Oil price: I said last week, rather optimistically, that the US-Iran conflict might be over. Since then, strikes have been exchanged in the Strait of Hormuz and both countries have accused the other of breaking the ceasefire.

However, the latest reporting (as of an hour ago, from the BBC) says that both sides have agreed to stand down from these latest attacks. Talks are set to resume tomorrow, and the Brent oil price has fallen further to $72, which is a pre-war price last seen in February this year. And so it seems that a peaceful resolution remains very likely.

Overnight market movements:

The FTSE is unchanged at 10,525

S&P 500 is up 1.1% at 7,390

Brent crude (August) is unchanged at $72.00/bbl

Gold is down 0.7% at $4,060/oz

Bitcoin is up 0.75% at $60,100

Wrapping it up there for now as I have a dental appointment! See you tomorrow.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£222bn | SR81) | Recommendation based on TROPION-Breast02 Phase III trial where AstraZeneca and Daiichi Sankyo's Datroway showed a statistically significant and clinically meaningful improvement for the dual primary endpoints of overall survival and progression-free survival. | ||

BT (LON:BT.A).A (£19bn | SR84) | BT and Verizon to form international JV & Updated Guidance for International JV Formation | BT and Verizon to combine their international operations in a new 50:50 JV, serving >3,000 customers in 180 countries, with c.$4bn in annual revenue. Transaction expected to close in 2027, no material change to FY27 profit or cash flow forecasts. | |

Plus500 (LON:PLUS) (£3.3bn | SR85) | Has launched CFTC-regulated Kalshi sports event-based contracts in the US, “bringing the highest-engagement product category in prediction markets directly to its customers.” | ||

Bridgepoint (LON:BPT) (£2.0bn | SR34) | Kayne is a private market real estate platform with c.$117bn of AUM. Upfront enterprise value of c.$1,393m, comprising $759m in cash and c.$189m of newly-issued BPT shares. Represents “a high single-digit multiple of expected 2027 EBITDA”. | ||

Georgia Capital (LON:CGEO) (£1.32bn | SR81) | Board has approved early redemption of US$50m of local bonds. Settlement expected in August 2026, following which GCAP will have fully repaid its holding company debt. Company also announced a further $10m buyback in addition to its current $50m buyback. These steps complete GCAP’s GEL 700m capital return programme. | ||

Foresight group (LON:FSG) (£458m | SR85) | AUM +8% to £13,024m. Revenue +11%, adj EBITDA +10% to £68.6m. Adj EPS +13% to 46.4p, with dividend +12% to 27.1p. Current trading: post-period end AUM c.£13.1bn and FUM c.£9.2bn, following incremental fundraising. | GREEN ↑ (Graham) | |

Porvair (LON:PRV) (£395m | SR77) | Revenue +9% (2% OCC), adj pre-tax profit +10% to £13.2m. Adj EPS +11% to 22.1p. Outlook: “Before taking account of the part-year contributions from GV and Carekem, the Board's expectations for the full year remain unchanged.” | ||

AdvancedAdvT (LON:ADVT) (£205m | SR28) | Revenue +23%, adj pre-tax profit +21% to £13.4m, adj EPS +23.5% to 10.5p. Net cash of £96m. Outlook: “the group is trading in line with the management’s expectations”. | ||

Ferrexpo (LON:FXPO) (£171m | SR) | The Group continues to operate under highly constrained conditions as a result of the war in Ukraine and related operational and financial challenges. Expects to have sufficient cash to continue operating beyond August 2026. Continues to pursue $100m equity fundraise. | (Shares suspended since May.) | |

Smiths News (LON:SNWS) (£167m | SR98) | Secured a new long-term contract with Associated Newspapers, publisher of the Daily Mail and The i Paper. Effectively secures national distribution of ANL’s leading titles from January 2028 through 2037. Represents an incremental uplift in revenue of c.£105m from Jan 2028. | GREEN = (Graham) I think the profit numbers in 2027 will be under some pressure, as one-off costs are incurred. Then the two expanded contracts should start to run profitably the following year. The big news today is that 2028 is now shaping up to be even better than we might have automatically assumed after the last contract announcement. So there’s no reason to change my positive stance here. This is a Super Stock (StockRank 98) on a P/E multiple of about 7x after today’s gains. | |

EcoSynthetix (TSE:ECO) (£166m | SR29) | Ministerial Approval Received for Namibia PEL 98 Farm-Out. PEL97,99 & 100, and South Africa Block 1 Section 11 Processes Underway. | ||

Focusrite (LON:TUNE) (£115m | SR78) | Revenue +1.3%, adj EBITDA +5.7% to £24.7m, adj EPS -7.7% to 15.6p. Launched 38 new products and 66 updates to existing product lines, net debt halved to £8.6m. Outlook: Q1 trading ahead of prior year, expectations for FY27 are unchanged. Broker Cavendish notes that Focusrite’s adjusted EPS for the 12 months to 28 Feb 26 of 15.6p was below their March forecasts of 17.3p Cavendish “to review [FY27] forecasts following this morning’s result." | AMBER ↑ (Roland) [no section below] Today’s results claim to be in line with expectations, but earnings have missed broker estimates (see left), so it looks like Graham was correct to be cautious in March. Another blot on these numbers is the £9.8m impairment for the Sequential business, “reflecting the difficult market for premium synthesizers”. This follows a £5.4m impairment to Sequential assets in FY24. I believe Focusrite paid c.£18m for Sequential in 2021, so the company has now written off nearly 85% of the value of this deal. While I recognise that market conditions have been tough at times, this doesn’t seem like a very good capital allocation decision by management. The current year is said to have started well and Focusrite says its FY27 expectations are unchanged. This suggests earnings could rise to c.19.5p and places the business on a P/E of 10. That could be a decent entry point if the group can deliver a return to sales growth, which should benefit margins. On balance I am going to revert to neutral today, although I would have liked to see updated broker numbers too. | |

Solid State (LON:SOLI) (£109m | SR76) | Revenue +23%, adj pre-tax profit +72% to £8.6m. Adj EPS +77.4% to 11.0p. Strong demand from defence and security sector, accounting for c.47% of group revenue. Outlook: open order book of £102.4m, expects to exceed current market expectations for FY27. | AMBER/GREEN = (Roland) These results are ahead of revised FY26 consensus forecasts and also include an upgrade to FY27 guidance. Solid State’s strength in defence appears to be driving good levels of growth despite some more challenging conditions elsewhere. Positive operating leverage delivered an improvement in margins last year, but profitability still remains somewhat average and the shares aren’t obviously cheap. Despite this, I don’t see any reason to change my previous view today given the strong momentum in the business. | |

Roadside Real Estate (LON:ROAD) (£106m | SR16) | Acquisition of DA Roberts Fuels Ltd is further delayed due to HMRC process timelines following a family bereavement associated with the vendor. Now expect completion in Q3 2026. | ||

Somero Enterprises (LON:SOM) (£103m | SR81) | Following investigation, Computershare has confirmed that “certain shareholder votes were not submitted to Computershare and as a result were never included in the final vote count”. The Board recognises “the significant proportion of votes cast against AGM resolutions” and is reviewing the situation. A further update will be provided in mid-July 2026. | ||

Andrada Mining (LON:ATM) (£82m | SR19) | “... strong start to the new financial year”. Q1 contained tin production +20% to 286 tonnes, with tin concentrate production +16% to 473 tonnes. Elevated tin prices expected to support strong cash generation. Funding secured for Uis ore sorting expansion. | ||

Wynnstay (LON:WYN) (£81m | SR94) | Gross profit +0.7%, adj pre-tax profit +11.7% to £6.0m. Adj EPS +15.5% to 20.9p, with net cash +5.8% to £10.9m. Reports challenging agricultural market conditions, but says restructuring benefits are evident through improved performance. Confident in delivering FY26 results in line with expectations. | AMBER/GREEN = (Roland - I hold) These results show improved profitability in mixed trading conditions. It seems that the five-year Project Genesis plan is starting to deliver results. The risk is that it’s too soon to know if this will lead to a sufficient improvement in future free cash flow to offset the multi-year increase in spending required. At this stage I remain broadly positive. I think the valuation is reasonable and see no reason to change my view given the in line nature of today’s guidance. | |

Creo Medical (LON:CREO) (£61m | SR17) | “As previously reported, the FY25 growth momentum has continued into FY26 with strong trading performance in the first three months of the current financial year…. FY26 revenue growth will be between 50% and 60% compared to FY25 (previous guidance was between 40% and 60% growth).” | ||

Blencowe Resources (LON:BRES) (£37m | SR9) | BRES has selected the preferred site for the future downstream operations associated with its Orom-Cross Graphite Project in Uganda. Has secured an option to purchase a site of 100 acres located approximately 35km north of Gulu in Northern Uganda. | ||

Tortilla Mexican Grill (LON:MEX) (£29m | SR79) | SP -3% Final results to be “broadly in line” with May guidance. Additional time needed to review French operations to ensure matters are fully understood. Shares to be suspended on 1st July. | AMBER/RED = (Graham) [no section below] | |

Atome (LON:ATOM) (£28m | SR1) | ATOME continues its engagement with the relevant authorities in Paraguay and ANDE, the state-owned electrical distribution entity, with regards to the Power Purchase Agreement necessary for the Villeta Project. | ||

Portmeirion (LON:PMP) (£26m | SR50) | The agreement for a new 5-year £36 million asset-based lending facility has now completed and is at a lower blended coupon than the prior facility. | ||

Fiinu (LON:BANK) (£24m | SR2) | Revenue £663k. Operating loss £10.3m. Cash £3.94m. Chief Strategy Officer resigns. | Publishing results just before the six-month deadline. | |

Genedrive (LON:GDR) (£21m | SR18) | Collaboration agreement with Thermo Fisher Scientific Inc. enabling genedrive to develop a CYP2C19 pharmacogenetic in vitro diagnostic test for deployment on Thermo Fisher Scientific's QuantStudio™ 5 Dx real-time PCR laboratory platform. | ||

Xtract Resources (LON:XTR) (£15m | SR41) | Pre-revenues. Operating loss £2.2m. “The year under review has been very active and to a certain degree transformational. The transformation being conversion from greenfield and brownfield project into development and production.” | ||

Fulcrum Metals (LON:FMET) (£12m | SR15) | Signs a non-binding US$20 million royalty financing term sheet and a £200,000 equity subscription with Chancery Royalty in relation to the Teck-Hughes tailings project in Kirkland Lake, Ontario. | ||

Powerhouse Energy (LON:PHE) (£11m | SR2) | Revenue for 2025 was £1.23 million (2024: £499k), all derived from Engsolve activities. Operating loss £2.9m. “Powerhouse currently has approximately several live enquiries, defined as opportunities the Company believes have potential to become revenue-generating projects.” | Publishing results just before the six-month deadline. | |

Arcontech (LON:ARC) (£10m | SR63) | New contract for its CityVision real-time market data platform to enable multiple data sources to be consumed by various applications written in different programming languages. Value c. £800k. Current performance for FY26 is in line. | ||

Tap Global (LON:TAP) (£10m | SR5) | Launches Stabld, the Group's own stablecoin, live within the Tap app's Earn product from today. Stabld is the brand for the Group's planned family of fully-reserved, fiat-backed stablecoins. | ||

Safestay (LON:SSTY) (£9m | SR51) | Revenue £20.6m (2024: £23m including discontinued operations). Loss £10.1m. NAV per share 22.21p. Current trading: average bed rate is marginally ahead of the prior year. Occupancy levels impacted by consumer behaviour changes. | Publishing results just before the six-month deadline. | |

Autins (LON:AUTG) (£8m | SR87) | FY26 revenue £17.6m (FY25 equivalent: £19.3m). Adjusted operating profit £0.4m. Outlook: in line. FY27 revenues £22m and profit after tax £0.8m, weighted to H2. FY28 revenues £26m, profit £1.4m. The Board is now guiding FY29 revenues of £27m and PAT of £1.9m. |

Graham's Section

Foresight group (LON:FSG)

Up 7% at 438.5p (£490m) - FY March 2026 results - Graham - GREEN ↑

We already had a full-year update from Foresight in April, covered by Mark.

Since then, the company has announced the sale of £1 billion of its AUM - it wants to focus on Real Assets and Private Equity, and so it sold its public markets division (“Foresight Capital Management”).

Today’s full year results therefore exclude FCM:

AUM £13 bn (+8% year-on-year, or +5% at constant currencies)

FUM £9bn (+7%, also +5% at constant currencies)

Revenue £165m (+11%), of which recurring revenue is £135m.

This good underlying growth converts into a 10% increase in “Core EBITDA pre-SBP” which rises to £68.6m (SBP means share-based payments).

Let’s sense-check this against the actual profit figures. From the annual report itself:

Operating profit £54m (prior year £41.4m)

PBT effectively the same figure, £54m.

So while the company focuses on “Core EBITDA pre-SBP” (what a mouthful), the actual profit figures themselves are clean and not so far off the adjusted ones.

Current trading: AUM has ticked up to £13.1bn and FUM to £9.1bn, marginally higher than the year-end numbers.

Executive Chairman comment:

We enter the new financial year wholly focused on our core Real Assets and Private Equity divisions with a diversified fundraising pipeline across institutional and retail investment vehicles managing long duration capital, and remain committed to our medium-term growth guidance."

Worth noting that Mr. Fairman owns nearly 30% of the business, so he is highly aligned with other shareholders.

Estimates: Cavendish say that today’s core EBITDA number is in line with consensus: revenues missed expectations, but expenses were also lower than forecast.

The 12% increase in the dividend announced today (to 27.1p) was slightly higher than expected.

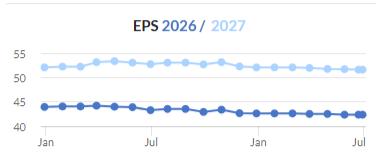

Cavendish have not yet reviewed their forecasts but they do maintain a “BUY” rating. They forecast adjusted EPS of 51.9p in the current year (FY March 2027), and then 68.1p the following year.

Graham’s view

I must confess that I don’t know Foresight’s funds very well.

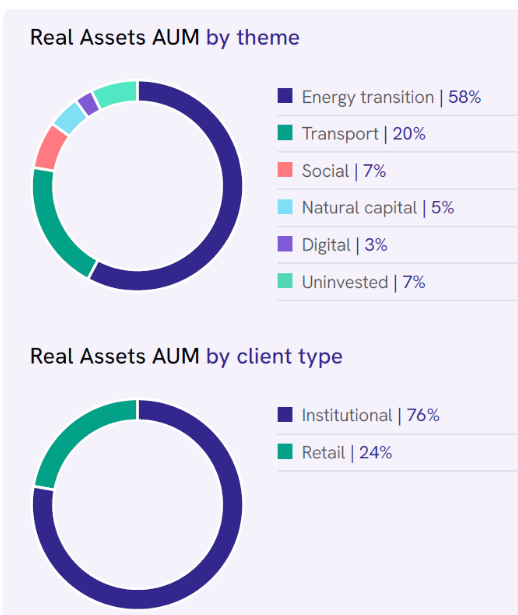

The breakdown is that they are mostly (£11.1bn) invested in Real Assets in Europe and Australia. This is further broken down as follows:

As you can see, the majority is invested in the “Energy Transition” - wind farms and woodland, for example.

Fundraising continues for their new FEIP II fund, about halfway towards their €1.25bn target.

The rest of AUM (£1.9bn) is Private Equity; they are “one of the most active UK regional SME investors”.

As far as our stance on this goes, I don’t see why not to be fully GREEN on it.

EPS forecasts have been stable:

Mark pointed out in our previous coverage that FUM forecasts would be missed, but this hasn’t had much of an impact on profits. And when businesses are trading at c. 8x earnings, I don’t think we need to expect everything to go perfectly as planned: if the general growth trajectory continues for a few years, and economic returns remain strong, then the current valuation will be too cheap either way.

This has a QualityRank of 99: successful fund managers often generate very strong margins and returns, as this one does.

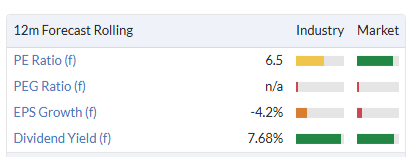

I’m therefore taking us back to fully GREEN, as I don’t see what there is to dislike. The P/E is still below 10x after today's rise and is even 6.4x based on FY March 2028 forecasts.

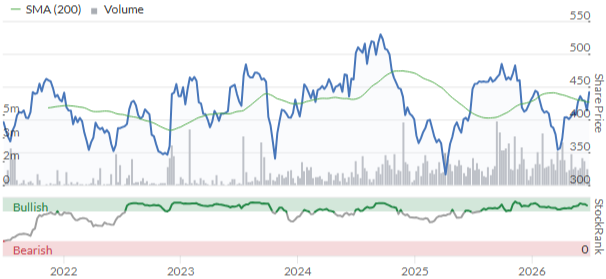

Looking at the chart for the past few years, I see that the share price has been pretty stable, all things considered. The market wasn’t expecting much:

But recent performance shows that fund managers can still do very well out of the “energy transition”. Maybe the structure is key here: investing mostly in private, real assets and gaining long-term commitments from their customers?

Smiths News (LON:SNWS)

Up 3.6% at 70p (£173m) - Associated Newspapers Limited - National Contract Win - Graham - GREEN =

More great news from Smiths News, this cigar butt stock that refuses to die: it has “a new long-term contract with Associated Newspapers Limited… publisher of 'Daily Mail', 'The Mail on Sunday' and 'The i Paper'.”

The transformational agreement with ANL…is on enhanced commercial terms for Smiths News and includes (i) an expansion of the distribution territories in which the Company is appointed as ANL's exclusive wholesale distributor, thereby effectively securing national distribution of ANL's leading titles across all of Great Britain, to take effect from January 2028 and (ii) an extension in the contract term of our appointment through to July 2037.

This sounds very similar to the other contract we reported on recently, where News UK & Ireland (publisher of the Sun) upgraded to national distribution at Smiths News, with a £125m uplift in annual revenue for Smiths. The News UK contract also runs until 2037.

The ANL contract is expected to lift revenues by c. £105m p.a. from January 2028.

The two contracts announced recently therefore “represent c.36% of the national newspapers and magazines market having been secured from January 2028 for Smiths News”.

CEO comment:

Today's announcement continues to reinforce our position as a trusted partner for our industry and further secures a sustainable future for print news distribution, reflecting our shared commitment to supporting the industry over the long term."

Estimates: the previous contract announcement warned us that there would be costs associated with expanding their geographical capabilities. Today’s announcement reaffirms this but doesn’t yet give any details. But it’s very reassuring that the increased capacity will now be used by at least two of the company’s major customers!

In the absence of more detailed guidance, Canaccord Genuity have left their forecasts unchanged today, expecting 10.4p of EPS this year (FY August 2026) and 10.3p of EPS next year.

Graham’s view

I think the profit numbers in 2027 will be under some pressure, as one-off costs are incurred. Then the two expanded contracts should start to run profitably the following year.

The big news today is that 2028 is now shaping up to be even better than we might have automatically assumed after the last contract announcement.

So there’s no reason to change my positive stance here. This is a Super Stock (StockRank 98) on a P/E multiple of about 7x after today’s gains.

It has announced a combined £230m of incremental revenues from two major customers, starting in 2028. For context, annual revenues have been running at about £1 billion.

Checking the share price, I see that it has been range-bound year-to-date. I can’t predict the future but based on the fundamentals, it would make sense to me if this broke out of the range to the upside before too long.

Roland's Section

Solid State (LON:SOLI)

Up 5% at 202p (£115m) - Final Results - Roland - AMBER/GREEN =

Electronics group Solid State upgraded its FY26 guidance in April. The company has followed suit today by beating revised consensus forecasts and upgrading its guidance for FY27.

The resulting upgrade should give our broker consensus trend chart a pleasing uphill slope:

I’ll return to today’s upgraded forecasts shortly, but let’s take a look at the main points from today’s results.

FY26 results summary (y/e 31 March)

Revenue up 23.2% to £154.1m (+1.4% vs consensus £152m)

Adjusted pre-tax profit up 72% to £8.6m

Adjusted EPS up 77.4% to 11.0p (+6.8% vs consensus 10.3p)

Dividend up 10% to 2.75p per share

Net debt down 43% to £4.2m

Orderbook -1% to £102.4m

Trading commentary

All three divisions delivered improved year-on-year performance, supported by strong demand for AI data centre infrastructure and defence and security applications.

Solid State’s reporting structure was tweaked last year to separate the Power segment from Systems and Components. The group now has three reporting segments:

Power (revenue +15.6% to £31.8m, op profit +500% to £1,677m): demand for battery technologies and systems “has grown across a range of un-crewed applications”, including drones, autonomous underwater vehicles, robotics and unmanned ground vehicles. The division signed c.$20m of new defence orders in the final four months of the financial year.

Systems (revenue +48% to £62.5m, op profit +71.6% to £8.9m): “Adoption of the Persistent Systems communications ecosystem and our associated technology solutions continued to build, supporting strong equipment sales under the NSPA framework programme.”. Delivered a $10.8m order to the British Army in Q1 under Project CAIN, a multi-year programme.

Components (revenue +8.2% to £59.8, op profit +2.3% to £2.2m): market conditions were challenging. However, demand in the medical and defence sectors was strong, “particularly for certain power-related products driven by AI-associated data centre investment”. A number of new design wins have been secured in the UK and US, but the company warns of the growing impact of longer lead times and rising prices for certain components, especially memory products.

Looking across the business, the US accounts for around 23% of revenue, while the UK is the largest single market at c.45%. Europe makes up the majority of the remainder.

Solid State’s CEO Jon Macmichael notes that the group’s UK and US production footprint remains one of its “most important strategic assets”; governments in both countries are keen to secure domestic supply chains for defence equipment.

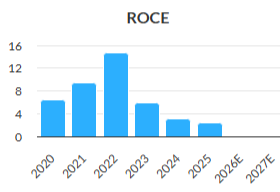

Profitability: last year’s strong revenue growth delivered welcome operating leverage, with sales rising more quickly than operating costs. The result is a significant improvement in profitability (using reported profits):

Operating margin: 4.5% (FY25: 1.1%)

Return on Capital Employed (ROCE): 8.6% (FY25: 1.9%)

Return on Equity (ROE): 6.5% (FY25: 0.8%)

To its credit, Solid State also reports both ROE and ROCE in today’s results. These are adjusted figures, though, and result in somewhat higher numbers than my standard calculations (which mirror those in the StockReport):

Should I allow Solid State’s profit adjustments? Checking the details in the footnotes shows these are all fairly standard:

Personally, I find it easier to use the statutory figures. I see share-based payments as remuneration and I think that deducting amortisation from the balance sheet while leaving it in the profit calculation is likely to flatter the returns on capital being generated by past acquisitions.

My litmus test is usually to consider whether free cash flow is closer to reported net profit or adjusted net profit. In this case, free cash flow of £5.3m lies midway between the relevant figures of £4.1m and £6.3m.

This gives the stock a free cash flow margin (vs revenue) of 3.4%, supporting my view that while profitability is improving, it would be nice to see a further improvement in margins.

Valuation: today’s results and share price rise give Solid State a trailing P/E ratio of 19. Using free cash flow instead gives a multiple of 22.5, again supporting my preference for non-adjusted figures.

Outlook & Broker Estimates

The Group has had a good start to the new financial year with current trading in line with the Board's expectations, and we expect to exceed current market expectations for FY26/27.

Solid State ended the year with a flat orderbook of £102.4m, but Mr Macmichael is evidently confident this provides sufficient visibility to upgrade guidance for FY27.

House broker Cavendish has upgraded FY27 forecasts today and introduced FY28 estimates:

FY27E adj EPS: 11.5p (+9% vs 10.5p previously)

FY28E adj EPS: 12.7p (+10% vs FY27E)

These upgraded estimates leave Solid State’s forward valuation largely unchanged, albeit with an improved rate of EPS growth:

Roland’s view

I upgraded Solid State to AMBER/GREEN in December, suggesting that the business had “the potential to deliver medium-term growth in defence as well as an eventual recovery in industrial demand”.

This optimistic view was followed by a sharp StockRank Jump in April (a signal covered in Ed’s latest article), since when the share price has risen by around a third:

Strong Quality and Momentums scores should be enhanced by today’s results and support a High Flyer styling at the time of writing:

While the valuation remains relatively full and profitability is still below the level I’d like to see, the direction of travel is clearly positive. I don’t see any reason to change my previous view today. AMBER/GREEN =

Wynnstay (LON:WYN)

Up 2% at 358p (£83m) - Interim Results - Roland - AMBER/GREEN =

(At the time of writing, Roland has a long position in WYN.)

This agricultural group is a producer and distributor of grain, fertiliser and animal feed. Wynnstay also has a network of retail stores supporting the agricultural/rural market. The group’s footprint is predominantly the west of England and Wales

Wynnstay is currently mid-way through a five-year plan instigated by CEO Alk Brand shortly after his appointment. In broad terms, the aim of Project Genesis is to improve profitability and efficiency and create a more integrated business with stronger potential for growth.

Low growth and poor returns on capital have been a hallmark of this cyclical business, but Brand believes he can change this.

I bought shares in Wynnstay as I was attracted by the (then) deep discount to book value, balance sheet strength and long dividend track record. But as Mark highlighted in February, increased spending has reduced dividend cover and the valuation isn’t as cheap as it was.

Do today’s interim results support continued confidence?

Half-year results summary

Profitability improved sharply during the six months to 30 April, at least on an adjusted basis:

Revenue flat at £304m

Gross profit up 0.7% to £42.3m

Adjusted pre-tax profit up 11.7% to £6.0m

Adjusted EPS up 15.5% to 20.9p

Net cash up 5.8% to £10.9m

Interim dividend up 3.5% to 5.9p

Performance was reassuringly similar at a statutory level, with reported pre-tax profit of £6.2m and earnings of 21.3p per share. I don’t see any concerns over adjustments in these figures.

Trading commentary

Agricultural markets remained mixed during the period. Livestock sectors continued to experience pressure from farm profitability dynamics, whilst uncertainty around government policy and agricultural support schemes remained a feature of the trading environment. The Group also faced ongoing inflationary pressures across labour, logistics, energy and other operating costs.

Feed & Grain (adjusted pre-tax profit +144% to £2.2m): “one of the clearest demonstrations of the benefits being delivered through Project Genesis”. Although manufactured feed volumes were lower on a LFL basis, the reduced cost base and optimisation of manufacturing operations completed last year drove a significant improvement in profitability, while also creating additional manufacturing capacity to support future growth.

Arable (adjusted pre-tax profit +36% to £1.9m): this division benefited from higher manufactured fertiliser volumes and a full-period contribution from the Avonmouth blending facility. Short-term volatility due to the Middle East conflict provided “a modest benefit to profitability”, although much of the spring selling season had already been contracted. No disruption to fertiliser supply chains was experienced during the period.

Stores (adjusted pre-tax profit -36% to £2.0m): the fall in profit was mainly due to “lower small bag feed sales and inflationary cost pressures”. There was some improvement in performance during the second quarter.

It looks to me like the changes made so far through Project Genesis probably are delivering tangible results.

This is reflected in a tangible improvement in profitability at a group level.

Profitability: Wynnstay is a commodity business with a large proportion of pass-through revenue (cost price + margin). This means it can be useful to consider the ratio of operating profit to gross profit when looking at margins:

H1 26 operating margin: 2.0% (H1 25: 1.8%)

H1 26 op profit/gross profit: 14.4% (H1 25: 13.1%)

Trailing 12-month return on capital employed: 6.4% (FY25 underlying: 6.1%)

While low, these metrics are improving and should also be seen in the context of the company’s discount to book value. This increases the effective theoretical returns available to shareholders.

For example, current-year forecasts imply a return on equity of 5.5% based today’s reported book value of 583p per share.

However, the stock currently trades at 358p, around 40% below book value. Buying the shares at this level means current forecasts imply a return on cost of equity of nearly 9%. That’s still not very high, but it’s a lot better!

Unfortunately this is also a reason why I only expect Wynnstay to trade close to book value on rare occasions when it’s enjoying a cyclical boom in profits – unless Project Genesis really can transform the profitability of the business.

Past performance provides a graphic illustration of the cyclicality of this business:

Cash generation: Wynnstay has a heavy seasonality to cash flow due to working capital movements – the company must build up large stocks to support the farming calendar. H1 marks a low point for cash.

Pressure on working capital rose this year due to higher commodity prices, but the impact on cash flow was offset by “strong working capital management”:

As expected, the half year reflected the peak point of the Group's annual working capital cycle. During the period, agricultural commodity prices increased, particularly within fertiliser markets, creating additional working capital requirements. Despite this inflationary backdrop, the Group improved cash conversion through tighter inventory management, aged debt management, disciplined procurement and enhanced working capital controls.

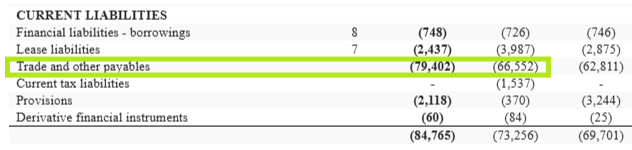

The upshot of this is that Wynnstay ended the half year with a much higher payables balance than last year:

What we can’t tell from these numbers is the proportion of this increase which reflects higher commodity prices, versus the impact (if any) of slower payments to the group’s suppliers.

However, the increase in the company’s receivables balance was on a similar scale to the increase in payables, leaving the receivables/payables ratio largely unchanged. This suggests to me that much of the increase in payables was due to higher commodity prices, with Wynnstay also seeing a comparable rise in the value of unpaid invoices owed by its customers.

Overall working capital remained unchanged at c.£84m at the end of the half year, suggesting to me that the company is indeed managing working capital move successfully.

Of course, the real test of the group’s working capital management will be the year-end balance sheet. Broker forecasts suggest it should fall from £25.7m to £21.5m as the combination of higher capex and dividend payments drive overall cash outflows.

Outlook

The Board remains confident of delivering full-year results in line with current market expectations, representing a further improvement on FY25.

Broker forecasts from house broker Shore Capital are unchanged today:

FY26E adj EPS: 31.5p

FY27E adj EPS: 34.6p

These forecasts put the stock on fairly modest multiples, with the dividend yield still attractive at 5%:

Roland’s view

Wynnstay’s profitability appears to be improving in quite mixed market conditions. The catch is that ongoing higher levels of capital expenditure mean that free cash flow is expected to be close to breakeven in both FY26 and FY27. This means that the dividend will effectively be paid out of the group’s net cash balance, rather than from surplus trading profits.

This may not be a problem if the capex delivers hoped-for results and future cash flow reflects this. But it’s too soon to know how likely this is.

Today’s in line results are broadly encouraging, as far as they go. I think it’s also somewhat positive to see that Mr Brand has spent nearly £80k buying Wynnstay shares since his appointment in October 2024.

Wynnstay’s share price has pulled back somewhat since Mark’s comments in February and the valuation looks relatively more appealing to me today. The StockRanks also have broadly positive view, with Super Stock styling:

I’m going to leave our AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.