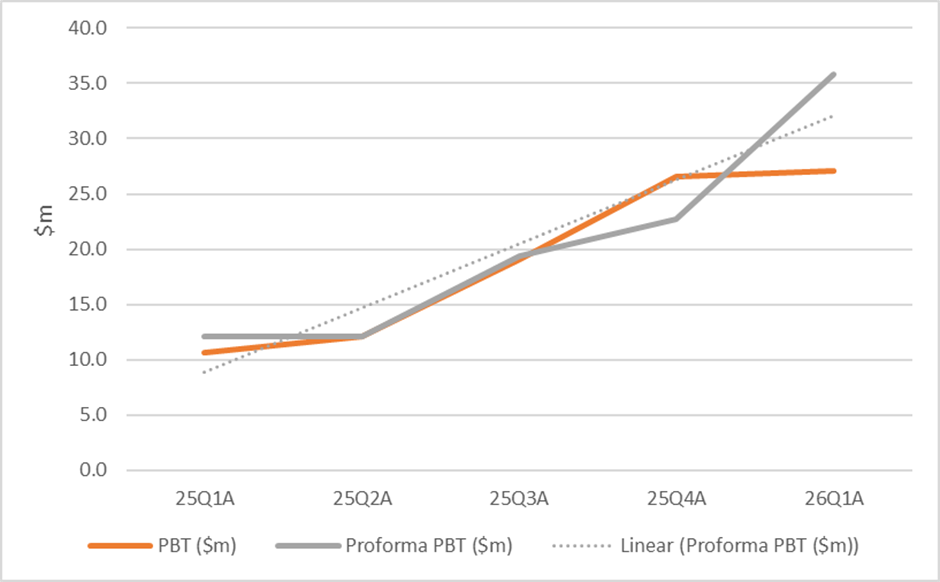

However, revenue and profits are less impressive compared to 25Q4. Revenue is flat despite a further rise in the gold price:

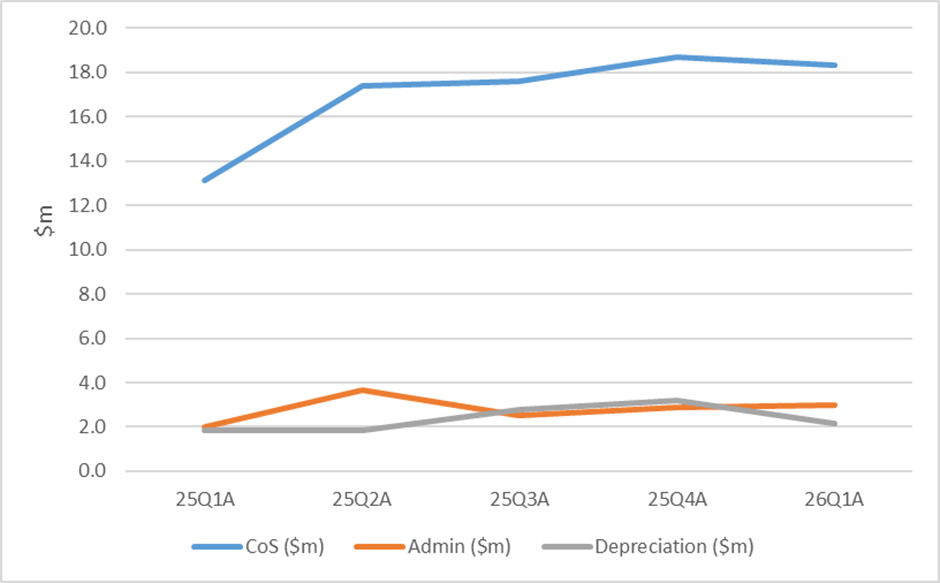

And cost of Sales has taken a big jump from Q1 last year:

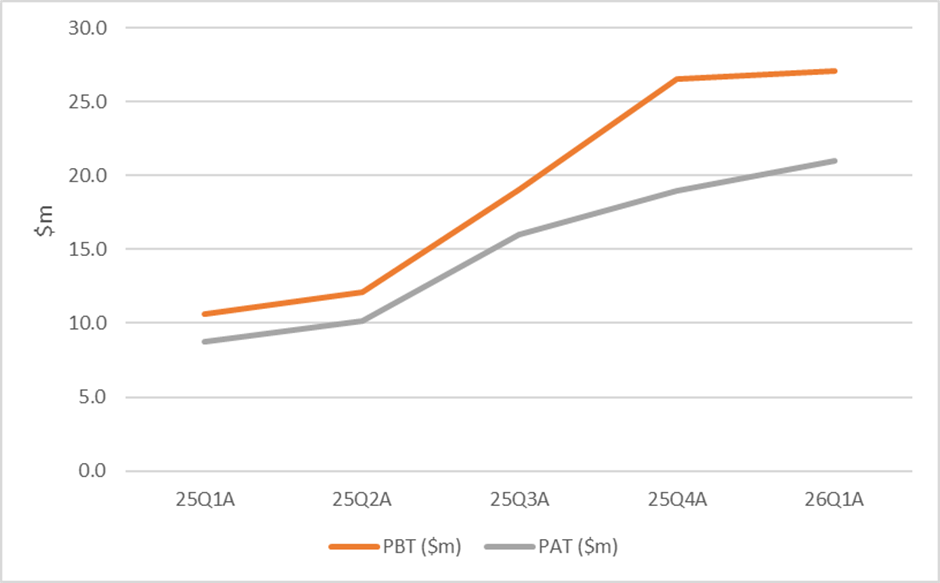

Meaning that PBT was flat quarter-on-quarter:

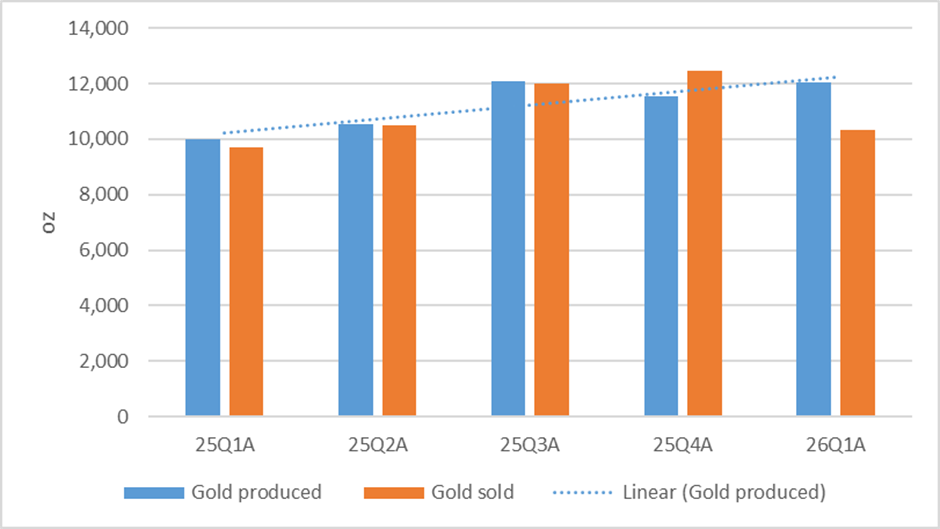

However, the reason for the flat revenue is that fewer ounces were sold than produced:

This is fairly normal and tends to reflect shipping timings and refinery schedules. We saw variations by quarter in FY25, but these evened themselves out. We can calculate the proforma revenue and PBT, as if they had sold exactly the ounces they had produced in that quarter:

Overall this shows that Q1 was a more impressive quarter than the initial numbers suggest (and Q4 last year less-impressive). Much of this improvement was due to the gold price rise, of course, but this doesn’t detract from the strength of the financials.

Cash Costs

The other potential concern is that cost/oz has faced a significant rise in the quarter, does this mean the company will be less profitable going forward?

- Cash Cost for the quarter of $1,863 per ounce (Q4-2025: $1,799 per ounce).

- All-In Sustaining Cost for the three-month period to March 2026 of $2,293 per ounce (Q4-2025: $1,818 per ounce).

[As an aside, if anyone is not sure about these metrics, here is a reminder of the definitions from my recent gold producers article:

Companies typically report and provide guidance on two cost metrics: Cash Cost and All-In Sustaining Cash Cost (AISC). The cash cost is the direct cost to produce one ounce of gold and includes mining costs, processing costs, on-site labour, energy and refining costs. However, it excludes corporate overhead, all capex or exploration costs, interest and taxes. It can be thought of like EBITDA for trading companies, useful to their bankers to protect against an extreme downside scenario, but not something to base a valuation on.

Much more useful for investors is the All-in Sustaining Cash Cost, which adds sustaining capex, admin and corporate costs, rehabilitation provisions, and adjusts for inventory movements. It still includes interest and taxes, but gives investors a good estimate of the operating profit per oz that a company will make at a given gold price.]

This is explained as:

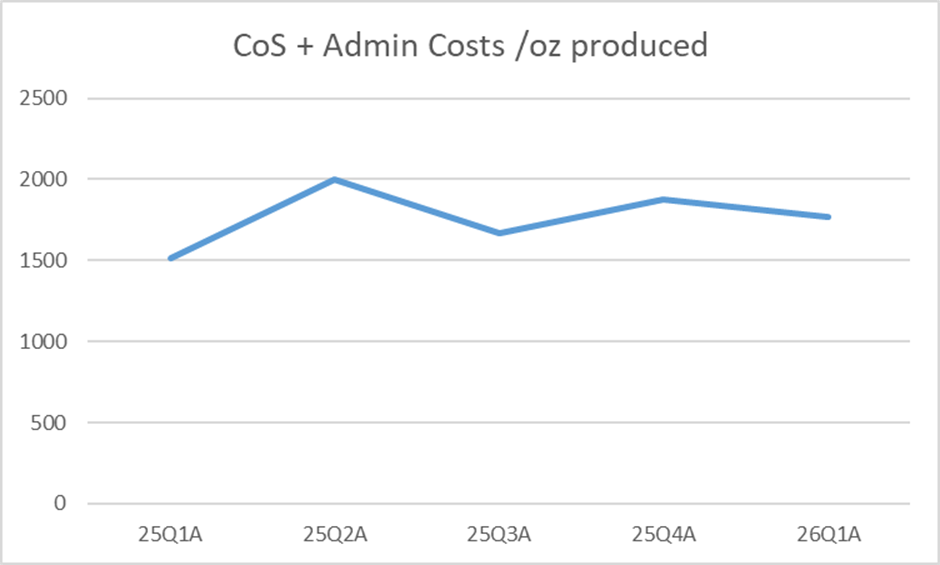

Cash cost and AISC are incrementally higher than Q4-2025, largely driven by the ramp up at Coringa. With the Meio zone now at commercial production, costs associated with mining the Meio zone are now included in cash cost and AISC.

This is due to the way these figures are calculated. Before commercial production, the costs were classified as capex or pre-operating development costs. Under international accounting standards, these expenses sit on the balance sheet and are not factored into the Cash Costs or AISC. Now that the Meio zone is officially "commercial," the accounting rulebook changes. The money spent to extract ore from this zone is now treated as an operating expense and these expenses are directly calculated into both Cash Costs and AISC.

This is more of an accounting change than a cost-rise due to cost inflation. My own simple calculation of CoS + Admin Costs/oz produced shows that this is fairly flat, although with significant variation quarter to quarter:

Broker Tamesis says that:

Cash cost and AISC were $1,863/oz and $2,293/oz, respectively, both tracking in line with our forecasts for the year (see Fig. 1)

But then the table they refer to just lists these exact figures. Not exactly helpful for confirming this claim!

Overall, this highlights that none of these metrics are perfect, as they all include or exclude some costs and have accounting judgments contained within them. AISC includes taxes, and I notice that tax rates calculated on a quarterly basis are nudging up toward the standard Brazilian corporate tax rate of 34%, from previously low levels. Presumably, as prior-year tax losses are being exhausted.

I do expect CoS to rise due to higher diesel prices, labour inflation, and the additional safety personnel hired in response to recent tragic events. However, on a per-ounce basis, I expect these costs to be static or decline due to increased production and economies of scale, particularly when higher production comes from grade improvements rather than just higher ore throughput.

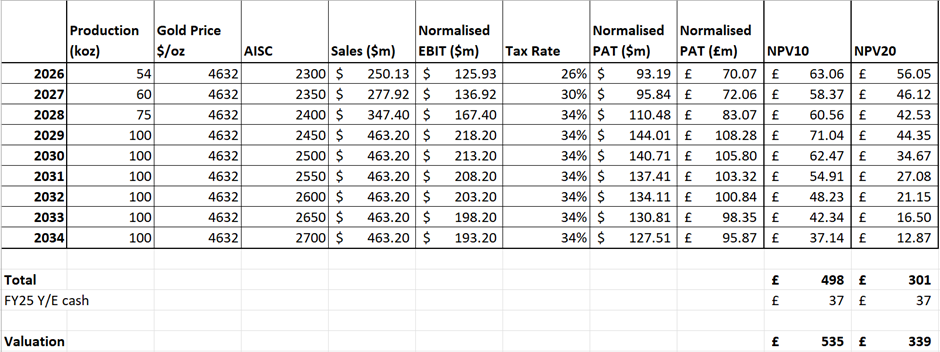

Valuation:

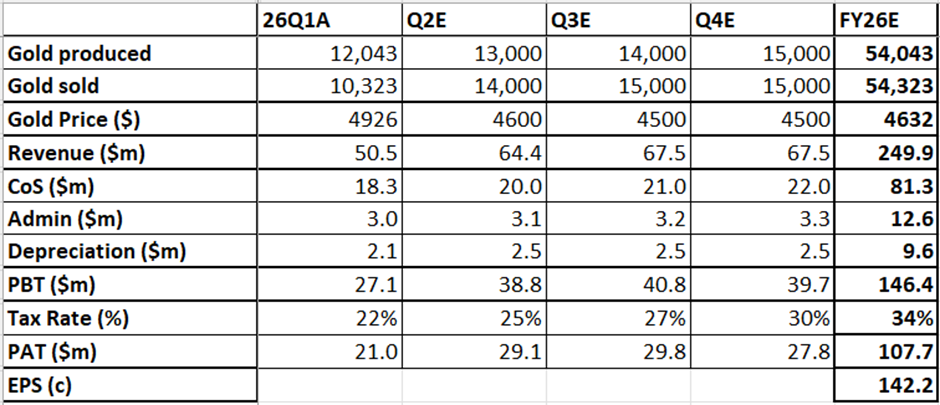

This is probably a good point to update my financial model for the company.

Q1 looked a little light on the production front, given the full-year target, though the company says it expects this to ramp incrementally throughout the year. I would typically assume they will come in towards the bottom of the guidance range at the moment.

One thing you can guarantee about modelling the future is that you will be wrong. However, here is my current best-guess for how things will pan out:

This is pretty much in line with the current broker consensus of 143c EPS, which is comforting given recent weakness in the gold price.

Looking to future years, and updating that AISC, takes the edge off my previous valuation:

However, there is still some significant margin of safety. The market is either valuing the company as if the gold price will fall significantly, the planned production ramp-up won’t occur, or it's using a very high discount rate to reflect the risks.

Mark’s view

Looking into the details of this update has assuaged some of my concerns. The flat quarter-on-quarter performance was due to the timing of gold sales rather than anything else. The rise in AISC costs is largely due to accounting changes rather than any significant cost inflation. Indeed, CoS and Admin costs per ounce are largely flat over time.

Taking the higher AISC does take the edge off my valuation model. However, FY26 looks set to be a great year, despite recent weakness in the gold price. There appears to be enough upside left at the current price in all but the most extreme downside scenarios. As such, I am happy to maintain our previously mostly positive view (and my shareholding). As usual, only the inherent risks associated with mining stop this from being a fully positive view. AMBER/GREEN

Churchill China (LON:CHH)

Down 1% at 336p (£37m) - AGM Statement - Mark - BLACK/AMBER/GREEN =

It's a rather short update, as is often the case, for AGM Statements.

The Company is pleased to note that hospitality sales remain broadly in line with expectations.

Broadly in line, is of course code for slightly below. Which raises the question why the Company is pleased to be telling us this. Are we to ascertain they are behind market expectations, but the board were expecting it to be much worse, but hadn’t yet told us, so this exceeds their expectations? Either way, the inclusion of the word “pleased” raises more questions than answers!

In the recent results they said:

The Group has continued to maintain a good level of sales in the UK given our strong market position in the pub chain sector, which tends to be less impacted by economic sentiment compared with independents… The hospitality trade continues to be relatively buoyant, however profitability remains under pressure. This has lead to good levels of replacement business but new installations in the rest of the world have been delayed and this has caused a reduction in turnover in this area of the business.

Yet sales fell. If this happened in a “relatively buoyant” hospitality market, what will be the impact of a weaker one?

The reality is that the end markets are incredibly tough for Churchill right now and they are doing what they can to mitigate this:

Although mindful of geopolitical uncertainties, including the conflict in the Middle East, we are proactively managing the factors within our control and remain confident in our long-term outlook.

The focus on the long-term is admirable, but also suggest that the short and medium term are going to be weak and there is not much they can do apart from control costs.

They also mention the as yet undetailed announcement of £120 million of government support for the UK ceramics industry. However, I can’t help feeling that Churchill’s prudence means that they are the least likely to benefit from it. The shares reacted positively to recent results, largely because they had fixed their energy cost:

In 2026 the Group has open exposure to circa 16% of its gas costs and has forward purchased 64% of its gas requirements for 2027.

Government support in the form of energy price caps won’t have a big impact until 2028. The support may also be financial. Something like export guarantee financing would have a material impact on the financial health of someone like Portmeirion (where I have a starter holding). However, with material net cash this wouldn’t do much for Churchill.

We have no view of broker coverage to inform how this has landed with them.

Mark’s view

Roland upgraded this to AMBER/GREEN following recent final results, citing the valuation disconnect. I’m minded to agree with him, particularly given the discount here:

However, there is no doubt that market conditions are tough, and that any return to top line growth appears to have been kicked into the long grass by today’s update. I’m going to adopt a wait-and-see approach today and keep our view the same.

Clean Power Hydrogen (LON:CPH2)

Suspended - 1MW MFE220 Factory Acceptance Test update - Mark - BLACK/RED

This rather blandly titled RNS is a bit of a shocker:

In the final stages of testing at the Company's dedicated and secure test site facility in Rossington, near Doncaster, the unit experienced an unexpected error, causing it to commence a standard shutdown procedure. During that shutdown procedure, the unit experienced an incident which has caused significant damage to the equipment. In line with the Company's health, safety and environmental protection processes, all operations have been suspended and a thorough investigation is underway into the causes of the original error and the subsequent failure.

This sounds pretty catastrophic and given the use of hydrogen, one can imagine the worst case outcome would be the total destruction of the unit. It also casts into doubt the commercialisation of the technology. They say this materially delays successful completion of the FAT for the MFE220 unit which was previously expected imminently. This shows the risk that investors in unproven technology face.

They say they are reviewing their insurance coverage, but this doesn’t help them in the near term. It also highlights the risks investors face when companies are undercapitalised through to cash break even. They say they were already in discussions with investors on a capital raise, but “In light of the incident during testing, these discussions have been paused pending greater technical clarity.”

Investors had become excited about the prospects over the last few months as a series of MOU’s had been signed with some much larger companies, such as Siemens. However, in light of today’s announcement these may represent a weakness rather than a strength, as they are having to review “the potential implications for its commercial arrangements with customers.”

The result of the lack of clarity on the company’s finances has led to today’s suspension.

Mark’s view

Commiseration to any holders here. The best outcome appears to be a very discounted equity raise, the worst outcome is insolvency. I’m pleased to say Graham had already been RED on this company when he looked at it a year ago, meaning that he had called the risky nature of this venture correctly. It will be no surprise that today’s events don’t lead to an upgrade in our stance!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.