Aside from football, there isn’t much overnight news. On the football front, I’m curious to know how many of you will be staying up on Sunday night to watch the Mexico match - is it too late to declare Monday a Bank Holiday?

As there is little news, let’s take a moment to see how my 2026 watchlist performed in H1.

Mortgage Advice Bureau (Holdings) (LON:MAB1): total return minus 22.9%

Hostelworld (LON:HSW): minus 9.3%

Cavendish (LON:CAV) minus 8.8%

Mercia Asset Management (LON:MERC) minus 8.5%

Peel Hunt (LON:PEEL) minus 2.4%

Nichols (LON:NICL) +2.0%

B.P. Marsh & Partners (LON:BPM) +5.3%

PayPoint (LON:PAY) +23.2%

CMC Markets (LON:CMCX) +53.2%

Polar Capital Holdings (LON:POLR) +67.5%

I think this gives an average result of 9.9%, highly concentrated in the top three names.and slightly better than the FTSE All-Share (7.2%).

But if I’m allowed to cherry-pick slightly, I’d also point out that Polar’s year-to-date return improved to +74.6% yesterday, while CMC improved all the way to 117% - so it was an exceptionally nice start to H2! Unless my sums are wrong, the average year-to-date return as of last night was 17.4%.

Overnight market movements:

The FTSE is down 0.1% at 10,470

S&P 500 is unchanged at 7,490

Brent crude (September) is down 1.2% at $70.90/bbl

Gold is up 0.8% at $4,060/oz

Bitcoin is up 0.9% at $60,650

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Halma (LON:HLMA) (£15.0bn | SR76) | Acquired itemedical and Naslund Medical for its Healthcare Sector companies SSG and IZI Medical. Cash consideration for itemedical is €23m (£20m), cash consideration for Naslund Medical is $45m (£34m). | ||

3i Infrastructure (LON:3IN) (£3.5bn | SR49) | Received proceeds of €1.1 billion on 17 June 2026 for TCR. Repaid revolving credit facility in full. Expects to complete €300m investment in LMD, a data centre campus in Norway. Portfolio performing well and income in line with expectations. | ||

Currys (LON:CURY) (£1.79bn | SR92) | Building an ever-stronger Currys (FY Results) & Launch of £50m Share Buyback Programme | Revenue +6%, like-for-like +4%. Adjusted PBT +18% (£191m). Year-end net cash £176m. New £50m buyback. Outlook: trading in new financial year has been very solid, comfortable with market consensus. New CEO starts in August. | |

Pantheon International (LON:PIN) (£1.55bn | SR N/A) | NAV per share +1.2% for the month of May driven by foreign exchange movements (+0.8%) and buybacks (+0.5%). | ||

Great Portland Estates (LON:GPE) (£1.35bn | SR27) | 21 new leases and renewals signed in the quarter. Market lettings on average 3.7% ahead of March ERV. | ||

Supermarket Income REIT (LON:SUPR) (£1.1bn | SR64) | £375 million syndicate and £70 million bilateral loan will refinance all of SUPR’s existing unsecured loan facilities maturing over the next two years. | ||

Baltic Classifieds (LON:BCG) (£866m | SR37) | Revenue +7%, EBITDA margin stable. Operating profit +13% (€60.4m). Outlook: revenue growth of around 10% in 2027, with growth anticipated to be slower in the first half and faster in the second half of the year. Full-year margin to be in line with previous medium-term guidance of mid-70s. | ||

Neuberger Private Equity Partners (LON:NBPE) (£594.5m | SR69) | Neuberger Private Equity Partners Announces H2 2026 Dividend | Neuberger Private Equity Partners Announces 2H 2026 dividend of $0.47 to be paid on 28 August | |

Puretech Health (LON:PRTC) (£321m | SR32) | PRTC’s founded entity Celea announced the completion of a $180 million financing. “This transaction establishes Celea as an independent company with dedicated capital to advance deupirfenidone and a high-quality syndicate to support the company's continued growth.” | ||

Concurrent Technologies (LON:CNC) (£232.7m | SR48) | $9.4m order from a major US defence prime contractor. Order relates to the supply of standard product computer plug-in cards, and a commitment by the customer to procure components to support potential future production requirements (with a short-term cancellation period). | AMBER = (James) Concurrent Technologies secured a $9.4m US defence order, adding to a c.£17m European contract won in June, pushing shares up 1.8%. Both follow strong FY25 results – revenue up 14% to £45.9m, pre-tax profit up 25% to £6.5m – with order intake at a record £47m. The valuation already reflects a lot of this growth (45x trailing earnings, falling to 29.3x for FY27), and Systems remains the key swing factor. Amber: strong execution, but priced for it. | |

James Latham (LON:LTHM) (£206m | SR89) | evenue +7.2%. PBT £25.1m (FY25: £24.3m). “The momentum that we saw in the final quarter of this financial year has carried on into the current financial year, with a slight improvement in the margin and also the volume per working day… Customer demand is quite patchy, with some customers reporting strong order books, while others are somewhat quieter.” | ||

Activeops (LON:AOM) (£188m | SR49) | ARR +46%. Adjusted PBT -23% (£1m). Statutory loss £2.3m after £3m of exceptional costs relating to an acquisition. Trading in the first few months of FY27 has been in line with the Board's expectations. | ||

Genel Energy (LON:GENL) (£145m | SR29) | RECOMMENDED CASH ACQUISITION of Capricorn Energy plc by Genel Energy No.9 Limited | US$4.74 in cash for each Capricorn Share held. | TAKEOVER |

Sintana Energy (LON:SEI) (£103m | SR16) | Sintana Energy announces mid-year operational update with milestones across its Namibia, Uruguay, and Angola portfolio. In Namibia, TotalEnergies farmed into PEL 83 (taking operatorship). | ||

Trifast (LON:TRI) (£96m | SR84) | Trifast FY26 (to 31 March 2026): revenue down 6.7% to £208.4m as it prioritised revenue quality over volume. Underlying EBIT rose to £16.3m (margin up to 7.8%) and underlying PBT to £12.3m. Management points to momentum continuing into FY27 and the strongest pipeline since its strategy began. | AMBER = (Graham) I have zero criticism of anything I’ve read here, in terms of what management are attempting to do strategically: focusing on the quality of revenues, and using EBIT margin and ROCE and their key performance indicators. I’m just not convinced that this stock deserves to trade at a much higher earnings multiple than it already does, given the type of business that it is. | |

Braemar (LON:BMS) (£79m | SR92) | Braemar issued an AGM trading update: positive momentum continuing into the new financial year, with the board confident of delivering profitable growth for FY27 in line with consensus (revenue £139.7m, underlying operating profit £14.2m). James Gundy steps down as Group CEO/director today (staying on for shipbroking activities), succeeded by Grant Foley (previously Group CFO/COO). | ||

Zephyr Energy (LON:ZPHR) (£71.8m | SR33) | Zephyr Energy has acquired another 2,294 acres of TLA leases in the Paradox Basin, Utah. It adjoins its White Sands Unit. It was won via sealed-bid auction, 5-year primary term, 16.67% royalty, funded from cash. | ||

Clean Power Hydrogen (LON:CPH2) (£68.2m | SR N/A) | Clean Power Hydrogen is launching a Retail Offer via BookBuild – new shares at 1.5p each, open only to existing shareholders, targeting a minimum of £0.5m. This is separate from a wider fundraising announced on 1 July. | ||

James Cropper (LON:CRPR) (£33m | SR91) | James Cropper has completed a refinancing: a new £15m invoice discounting facility (committed 3+ years) plus a £7.1m part-repayment of its UK bank loan with the remainder repayable quarterly to March 2030. | ||

PCI- PAL (LON:PCIP) (£32m | SR35) | PCI-Pal has retained HMRC as a customer after a competitive re-tender via a reseller partner. The new deal is an 8-year term with revenue expected broadly in line with the existing contract. CEO notes this is the third of PCI-Pal’s largest customers re-secured on mutli-year terms since the start of FY25. | ||

Insig Ai (LON:INSG) (£16m | SR0) | MoU signed with a new Far East macro fund: Insig AI will build and host its “Fund Engine” – a web app centralising data sources with LLM-based analysis tools. Expected revenues of $240,000 with $120,000 expected in the first three months and $120,000 in the following 12 months. |

Graham's Section

Trifast (LON:TRI)

Down 2% at 68.9p (£94m) - Final Results - Graham - AMBER =

We have FY March 2026 results from Trifast, “the international specialist in the design, engineering, manufacture, and distribution of high-quality engineered fastenings”.

At the trading statement in February, I was neutral, due to a perceived lack of growth, with shrinking revenues and a track record of very average economic returns.

The share price is lower since February and the market doesn’t seem terribly impressed with these full-year results, so maybe my first impressions of the stock were reasonable?

Quick overview of FY26:

Revenue fell 7.3% at constant exchange rates “as anticipated, reflecting softer market demand alongside the strategic decision to focus on the quality of revenue.”

Gross margin improves from 28.3% to 30%.

Underlying EBIT up 9% to £16.3m.

ROCE comes in at 8.5%, improved from 8.1% the prior year.

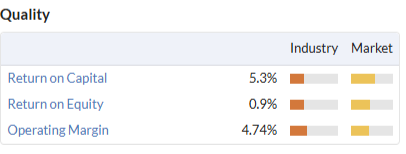

This is higher than Stockopedia’s calculation from the statutory numbers:

Regardless of whether a fair ROCE number is 5-6% or 8.5%, it’s clear that these are fairly ordinary returns - and in the ballpark what you might expect from a company that designs, engineers and manufactures “industrial fastenings”.

Pics from their product page:

Statutory numbers

The actual PBT result is only around breakeven at £0.1m, despite an "underlying" PBT of £12m.

This is due to c. £12m of "separately disclosed items”, i.e. adjustments to the accounts.

Of these, by far the biggest is £6m spent on something called Project Ignite: “the implementation of the Group's cloud-based ERP system, Microsoft Dynamics 365.”

There’s another £2.4m on “restructuring and transformation costs”. The previous year, there were £2.6m of such costs.

Another big item is a £1.4m write-off after the company ceased manufacturing in Malaysia.

Trifast has also been losing money to something called “facilitation payment fraud”. I believe that a facilitation payment is a form of bribery - has Trifast been fraudulently induced to make such payments?

Overall, the level of adjustments to these accounts is very high.

In general, I do not allow companies to adjust out their ERP software costs or their “restructuring and transformation” costs, as these types of costs seem to occur every few years, or even every year in some cases. I see them as a normal cost of running a business, not an exceptional cost, and I'm frankly a bit sick of companies telling us that they are exceptional.

The only compromise I’d be willing to entertain is to maybe spread out the cost of a very large ERP software expense over more than one year. So if you really wanted to spread out the “Project Ignite” costs over a few years, rather than putting them all in a single year, I could go along with that.

Outlook sounds fine:

The Group enters FY27 with improved operational and financial strength, structurally stronger margins, enhanced earnings visibility and a clear path back to profitable top-line growth, focused on key growth regions of North America and Asia.

Positive momentum has continued into FY27, with the commercial pipeline the strongest since the strategy was implemented.

Looking further ahead, “The Board remains confident in achieving the Group's medium-term EBIT margin target of >10%, underpinned by structural improvements in efficiency, mix and pricing.”

EBIT margin for FY26 was 7.8%, up from 6.7% the prior year.

CEO comment:

We are delivering what we said we would do: improving EBIT margins through disciplined, sharper execution and focused strategic change.

FY26 demonstrates that the Rebuild phase is working. We grew profits and expanded margins in a softer revenue environment, reflecting a deliberate focus on quality of revenue over volume.

Graham’s view

I have zero criticism of anything I’ve read here, in terms of what management are attempting to do strategically: focusing on the quality of revenues, and using EBIT margin and ROCE and their key performance indicators.

I’m just not convinced that this stock deserves to trade at a much higher earnings multiple than it already does, given the type of business that it is:

If the results were completely clean, I might be able to take a mildly positive view. And for future reference: if we see really clean profits in H1 or at the next full-year results, I should consider that. I'll keep a close eye on the "separately disclosed items", as always.

For now, however, I’ll stay neutral on this Super Stock. The algorithms like it more than I do:

James's Section

Concurrent Technologies (LON:CNC)

Up 1.3% at 271p (£232.7m) - Concurrent Technologies secures $9.4m order from US Defence Prime Contractor - James - Amber

Concurrent’s announcement of a $9.4m US defence production order pushed the stock into positive territory for the day. The order – its share price up around 1.8% at the time of writing – adds to a circa £17m, four-year European defence contract announced on 11 June to supply over 3,400 VME-based computer board units for ground-based air defence systems.

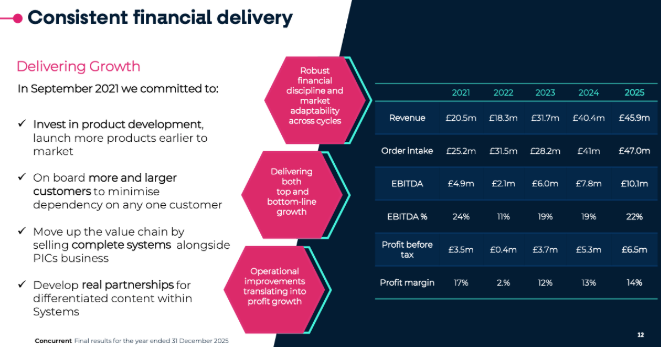

Both these announcements follow a strong set of full-year results, where revenue rose 14% to £45.9 and pre-tax profit up 25% to £6.5m. The company said it was confident of delivering results in line with market expectations for FY26 – Cavendish have forecasted revenue at £52m and EPS of 7.8p.

A broader look at the business's performance since the turn of the decade is very reassuring. Revenue has grown from £21.1m in 2020 to £45.9m in FY25. The consensus forecast sees that figure hitting £59.7m by FY27. Over the same period, net profit has shifted from £2.75m to a projected £8m.

This is the type of growth that investors are willing to pay handsomely for… and that’s exactly what’s happening here. The stock is trading at 45.5x earnings from FY25, and the projected earnings see that figure fall to 36.6x for FY26 and 29.3x for FY27. Coupled with a PEG ratio of 1.48, there’s no clear value signals.

Living up to the valuation

Can it satisfy the valuation? This is the million dollar question. Let’s take a closer look at the business.

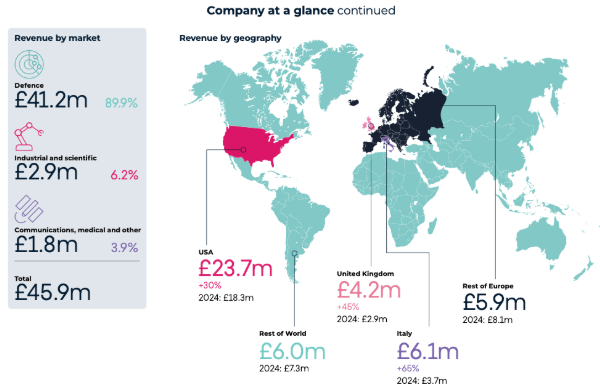

Concurrent designs and manufactures rugged embedded computer technology – hardware built to survive extreme environments and combat conditions. Unsurprisingly, defence is by far the company’s largest segment, representing 89.9% of sales, and its customers include some of the largest primes including Raytheon, MBDA, and BAE Systems.

Interestingly, its largest customer represents 13% of sales, and its second largest at 6% – this suggests sales aren’t overly concentrated as they can be in the defence sector.

Source: FY25 Report

Once a customer designs Concurrent's hardware into a programme, it typically stays there for that programme's life – often seven to ten years. That's the source of the group's order visibility: FY25's design wins alone carry an estimated £145m of lifetime value, work that hasn't been booked as revenue yet but is expected to convert over the coming years. Record order intake of £47m in FY25, plus the two contract wins since the year-end, suggest that pipeline is still growing rather than plateauing.

Source: FY25 Report

However, the margin picture tells a two-speed story. Group gross margins rose to 53.3% in FY25, driven almost entirely by Products, which runs a 57% gross margin. The Systems business is the drag: its gross margin sits at just 16% (up from -7% in FY24) and it posted an operating loss of £0.3m.

It’s the Systems business that offers a lot of the company’s potential, however. Systems revenue rose 160% in FY25 although profitability was delayed due to slower than anticipated contracting. It’s a “watch this space” type thing.

Another factor in the company’s favour is the balance sheet: £14.4m in net cash and no debt, giving management room to keep investing in Systems and new facilities without needing to raise equity.

James’s view

Concurrent's order book and margin trajectory both point the right direction. What’s more, today's contract win is more evidence the pipeline keeps converting rather than plateauing. The margin picture is also largely positive, with the 14.1% operating margin ahead of the industry average according to Stockopedia data.

However, at 45x trailing earnings and a PEG above 1, the market has already given the company credit for a lot of this and potential catalysts look to be priced in –Systems reaching profitability and more design wins continuing to convert at pace are now expectations

I'll keep Concurrent at Amber: a well-run, genuinely growing business, but not one I'd chase at this price without evidence the next leg of growth is landing.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.