Good morning! Today's Agenda is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Halma (LON:HLMA) (£14.8bn | SR75) | Continues to expect mid-teens percentage organic constant currency revenue growth, including a continued benefit from premium growth in photonics within the Environmental & Analysis Sector. Adjusted EBIT margin (excluding the one-off profit in the first half) of around 22%. Cash conversion to be in line with KPI of 90%. | ||

Informa (LON:INF) (£9.97bn | SR51) | Revenue up 6.3% on an underlying basis, adjusted operating profit up 8.7% (to £1,139.8m). 2026 is trading to plan. “We continue to target higher underlying revenue growth in 2026 at 6%±, with B2B Live Events underlying growth of 7%+, alongside double-digit growth in underlying earnings per share…” | ||

Computacenter (LON:CCC) (£3.36bn | SR87) | Revenue +33.2%, services revenue +2.9%. Adjusted operating profit +11.3% (£274.7m). Exited 2025 in a strong position. ”Looking to 2026, while we remain mindful of the uncertain macroeconomic and political environment, as well as the hardware component shortages currently affecting the IT industry, we are confident in our ability to navigate these challenges. Therefore, we expect to make further strategic and financial progress on an organic basis, enhanced by the acquisition of AgreeYa.” | ||

Shawbrook (LON:SHAW) (£2.14bn | SR85) | Underlying PBT +16% to £340.5m. Underlying return on tangible equity was 17.2% (FY 2024: 17.5%). ”We enter 2026 with strong momentum and a clear line of sight to delivering our medium-term guidance. With a scalable platform, prudent capital allocation and proven execution, we are well positioned to continue delivering high-quality growth and returns for shareholders…” Medium-term guidance reiterated, including mid-high teens growth in underlying PBT. | ||

Bridgepoint (LON:BPT) (£1.99bn | SR18) | 13.0% growth in underlying management fees and other income. Assets under management increased by 24.5% to $94.1 billion. Reported profit before tax of £85.7 million (FY 2024: £80.7m). “Bridgepoint posted an impressive performance in 2025 with funds across our platform continuing to deliver for the world's top institutional investors… Looking ahead, we are making excellent progress in fundraising and there is a good transaction pipeline in place for 2026 and beyond.” | ||

Helios Towers (LON:HTWS) (£1.93bn | SR64) | FY 2025 performance ahead of expectations. Revenue +8%, adj. EBITDA +12% ($471m). Profit after tax increased by US$12.4m to US$39.4m. 2026 outlook: adjusted EBITDA of US$510m-US$525m. | ||

TP Icap (LON:TCAP) (£1.83bn | SR86) | Revenue +6%, EBIT +14% (both at constant currency). Adjusted EBIT +10% to £348m. Despite a £9-10m currency headwind, “the Board still expects the Group to achieve adjusted EBIT in line with current market expectations”. Market expectations: adj. EBIT £361m (range of £347m to £370m). | GREEN ↑ (Graham)

I’m fine with upgrading this to GREEN (from Roland’s AMBER/GREEN). The StockRank is strong at 86, the P/E is modest at about 8x even after today’s gains, and it has beaten expectations for 2025. The effect of heightened volatility in oil markets is impossible to predict with certainty but it’s probably not a bad thing for TCAP. So this is looking quite interesting to me here. The share price has stalled since November 2024, but the profit outlook has improved quite a bit since then. | |

Resolute Mining (LON:RSG) (£1.61bn | SR66) | RSG has formally approved the Final Investment Decision for its Doropo Gold Project in Côte d'Ivoire, marking a transformational step towards construction and production. Net cash of US$209m (December 2025). “As the Project advances, Resolute will continue to evaluate all funding options in the context of prevailing market conditions, to maintain its balance sheet flexibility and as additional growth initiatives are identified.” | ||

Energean (LON:ENOG) (£1.57bn | SR48) | Agreement to acquire Chevron's 31% operated interest in Block 14 and 15.5% non-operated interest in Block 14K, offshore Angola. The first step in Energean's strategy to expand its operations into West Africa. Block 14 assets produce around 42 kbbl/d of oil in total, equivalent to 13 kbbl/d net to the interest to be acquired. The base consideration is $260 million in cash. Contingent payments of up to $25 million per annum, capped at $250 million in aggregate, may become payable up until 2038. | ||

Volution (LON:FAN) (£1.24bn | SR57) | Revenue +21.7%, adjusted operating profit +21.1% (£51.6m). Organic revenue growth of 4.2% (at constant currencies). The short to medium-term outlook “remains very encouraging”. “Following the Group's strong first half performance, we expect to make further strategic and operational progress in the second half of the year and the Board now expects adjusted earnings per share for FY26 to be at the top end of the range of market forecasts." Forecasts are for EPS of 35p to 36.5p. | ||

Vesuvius (LON:VSVS) (£1.08bn | SR92) | Revenue +0.7% like-for-like. Adjusted operating profit down 17% like-for-like to £151.1m. Challenging year with difficult end market conditions, particularly in EU+UK. Performance in line with expectations. Whilst we are mindful of the current geopolitical uncertainty, absent an extended disruption, we continue to expect to deliver profit growth in 2026 in line with expectations, on a constant currency basis. | ||

Trainline (LON:TRN) (£739m | SR80) | FY February 2026: net ticket sales +7%, revenue +2% (both at constant currency). “A robust trading performance, in line with previously raised expectations.” Expecting a double-digit percentage increase in adjusted EBITDA, within the previously upgraded guidance range of 10% to 13%. | ||

Alfa Financial Software Holdings (LON:ALFA) (£573m | SR44) | Revenue +15% to £126.7m, Op Profit +17% to £40.1m, PBT +18% to £40.1m, Net Cash £26.4m (FY24: £20.5m). “Over recent years we have been very successful in growing our US business so that it now accounts for 45% of our revenues, which at current exchange rates creates a headwind for growth in our reported results. Overall however, despite the impact of currency headwinds and wider macro uncertainty, we expect to see good revenue growth in 2026 and beyond.” | ||

Restore (LON:RST) (£315m | SR47) | Revenue +27% to £304.7m, Adj. Op profit +18% to £55.5m, Adj. EPS +23% to 22.5p. Net Debt excl leases £123.8m (FY24: £89m). “Trading since the start of the year has been strong. All divisions are performing in line with or above our expectations, and accordingly we expect full year adjusted profit before tax to be slightly ahead of current market expectations.” | AMBER/GREEN = (Mark) Growth here is all acquisition-led with organic revenue from continuing operations down slightly. We therefore need to be careful making investment decisions based on adjusted figures which include all the benefits from acquisitions but exclude all of the associated costs. This is a steady and cash-generative business and using acquisitions to store up sticky customers and shred costs is a good strategy. I am therefore a bit concerned about the buyback announced today, as it will limit the scope for further bolt-ons unless they are willing to relax their leverage target range. However, fundamentally, it is now cheaper than when we last reviewed it, with EPS forecasts rising and the share price dropping. It also appears to have some momentum behind the business, even if the numbers require heavy adjustments to show it. So I am happy to keep our broadly positive view. | |

Ab Dynamics (LON:ABDP) (£285m | SR44) | Positive trading momentum in the final quarter of FY25 has continued during 26H1. Order intake in H1 of £64m (HY25: £66m, FY25: £110m). | ||

On Beach group (LON:OTB) (£280m | SR52) | FY26 bookings +10%, Q1 travelled volumes +14%, Q2 +34%. Limited exposure to ME, but significant slowdown in demand following the onset of conflict in the region, particularly to destinations such as Turkey, Greece, Cyprus and Egypt. Both will impact Group profitability and as a result the Group is temporarily suspending its guidance of £39m to £43m Adj. PBT for the full year. | BLACK (suspension of forecasts after ME impact) /AMBER/GREEN ↓ (Mark) I can see the attraction for long-term holders who believe in the management’s medium-term ambitions. However, with today’s update not being able to quantify the short-term impact of world events, let alone longer-term effects, the uncertainty increases significantly. So at the risk of playing ping pong with our stance, I think we have to be more cautious today. I was also surprised at the lack of reaction prior to today’s news, and I wonder if it makes sense to take a wait-and-see approach across the sector. Especially for those travel businesses that have yet to report the impact they are seeing, or like OTB are unable to quantify it. | |

Secure Trust Bank (LON:STB) (£269m | SR97) | Lending+8.1% to £3.3bn, Continuing PBT Flat at £59.3m, CET1 +60bps to 12.9%. TBV/share +5.8% to £19.73. £10m buyback. “Having taken decisive strategic actions in 2025, 2026 will be a transitional year to launch new products and reduce cost.” | ||

James Fisher And Sons (LON:FSJ) (£256m | SR90) | Revenue +4.3% to £377.2m, u/l Op. Profit +56% to £28.6m (reported PBT £4.3m), Net debt £54.4m (FY24: £56.1m). “Trading has started the year in line with management expectations; the Board remains confident in delivering further progress in 2026.” | AMBER = (Mark) Yet again, I am struggling to see the attraction here. These results appear to be a slight miss, and profit increase requires investors to believe the many adjustments are fair. This calls into question their ability to hit their medium term 10% operating margin target. However, the market appears to have priced in them as if they have already got there, and more, giving considerable downside if they fail. There appears to be little in the way of balance sheet protection at these levels, with increasing net debt once leases are included, and a declining TBV. While the Momentum Ranks stays strong, I am happy to keep our neutral view, but I would be quick to take a more negative stance if that Momentum started to fade. | |

Optima Health (LON:OPT) (£162m | SR67) | Enters partnership with Perkbox to deliver occupational health and wellbeing solutions, expected to deliver £6.5m revenue pa. Forms part of the £8.3m annualised new business that was secured or at preferred bidder stage in the HY26 results. | ||

GreenX Metals (LON:GRX) (£138m | SR11) | LBT $8.21m (25H1: $2.09m Loss), Cash $2.19m (25H1: $6.83m), before raising $13.6m gross in Feb 2026. | ||

Jubilee Metals (LON:JLP) (£121m | SR27) | Secured additional high-grade copper feed material for the Roan concentrator for $1.8m. At Large Waste Project, the sellers have elected to receive the next stage payment of $2.6m in Jubilee shares. Balance of the acquisition $5.4m. | ||

4Basebio (LON:4BB) (£80.3m | SR1) | Scott Lorimer appointed as Chief Operating Officer. | ||

Fairview International (LON:FIL) (£40.3m | SR8) | Revenue +7.1% to £2.98m, PBt +122% to £1.22m, EPS +100% to 0.16p. “The increase in enrolments and applications is particularly encouraging given the additional resources we have invested in marketing our schools since the IPO.” | ||

Abingdon Health (LON:ABDX) (£20.1m | SR18) | $2.5m contract to provide project management and expert technical support for the development and regulatory submission of a clinical self-test. Will commence shortly with the majority of the revenues to be recognised in FY27. | ||

Sareum Holdings (LON:SAR) (£19.3m | SR4) | LBT £1.85m (25H1: £1.33m Loss), Cash £2.49m (30 Jun: £3.55m). |

Graham's Section

TP Icap (LON:TCAP)

Up 7% at 263p (£1.96bn) - Final Results - Graham - GREEN ↑

It’s an excellent headline to start off the full-year results at this major international broker.

Record results, with adjusted EBIT ahead of expectations, announcing an £80m share buyback

They must have had an interesting week or two, considering the action in the oil markets.

Adjusted EBIT is up 10%, while real EBIT is up 14%:

They say that consensus expectations for adjusted EBIT was £345m, so they are 1% ahead of that.

Announcing an £80m buyback, the CEO says:

This strong performance reflects the disciplined execution of our strategy. We grew the business, maintained strict cost control and continued to drive operating leverage. This is evident in our increasingly diversified buy-side and sell-side offering, with both Global Broking and Liquidnet delivering record profitability.

The £80m buyback would eliminate 4% of shares outstanding at the current market cap - not bad.

Let’s take a quick tour their the strategic highlights:

The acquisition of Vantage Capital Markets was recently announced - looks highly complementary.

“Strong broker recruitment in Energy & Commodities” - this division saw a revenue decline in 2025, but I presume it will be busy in 2026?

Ongoing expansion of Liquidnet and investment in the data business Parameta, but there will be no IPO of Parameta in the short-term (“the context remains challenging for an IPO”).

£35m of annualised savings across the group, £10m ahead of plan, with a total of £50m targeted by 2027.

Liquidnet and Parameta are both growing revenues at modest rates: 4% at Liquidnet, 5% at Parameta.

Current trading and outlook

The Group has continued to benefit from supportive market conditions in the current fiscal year to date. We have significant US dollar earnings* and at current spot rates we would anticipate a £9-10m FX headwind to our 2026 adjusted EBIT. Despite this, the Board still expects the Group to achieve adjusted EBIT in line with current market expectations.

Expectations are for EBIT of £361m (range £347m to £370m).

It’s worth reflecting on the statement that they are expecting to do this despite an FX headwind of up to £10m.

I interpret that very positively, as FX movements are of course beyond their control.

Hopefully, for them, the dollar can recover later in the year and enable them to beat expectations.

Checking the GBPUSD exchange rate, I see that it’s up by 3.4% over the past year (from about 1.30 to 1.34). It makes sense that this would feed through to TCAP’s results (60% of its revenues are denominated in USD, versus only 40% of costs).

Graham’s view

I’m fine with upgrading this to GREEN (from Roland’s AMBER/GREEN) for the following reasons:

StockRank is strong at 86

P/E is modest at about 8x even after today’s gains.

Highly reputable businesses (this is a giant in global financial markets, even if it’s not a household name).

Nice mix of brokerage and data services.

Beating expectations for last year and trading in line for the current year, despite an FX headwind (suggesting very strong underlying trading).

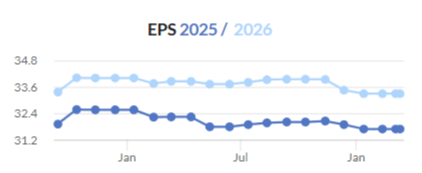

Earnings forecasts have oscillated within a narrow range, implying good visibility:

The effect of heightened volatility in oil markets is impossible to predict with certainty but it’s probably not a bad thing for TCAP.

So this is looking quite interesting to me here. The share price has stalled since November 2024, but the profit outlook has improved quite a bit since then:

Mark's Section

Restore (LON:RST)

Up 5% at 243p - Full Year 2025 Results - Mark - AMBER/GREEN

So far this year, the share price has been tracking downwards, reflecting generally weak market conditions for companies of this size:

However, it seems unlikely that their core business of document storage and shredding should be impacted by UK government policy or the war in Iran, and so it has proven. Revenue from continuing operations is up 27% to £304.7m and Adjusted EPS comes in at 22.5p versus the 22.1p consensus in Stockopedia. However, both of these are slightly problematic:

Organic Revenue Growth:

When we’ve reviewed this on the DSMR in the past, we have commented that it is hard to justify a P/E greater than high single figures for a business without organic growth. In these results, they say:

Organic growth was broadly flat as we continued to focus on operating margins, particularly in our digital and IT Lifecycle activities.

Broadly flat, of course, means slightly down. Things look better going forward, where they say “We expect to see healthy organic growth in 2026, now that our businesses are in the right shape.” but this doesn’t quantify this. Is “healthy” just slightly above inflation at say 5%, or more like 10-20%? And how far into the future can this organic growth be sustained? These factors make a huge difference to the multiple that investors should be paying for this business.

Looking at brokers’ notes for guidance, I see Canaccord have around 13% revenue growth for FY26 pencilled in and around 5% for the following years. Cavendish are more conservative at 10% and 3%, respectively. Without a significant acquisition spend forecast, these will be the expected organic growth rates. With a small amount of operational gearing, a high single-digit EV/EBIT multiple should be justifiable.

Adjustments:

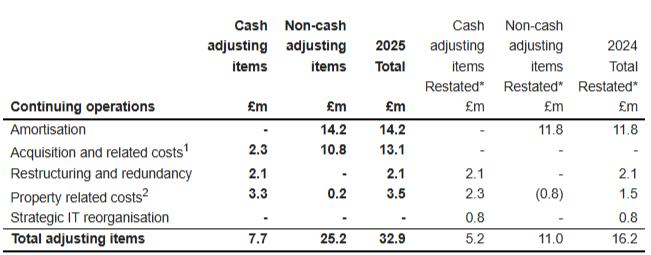

What stands out is that you can drive a lorry full of document storage boxes between the adjusted and statutory earnings:

Here’s how the figures break down:

While the majority of these are non-cash, there is no getting around that a company such as this has significant leeway in their reporting of adjusted EPS. When they include the profit benefit from acquisitions, but exclude the cost of making those acquisitions and rationalising the cost-base of the acquired companies, then the adjusted figures are always going to improve. In this case, the period contained significant activity on this front:

Acquisition of Synertec and six further bolt-ons, expanding the Group's capabilities across inbound and outbound communications and strengthening market share in shredding.

Outlook:

2026 has started well:

Trading since the start of the year has been strong. All divisions are performing in line with or above our expectations, and accordingly we expect full year adjusted profit before tax to be slightly ahead of current market expectations

However, I am mindful of the dynamics described above. They say they have made two further bolt-on acquisitions in early 2026, so with them likely adjusting out the acquisition costs, it should not be surprising that adjusted PBT forecasts increase.

Canaccord increased their FY26 adj. EPS by 3.7%, from 24.1p to 25.0p, which follows a 5% upgrade they made in December. Cavendish make no change as they were already at a more aggressive 26.5p for FY26 adj. EPS.

The company is clearly benefiting from work over the last few years to improve the profitability of their core businesses. For example, in Technology, they generated an adjusted operating profit of £2.8m vs a loss of £1.4m in 2023.

Balance sheet:

There are further signs that these improvements have a significant acquisition component. Net debt excluding lease liabilities rose from £89m to £123.8m. This is within their 1.0 - 2.0x target range, but at 1.9x, it is at the upper end.

This is expected to reduce slightly during 2026. However, Canaccord increase their 2026 year-end forecast to £120m from £103m, partly due to them estimating £15m of shares bought back in the period. This suggests that there may not be as much headroom as in the recent past to make these earnings-enhancing bolt-ons while remaining within their target leverage.

Earnouts from past acquisitions appear to be accounted for as “Other payables”. These have gone from £0.2m to £16.0m over the past year. Personally, I would treat this as additional debt, as it is highly likely to be paid in cash, unless things go seriously wrong with the acquired businesses.

Cash flow:

Things look much better on the cash flow front, with reported Free Cash Flow up 4% to £42.9m. The company increase their dividend by 19% today and initiate a £20m buyback. A 7.8p dividend is forecast for FY26 costing around £10m. Canaccord say these are “both funded by FCF without limiting future growth investment”, I’m not sure I agree with this statement. Current forecast FCF is largely going on the dividend and buyback in FY26. If they want to make further material acquisitions it will require them taking on further debt and relaxing their target leverage multiple.

Mark’s view

The reality is that this is a relatively mature business that will not grow quickly without further consolidation. I don’t think we should place too much faith in adjusted figures, which take all the benefit from acquisitions and don’t include any of the costs. However, that doesn’t mean they don’t have significant opportunities to acquire bolt-on businesses, eliminate duplicate costs, and keep scaling up. This tends to be a profitable and sticky business, which means it has nice, predictable cash flows. This enables them to run with high leverage and further juice the returns to equity. The process of storing up customers and shredding costs is a fundamentally good one.

I am therefore a little concerned that the inclusion of a buyback means acquisition opportunities are weaker than in the past, or that they will need to push their leverage ratio to make them. The good news is that this should help support a share price that has been weak recently, perhaps more due to institutional flows than changes in the business outlook.

Both Canaccord and Cavendish have pretty high price targets, making the case for undervaluation compared to global peers, or where the company has traded in the past. However, they make this case using some pretty punchy multiples, in my opinion, for a business that has mid-single digits organic growth potential over the long-term, and limited scope for further acquisitions. However, it is a steady, cash generative business that is doing the right things in order to turn around its struggling parts, and grow the rest (via bolt-ons).

Fundamentally, it is slightly cheaper today than when we last reviewed it on the DSMR, having had some modest EPS upgrades and a share price that has fallen. So I see no reason to change our previous AMBER/GREEN stance.

On Beach group (LON:OTB)

Down 11% at 171p - AGM Trading Update - Mark - BLACK (suspension of forecasts after ME impact) /AMBER/GREEN ↓

For the first five months of the year, things have been going well here with positive momentum building:

· FY26 bookings: +10%1 and bookings from repeat customers +19%

· Q1 FY26: travelled volumes +14%

· Q2 FY26: travelled / departure volumes +34%.

However, this is one of the first instances where we are seeing the direct impact of the Iran war in the numbers, rather than the market anticipating the impact:

Current trading from 1 March 2026

Whilst the Group has limited exposure to destinations in the Middle East, it has experienced a significant slowdown in demand following the onset of conflict in the region, particularly to destinations such as Turkey, Greece, Cyprus and Egypt. It’s impossible to predict when the conflict will end, and the pace at which demand for these destinations will recover, but both will impact Group profitability. As a result the Group is temporarily suspending its guidance of £39m to £43m Adj. PBT for the full year.

This makes sense. I think the direct impact is pretty limited. The chances of being hit by an Iranian missile while on holiday in the Eastern Mediterranean is incredibly low. However, as events in Dubai have shown, it doesn’t take much to create significant disruption.

The reason most people book package holidays is that they have to organise very little themselves and don’t have to worry about things that independent travellers have to consider. If disruption becomes more common, it’s easy to imagine these types of bookings drying up.

Perhaps the most worrying aspect is that they are unwilling to quantify the impact of the Middle East turbulence. This makes it very hard to say whether today’s 11% drop in share price is an overreaction.

What is a little surprising to me is that the market hadn’t anticipated this disruption, with the shares only down around 7% over the last month:

While On The Beach doesn’t have the same direct costs as someone like Jet2, which operates its own aircraft, I expect that flights to “safer” destinations will increase as higher fuel costs are reflected in fares. (OTB doesn't block-book flights, but rather books the individual flights in real-time when a customer confirms a holiday on their website).

There is some reassurance that they continue to trade profitably and generate cash. However, it would take quite some disruption for them to go from £39-43m EBIT on £138m forecast revenue to a loss, so this isn’t as comforting as it first sounds.

They also remain committed to their medium-term “ambition” of “£2.5bn TTV, £100m EBITDA, £85m PBT and 38.7p EPS.” It seems a bit strange to quote a precise EPS figure; how will they know precise finance or tax charges in the future?! However, it is clear that the current share price of 170p-ish will look too cheap if they hit these figures. Even before today’s withdrawal of guidance, I can’t see any specific recent coverage on Research Tree. I’m guessing these are described as “ambitions” as they are further out than the current forecast window. In the current environment they may prove too optimistic.

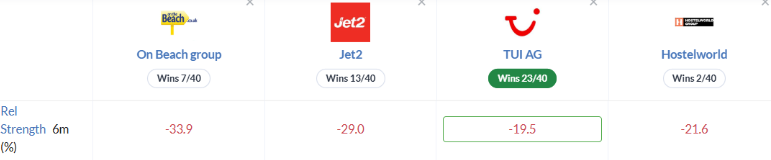

Read across:

I am also surprised by the lack of reaction elsewhere in the sector. Jet2 appears to have reacted to this announcement by dropping 4% today. Overall, though, both Jet2 and Hostelworld are only down around 10% over the last month, not that far off where OTB was prior to today’s fall. While they have different business models and target markets, the scope for continued disruption is still high.

Tui has dropped 20% in the last month, although it still has higher relative strength over the last six months:

I’m not sure I’m keen to jump in anywhere in this sector at the moment. The scope for continued disruption far beyond initial expectations seems quite high to me.

Mark’s view

Graham upgraded OTB to GREEN when he last reviewed it on the DSMR, on valuation grounds. The price is now understandably below that level, and I can see the attraction for long-term holders who believe in the management’s medium-term ambitions. However, with today’s update unable to quantify the short-term impact of world events, let alone longer-term effects, the uncertainty increases significantly. So at the risk of playing ping pong with our stance, I think we have to be more cautious today. AMBER/GREEN.

James Fisher And Sons (LON:FSJ)

Up 1% at 510p - Preliminary results - Mark - AMBER =

I've always struggled to see the attraction in James Fisher and Sons. But the SuperStock moniker, and the investment from turnaround specialist Rockwood Strategic, suggests I am missing something.

I am hoping today’s results will change my mind. But the top-line figures aren’t a great start…:

Revenue increased 4.3% to £377.2m

The only forecast I can see is from Singer, who had £395.9m revenue pencilled in, so this seems like a miss. Reuters’ third-party reporting seems to confirm it:

UK marine services firm's 2025 revenue fell 9.9%, missing analyst expectations.

Adjusted operating profit for 2025 missed consensus.

Company cites disposals and staged closures as main drivers of revenue decline.

Regardless of this analysis, I expect a company trading on a 20+ P/E ratio to be growing faster than this.

Things are better on the profit front though:

Underlying operating profit increased 56.3% to £28.6m

At least on an adjusted basis:

Reported profit before tax of £4.3m (FY24 £54.0m, which included £54.9m from gain on disposals)

Adjustments:

As usual when there is a big gap between adjusted and reported figures, we need to dig out the details:

None of these looks particularly one-off, apart from £2.2m of pension payments included in “Other”:

Other - comprises costs outside the normal course of business, including exceptional legal and professional fees relating to isolated matters. It also includes £2.2m associated with the estimated settlement of a historic pension matter.

Amortisation and impairment are, at least, non-cash.

Balance Sheet:

They say “net debt reduced in the year to £54.4m” in their headline. But when I look at the details, this is down from £56.1m. In other words, it’s barely budged. This excludes lease liabilities which have increased with the leasing of additional tankships, meaning net borrowing, including all lease liabilities, was £144.1m versus £108.0m at the end of 2024.

Overall, the balance sheet doesn’t seem that strong to me. Payables now exceed receivables and there are increasing provisions. There is little in the way of tangible asset value backing, and the tangible book value has been declining:

Outlook:

The outlook statement is in line:

Overall market conditions remain largely supportive, and 2026 trading has started in line with management expectations. Whilst early in the year and mindful of macroeconomic and geopolitical uncertainties, the Board remains confident of delivering continued progress in 2026, building further towards our medium-term financial targets of 10% underlying operating profit margin and 15% ROCE.

However, that means a forward P/E of over 20. Singer forecasts growth into 2027, but that requires some faith, given today’s revenue miss, and still doesn’t make them look cheap.

It is also worth thinking about what their “medium-term financial targets” actually mean. A 10% margin on roughly £400m in revenue is £40m in EBIT. Say we give them a 10x EV/EBIT rating, that would be an EV of £400m, or a market cap of around £245m, pretty much today’s figure.

There may be some modest revenue growth. However, this would be based on 2028 or 2029 numbers and would need to be discounted back to today. All in all, it seems like the market has already priced in the medium-term targets as having been met, whereas the company’s history would throw considerable doubt on their achievement. Plus, the word “adjusted” may continue to do the heavy lifting in their results.

Mark’s view

I’m sure there is some grand plan that I’m missing which will appear in forecasts well outside the forecast window. However, yet again, I'm still struggling to see the attraction. If the company is doing well in the current defence and oil environment, why would they suddenly see a step-change in fortunes? Their “medium-term financial targets”, if achieved, make them look fairly valued today.

Given the strong MomentumRank, I’m happy to keep our previous neutral stance, but would be quick to take a more negative view if that Momentum starts to fade. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.