Good morning! The Agenda is now complete (we think!).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Next (LON:NXT) (£11.7bn) | Full Year Results | Sales in the first 8 weeks of FY Jan 2026 are ahead of exps. Upgrades guidance. | GREEN (Graham holds) |

Playtech (LON:PTEC) (£2.2bn) | Full Year Results | Adj. EBITDA slightly ahead. New medium-term financial targets, including adj. EBITDA €250-300m. | |

International Public Partnerships (LON:INPP) (£2.0bn) | Full Year Results | NAV per share falls from 152.6p to 144.7p. Primarily due to increase in discount rates. | |

James Halstead (LON:JHD) (£638m) | Interim Results | Rev -5%, PBT +4% (£28.5m). H2 started well. Govt spending is expected to increase during 2025. | |

Chesnara (LON:CSN) (£421m) | Full Year Results | Cash generation £60m (LY: £52m). PBT £21m. Outlook for M&A remains positive. | |

Franchise Brands (LON:FRAN) (£264m) | Full Year Results | System sales +20%. Adj. PBT +8% (£21.3m). Full-year adjusted EBITDA in line (£35m). | AMBER (Graham) [no section below] These accounts are heavily adjusted with over £10m of amortisation and £1.5m of share-based charges. But operating cash flow is very good at £33.7m, with minimal capex and software spending. However the balance sheet provides no tangible support and is deeply in the red on a tangible basis, underlining the need to deleverage. I’m a fan of the franchising business model and management are highly credible. It’s tempting to give it an upgrade here on valuation grounds. Stockopedia classifies it as a Falling Star. |

Enquest (LON:ENQ) (£247m) | Full Year Results | Production efficiency c. 90%. Profit after tax $93.8m. 2025: expected to average 40 - 45k boepd. | |

M&C Saatchi (LON:SAA) (£207m) | Full Year Results | 2024 in line. LfL revenue +0.4%, PBT +4.2% (£30.5m). Outlook in line. | AMBER (Megan) Encouraging signs of a positive strategy starting to deliver the turnaround. But the market remains unmoved for now. |

Arbuthnot Banking (LON:ARBB) (£149m) | Full Year Results | EPS -32% to 152.3p, Net Assets £267.0m, Total dividend 69p (2023: 46p), an increase of 50%. | |

Somero Enterprises (LON:SOM) (£143m) | New CEO | Outgoing CEO Jack Cooney has been in position since 1997. The new CEO has been COO at a large trailer manufacturer, President at another equipment manufacturer, and for 22 years was with Deere & Co. | AMBER (Graham) [no section below] Jack Cooney is in his late 70s and could have retired already if he wished. It makes sense to pass on the baton. I am neutral on this stock as while I like the company, I think competition has become more intense with a cheaper rival making life more difficult for Somero. Hopefully the new CEO can come up with a plan to reinvigorate strategy. He mentions international growth potential in his comments today and this is another source of opportunity where Somero could do better. |

Capital (LON:CAPD) (£122m) | Full Year Results | Rev +9.3%, Adj. Op. Profit -21.5% to $47.3m, Basic EPS -61% to 6.8c. |

AMBER Mark (I hold) |

Microlise (LON:SAAS) (£121m) | Full Year Results | Rev +11% to £79.5m, Adj. Op Profit +13% to £6.3m. Cash £11.4m (FY23: £16.8m). Cash & Adj. EBITDA exceeding market expectations. Confident in prospects for 2025. | AMBER/RED (Mark - no section below) They say that cash & adj. EBITDA are ahead. However, EBITDA is meaningless for companies that capitalise intangibles and cash balance is down due to an acquisition. This added £4.9m of revenue in 2024, making the organic growth rate look mediocre. Too low to justify an 18x forward P/E. The algos rate this a high flyer, but with a momentum rank of just 59 and a 1-yr RS of -28%, I wonder for how long. |

SRT Marine Systems (LON:SRT) (£115m) | Half Year TU | Rev +370% to £26.2m, EPS 0.93p, Net debt £9.8m, Cash £4.5m but receivables of £32.5m, mostly paid after period end. | |

Seeing Machines (LON:SEE) | Interim Results | Rev. broadly flat at $25.3m. LBITDA $9.7m (24H1:$14.3m). Cash. Net debt $8.8m. Cost reductions to get to cash flow B/E in 2025. | |

Tribal (LON:TRB) (£85m) | Full Year Results | In line with TU on 31st Jan. ARR +6.5%, Rev +6%, Adj. EBITDA +17.8% to £16.7m. 25H1 In line. | AMBER/GREEN (Mark) |

Wynnstay (LON:WYN) (£69.4m) | AGM Update | In line & slightly ahead of last year. | |

Town Centre Securities (LON:TOWN) (£56m) | Interim Results | EPRA NTA flat at 277p/share, EPRA EPS 4.2p (HY24: 7.9p). LTV from 50.8% to 50.1%. Outlook: ”Resilient trading performance has continued” | |

Brave Bison (LON:BBSN) (£32.3m) | Acquisition | Up to £3.5m for performance marketing agency Builtvisible |

AMBER/GREEN (Mark - I hold) |

Robinson (LON:RBN) (£20m) | Full Year Results | Rev +14% to £56.4m, U/L Op Profit +45% to £3.2m, FY24 In line. Broker raises FY25 forecasts by 8.6%. | |

React (LON:REAT) (£17m) | AGM Statement | “…continuing to perform well in challenging market conditions…reduced customer activity…” | |

Empresaria (LON:EMR) (£13.0m) | Full Year Results | NFI -12% to £50.4m, Adj. Op Profit -25% 25% to £3.8m. EPS -1.0p, net debt up to £15.3m. | AMBER/RED (Mark - no section below) These results are in line with most of the sector, i.e. terrible, but unlike most peers, they run with significant debt instead of cash. This has to limit their ability to grow business when any recovery comes and adds to the risk that they don’t survive to see any uptick in prospects. |

Airea (LON:AIEA) (£10.3m) | Final Results | FY Revenue flat, U/L Op. Profit -13% to £1.6m. |

AMBER (Mark) |

Northamber (LON:NAR) (£7m) | Interim Results | EPS -2.2p, Net assets £21.7m. | AMBER/RED (Mark - no section below) |

Graham's Section

Next (LON:NXT)

Up 8% to £108 (£13.3bn) - Full Year Results - Graham - GREEN

At the time of publication Graham has a long position in NXT.

It’s difficult to find any fault in these financial headlines:

Full-price sales +5.8%, group sales +8.2%

PBT +10.1% (£1,011m)

Pre-tax EPS +11.6%, enhanced by buybacks

And the new year (FY Jan 2026) has started well. But remember that NXT always makes cautious estimates of its future performance, so that it very, very often does beat its expectations.

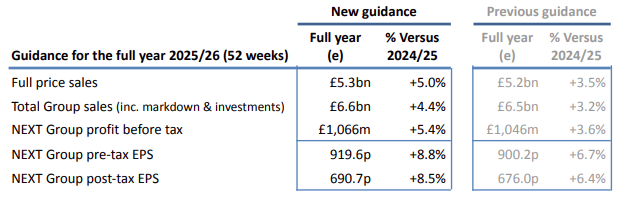

Full price sales in the first 8 weeks ahead of expectations

Upgrades full price sales guidance for H1 to +6.5% (from +3.5%), resulting in sales for the full year +5% (from +3.5%).

PBT guidance increased by £20m to £1,066m, which would be growth vs. the prior year of +5.4%. With the help of share buybacks, EPS is to grow by +8.5%.

Management Commentary - it’s nice to read that “we are as positive about the Company today as we were then”, referring to last year’s annual report.

As usual, there is very helpful information on the company’s strategy - the “Big Picture”.

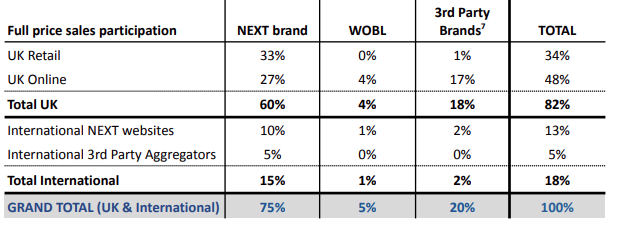

The table below gives a nice overview of sales.

“WOBL” means wholly owned brands and licences - things like “Love & Roses” and “Baker by Ted Baker”.

3rd Party Brands includes Reiss, FatFace and Joules but it does not include their sales through their own channels. The table below only relates to Next’s own channels:

So we have 60% of sales relating to the NEXT brand in the UK, which are still mostly Retail rather than Online.

20% of Sales relate to 3rd party brands, most of which are Online.

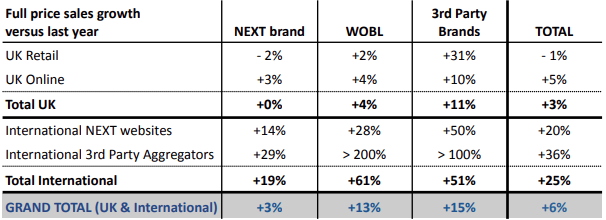

The same table is given with growth in every category:

Key points for me are that total International sales are rising at an impressive 25%, vs. Total UK growing at just 3%.

And then within the UK, the NEXT brand is flat (+0%) while 3rd Party Brands are growing faster, +11%.

Management commentary continues with its usual wisdom, to give one example:

We are very wary of grand visions: few things date faster than a vision of the future. Yet if global fashion tastes do continue to converge then it is likely that, online at least, a small number of increasingly global brands will serve more and more of the world's fashion needs. Our aim is to create ranges that are strong enough for NEXT to earn its place as one of those brands.

There is a risk here: some readers might think that becoming a global brand was an objective in itself. For clarity, our aim is to profitably serve as many customers as we can, and selling overseas is an opportunity to further that aim. Shareholders need not worry that we will open unprofitable shops, or make bad marketing investments, in the abstract pursuit of “global” status

Next’s report is 84 pages long and I have about 20 other companies I could look at today, so I’ll have to cut my remarks short. But let’s try to pick up a few other key points before wrapping this up.

Zalando SE (ETR:ZAL) - Next’s “aggregation partner” in Germany. This relationship appears to be deepening. Later this year, orders taken on Next’s European sites and on Zalando’s own sites will be fulfilled from the same operation through Zalando’s warehousing and distribution business.

Adjustments: these are beautifully clean accounts with £1,011m of “NEXT Group profit before tax” converting to £987m of statutory PBT. That’s nearly a 98% conversion rate!

Forward guidance: while the company has upgraded its H1 guidance, it’s leaving H2 guidance unchanged for two reasons:

H2 was much stronger than H1 last year, so there are tough comparatives.

UK tax rises in April are expected to weaken the UK employment market and negatively impact consumer confidence.

One of the reasons I’ve been so nervous about the broad impact of higher NICs is that I value Next’s views so highly - I probably trust them more than I trust many economists, when it comes to the economy! Let’s hope that they are being overly cautious, as usual.

I’ll post this as an example of the type of guidance every company should provide as a matter of routine:

They also provide a very detailed bridge between the profit result for FY Jan 2025 and the expected profit result for FY Jan 2026, showing all of the factors that are expected to improve or worsen the result this year.

For example, wage cost inflation and higher NICs are expected to cost £67m, which approximately matches the £66m benefit from 5% growth in full price sales. They separately expect a £71m benefit from various cost savings, operating efficiencies, and gross margin improvements from higher prices.

Net debt finished the year at £660m, down £40m (excludes lease liabilities).

Dividends: the company expects to pay £286m in dividends this year.

Buybacks: even after paying the dividend, they expect to have £426m of surplus cash. £110m of this will be retained to help pay off a £250m bond that matures this year. They intend to spend the remaining surplus of £316m on buybacks.

Graham’s view

Next remains the gold standard when it comes to transparency, honesty and helpfulness in company reporting. See my comments in January and October for further background.

The shift from retail to online continues but at a slow pace, with only a 1% reduction in total UK Retail sales across all brands, vs. 5% growth in Online sales.

A large part of me wishes that the shares were cheaper, so that the planned buybacks gave EPS a bigger boost. At this valuation the buybacks aren’t going to boost EPS by all that much:

The stock is ranked as a High Flyer and I think I’ll upgrade my stance on it from AMBER/GREEN to GREEN. My reasons are:

While in general I’m very concerned about higher NICs, Next has provided very detailed guidance to explain how it will hit its profit forecasts this year despite that headwind.

Unlike other retailers, Next has the profit margin to enable it to absorb these costs - a competitive advantage that will further cement it as one of the “last men standing” in retail.

New revenue and profit guidance is still very cautious for H2. I’m inclined to think that further upgrades are likely.

This isn’t the bargain it’s been before, but its competitive position has never been stronger.

Megan's Section

M&C Saatchi (LON:SAA)

Unchanged at 170p (£208m) - Full year results - Megan - AMBER

M&C Saatchi (LON:SAA)’s share price recovery back to pre-Covid levels has enjoyed two main surges. The first came to a halt in 2022 after a series of takeover bids fell through, and the second wound down last summer after the company failed to report financial results for more than six months after the financial year end. Since then, the share price has meandered downwards as wary analysts have cut their earnings forecasts for both 2024 and 2025.

This morning, the company has announced that adjusted earnings for 2024 were in-line with those lower forecasts at 17.6p. That’s a 6% improvement on last year - a reflection of the slight uptick in adjusted net sales and a major improvement in margins thanks to a better mix of high margin non-advertising revenue.

There’s a fair amount to dig into here. But thankfully, management seems to be trying to make amends for its poor results communications last year, by laying out its results in great detail.

Heavy adjustments warranted?

The first is that the company wants to draw our attention to the like-for-like results. That’s hardly surprising. While sales were down on a reported basis and operating margins still below 10%, on an adjusted basis, the numbers were far more encouraging.

When it comes to sales, the like-for-like numbers are far more useful. In 2024, M&C Saatchi made progress away from its dependency on advertising, which included the removal of its poorly performing South Africa business. Like-for-like revenues were up 3.7%.

But in the profit figures, management seems to have got a little carried away with its adjustments. There are £12.7m of operating costs stripped out of the like-for-like numbers which have nothing to do with discontinued businesses (this compares to £25m of adjustments last year).

I don’t like it when companies include amortisation as a cost to strip out of ‘adjusted’ figures. These are costs which will continue to repeat year after year. I am also unconvinced that stripping out the £7.2m of ‘global efficiency restructuring’ costs should be taken as one-off. M&C Saatchi still has more restructuring to come so more costs of this nature can be expected next year.

On an adjusted basis, operating margins were a resilient 15.4%, but it’s actually the underlying number which was more impressive to me. Sure, it’s still languishing in the single digits, but the underlying operating margin of 9.7% is still a big improvement on last year and reflective of a better sales mix.

What are ‘Issues’?

Which brings me onto my second key point. Improving margins are a reflection of the greater mix of non-advertising revenues. These are the sales generated from PR services and consulting projects including branding, messaging and technical.

The main area of growth comes from a division which management refers to as ‘Issues’. It’s not entirely clear what these sort of services are, but it appears to be services rendered to government bodies and organisations which require specialist skills. Management says these customers are sticky, meaning barriers to entry are high.

‘Issues’ sales rose 27% in 2024 to £58m, which means they now contribute a quarter of total company revenue. The company doesn’t break down the profit mix from individual operating segments, but as this was the only division to report revenue growth, I assume margins are quite strong. The sales contribution from the lower margin ads business is now just 33%, compared to 61% in 2020.

Imminent seller alert

In 2022, renowned tech investor Vin Murria took a stake in M&C Saatchi worth £15m (as part of her attempts to acquire the entire business). She now owns 12% of the shares in issue.

There is speculation that Ms Murria will be looking to exit at some point in the not too distant future, meaning there could be quite a significant seller in the market. A potential cloud to watch out for.

Megan’s view:

Results today are certainly encouraging. After years of troubles stuck in the downward cycle of advertising demand, M&C Saatchi seems to at last have a strategy that can prompt proper growth. Shares are trading on 8.5 times 2025 forecasts, which looks decent value, especially given the fact that those forecasts look more resilient than they have done in a while.

But the market doesn’t yet seem moved by the promising signs and until I see a change in momentum, I am happy to watch this one from the sidelines. AMBER

Mark's Section

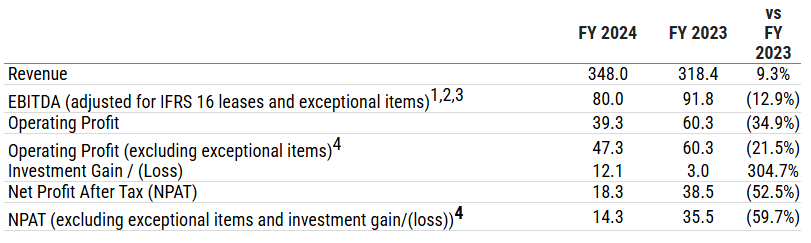

Capital (LON:CAPD)

Down 2% to 61p - Final Results - Mark (I hold) - AMBER

Revenue is up here, but that is the only bright spot, with pretty much every metric going the wrong way:

The investment portfolio, which is one of the reasons some investors don’t like this business, is actually one of the few bright spots. I can’t help feeling I should have sold my shares a few years ago and just mirrored their listed equity portfolio, which has performed far better!

They are still profitable, though and highly cash generative:

The problem is that this has gone back out of the door in capex, leading to an increase in net debt, despite selling a chunk of their listed investments during the year.

With these results, it is not surprising that the CEO recently fell on his sword, and it is left to founder and executive Chair, Jamie Boynton, to pick up the pieces. So what has gone wrong?

Firstly, their only two mining contracts came to an end:

Sukari Gold Mine (Egypt) waste mining contract came to its natural end in September 2024; and

At Belinga (Gabon), the customer gave notice to conclude our mining contract early in Q4 2024, as they altered their development strategy at the project.

This has left them with a load of mining equipment that is not being utilised. One option was to sell this. However, they have decided that they will generate higher returns by deploying this to the operation of an existing major client, Barrick. The downside is that this takes time to ramp up:

§ Early works civils focused on the construction phase of the project prior to first production. The first items of equipment are anticipated to arrive on site in H1 2025; and

§ Tailings storage facility ("TSF") mining services, with phased arrival of further equipment on site planned through 2025 with a gradual ramp up in operations from Q4 2025 onwards and currently envisaged to be at run rate utilisation in H2 2026.

Secondly, they have seen delays in the ramp-up of their drilling contracts in North America. There is a distinct lack of commentary in these results, and I would have liked to have seen more details on this, given that this has been largely responsible for the weakness in trading. In January, they said:

However, as previously announced, Nevada Gold Mines ("NGM") has seen delays which has had significant impact on Group margins with the contract revenues not yet supporting the cost base put in place to deliver the project.

This has also impacted the labs business. This has been generating high revenue growth for a number of years, but as is often the case with high-growth businesses, they can’t maintain this indefinitely. Here, the notes in the annual report show that losses have increased:

The overall impact is:

As a result, we expect margins to bottom in H1 2025 and see a recovery thereafter. 2025 revenue is expected to be in the range of $300 - 320 million with revenues H2-weighted given the ramp up of new projects, predominantly in our mining business.

The result is a further reduction in EPS for FY25:

This makes the company no longer cheap on earnings, even if one ignores the net debt.

None of these issues seem unfixable, though. The company now trades on a P/TBV of 0.58. These assets have been quite productive in the past. Here is what the company expects for the future:

Mark’s view

There is no doubt that this has been a disappointment. Management have clearly bitten off more than they can chew with so many new developments. This indigestion is now clearly visible in the financial results. However, this entrepreneurial team have a history of growing a business generating very good returns on capital. I wouldn’t bet against them being able to do this again. At this stage, I think the AMBER rating that Roland gave this recently seems about right.

Tribal (LON:TRB)

Down 11% to 35.7p - Final Results - Mark - AMBER/GREEN

The market hasn’t liked the results here, which seems a bit strange, as only two months ago, the market was bidding the shares up on an ahead statement:

EPS come in line with these updated forecasts:

Adjusted basic earnings per share from continuing operations before exceptional items and intangible asset impairment charges and amortisation, which reflects the Group's underlying trading performance, increased to 4.7p due to the improved adjusted profit before tax in the year.

Although, this is another company where the gap between adjusted and statutory figures is huge:

Statutory basic earnings per share increased to 2.6p (2023: 2.5p) as a result of the statutory profit in the year of £5.5m (2023: £5.3m).

Here are the details:

While not ideal, most of those do appear to be genuinely one-off or non-cash. Although, there is about £1m of restructuring costs, and this does appear to be an ongoing, although down from around £2m the year before.

It goes without saying that adjusted EBITDA is a completely pointless measure for any company that capitalises intangible development costs and can be ignored completely.

I find that cash flow is often a better measure of performance when it comes to companies that heavily adjust their figures. Here, operating cash flow comes out as £12.67m. Taking of £2.152m of tax, £1.066m of interest, £4.683m of capex, and £0.844m of lease payments gives £3.925m of free cash flow before movements in working capital. This works out to a P/FCF of around 20. So, it is not immediately great value, but not dafty-rated either, especially if we accept that their investment into intangible assets is generating value.

There isn’t a lot of debt, with Net debt at 31 December 2024 £3.2m, down from £7.2m in 2023. The gross debt is £8m, but paying over £1m of interest suggests that this is not the normal state of affairs during the year. I would like companies to be required to state the minimum, maximum and average net debt during the year as this would be far more informative than the balance sheet figure. The difference is probably because, like many software companies, their cash balance is a function of being paid up front for software licenses. The balance sheet shows both trade payables and contract liabilities increasing:

Current liabilities exceed current assets by £23.5m given a low current ratio. This isn’t necessarily an issue for such a business. However, it becomes a problem if revenue declines significantly, as this would suck in cash. There doesn’t seem to be any risk of this in the short term as they say:

Following the success of FY24, we are confident in achieving results in line with the Board's expectations for FY25.

Their broker, Singer, keep unchanged forecasts with essentially flat revenue for FY25 and FY26. EPS drops to 3.7p for, rising to 40p for FY26. The reasons given are:

FY25 EBITDA forecasts reflect the anticipated loss of a large legacy customer (£3m impact) meanwhile the company’s continued push to drive subscription revenue (instead of perpetual licence deals) may add a further £1.5m revenue/EBITDA headwind, such that - all told - the more relevant/LFL EBITDA comp for FY25 is c.£12m (rather than the £16.7m Tribal achieved).

The lack of growth here may be the reason why the shares are weak today, although this is not new news.

Mark’s view

After all, a 10x P/E doesn’t really stand out in today’s small cap market. However, it is reasonable for this kind of “sticky” software company. (What I hear on the ground is that everyone complains about Tribal’s software, but they still use it as it is the industry standard that everyone knows!). Having beaten for FY24, they may well be being cautious on forecasting, given the economic backdrop. Overall, I find little in these results to explain the sell-off today, so I am maintaining the AMBER/GREEN rating.

Brave Bison (LON:BBSN)

Down 4% to 2.4p - Acquisition - Mark (I hold) - AMBER/GREEN

This is another bolt-on for this digital media and marketing company run by the sons of Michael Green of ITV fame, and backed by some big industry names. Graham liked the last acquisition saying “This deal sounds to me as if it is strategically sound, and I can’t possibly argue that they have overpaid, given how the purchase has been structured.” This time the initial payment amount for “Builtvisible” is similar but the structure is not as good, with only half of follow on payments contingent on performance:

The total cash consideration for the Acquisition is up to £3.0 million, with initial consideration of £1.5 million payable on completion, deferred consideration of £1.0 million payable in tranches over 18 months from completion and contingent consideration of £0.5 million payable subject to performance conditions.

There is an equity component, too. Unlike all their other option, which start at 3p/share, they have had to issue nil-cost options here:

will vest on the third anniversary of completion of the Acquisition in 2028, subject to achievement of performance conditions and continued employment with the Group. The Equity Awards are worth approximately £0.5 million based on the current Brave Bison share price of 2.6 pence.

However, this does tie in key personnel for three years, which is key in people businesses. It no doubt reflects that this is a business that requires less restructuring to be earnings enhancing for the group. Their broker, Cavendish, say:

We leave forecasts unchanged until we receive further information on Builtvisible’s financials and its FY25E trading expectations.

This is in line with a company that has always been very conservative when guiding brokers' forecasts.

Mark’s view

While the Cavendish price target of 4.7p based on peer multiples may be a bit rich, this is a growing, cash-generative company on a very modest rating, especially if one nets out the growing cash balance. It looks too cheap at the current price, despite being a sector I’m generally not a fan of. AMBER/GREEN

Airea (LON:AIEA)

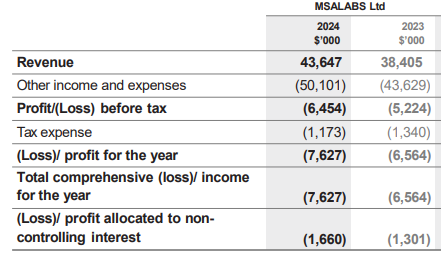

Down 2% to 24.5p - Final Results - Mark - AMBER

By pure coincidence, three of the low P/TBV stocks that feature in the article I wrote this week have reported today. This is one of them.

The results show a stronger second half:

· Strong sales growth of 6.0% in the second half, recovering from 5.6% shortfall in first half

· Full year revenue increased by 0.6% to £21.2m (2023: £21.1m)

· Underlying operating profit of £1.6m, excluding non-recurring costs

· Operating profit before valuation gain decreased to £0.7m (2023: £1.8m), impacted by non-recurring costs of £0.9m

Annoyingly, they are going to make me look up what the change from the previous underlying operating profit was, but if this was good progress, they would surely mention it. I hate it when companies do this, showing the good comparators and not the bad. It is so obvious that they don’t fool anyone! -13% is the answer.

There is an increasing gap to statutory results, explained as:

The non-recurring costs of £0.9m included;

· an increase in labour and production overheads of £0.6m following the strategic review and successful implementation of the Group's stockholding policy

· investment in the new tiling line which resulted in the temporary use of third-party storage at a cost of £0.1m

· legal expenses of £0.1m in defending a trademark challenge

· professional costs of £0.1m associated with investment in intellectual property

I can’t help feeling that most of these need far more explanation than is given. How is a labour and overhead increase a one-off? is the trademark challenge settled? and what is the IP invested in? There doesn’t appear to be any shareholder presentation to put these to management either.

Cash is down significantly from £5.8m to £2.1m, but again, it is net cash that investors really care about, and they make me do my own calculations - £3.9m down to £1.2m. Apart from some working capital movements, the main difference is the £2.2m in their plant. This is a company in transition, and this is how I described it in the P/TBV article:

However, a new management team has been appointed, and they are making some major changes in how the business is being run. Firstly, they have targeted a reduction in working capital and stock in particular. Plus, they are marketing the company’s investment property, valued on the balance sheet at £4.1m. This cash is being invested in significantly increasing production capacity at their facilities. This sort of strategy is not without risks, but assuming they have got their market analysis right, this could see significant growth.

They report some progress on this, saying that:

The investment in our manufacturing facility is nearing completion, and along with the ongoing transformation of the business, the Group is well placed for profitable future growth.

However, I’m just not sure where those extra sales are going to come from. Opening a showroom in Dubai may be one of the steps, but is that really going to completely transform the sales outlook? Inventories are down, but there is no progress on the sale of their investment property. I do wonder if they will be forced to put some of that cash into their pension deficit when it arrives. Net assets are up but by less than the reduction in the pension deficit, which is largely an accounting change.

Mark’s view

If this business transformation is successful and the assets here become productive, then the step change in earnings will make this look very cheap. However, it is hard to see any sign of that in these results and there are may niggles which suggests the shareholder unfriendliness remains despite the change in management. The wise thing to do may be to wait for the initial signs that the news sales strategy is gaining traction before considering any investment. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.