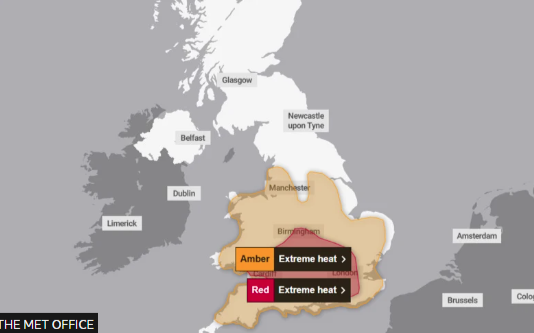

Heatwave: the Met Office says there is “a risk of serious illness or danger to life” over the next few days. There’s a Red weather warning for London and surrounding areas, including parts of Wales. A maximum temperature of 39 degrees is possible today:

I made it to a big box retailer just before it shut yesterday evening, and picked up a tall, cheap, oscillating fan that resembles a skinny Dalek. About 90% of customers in the shop were there for the same reason, and supplies were rapidly diminishing! My new friend should be a wonderful boost to my productivity (and will therefore be included on my tax return).

Alan Greenspan passed away on Monday, aged 100. One of the first times I came across Mr. Greenspan was when I read the book Capitalism: The Unknown Ideal as a teenager. First published in 1966, it included several chapters written by Greenspan. I thought he was a genius! For example, he wrote this in a chapter called Gold and Economic Freedom:

"...prior to World War I, the banking system in the United States (and in most of the world) was based on gold and even though governments intervened occasionally, banking was more free than controlled. Periodically, as a result of overly rapid credit expansion, banks became loaned up to the limit of their gold reserves, interest rates rose sharply, new credit was cut off, and the economy went into a sharp, but short-lived recession. (Compared with the depressions of 1920 and 1932, the pre-World War I business declines were mild indeed.)...

When business in the United States underwent a mild contraction in 1927, the Federal Reserve created more paper reserves in the hope of forestalling any possible bank reserve shortage. More disastrous, however, was the Federal Reserve’s attempt to assist Great Britain who had been losing gold to us because the Bank of England refused to allow interest rates to rise when market forces dictated (it was politically unpalatable)...

The “Fed” succeeded; it stopped the gold loss, but it nearly destroyed the economies of the world, in the process. The excess credit which the Fed pumped into the economy spilled over into the stock market-triggering a fantastic speculative boom. Belatedly, Federal Reserve officials attempted to sop up the excess reserves and finally succeeded in braking the boom. But it was too late: by 1929 the speculative imbalances had become so overwhelming that the attempt precipitated a sharp retrenching and a consequent demoralizing of business confidence. As a result, the American economy collapsed.

Unfortunately, by the time I read this book in the early 2000s, there was nobody at the Federal Reserve who seemed to understand the Fed's role in creating booms and busts.

Overnight market movements:

The FTSE is set to open down 0.4% at 10,415

S&P 500 is up 0.25% at 7,380

Brent crude (August) is down 1.1% at $76.30/bbl

Gold is down 0.9% at $4,075/oz

Bitcoin is up 0.7% at $62,850

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Anglo American (LON:AAL) (£43.7bn | SR61) | Definitive agreement to implement a joint mine plan for the Los Bronces and Andina copper mines in Chile, following receipt of the required competition and regulatory approvals. | ||

SEGRO (LON:SGRO) (£10.0bn | SR73) | Prologis sent a letter to the SEGRO board. The proposal was unequivocally rejected. SEGRO shareholders would receive 0.084 new Prologis shares for each SEGRO share. Based on the Prologis share price of $145.3, this would represent a 24.6% premium to the most recent SEGRO share price. | TAKEOVER (AMBER) (Roland) Prologis shares trade on 2.5x book value, so it would obviously be a good trade for the US firm to use its stock to buy SEGRO at 1x book value. I think SEGRO’s board is right to reject this proposal, though. If Prologis won’t offer a premium, then I don’t see much reason why SEGRO shareholders would want to sell out. While market conditions in the UK and Europe may have been more difficult than in the US, I don’t see any reason why SEGRO can’t continue to generate value for shareholders on a medium-term view. | |

Berkeley group (LON:BKG) (£3.2bn | SR47) | £451m pre-tax profit. NAV per share up 9% to £39.17. Outlook: While short-term buyer caution has been driven by uncertainty over the timing of interest rate reductions, underlying demand indicators remain positive, and transactions will recover as conditions and confidence improve. | AMBER = (Roland) [no section below] I covered this respected housebuilder in more depth in April and concluded that the valuation was almost certainly cheap, but the catalysts for and timing of any recovery were uncertain. I don’t have much to add to this today except to note that as far as I can see from my research, until this year, Berkeley shares had not traded below book value since 2008. I’m going to stay neutral today as the group’s subdued profits mean the current valuation is probably fair, in my view. Consensus shows earnings falling again in both FY27 and FY28. But for a patient buyer or an investor with a more bullish view on prospects for London housing (perhaps under the next PM), I think Berkeley could be worth a closer look. | |

Primary Health Properties (LON:PHP) (£2.4bn | SR56) | PHP confirms that it is in advanced discussions with an investor regarding the potential contribution of the private hospital portfolio to seed a new joint venture. | AMBER/GREEN (Roland) [no section below] An updated note from broker Shore Capital this morning suggests the unnamed JV partner might be GIC – the Singapore sovereign wealth fund. A private hospital JV to help deleverage following the Assura merger has been in the pipeline for some time, so it’s good to see signs of progress. While PHP’s loan-to-value ratio of 57% is higher than I’d normally want to see, the high occupancy and long lease terms of the REIT’s healthcare estate mean I’m willing to be relatively relaxed about this in the short term. With the stock trading slightly below book value and offering an 8% dividend yield, I’m inclined to be moderately positive ahead of PHP’s interim results on 30 July. | |

B&M European Value Retail (LON:BME) (£1.88bn | SR54) | New CFO with effect from February 2027. Currently VP of Commercial Finance at ASDA. | ||

ITM Power (LON:ITM) (£873m | SR23) | ITM and DB Systemtechnik have signed a Letter of Intent to forge an innovation and research partnership for the development, piloting and testing of green energy solutions for the transport and critical infrastructure sectors. | ||

Trainline (LON:TRN) (£766m | SR86) | New CEO from September 2026. Most recently he was CEO of the UK & Ireland division of Flutter Entertainment. | ||

GlobalData (LON:DATA) (£586m | SR36) | The new CFO will join from September 2026. Was CFO at Keywords Studios. | ||

THG (LON:THG) (£524m | SR27) | Full year guidance reiterated. H1 Group revenue growth of c.+6.5% (H1 2025: -2.5%) and H1 Adjusted EBITDA of at least £40m. | ||

Beximco Pharmaceuticals (LON:BXP) (£389m | SR n/a) | Q3 25 Results, Q1 26 Results, Half-Year 26 Results & Q3 26 Results | Nine months ended 31 March 2026: net sales increased 13.1% to Bangladesh Taka 41,428.0m / £256.9m. Profit after tax increased 34.0% to BDT 7,048.6m / £43.7m. | Beximco shares have been suspended since 2 Jan 26. |

Empire Metals (LON:EEE) (£303m | SR10) | Total consideration of A$750,000 cash, comprising the A$50,000 non-refundable deposit previously received and the balance of A$700,000 received by the Company on completion. | ||

Essentra (LON:ESNT) (£234m | SR39) | The transaction has been completed at an acquisition multiple of 6.5x FY25 EBITDA and is expected to be accretive to margins and adjusted EPS in the first full year post-completion, with a return on invested capital of 15% anticipated in the third full year of ownership. | ||

Vertu Motors (LON:VTU) (£228m | SR97) | Group margins remain stable and overall trading performance remains ahead of prior year levels. The Board expects FY27 results to be ahead of current market expectations (consensus: adj pre-tax profit of £23.5m to £25.1m). Shore Capital broker estimates updated: - FY27E adj EPS: 5.9p (prev. 5.7p) - FY28E adj EPS: 6.3p (unch.) | AMBER = (Roland) Vertu appears to be taking sensible measures to improve the performance of its dealer portfolio, tilting further towards Chinese brands and combining sub-scale/underperforming franchises. Today’s c.4% upgrade to FY27 profit forecasts still leaves expectations well below the level seen before March’s downgrade. While I share the company’s view that the government regime mandating a shift to EV sales is an adjustment period, I think Vertu’s subdued profitability means the valuation is probably about right at the moment. I’m staying neutral today. | |

Avingtrans (LON:AVG) (£203m | SR65) | The Board is pleased to report that FY26 profit will be in line with market expectations. The Group has continued to secure strategically significant contract awards across its core nuclear and infrastructure markets, while also making encouraging progress in expanding its presence in adjacent growth sectors. | AMBER/GREEN = (Roland) [no section below] This seems a positive update overall, with news of new contract wins in the group’s nuclear business in both the US and South Korea. There’s also a contract win in the UK for high-spec tunnel doors for the HS2 project. Revenue in the Medical & Industrial Imaging division was “lower than had been intended” due to the timing of regulatory clearances, but progress is being made. The only dud note is that Avingtrans now expects to have to repay c.$5m of Covid-era loans to which it was not entitled as a foreign-owned business. While this is a material amount for a business that generated £8m of operating profit last year, payments are expected to be spread over 24 months. With earnings growth running at double digits and a mid-teens P/E, the outlook seems favourable to me. My only niggle – without in-depth research – is that profitability appears low, with an operating margin of c.5%. I’m going to leave Graham’s previous view unchanged today. | |

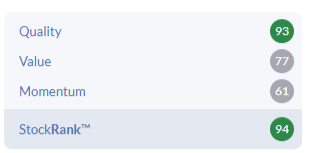

Liontrust Asset Management (LON:LIO) (£177m | SR94) | Adj pre-tax profit -36.9% to £30.5m, with adj EPS -35.4% to 36.7p. AUMA -13.4% to £19.6bn, with net outflows of £4.2bn. | GREEN ↑ (Graham)

I’m glad I resisted the temptation to take a neutral stance on this last time, as I stuck to the view that “profits are profits”. The algorithms take a similar view, calling it a Super Stock: It’s unfortunate that outflows continue, but we can look on the bright side: outflows are currently much slower than they were before, and market movements are offsetting them very well. Plus, it looks like broker forecasts might have finally stopped falling:. So as a contrarian value play, I still like this. Indeed, I’m going to trust my instincts and go GREEN now, on the back of today’s upgrades. | |

Jadestone Energy (LON:JSE) (£150m | SR35) | Based on the strong performance of the first well and data gathered while drilling the second well, the third well has now been confirmed and drilling has begun. 2026 capex guidance of $50-80m is unchanged. | ||

Pharos Energy (LON:PHAR) (£106m | SR93) | Pharos is recommending a cash offer from Ratio Petroleum Energy for up to 28p per share, including dividends. | TAKEOVER | |

Vulcan Two (LON:VUL) (£76m | SR35) | In March 2026, the Company completed a £40m fundraise and the acquisitions of CloudRx, Webmed and Hyperdrug, creating a diversified healthcare platform spanning both B2B and B2C digital pharmacy services. A new distribution facility in Leeds is also being fitted out. | ||

Cobra Resources (LON:COBR) (£47m | SR9) | Approx 80% of drilling results from Boland and Head have been received to date. Latest assays from the Head prospect point to a scalable system open to the north and south, while unique acid generation characteristics further enhance production economics. | ||

PROCOOK (LON:PROC) (£42m | SR75) | Revenue +23% with LFL +11.8%. Pre-tax profit +64.5% to £2.5m, with free cash flow of £3.5m. New customers +24.6%, active customers +24%. Outlook: confident of delivering FY27 expectations. | ||

Cavendish (LON:CAV) (£36m | SR61) | SP -5% Revenue +2.3%, pre-tax profit +114% to £1.5m. Adj EPS -15% to 0.8p. Transaction volume 96 (FY25: 100). "While market conditions remain uncertain, Cavendish is well positioned to benefit from improving sentiment over time." | GREEN = (Graham) [no section below] According to Hardman Reseach, "all main figures were in line with expectations". Checking the balance sheet, I see that net assets are £25m, after excluding intangibles, covering nearly half of the market cap. Looking ahead, Harman forecast that PBT will more than double in the current financial year (FY27) to £3.6m on the back of a modest increase in revenues from £56.9m to £60m. Cavendish themselves have offered a balanced outlook statement. I remain of the view that this continues to offer value at the current level. The unchanged 0.8p dividend provides a yield approaching 10% while investors wait for some capital appreciation. | |

Coppa Collective (LON:COPC) (£25m | SR82) | LFL sales +1.8%, with group revenue flat at £25m. Adj EBITDA +200% to £0.3m, with pre-tax loss narrowed to £1.7m (H1 25: £2.2m). Group continues to see resilient consumer demand, albeit with cost pressures. | ||

Haydale (LON:HAYD) (£25m | SR N/A) | Revenue +463% to £2.25m with gross profit +325% to £0.85m and adj operating loss of £1.16m (H1 25: £0.68m), “reflecting investment in platform execution and the enlarged Group operating structure”. Outlook: the board “remains focused” on delivering current FY26 market expectations (Revenue £8m, adj pre-tax loss of £2.5m). | ||

Light Science Technologies Holdings (LON:LST) (£18m | SR4) | The Group currently has two passive fire protection installation projects in progress with a combined contract value of c.£390k to c.£775k depending on the extent of remediation required. Additionally, total Injectaclad material supply orders secured since the acquisition of RLUK now amount to c.£885k. | ||

River Global (LON:RVRG) (£17m | SR34) | The Financial Conduct Authority has approved the change in control for River Global Holdings and the proposed acquisition of RGH by Liontrust is therefore expected to complete on 30 June 2026. AUM on Friday, 19 June 2026 was £3,442 million (31 March 2026: £3,101 million). | ||

Eco Buildings (LON:ECOB) (£16m | SR5) | Following a recent £2.35m fundraise, Eco has started construction of a second manufacturing online at its production facility in Durres, Albania. | ||

Lexington Gold (LON:LEX) (£13m | SR7) | Entered into an agreement with GoldOz Ltd to acquire 100% of the issued share capital of Global Asset Resources Ltd ("GAR") from Lexington Gold. GAR is the company through which Lexington Gold holds its 51% interests in the Company's three principal Carolina gold projects. Lexington will receive A$350k and 25.5m new GoldOz shares when GolzOz relists on the ASX. | ||

Fulcrum Metals (LON:FMET) (£13m | SR12) | FY25: no revenue and pre-tax loss of £553k. Highlights: completed acquisition of Teck-Hughes Gold Tailings Project and divestment of Tully Gold Project. Successfully raised £1.9m during the year and £1.3m subsequently to fund project developments. | ||

Thor Energy (LON:THR) (£12m | SR31) | Programme will acquire c.464 line-kilometres of 2D seismic across the HY-Range project in Q3/Q4 2026. Fully funded from existing cash. |

Graham's Section

Liontrust Asset Management (LON:LIO)

Up 14% at 336.3p (£202m) - Annual Financial Report - Graham - GREEN ↑

While the results from this fund manager are poor, they aren't too far off the existing forecasts at Panmure Liberum.

Revenue £123m vs. Panmure estimate £126m

Operating profit £29.5m vs. Panmure estimate £30m

Adj. EPS 36.7p vs. Panmure estimate 37.6p.

Net outflows during FY26 were very large at £4.2bn, but this was already known.

What’s more interesting is the outlook, and that’s where things are looking up.

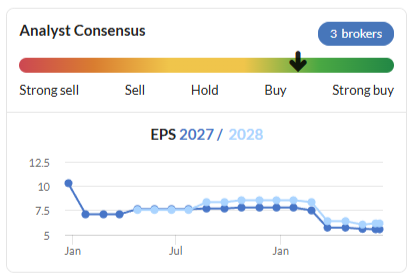

Panmure have increased their EPS forecasts for FY27 (from 35.7p to 36.7p, matching the FY26 result) and for FY28 (from 41.7p to 43.1p). They also introduce a new FY29 EPS forecast of 49.7p, which sounds a little aspirational to me while still being within the bounds of possibilities.

At the current share price, that gives a P/E multiple of 9x for the current year, falling to 8x for next year.

The acquisition of River Global is going ahead at the end of this month, slightly sooner than expected, bringing in another £3bn pounds of AUM.

Current Trading Update

AUM as of last week was £21.4bn, up strong from £19.6bn at year-end (March 2026).

In Q1 of the new financial year, so far, there have been net outflows of £276m - a much slower pace of outflows than we saw last year.

CEO comment:

"The improvement in Liontrust's flows over the past nine months is testament to the expansion of our distribution internationally and broadening of client types. This reflects the significant development at Liontrust over the past couple of years, with net outflows now at £276 million for the current quarter with one week to go, and strategies such as Cashflow Solution benefiting from both strong performance and client diversification….

We have had a very positive response from both RGH and Liontrust clients to the acquisition and are pleased with the way in which the two companies have come together to ensure completion is as smooth as possible… We will take advantage of any other such strategic deals as and when they appear.

Dividend: this has been rebased at a much lower level. The total dividend for FY26 is 19p, vs. 72p in the prior year. At ;east 19p is covered very well by EPS.

Outlook: nothing too specific here.

Liontrust is showing positive results of all the progress we have made over the past few years. We are well positioned to take advantage of the opportunities ahead for active management.

Graham’s view

I’m glad I resisted the temptation to take a neutral stance on this last time, as I stuck to the view that “profits are profits”.

The algorithms take a similar view, calling it a Super Stock:

It’s unfortunate that outflows continue, but we can look on the bright side: outflows are currently much slower than they were before, and market movements are offsetting them very well. Plus, it looks like broker forecasts might have finally stopped falling:

So as a contrarian value play, I still like this. Indeed, I’m going to trust my instincts and go GREEN now, on the back of today’s upgrades.

Roland's Section

Vertu Motors (LON:VTU)

Up 2.8% at 75p (£234m) - AGM Trading Update - Roland - AMBER =

Today’s AGM update is short but relatively positive, with a modest upgrade to full-year profit guidance for the year ending 28 February 2027.

… the Board anticipates that full year results for FY27 will be ahead of current market expectations

Trading appears to be relatively positive despite well-documented headwinds:

The Group continues to trade positively in the financial year, with like-for-like volume growth in all channels: new retail, Motability, used vehicle and fleet and commercial. Aftersales is contributing to growth in Group profits year-on-year. Group margins remain stable and overall trading performance remains ahead of prior year levels.

One factor behind the company’s success appears to be the company’s growing tilt towards Chinese car brands. These are among the fastest-growing in the UK market at the moment due to their low prices, high specs and weighting towards EV models:

The Group will launch its first Omoda and Jaecoo dealership on 1 July 2026 […] another Group outlet will be re-franchised to Omoda and Jaecoo on 1 October 2026. The Group will have 15 sales outlets representing Chinese automotive brands following these openings.

Checking the company’s website, Vertu already has a number of BYD, MG and Geely franchises.

Sales of the Chinese brands sold by Vertu have rocketed this year according to SMMT (trade body) data for the year to May:

BYD +113% to 31,553 (3.4% market share)

Geely +n/a% to 4,378 units (0.5% market share)

Jaecoo +369% to 27,996 (3.0% market share)

MG +9% to 38,346 (4.2% market share)

Omoda +169% to 15,078 (1.6% market share)

For context, popular brands such as Ford, BMW, Toyota, Peugeot and Volkswagen have all seen sales (and market share) decline this year, quite materially in some cases.

I expect Chinese car manufacturers to continue to carve out a permanent share of the UK market. This would repeat a process seen historically with Japanese brands and more recently with Korean firms Kia and Hyundai.

Cost savings are also being made by combining (presumably) underperforming sites into multi-franchise operations:

Cost benefits will arise from portfolio changes, such as the relocation in the coming months of Sheffield Mazda from a stand-alone site to a multi-franchise operation alongside the Nissan franchise in the city. Group operating costs remain tightly controlled.

Updated forecasts

Vertu doesn’t tell us what its new expectations for profit are, but fortunately we do have access to updated broker coverage today, adding some numbers to the commentary.

Here are the latest forecasts from Shore Capital, with thanks for making these available on Research Tree.

FY27E adj EPS: 5.9p (+3.5% vs 5.7p previously)

FY28E adj EPS: 6.3p (no change)

Today’s upgrade is limited to FY27 and is fairly modest. When set against the backdrop of downgrades earlier this year, we can see that expectations are still significantly lower than they were six months ago:

Roland’s view

UK car retailers (and European car manufacturers) have issues with the government’s ZEV mandate, which requires a fixed percentage of sales to be zero emission on pain of a financial penalty for each non-compliant car sold.

Manufacturers are forcing discounted EV stock on dealers, stimulating sales but putting pressure on dealers’ margins. Consumers still have mixed views on EVs and aren’t quite buying enough of them yet to meet targets, preferring hybrid models.

There’s pressure on the government to dilute its target of 80% ZEV new registrations by 2030. Perhaps the incoming Prime Minister will do this.

SMMT data and forecasts suggest EV market share will have risen from 16.4% in 2024 to 26.8% in 2026. The government targets for those years were 22% and 33% respectively, so it looks like adoption is running c.5% behind target. Even so, there’s clearly strong momentum in EV uptake.

Vertu has previously referred to this as an adjustment period and I think it’s fair to expect the situation to ease over time. But the structural challenges facing European automakers are significant, and I think it could take some time for profitability to improve.

In the meantime, forecasts suggest Vertu will continue to generate a 5% to 6% return on equity on its asset-rich balance sheet.

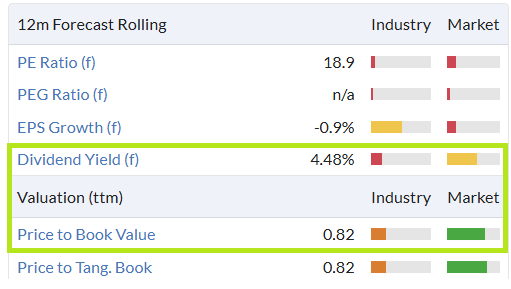

For me, this suggests the current valuation of 0.6x book value is probably about right, as it gives buyers today a c.10% expected return on cost of equity.

Looked at differently, a forward P/E of 12+ and a dividend yield of 2.8% seem high enough for a slow-growing, low-margin car dealership group.

On balance, I don’t think today’s slight upgrade is enough to justify an upgrade to our view, so I’m going to leave Mark’s previous AMBER unchanged.

SEGRO (LON:SGRO)

Up % at p (£m) - Prologis: Statement re Possible Combination and SEGRO: Statement Regarding Possible Offer - Roland - TAKEOVER (AMBER)

This FTSE 100 REIT is not a stock we’ve looked at before, but it’s the UK’s largest listed REIT, with a £19bn portfolio of logistics properties and – increasingly – data centre projects.

SEGRO’s share price spiked during the pandemic, but the valuation has since returned to more earthbound levels.

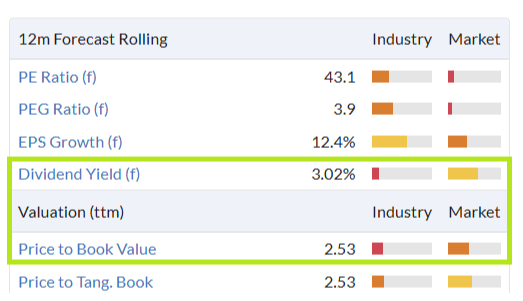

Prior to today’s bid news, SEGRO shares offered a small discount to NAV and a useful dividend yield:

That brings us up to date, so let’s take a look at today’s news.

Offer from Prologis

Prologis (NYQ:PLD) is a US REIT with a similar focus to SEGRO. Naturally, it’s a lot larger, with $235bn of assets under management. It’s also much more highly rated, with a £100bn market cap and a price/book ratio of 2.5x:

Here are the details of the Prologis offer:

0.084 new Prologis shares for each SEGRO share

Based on the Prologis share price of $145.3 and GBP:USD exchange rate of 1.32 as at market close on 23 June 2026, the Proposal represented a value of 925 pence per SEGRO share.

SEGRO’s net asset value was last-reported at 925p, on an adjusted basis. So this is an offer at book value.

SEGRO’s board has rejected the proposal:

The Board of SEGRO has unanimously and unequivocally rejected the Proposal, which falls a long way short of SEGRO's own views on value.

The Board of SEGRO considered the Proposal together with its advisers and believed that the Proposal was opportunistically timed and sought to take advantage of the clear dislocation between SEGRO's current share price and its highly attractive underlying business and strong prospects. This has been accentuated by major geopolitical issues which have adversely impacted trading valuations across the UK and European real estate sectors relative to the US REIT sector.

This situation reminds me a little of the bid for Ramsdens yesterday.

It makes perfect sense for Prologis to use its shares to attempt to buy SEGRO at book value when Prologis shares are valued by the market at 2.5x book value.

Making an acquisition on this basis will theoretically lift the share price of the acquiring company, as it benefits from a re-rating of the acquired earnings. We can see above that the Prologis P/E is double SEGRO’s P/E rating.

Prologis comments on acquisition

Unsurprisingly, the US firm is quick to highlight the potential for share price gains:

SEGRO shareholders would receive shares in the world's largest logistics REIT with a $140.9 billion market capitalisation, unlocking, on closing, significant upside to the current share price.

Prologis also believes it is able to provide “accelerated growth” compared to what might be achievable by SEGRO as an independent business.

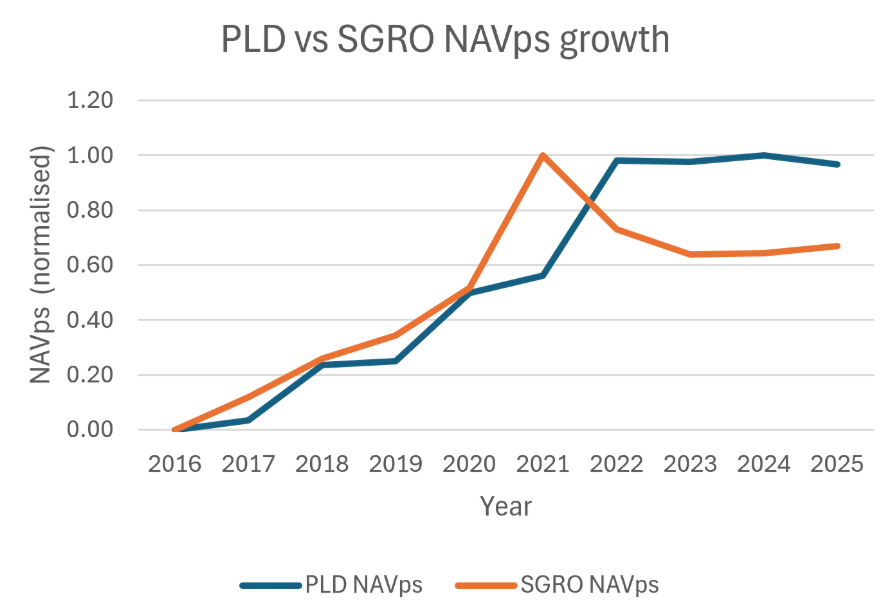

Using net asset value per share as a guide, performance over the last five years appears to support this claim, but a 10-year view shows the companies to be more evenly matched:

Prologis 5y NAVps CAGR: 5.8% / 10yr CAGR 8.1%

SEGRO 5y NAVps CAGR: 2.3% / 10yr CAGR 7.3%

Zooming out to take a 10-year view suggests that SEGRO’s claim of more difficult geopolitical conditions in the UK and Europe may have some merit. Until 2022, both companies were level-pegging on NAV growth:

Roland’s view

Whether either of these companies is really worth a significant premium to book value is a more nuanced question.

I would personally be very reluctant to buy shares in a REIT at more than 2x book value, especially as Prologis has a five-year average return on equity of just c.7%. If market conditions change there could be little to prevent the stock de-rating to trade closer to underlying asset value.

However, there’s no denying the scale and momentum of the US market and investors’ apparent willingness to support much higher ratings for US stocks. Prologis has also turbocharged its growth in recent years with a number of large acquisitions – I guess this could continue for a little while yet.

SEGRO shareholders can choose to sell into today’s spike or wait to see if Prologis comes back with a more convincing bid by the Takeover Panel deadline date of 22 July.

Personally, I would be inclined to continue holding SEGRO shares if I owned them and liked the sector. I think the valuation remains fair and don’t see any reason why the business can’t deliver further growth over the medium term.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.